Brief Exercise 5–16

If a seller is purchasing distinct goods or services from a customer at the fair value

of those goods or services, we account for that purchase as a separate transaction.

Otherwise, excess payments by the seller are treated as a refund of the customer’s

purchase. If the payments are made (or are expected to be made) at the time of the

original sale, the transaction price of the customer’s purchase is reduced

immediately by the refund. If payment is not expected at the time of the sale,

Brief Exercise 5–17

Under the adjusted market assessment approach, O’Hara would base its estimate

of the stand-alone selling price of the club-fitting services on the prices charged by

Brief Exercise 5–18

Under the expected cost plus margin approach, O’Hara would base its estimate

Brief Exercise 5–19

Under the residual approach, O’Hara would base its estimate of the stand-alone

Brief Exercise 5–20

The software license is a right of use, since Saar’s activities during the license

period (which for this software does not have an end date) will not affect the value

Intermediate Accounting, 8/e 5–23

Brief Exercise 5–21

Because Carlos had completed training and was open for business on August 1,

2016, TopChop apparently has satisfied its performance obligation with respect to

Brief Exercise 5–22

Brief Exercise 5–23

Brief Exercise 5–24

GoodBuy should not recognize revenue when it sells the $1,000,000 of gift

Brief Exercise 5–25

receivable for the $3,000 until it delivers the furniture to Ramirez.

Brief Exercise 5–26

For long-term contracts, we view a company as having a contract asset if CIP >

Intermediate Accounting, 8/e 5–25

Brief Exercise 5–27

Total estimated cost to complete = $6 million + 9 million = $15 million

% of completion = $6 million $15 million = 40%

Brief Exercise 5–28

Brief Exercise 5–29

No revenue or gross profit recognized until project completed in year 2.

Brief Exercise 5–30

Brief Exercise 5–31

Receivables turnover ratio = Net sales

Average accounts receivable (net)

Intermediate Accounting, 8/e 5–27

Brief Exercise 5–32

Profit margin = Net income

Sales

Shareholders’ equity, beginning of period $500,000

Brief Exercise 5–33

Return on

equity

=

Profit

margin

×

Asset turnover

×

Equity multiplier

Intermediate Accounting, 8/e 5–29

Brief Exercise 5–34

Inventory turnover ratio = Cost of goods sold Average inventory

APPENDIX BRIEF EXERCISES

Brief Exercise 5–35

2016 Gross profit = $3,000,000 – $1,200,000 = $1,800,000

2016 Gross profit percentage = Gross profit Sales:

Brief Exercise 5–36

Brief Exercise 5–37

No gross profit will be recognized in either 2016 or 2017. Gross profit will not

Intermediate Accounting, 8/e 5–31

Brief Exercise 5–38

Year 1:

Revenue: $6 million

Year 2:

Revenue: $14 million ($20 million total – 6 million in year 1)

Brief Exercise 5–39

Orange has separate sales prices for the two parts of LearnIt-Plus, so that

vendor-specific objective evidence (VSOE) allows them to allocate revenue to those

Brief Exercise 5–40

Orange has separate sales prices for the two parts of LearnIt-Plus, so the

company can base its estimates of the fair value of those parts according to their

Brief Exercise 5–41

Specific conditions for revenue recognition of the initial franchise fee are

Intermediate Accounting, 8/e 5–33

EXERCISES

Exercise 5–1

The FASB Accounting Standards Codification® represents the single source of

Requirement 1

Regarding the five steps used to apply the revenue recognition principle, the

appropriate citation is:

Requirement 2

Regarding indicators that control has passed from the seller to the buyer, such

that it is appropriate to recognize revenue at a point in time, the appropriate citation

is:

Requirement 3

Regarding circumstances under which sellers can recognize revenue over time,

the appropriate citation is:

Exercise 5–2

Requirement 1

Ski West should recognize revenue over the ski season. Ski West fulfills its

performance obligation over time as it delivers the service to its pass holders by

providing access to its ski lifts.

Requirement 2

November 6, 2016 To record the cash collection.

December 31, 2016 To recognize revenue earned in December (no

revenue earned in November, as season starts on December 1).

Requirement 3

$90 is included in revenue in Ski West’s 2016 income statement. The $360

Intermediate Accounting, 8/e 5–35

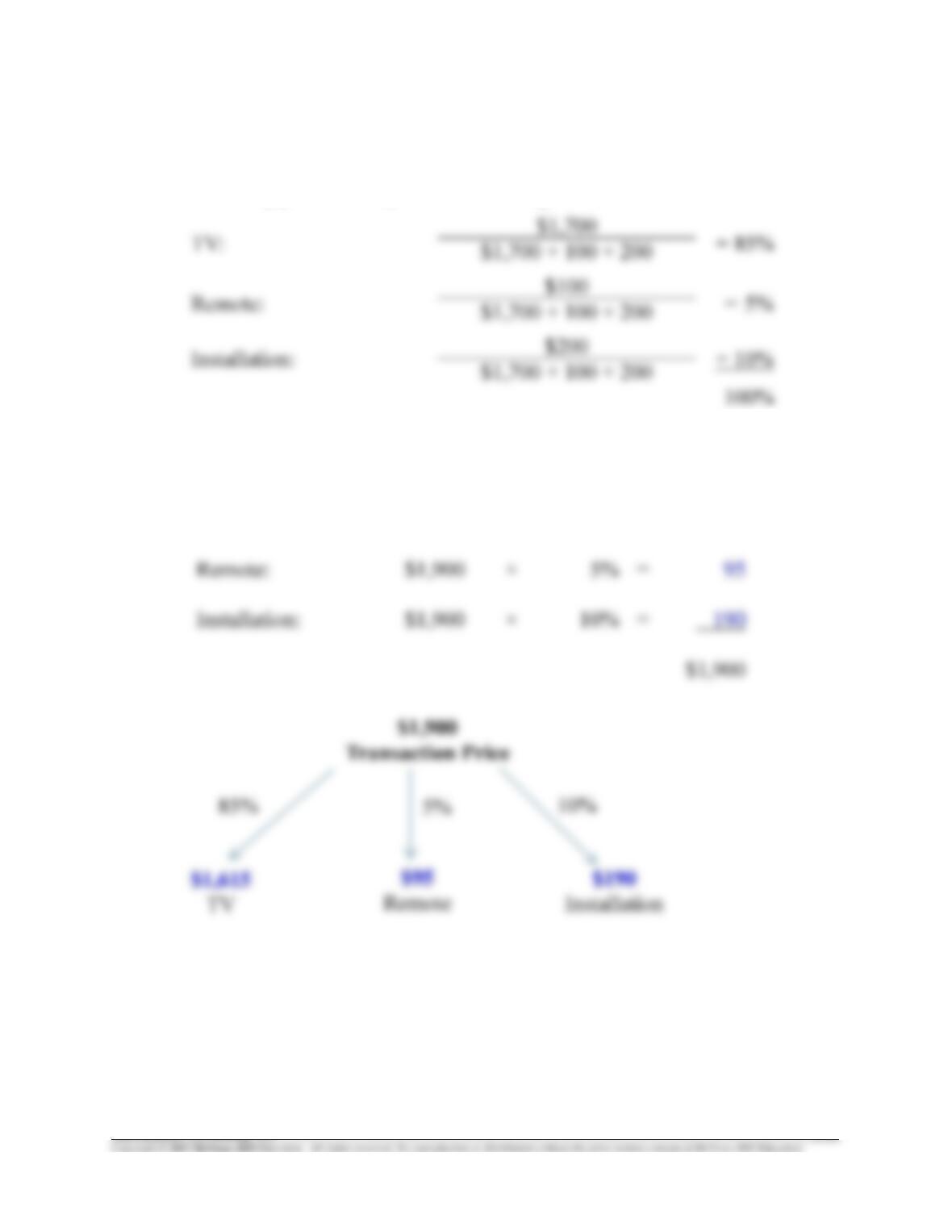

Exercise 5–3

VP first must identify each performance obligation’s share of the sum of the

stand-alone selling prices of all performance obligations:

VP would allocate the total selling price of the package ($1,900) based on stand-

alone selling prices, as follows:

TV:

$1,900

×

85%

=

$1,615

Exercise 5–4

The FASB Accounting Standards Codification® represents the single source of

authoritative U.S. generally accepted accounting principles.

Requirement 1

Regarding the basis upon which a contract’s transaction price allocated to its

Requirement 2

Regarding indicators that a promised good or service is separately identifiable,

the appropriate citation is:

Requirement 3

Regarding circumstances under which an option is viewed as a performance

obligation, the appropriate citation is:

Intermediate Accounting, 8/e 5–37

Exercise 5-5

Requirement 1

Number of performance obligations in the contract: 2.

Requirement 2

Value of the gold bars:

$1,440/unit 100 units = $ 144,000

Exercise 5-5 (concluded)

Gold Examiner then allocates the total selling price based on stand-alone selling

prices, as follows:

Requirement 3

Entry on March 30, 2016:

Requirement 4

Entry on April 1, 2016:

$147,000

Transaction Price

Intermediate Accounting, 8/e 5–39

Exercise 5–6

Requirement 1

Number of performance obligations in the contract: 2.

Requirement 2

If Clarks can’t estimate the stand-alone selling price of SunBoots, it will use the

residual method to calculate that price as the amount of the total transaction price

minus the value of the discount.

Exercise 5–7

Requirement 1

The amount of revenue Manhattan Today should recognize upon receipt of the

subscription fee: $0.

Requirement 2

Number of performance obligations in the contract: 2.