Problem 15-25 (concluded)

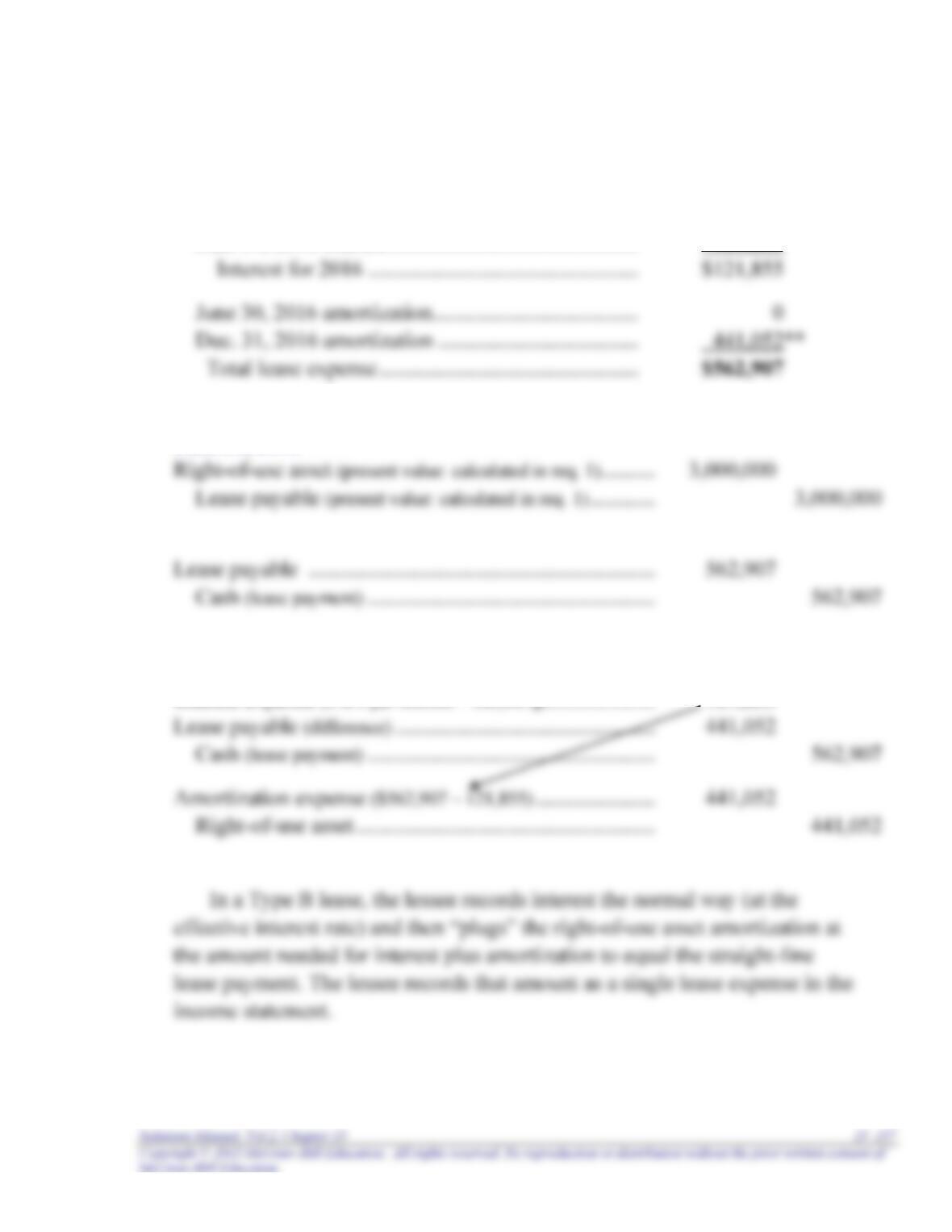

4. Expenses for year ended December 31, 2016

June 30, 2016 interest ………………………………………. $ 0

Dec. 31, 2016 interest ………………………………………. 121,855**

Calculations:

June 30, 2016*

December 31, 2016**

Interest expense (5% x [$3 million – 562,907]) ……………….. 121,855

CASES

Real World Case 15-1

Requirement 1

Note 11: “Financing Arrangements and Lease Obligations” indicates that the

Requirement 2

Note 11 Financing Arrangements and Lease Obligations (in part)

Operating and Capital Leases

(in thousands)

Operating Capital

Leases Leases

2014 $ 325,830 $ 115,340

Case 15-1 (concluded)

If the operating leases were capitalized, the capital lease liability would increase

by approximately a multiple of about 2.7. Note 11 above indicates that future lease

Requirement 3

In general, debt increases risk. Debt places owners in a subordinate position

relative to creditors because the claims of creditors must be satisfied first in case

of liquidation. Also, debt requires payment, usually on specific dates, and failure

to pay interest and principal may result in default and perhaps even bankruptcy.

The debt-to–equity ratio, total liabilities/shareholders’ equity, frequently is

calculated to measure the degree of risk. Other things being equal, the higher the

ratio, the higher the risk. Using numbers from the balance sheet, we see that the

debt to equity ratio for PetSmart is:

15–160 Intermediate Accounting, 8/e

Research Case 15-2

Requirement 1

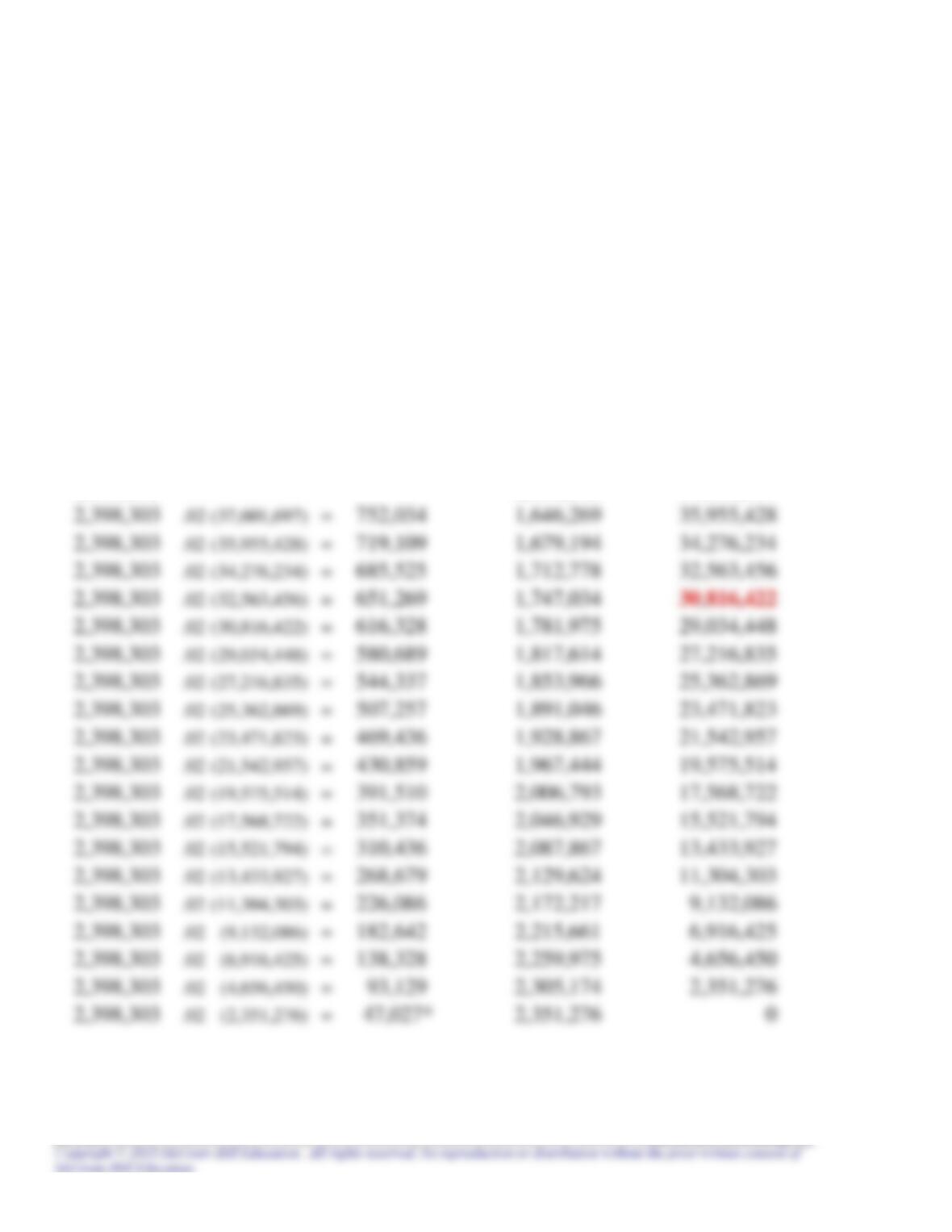

After the first full year under the warehouse lease, the balance in Dowell’s lease

payable is $30,816,422. This is the balance after reductions from the first five

quarterly lease payments as shown in this amortization schedule. (The first

payment was at December 31 of the previous year, the inception of the lease.)

Lease Amortization Schedule

Effective Decrease Outstanding

Payments Interest in Balance Balance

2% x Outstanding Balance

40,000,000

2,398,303 2,398,303 37,601,697

* rounded

Case 15-2 (continued)

Requirement 2

After the first full year under the warehouse lease, the book value (after

accumulated depreciation) of Dowell’s leased warehouses is 32,000,000:

Requirement 3

The specific citation that specifies the guidelines for derecognition of capital leases is

FASB ASC 840–30–40: “Leases–Capital Leases–Derecognition.” Accounting for

lessees is described in paragraphs 40–1 and 2; “Lease Modifications.”

(a) if the proposal to sublease will qualify as a termination of a capital lease:

40–1 A termination of a capital lease before the expiration of the lease term is

15–162 Intermediate Accounting, 8/e

Case 15-2 (concluded)

Requirement 4

In accordance with FASB ASC 840–30–40–1, the asset and obligation representing

the original lease would be removed from the accounts and a loss would be recognized

for the difference. The journal entry Dowell would record in connection with the

sublease is:

Communication Case 15-3

First, this case has no single right answer. The process of developing the

proposed solutions will likely be more beneficial than the solutions themselves.

Students should benefit from participating in the process, interacting first with other

group members, then with the class as a whole.

It is important that each student actively participate in the process. Domination

by one or two individuals should be discouraged. Discussion likely will include the

following:

a. Possible advantages of leasing include:

2. Leasing can provide an interest rate lower than the incremental borrowing

rate.

b. The lessee views a noncancelable lease as a capital lease if it meets at least

one of the following criteria.

1. The lease transfers ownership of the property to the lessee at the end of the

lease term.

15–164 Intermediate Accounting, 8/e

Case 15-3 (continued)

Present value of minimum lease payments, assuming a BPO:

Lease payments ($300,000 x 3.48685) $1,046,055

Otherwise:

Present value of minimum lease payments, assuming the purchase option is

not a BPO:

Lease payments ($300,000 x 3.48685) $1,046,055

Case 15-3 (concluded)

c. VIP would record the following at December 31, 2016:

15–166 Intermediate Accounting, 8/e

Ethics Case 15-4

Discussion should include these elements:

Leasehold improvement depreciation period

There may be some degree of latitude associated with uncertainty concerning

Ethical Dilemma:

How does a doubtful justification for the estimated life of leasehold

Who is affected?

Real World Case 15-5

Requirement 1

Leasing can allow a firm to conserve assets, to avoid some risks of owning assets,

and obtain favorable tax benefits. Also, leasing sometimes is used as a means of “off–

Requirement 2

When capital leases are first recorded, both assets and liabilities increase by the

Requirement 3

($ in millions)

Requirement 4

15–168 Intermediate Accounting, 8/e

Real World Case 15-6

Requirement 1

In a sale-leaseback transaction the owner of an asset sells the asset and

immediately leases it back from the new owner. We view the sale and simultaneous

Requirement 2

When amortizing the deferred gain over the lease term, if the lease meets the

Communication Case 15-7

Suggested Grading Concepts and Grading Scheme:

Content (80%)

30 Sale portion of the sale-leaseback (10 each).

Record cash for the sale price.

Decrease equipment at its undepreciated cost.

Establish a deferred gain for the excess of the sale

price of the equipment over its undepreciated cost.

15 Gain on the sale portion (5 each; maximum 15).

Amortized over the lease term.

As a reduction of depreciation expense.

Results in essentially the same depreciation and interest

as if the asset were not sold and leased back, but

a note is issued for cash instead.

Because the sale and the leaseback are two

components of a single transaction rather than two

independent transactions.

Consistent with the realization principle.

15 Leaseback portion of the sale-leaseback transaction (5 each;

maximum 15).

Both an asset.

And a liability.

At the present value of minimum lease payments.

Excluding any executory costs.

Asset amount cannot exceed fair value.

20 Conceptual basis (10 each).

Economic effect of a long-term capital lease on the

lessee is similar to that of an installment purchase.

Transfers substantially all of the benefits and risks

incident to the ownership of property to the lessee.

80 points

Writing (20%)

5 Terminology and tone appropriate to the audience (CFO).

6 Organization permits ease of understanding.

Introduction that states purpose.

Paragraphs separate main points.

9 English

Word selection.

Spelling.

Grammar.

20 points

Trueblood Case 15-8

15–170 Intermediate Accounting, 8/e

A solution and extensive discussion materials accompany each case in the

IFRS Case 15-9

Requirement 1

The desire to obtain “off-balance-sheet financing” sometimes is a leasing stimulus.

When funds are borrowed to purchase an asset, the liability has a detrimental effect on

Requirement 2

Whether or not there is any real effect on security prices, sometimes off-balance-sheet

Requirement 3

It would be more difficult for SCI to obtain “off-balance-sheet financing” through an

Air France/KLM Case

Requirement 1

In general – yes. More specifically – no.

Requirement 2

At December 31, 2013, AF’s operating lease commitments for aircraft totaled

€5,687 million. Its capital lease commitments for aircraft had a present value that