Problem 14–6 (continued)

December 31, 2016 (Western)

Interest expense ($1,200,000 + 80,000) …………………. 1,280,000

Discount on bonds payable ($20,000 x 4 months) 80,000

14–82 Intermediate Accounting, 8/e

Problem 14–6 (continued)

December 31, 2017 (Stillworth)

Interest receivable ($30,000 x 12% x 4/12)…………… 1,200

Discount on bond investment ($20 x 4 months) ….. 80

Problem 14–6 (concluded)

February 28, 2019 (Western)

Interest expense ($1,800,000 + 40,000 – 1,200,000) . 640,000

Interest payable (from adjusting entry) ………………. 1,200,000

Problem 14–7

Requirement 1

Interest $16,000,000¥ x 17.15909 * = $274,545,440

Principal $400,000,000 x 0.14205 ** = 56,820,000

Problem 14–8

1. Interest expense for year ended December 31, 2016

Dec. 31, 2016, interest expense (calculated below 1) . $4,422

2. Liabilities at December 31, 2016

Bonds payable (face amount) ………………………………. $500,000

14–86 Intermediate Accounting, 8/e

Problem 14–8 (concluded)

Calculations:

November 1, 2016

Cash (price: given) …………………………………… 442,215

Discount on bonds payable (difference) ……… 57,785 2

Problem 14–9

Requirement 1

Cash (price given) ………………………………………….. 5,795,518

Discount on bonds payable (difference) …………… 12,204,482

14–88 Intermediate Accounting, 8/e

Problem 14–10

Requirement 1

Land ………………………………………………………………….. 600,000

Notes payable (face amount) ………………………………… 600,000

Problem 14–10 (concluded)

Not required, but recorded at the same date (may be combined with interest

entry):

Notes payable (face amount) …………………………………… 100,000

Cash ………………………………………………………………. 100,000

14–90 Intermediate Accounting, 8/e

Problem 14–11

Requirement 1

Interest $ 6,000 x 3.79079 * = $ 22,745

Principal $150,000 x 0.62092 ** = 93,138

Present value (price) of the note $115,883

Problem 14–12

Requirement 1

$6,074,700 ÷ $2,000,000 = 3.03735

present installment present value

value payment table amount

Problem 14–13

Requirement 1

Interest $5,000¥ x 3.16987 * = $15,849

Principal $100,000 x 0.68301 ** = 68,301

Present value (price) of the note $84,150

¥ 5% x $100,000

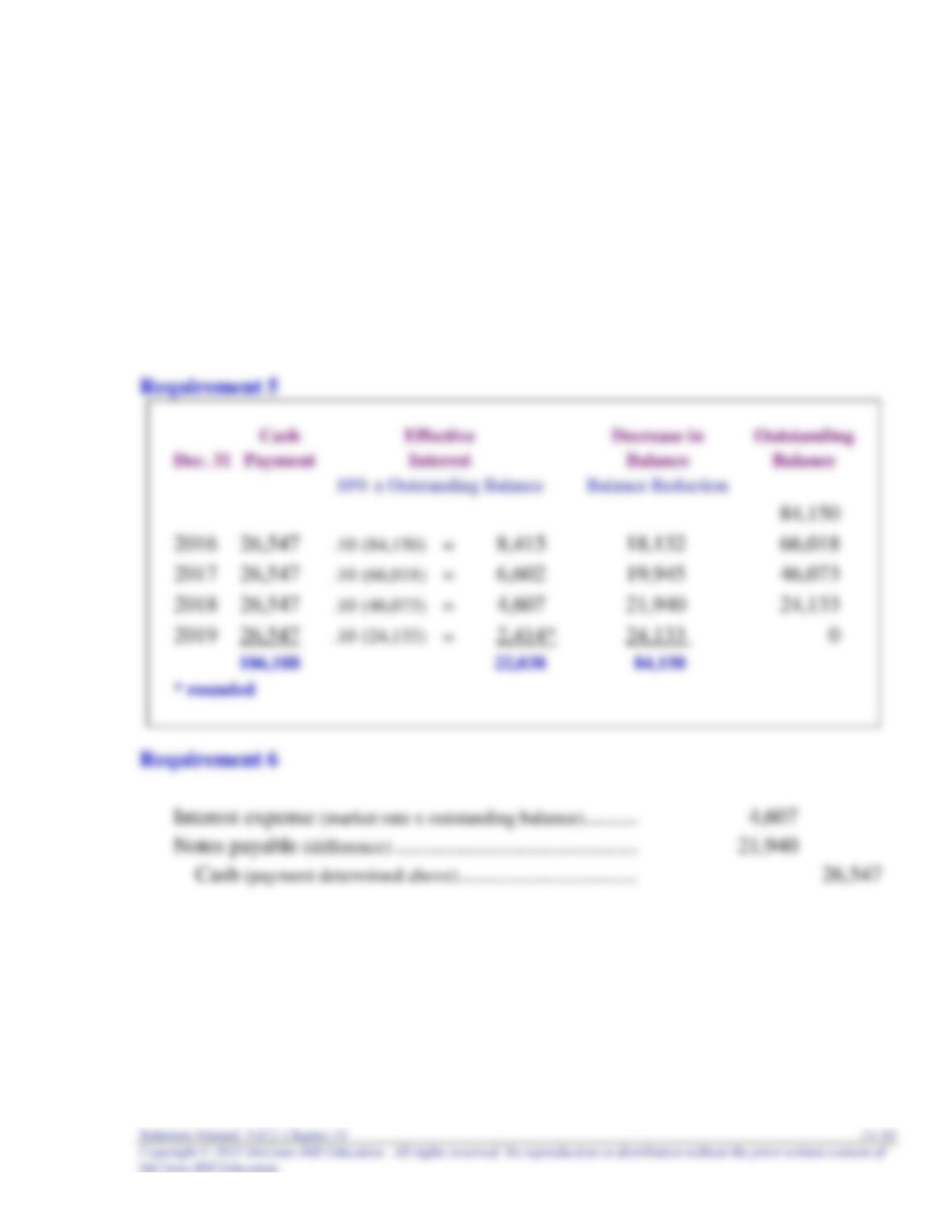

Problem 14–13 (concluded)

Requirement 4

$84,150 ÷ 3.16987 = $26,547

amount (from Table 4) installment

of loan n = 4, i = 10% payment

14–94 Intermediate Accounting, 8/e

Problem 14–14

Bonds payable (face amount) …………………………………… 800,000

Loss on early extinguishment (to balance) ………………… 13,100

Problem 14–15

Requirement 1

Interest expense (7% x $19,000,000) ………………………………. 1,330,000

Problem 14–16

1. Issuance of the bonds.

Cash ($385,000 – 1,500) ………………………………………….. 383,500

2. December 31, 2016

Interest expense ($20,000 + 750) ……………………………………. 20,750

3. June 30, 2017

Interest expense ($20,000 + 750) ……………………………………. 20,750

4. Call of the bonds

Bonds payable (face amount) ………………………………….. 400,000

14–96 Intermediate Accounting, 8/e

Problem 14-17

Under IFRS, transaction costs reduce the recorded amount of the debt, as well as the net

cash the issuing company receives from the sale of the bonds. A lower [net] amount is

borrowed at the same cost, increasing the effective interest rate. Since the recorded amount

of the debt is reduced by the transaction costs, the higher rate will be reflected in a higher

recorded interest expense.

1. Issuance of the bonds

Cash ($385,000 – 1,500)…………………………………………… 383,500

2. December 31, 2016

3. June 30, 2017

4. Call of the bonds

Bonds payable ($383,500 + 825 +825) ……………………….. 385,150

Problem 14–18

Requirement 1

Bonds payable (face amount) ………………………………….. 20,000,000

Problem 14–19

Requirement 1

($ in millions)

Convertible Bonds—2003 issue

Cash (97.5% x $200 million) ……………………………………………….. 195

Requirement 2

($ in millions)

Convertible bonds payable (90% x $200 million) …………………. 180

Problem 14–19 (concluded)

Requirement 4

($ in millions)

Convertible bonds payable (90% x $200 million) ………………….. 180.0

14–100 Intermediate Accounting, 8/e

Problem 14–20

Requirement 1

Microsoft’s note states that the company issued $1.25 billion of zero-coupon

.

Requirement 2

($ in millions)

Cash (proceeds given in Note 12) ……………………………. 1,240

Debt issue costs (to balance) ………………………………… 1