DOLLAR-VALUE LIFO RETAIL METHOD

➢ Using the LIFO retail method in combination with dollar-

value LIFO is referred to as the dollar-value LIFO retail

method.

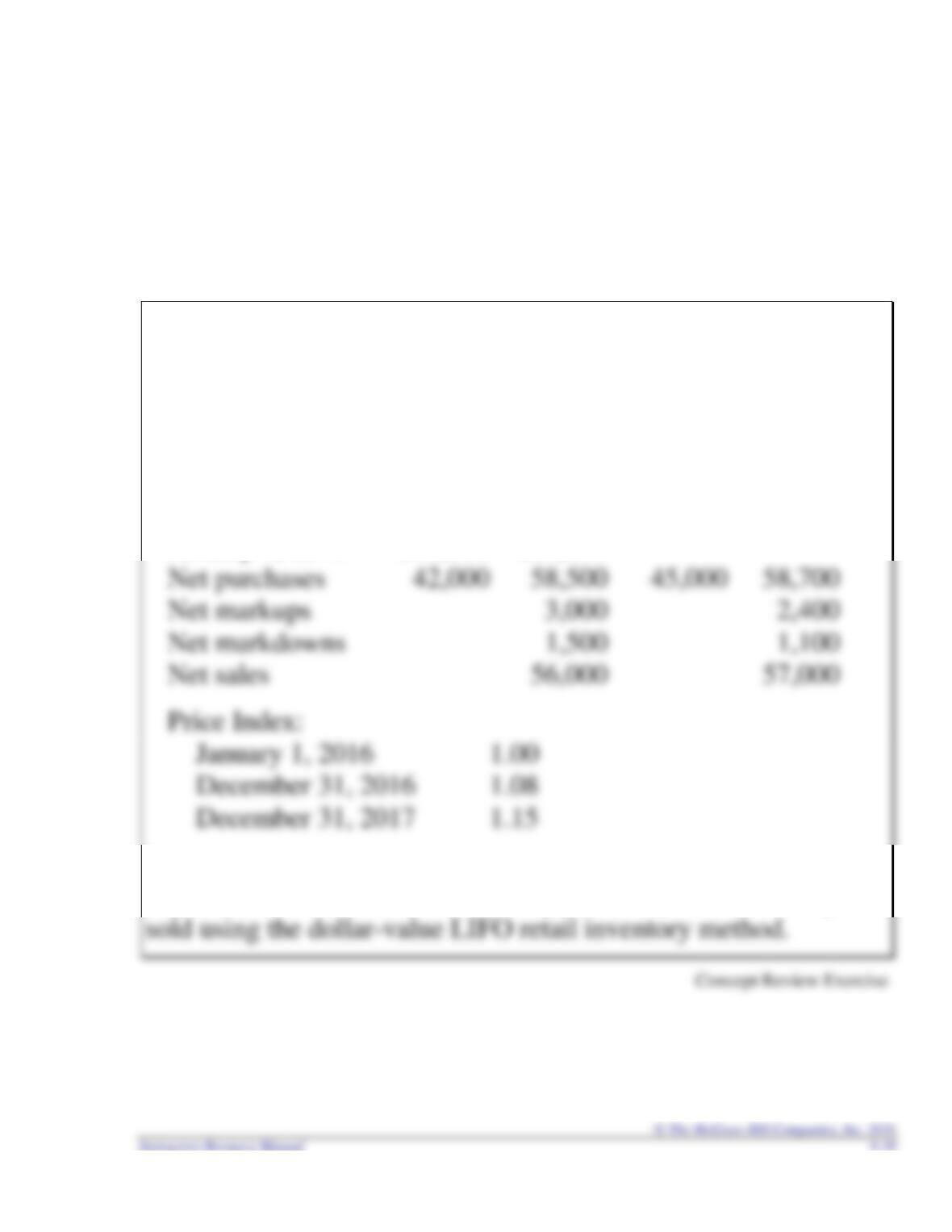

On January 1, 2016, the Nicholson Department Store adopted

the dollar-value LIFO retail inventory method. Inventory

transactions at both cost and retail and cost indexes for 2016 and

2017 are as follows:

2016 2017

Cost Retail Cost Retail

January 1, 2016 $16,000 $24,000

Required:

Estimate the 2016 and 2017 ending inventory and cost of goods

T9–13

9-20 Intermediate Accounting,8/e

DOLLAR-VALUE LIFO RETAIL METHOD

(continued)

2016

2017

Cost

Retail

Cost

Retail

Beginning inventory

$16,000

$24,000

$17,456

$28,000

Plus: Net purchases

42,000

58,500

45,000

58,700

Net markups

Less: Net markdowns

____

____

Goods available for sale (excluding beg. inv.)

42,000

60,000

45,000

60,000

Goods available for sale (including beg. inv.)

58,000

84,000

62,456

88,000

Less: Net sales

Estimated ending inv. at current year retail

$28,000

$31,000

Less: Estimated ending inventory at cost (below)

Base layer $16,000

2016

Step 1 Step 2 Step 3

Ending Ending Inventory Inventory

Inventory Inventory Layers Layers

at Year–end at Base Year at Base Year Converted to

Retail Prices Retail Prices Retail Prices Cost

$28,000

$28,000 = $25,926 $24,000 (base) x 1.00 x 66.67% = $16,000

2017

Step 1 Step 2 Step 3

Ending Ending Inventory Inventory

Inventory Inventory Layers Layers

at Year–end at Base Year at Base Year Converted to

Retail Prices Retail Prices Retail Prices Cost

T9-13(continued)

9-22 Intermediate Accounting,8/e

MOST INVENTORY CHANGES

➢ A change in inventory method, other than a change to LIFO,

is accounted for retrospectively by reporting all previous

periods’ financial statements as if the new inventory method

had been used in all prior periods.

➢ In addition, a disclosure note describes the change and

justification for the change along with the effects of the

change on items not reported on the face of the primary

statements, as well as any per share amounts affected for the

current period and all prior periods presented.

T9–14

MOST INVENTORY CHANGES

(continued)

Disclosure of Change in Inventory Method —

CVS Caremark Corporation

2.Change in Accounting Principle (in part)

Prior to 2012, the Company valued prescription drug inventories on a first-in, first-out

(“FIFO”) basis in retail pharmacies using the retail inventory method and in

distribution centers using the FIFO cost method. Effective January 1, 2012, all

Illustration 9-15

T9-14 (continued)

A CHANGE TO THE LIFO METHOD

➢ Accounting records usually are inadequate for a company

changing to LIFO to calculate the income effect on prior

years.

➢ Instead, the LIFO method simply is used from that point on.

➢ A disclosure note explains (a) the nature of and justification

for the change, (b) the effect of the change on current year’s

income and earnings per share, and (c) why retrospective

application was impracticable.

Change in Inventory Method Disclosure —Seneca Foods Corporation

10. Inventories (in part)

The Company decided to change its inventory valuation method from the FIFO method to

the LIFO method. In the high inflation environment that the Company is experiencing, the

Company believes that the LIFO inventory method is preferable over the FIFO method

because it better compares the cost of current production to current revenue. Selling prices

Illustration 9-16

INVENTORY ERRORS

➢ If a material inventory error is discovered in an accounting

period subsequent to the period in which the error is made,

any previous year’s financial statements that were incorrect as

a result of the error are retrospectively restated to reflect the

correction.

► Incorrect balances are corrected.

► A correction to retained earnings is reported as a prior

period adjustment.

► A disclosure note describes the nature and impact of the

error.

➢ When analyzing inventory errors, it’s helpful to visualize the

ways cost of goods sold, net income, and retained earnings are

determined.

Beginning inventory

Plus: Net purchases

Less: Ending inventory Revenues

Illustration 9-17

T9–16

9-26 Intermediate Accounting,8/e

INVENTORY ERRORS

(continued)

The Barton Company uses a periodic inventory system. At the

end of 2015, a mathematical error caused an $800,000

overstatement of ending inventory. Ending inventories for 2016

and 2017 are correctly determined.

Analysis: U = Understated O = Overstated

2015 2016

Beginning inventory Beginning inventory O

Illustration 9-18

T9-16(continued)

PURCHASE COMMITMENTS

➢ Purchase commitments are contracts that obligate a company to

purchase a specified amount of merchandise or raw materials at

specified prices on or before specified dates.

In July 2016, the Lassiter Company signed two purchase commitments.

Illustration 9A-1

Contract Period within Fiscal Year (the first commitment)

► If market price is equal to or greater than the contract price, the purchase

is recorded at the contract price.

► If market price is less than the contract price, the purchase is recorded at

the market price. Assuming a market price of $425,000, the following

entry records the purchase:

Inventory (market price) ………………………………………. 425,000

T9–17

PURCHASE COMMITMENTS

(continued)

Contract Period Extends beyond Fiscal Year (the second commitment)

► If the market price at year-end is less than the contract price for

outstanding purchase commitments, a loss and a corresponding liability

are recorded for the difference. Assuming a year-end market price for the

second purchase commitment of $540,000, the following adjusting entry is

recorded:

December 31, 2016

Estimated loss on purchase commitment

The Purchase

► If market price on purchase date has not declined from year-end price, the

purchase is recorded at the year-end market price.

Inventory (accounting cost) ………………………………………. 540,000

► If market price on purchase date declines from year-end price, the

purchase is recorded at the market price. Assuming the market price

declines to $510,000, the following adjusting entry records the purchase:

Inventory (market price) …………………………………………… 510,000

Suggestions for Class Activities

1. Research Activity

The Gymboree Corporation is one of the largest children’s apparel specialty retailers in North

America. Have students, individually or in groups, go to Edgar at www.sec.gov. Ask them to:

A. Find their way to the financial statements and notes for the most recent fiscal year.

B. Identify and explain the method(s) used to value inventories.

C. Assume that in the most recent fiscal year the company discovered that last year’s ending

inventory was overvalued by $10 million due to a mathematical error and:

1. Describe the accounting treatment of the error.

2. Determine the effect of the error on income before taxes for the current and prior years.

D. Assume that the company decided to switch its inventory method to FIFO. Explain the

accounting treatment for the change.

Points to note:

In its financial statement for the fiscal year ended February 1, 2014, Gymboree reported that

merchandise inventories are valued using the weighted average cost method.

2. Research Activity

PMX Communities is involved in the development of opportunities within the retail gold sales and

gold mining industries. During its fiscal year ended December 31, 2013, the company recorded an

inventory write-down.

Suggestions:

Have the class access the financial statements of PMX Communities using Edgar at:

1. What was the amount of the inventory write-down?

2. Where was the write-down reported in the income statement?

3. What are the reporting alternatives? Discuss the pros and cons of each alternative.

4. What prompted the write-down?

Points to Note:

In a separate line item in its income statement, the company reported an inventory write-down of

$65,076. Disclosure Note 3 – Inventory, attributed the write-down to gold pricing.

3. Professional Skills Development Activities

9-30 Intermediate Accounting,8/e

The following are suggested assignments from the end-of-chapter material that will help your

students develop their communication, research, analysis and judgment skills.

Communication Skills. In addition to Communication Cases 9-5 and 9-9, Analysis Case 9-6 can

be adapted to ask students to write a memo explaining the required treatment and disclosures.

Research Skills. In their careers, our graduates will be required to locate and extract relevant

information from available resource material to determine the correct accounting practice,

Analysis Skills. The “Broaden Your Perspective” section includes Analysis Cases that direct

students to gather, assemble, organize, process, or interpret data to provide options for making

business and investment decisions. This chapter includes Analysis Cases 9-6 and 9-12 (based

on the appendix).

Judgment Skills. The “Broaden Your Perspective” section includes Judgment Cases that require

students to critically analyze issues to apply concepts learned to business situations in order to

4. Ethical Dilemma

The chapter contains the following ethical dilemma:

ETHICAL DILEMMA

The Hartley Paper Company, owned and operated by Bill Hartley, manufactures and sells different

types of computer paper. The company has reported profits in the majority of years since the

company’s inception in 1972 and is projecting a profit in 2016 of $65,000, down from $96,000 in

2015.

Near the end of 2016, the company is in the process of applying for a bank loan. The loan

proceeds will be used to replace manufacturing equipment necessary to modernize the

manufacturing operation. In preparing the financial statements for the year, the chief accountant,

You may wish to discuss this in class. If so, discussion should include these elements.

Step 1—The Facts:

The Hartley Paper Company has reported profits in prior years, but projects decreased profit for

2016. At the end of 2016 the company applies for a loan to replace equipment and modernize

operations. Approximately $40,000 of the paper inventory has become obsolete and should be

written off in 2016. The owner, Bill Hartley, is considering waiting until 2017 to write down the

inventory so that 2016 income is favorable and the bank will not refuse to provide the loan. Assets

Step 2—The Ethical Issue and the Stakeholders:

The ethical issue or dilemma is whether the chief accountant’s obligation to his employer to

improve the company’s financial position to the bank is greater than his obligation to provide

information that is not misleading to users of the financial statements.

Step 3—Values:

Values include competence, honesty, integrity, objectivity, loyalty to the company, and

responsibility to users of financial statements.

9-32 Intermediate Accounting,8/e

Step 4—Alternatives:

1. Keep the inventory at its current value.

Step 5–Evaluation of Alternatives in Terms of Values:

1. Alternative 1 illustrates loyalty to Hartley and the company.

2. Alternative 2 exhibits values of competence, honesty, integrity, objectivity, and responsibility

Step 6—Consequences:

Alternative 1

Positive consequences: The bank would probably grant the loan, the company would be

modernized and remain competitive, and employees would keep their jobs.

Alternative 2

Positive consequences: Users of financial statements, including the bank, would receive more

relevant and reliable net income and balance sheet figures for 2016. The chief accountant would

maintain his integrity.

Alternative 3

Positive consequences: The chief accountant maintains his integrity and avoids conflict with

Hartley.

Step 7—Decision:

Student(s) must decide their course of action.

Assignment Chart

Learning Est. time

Questions Objective(s) Topic (min.)

9-1

1

Lower of cost and net realizable value

5

9-2

1

Lower of cost and net realizable value

5

9-3

1

Lower of cost and net realizable value

5

9-4

2

Gross profit method

5

9-5

2

Gross profit method

5

9-6

3

Retail inventory method

5

9-7

2,3

Gross profit and retail methods compared

5

9-8

3

Retail terms

5

9-9

3

Retail inventory method; average cost

5

9-10

4

Conventional retail method

5

9-11

3

LIFO retail inventory method

5

9-12

3

Retail inventory method

5

9-13

3,5

Retail method using LIFO compared to DVL

retail

5

9-14

6

Change in inventory method

5

9-15

6

Change in inventory method involving LIFO

5

9-16

7

Inventory errors

5

9-17

7

Inventory errors

5

9-18

8

IFRS; lower of cost and net realizable value

5

9-19

A

Purchase commitments [Based on Appendix]

5

9-20

A

Purchase commitments [Based on Appendix]

5

Brief Learning Est. time

Exercises Objective(s) Topic (min.)

9-1

1

Lower of cost and net realizable value

5

9-2

1

Lower of cost and net realizable value

5

9-3

2

Gross profit method

10

9-4

2

Gross profit method; solving for unknown

10

9-5

3

Retail inventory method; average cost

10

9-6

3

Retail inventory method; LIFO

10

9-7

4

Conventional retail method

10

9-8

4

Conventional retail method

15

9-9

5

Dollar-value LIFO retail

15

9-10

5

Dollar-value LIFO retail

15

9-11

6

Change in inventory costing methods

10

9-12

6

Change in inventory costing methods

10

9-13

7

Inventory error

10

9-14

7

Inventory error

10

Learning Est. time

Exercises Objective(s) Topic (min.)

9-34 Intermediate Accounting,8/e

9-1

1

Lower of cost and net realizable value

15

9-2

1

Lower of cost and net realizable value

15

9-3

1

Lower of cost and net realizable value

15

9-4

3,6,7

FASB codification research

20

9-5

2

Gross profit method

15

9-6

2

Gross profit method

15

9-7

2

Gross profit method

15

9-8

2

Gross profit method

20

9-9

2

Gross profit method; solving for unknown cost %

15

9-10

3

Retail inventory method; average cost

20

9-11

4

Conventional retail method

20

9-12

3

Retail inventory method; LIFO

20

9-13

4

Conventional retail method; normal spoilage

25

9-14

3,4

Conventional retail method; employee discounts

25

9-15

3

Retail inventory method; solving for unknowns

30

9-16

5

Dollar-value LIFO retail

25

9-17

5

Dollar-value LIFO retail

20

9-18

5

Dollar-value LIFO retail

20

9-19

5

Dollar-value LIFO retail; solving for unknowns

35

9-20

6

Change in inventory costing methods

15

9-21

6

Change in inventory costing methods

15

9-22

7

Error correction; inventory error

20

9-23

7

Inventory errors

15

9-24

7

Inventory error

20

9-25

7

Inventory errors

20

9-26

1,2,3,4,5,6,7

Concepts; terminology

15

9-27

A

Purchase commitments [Based on Appendix]

15

9-28

A

Purchase commitments [Based on Appendix]

15

CPA/CMA Learning Est. time

Exam Questions Objective(s) Topic (min.)

CPA-1

1

Lower of cost and net realizable value

3

CPA-2

2

Gross profit method

3

CPA-3

4

Conventional retail method

3

CPA-4

7

Inventory errors

3

CPA-5

8

IFRS

3

CMA-1

4

Conventional retail method

3

CMA-2

7

Inventory errors

3

CMA-3

7

Inventory errors

3

Learning Est. time

Problems Objective(s) Topic (min.)

9-1

1

Lower of cost and net realizable value

20

9-2

1

Lower of cost and net realizable value

20

9-3

2

Gross profit method

20

9-4

3,4

Retail inventory method; various cost methods

35

9-5

3,4

Retail inventory method; conventional and LIFO

35

9-6

4

Retail inventory method; conventional

25

9-7

3,4

Retail method; average cost and conventional

20

9-8

5

Dollar-value LIFO retail method

20

9-9

5

Dollar-value LIFO retail method

20

9-10

3,4,5

Retail inventory method; various applications

45

9-11

3,4,5

Retail inventory method; various applications

45

9-12

6

Change in methods

25

9-13

7

Inventory errors

25

9-14

7

Inventory errors

25

9-15

7

Integrating problem, Chapters 8 and 9; inventory

errors

40

9-16

A

Purchase commitments [Based on Appendix]

25

Star Problems

Learning Est. time

Cases Objective(s) Topic (min.)

Judgment Case 9-1

1,3,4

Inventoriable costs; lower of cost and net

realizable value; retail inventory method

25

Communication Case 9-2

1

Lower of cost and net realizable value

20

Integrating Case 9-3

1

Unit LIFO and lower of cost and net realizable

value

25

Judgment Case 9-4

3,4

The dollar-value LIFO method; the retail

inventory method

15

Communication Case 9-5

3,4

Retail inventory method

45

Analysis Case 9-6

6

Change in inventory method

35

Real World Case 9-7

6

Change in inventory method; Abercrombie &

Fitch

20

Real World Case 9-8

1,5,6

Various inventory issues; Chapters 8 and 9;

Fred’s Inc.

45

Communication Case 9-9

6

Change in inventory method; note disclosure

30

Judgment Case 9-10

7

Inventory errors

20

Ethics Case 9-11

7

Overstatement of ending inventory

30

Analysis Case 9-12

A

Purchase commitments [Based on Appendix]

20

Air France-KLM Case

8

IFRS; lower of cost and net realizable value;

Air France-KLM

10