C

CH

HA

AP

PT

TE

ER

R

1

13

3

C

Cu

ur

rr

re

en

nt

t

L

Li

ia

ab

bi

il

li

it

ti

ie

es

s

a

an

nd

d

C

Co

on

nt

ti

in

ng

ge

en

nc

ci

ie

es

s

Overview

With the discussion of investments in the previous chapter we concluded our six-chapter coverage

of assets that began in Chapter 7 with cash and receivables. This is the first of six chapters devoted

to liabilities. Here, we focus on short-term liabilities. Bonds and long-term notes are discussed in

the next chapter. Obligations relating to leases, income taxes, pensions, and other postretirement

benefits are the subjects of the following four chapters. In Part A of this chapter, we discuss open

accounts and notes, accrued liabilities, and other liabilities that are classified appropriately as

current. In Part B we turn our attention to situations in which there is uncertainty as to whether an

obligation really exists. These are designated as loss contingencies.

Learning Objectives

13-1. Define liabilities and distinguish between current and long-term liabilities.

13-2. Account for the issuance and payment of various forms of notes and record the interest on the

notes.

13-3. Characterize accrued liabilities and liabilities from advance collection, and describe when and

how they should be recorded.

13-4. Determine when a liability can be classified as a noncurrent obligation.

13-5. Identify situations that constitute contingencies and the circumstances under which they should

be accrued.

13-6. Demonstrate the appropriate accounting treatment for contingencies, including unasserted

claims and assessments.

13-7. Discuss the primary differences between U.S. GAAP and IFRS with respect to current

liabilities and contingencies.

L

Le

ec

ct

tu

ur

re

e

O

Ou

ut

tl

li

in

ne

e

Part A: Current Liabilities

I. Characteristics of Liabilities (T13-1)

A. Most liabilities obligate the debtor to pay cash at specified times and result from legally

enforceable agreements.

B. Some liabilities are not contractual obligations and may not be payable in cash.

C. A liability is a present obligation to sacrifice assets in the future because of something that

already has occurred.

II. What is a Current Liability? (T13-2)

A. Classifying liabilities as either current or long-term helps investors and creditors assess the

relative risk of a business’s liabilities.

B. Current liabilities are expected to require current assets and usually are payable within one

year.

C. Current liabilities ordinarily are reported at their maturity amounts. (T13-3)

1. Practical expediency

2. Conceptually, liabilities should be recorded at their present values.

3. Relatively short time to maturity

16-2 Intermediate Accounting, 8/e

III. Accounts Payable and Notes

A. Open accounts and notes

1. Accounts payable – Buying merchandise on account in the ordinary course of business

creates accounts payable

2. Trade notes payable – Formally recognized by a written promissory note; sometimes

bear interest

B. Short-term notes payable

1. Line of credit – allows a company to borrow cash without having to follow formal loan

procedures and paperwork

3. Noninterest-bearing notes – interest is “discounted” from the face amount of a note;

the effective interest rate is higher than the stated discount rate (T13-5)

4. Secured loans – a specified asset (often inventory or accounts receivable) is pledged as

collateral or security for the loan

C. Commercial paper (Exercise 13-3)

2. Lower rate than through a bank loan

3. Unsecured notes sold in minimum denominations of $25,000

4. Maturities ranging from 30 to 270 days

6. Usually backed by a line of credit

7. Recording its issuance and payment exactly the same as forms of notes payable

IV. Accrued Liabilities (T13-6)

A. Represent expenses already incurred, but for which cash has yet to be paid (accrued

expenses)

B. Recorded by adjusting entries at the end of the reporting period

C. Common examples: salaries and wages payable, income taxes payable, and interest

payable (T13-7)

D. An employer accrues an expense and related liability for employees’ compensation for

future absences such as vacation pay if the obligation meets four conditions:

2. The paid absence can be taken in a later year – the benefit vests (will be

compensated even if employment is terminated) or the benefit can be accumulated

over time.

3. Payment is probable.

V. Liabilities from Advance Collection

A. Deposits and advances from customers (T13-8)

1. Collecting cash from a customer as a refundable deposit creates a liability to return the

deposit

2. Collecting cash from a customer as an advance payment for products or services

creates a deferred revenue liability that converts to revenue when the seller satisfies its

performance obligation to deliver products or services.

B. Gift cards are a common example of advanced collection. Record deferred revenue

liability when sell the card, and then reduce it and recognize revenue if the gift card is

redeemed or the probability of redemption is viewed as remote.

C. Collections for third parties

2. Payroll-related deductions such as withholding taxes, social security taxes, employee

insurance, employee contributions to retirement plans, and union dues [discussed in

the Appendix]

VI. A Closer Look at the Current and Noncurrent Classification

A. Current maturities of long-term debt (Exercise 13-10)

1. The currently maturing portion of a long-term debt must be reported as a current

liability.

2. Long-term liabilities that are due on demand – by terms of the contract or violation of

contract covenants – must be reported as current liabilities.

B. Short-term obligations can be reported as noncurrent liabilities if the company:

2. Demonstrates the ability to do so by a refinancing agreement or by actual financing.

(T13-9)

3. Under U.S. GAAP, liabilities payable within the coming year are classified as long–

term liabilities if refinancing is completed before date of issuance of the financial

statements. Under IFRS, refinancing must be completed before the balance sheet date.

The FASB is considering an exposure draft proposing the IFRS method. (T13-10)

Part B: Contingencies

I. Loss Contingencies (T13-11)

A. Involves an existing uncertainty as to whether a loss really exists, where the uncertainty

will be resolved only when some future event occurs

B. Accrued only if a loss is

2. The amount can reasonably be estimated. (T13-12)

C. The contingent liability for product warranties almost always is accrued. (Exercise 13-13)

D. The contingent liability for premiums (like cash rebates) almost always is accrued. (T13-

13)

E. When the cause of a loss contingency occurs before the year-end, a clarifying event before

financial statements are issued can be used to determine how the contingency is reported.

(T13-14)

II. Unasserted Claims and Assessments (T13-15)

A. It must be probable that an unasserted claim or assessment or an unfiled lawsuit will occur

before considering whether and how to report the possible loss.

16-4 Intermediate Accounting, 8/e

1. Is a claim or assessment probable? {If not, no disclosure is needed.}

B. If the conclusion of step 1 is that the claim or assessment is not probable, no further action

is required.

III. Gain Contingencies (T13-16)

A. Gain contingencies are not accrued.

B. Conservatism

IV. IFRS (T13-17) Several important differences:

A. IFRS refers to accrued liabilities as “provisions,” and refers to possible obligations that are

not accrued as “contingent liabilities.” The term “contingent liabilities” is used for all of

these obligations in U.S. GAAP.

B. IFRS requires disclosure (but not accrual) of two types of contingent liabilities: (1)

possible obligations whose existence will be confirmed by some uncertain future events

that the company does not control, and (2) a present obligation for which either it is not

C. IFRS defines “probable” as “more likely than not” (greater than 50%), which is a lower

threshold than typically associated with “probable” in U.S. GAAP.

D. If a liability is accrued, IFRS measures the liability as the best estimate of the expenditure

required to settle the present obligation. If there is a range of equally likely outcomes,

IFRS would use the midpoint of the range, while U.S. GAAP requires use of the low end

of the range.

E. If the effect of the time value of money is material, IFRS requires the liability to be stated

at present value. U.S. GAAP allows using present values under some circumstances, but

liabilities for loss contingencies like litigation typically are not discounted for time value

of money.

F. IFRS recognizes provisions and contingencies for “onerous” contracts, defined as those in

which the unavoidable costs of meeting the obligations exceed the expected benefits.

V. Decision-Makers’ Perspective (T13-18)

A. Liabilities impact a company’s liquidity.

B. Liquidity refers to a company’s cash position and overall ability to obtain cash in the

normal course of business.

C. Critical that managers as well as outside investors and creditors maintain close scrutiny of

a company’s liquidity

D. The current ratio is a measure of short-term solvency.

1. Determined by dividing current assets by current liabilities

2. Should be evaluated in the context of the industry in which the company operates and

other specific circumstances

E. Outside analysts as well as managers should actively monitor risk management activities.

P

Po

ow

we

er

rP

Po

oi

in

nt

t

S

Sl

li

id

de

es

s

A PowerPoint presentation of the chapter is available in the Connect library.

T

Te

ea

ac

ch

hi

in

ng

g

T

Tr

ra

an

ns

sp

pa

ar

re

en

nc

cy

y

M

Ma

as

st

te

er

rs

s

The following can be reproduced on transparency film as they appear here, or you can

16-6 Intermediate Accounting, 8/e

CHARACTERISTICS OF LIABILITIES

Most liabilities obligate the debtor to pay cash at specified

times and result from legally enforceable agreements.

Some liabilities are not contractual obligations and may not

be payable in cash.

A liability has three essential characteristics. Liabilities:

2. that arise from present obligations (to transfer goods or

provide services) to other entities

➢ Notice that the definition of a liability involves the present, the

WHAT IS A CURRENT LIABILITY?

Classifying liabilities as either current or long-term helps

investors and creditors assess the relative risk of a company’s

liabilities.

Generally, current liabilities are payable within one year.

Formally, current liabilities are expected to require current

assets (or create current liabilities).

T13-2

16-8 Intermediate Accounting, 8/e

CURRENT LIABILITIES

General Mills, Inc.

Balance Sheet ($ in millions)

May 26, 2013 and May 27, 2012

Assets

[by classification]

Liabilities

CURRENT LIABILITIES: 2013 2012

Accounts payable $1,423.2 $1,148.9

LONG–TERM LIABILITIES:

[listed individually]

Shareholders’ equity

[by source]

Illustration 13–1

T13-3

8: Debt

Notes Payable. The components of notes payable and their

respective weighted average interest rates at the end of the period

are as follows:

2013 2012

Weighted Weighted

Dollars in millions: Average Average

Note Interest Note Interest

Payable Rate Payable Rate

U.S. commercial paper $ 515.5 0.2% $ 412.0 0.2%

To ensure availability of funds, we maintain bank credit lines

sufficient to cover our outstanding short-term borrowings.

Commercial paper is a continuing source of short-term

financing. We have commercial paper programs available to us in

Illustration 13–1 (continued)

T13-3 (continued)

16-10 Intermediate Accounting, 8/e

NOTE ISSUED FOR CASH

Interest on notes is calculated as:

FACE AMOUNT x ANNUAL RATE x TIME TO MATURITY

On May 1, Affiliated Technologies, Inc., a consumer electronics

firm, borrowed $700,000 cash from First BancCorp under a

noncommitted short-term line of credit arrangement and issued a

6-month, 12% promissory note. Interest was payable at maturity.

May 1

Cash ……………………………………………… 700,000

Illustration 13-3

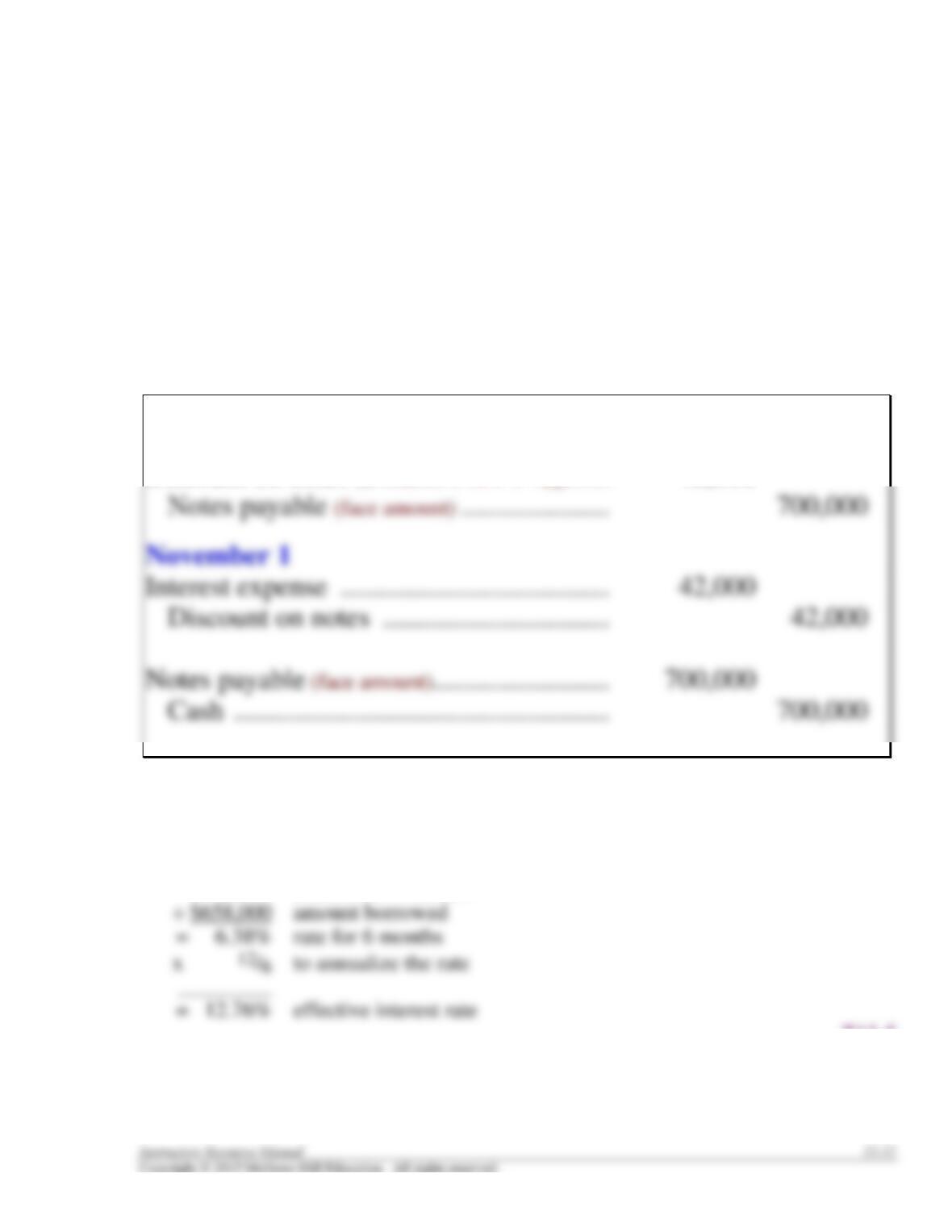

Noninterest-Bearing Note

The proceeds of the note are reduced by the interest in a

“noninterest–bearing” note.

Situation: $700,000 noninterest-bearing note, with a 12%

“discount rate.” The $42,000 interest is “discounted” at the

outset, rather than explicitly stated:

May 1

Cash (difference) …………………………………… 658,000

Discount on notes ($700,000 x 12% x 6/12)…….. 42,000

The amount borrowed is only $658,000, but the interest is calculated as the discount

rate times the $700,000 face amount. This causes the effective interest rate to be

higher than the 12% stated rate:

$ 42,000 interest for 6 months

T13-5

16-12 Intermediate Accounting, 8/e

ACCRUED LIABILITIES

ACCRUED INTEREST PAYABLE

Assume the fiscal period for Affiliated Technologies ends on

June 30, two months after the 6-month note is issued. The

issuance of the note, intervening adjusting entry, and note

payment would be recorded as shown below:

Issuance of note May 1

Cash ……………………………………………….. 700,000

Note payable ………………………………….. 700,000

Illustration 13-6

T13-7

16-14 Intermediate Accounting, 8/e

Customer Advance

A customer advance produces an obligation that is satisfied

when the product or service is provided.

Tomorrow Publications collects magazine subscriptions from

customers at the time subscriptions are sold. Subscription

revenue is recognized over the term of the subscription.

($ in millions)

When Advance is Collected

Cash …………………………………………………….. 20

Illustration 13-10

T13-8

Short-Term Obligations

Expected to Be Refinanced

Short-term obligations can be reported as noncurrent

liabilities only if the company:

(a) intends to refinance on a long-term basis and

(b) demonstrates the ability to do so

T13-9

16-16 Intermediate Accounting, 8/e

INTERNATIONAL FINANCIAL REPORTING STANDARDS

T13-10

LOSS CONTINGENCIES

A loss contingency involves an existing uncertainty as to

whether a loss really exists, where the uncertainty will be

resolved only when some future event occurs.

A liability is accrued if it is both(a) probable that the

confirming event will occur and (b) the amount can be at least

reasonably estimated:

Loss (or expense) …………………. x,xxx

Liability ………………………….. x,xxx

➢ Some loss contingencies don’t involve liabilities at all. Some

contingencies when resolved cause a noncash asset to be

impaired, so accruing it means reducing the related asset rather

than recording a liability (e.g. accounts receivable).

T13-11

16-18 Intermediate Accounting, 8/e

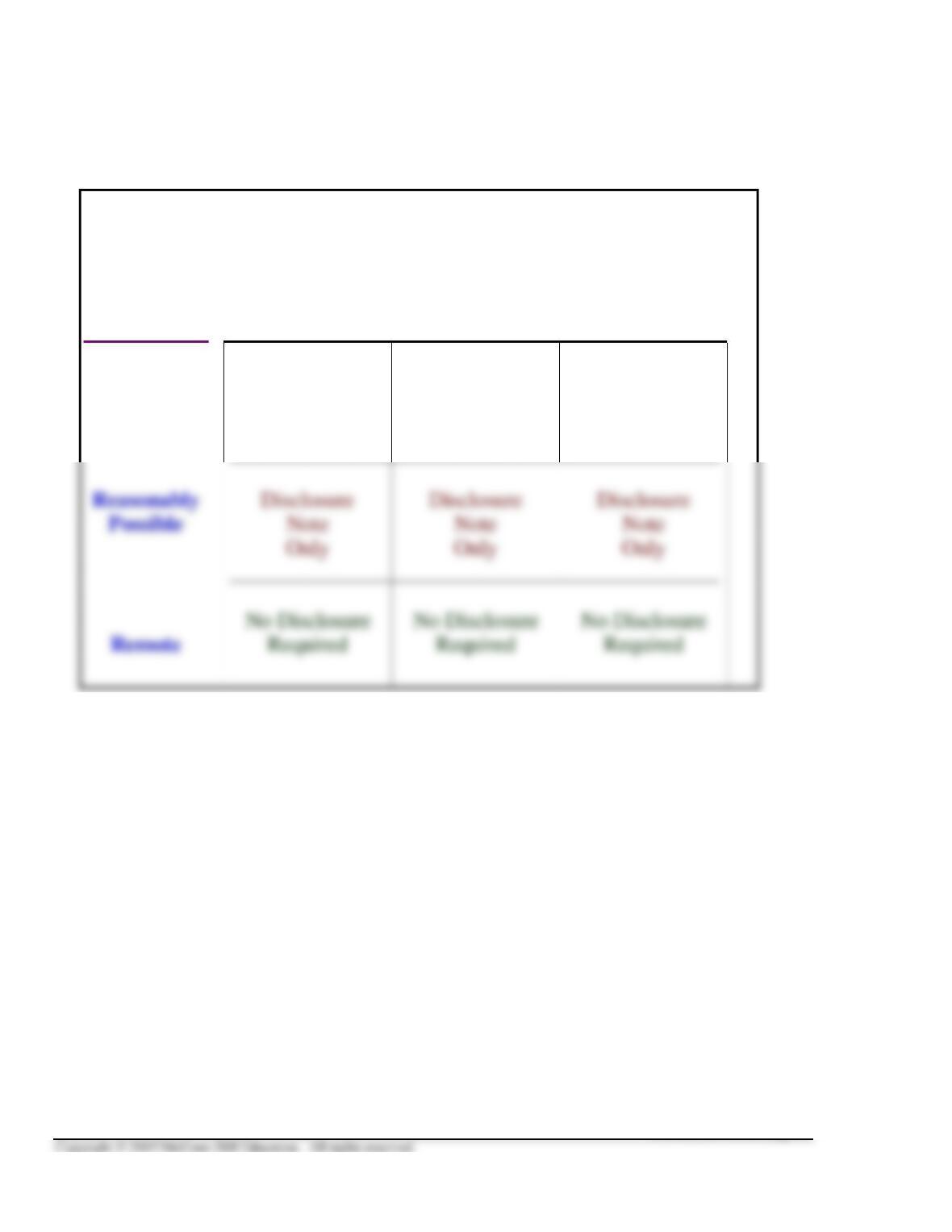

ACCOUNTING TREATMENT OF LOSS CONTINGENCIES

DOLLAR AMOUNT OF POTENTIAL LOSS

________________________________

Reasonably Not Reasonably

Known Estimable Estimable

LIKELIHOOD

Liability Liability Disclosure

Probable Accrued Accrued Note

& Disclosure Note & Disclosure Note Only

_____________________________________________

Illustration 13-16

T13-12