Question 4–1

Question 4–2

Income from continuing operations includes the revenue, expense, gain, and loss

Question 4–3

Question 4–4

The single-step format first lists all revenues and gains included in income from

continuing operations to arrive at total revenues and gains. All expenses and losses

Chapter 4 The Income Statement, Comprehensive Income, and

the Statement of Cash Flows

QUESTIONS FOR REVIEW OF KEY TOPICS

4–2 Intermediate Accounting, 8/e

Question 4–5

The term earnings quality refers to the ability of reported earnings (income) to

Question 4–6

Question 4–7

The process of intraperiod tax allocation matches tax expense or tax benefit with

Question 4–8

The net-of-tax income effects of a discontinued operation must be disclosed

separately in the income statement, below income from continuing operations. The

Question 4–9

GAAP permit alternative treatments for similar transactions. Common examples

are the choice among FIFO, LIFO, and average cost for the measurement of inventory

and the choice among alternative revenue recognition methods. A change in

accounting principle occurs when a company changes from one generally accepted

treatment to another.

Question 4–10

A change in accounting estimate is accounted for in the year of the change and in

subsequent periods; prior years’ financial statements are not restated. A disclosure

4–4 Intermediate Accounting, 8/e

Answers to Questions (continued)

Question 4–11

Prior period adjustments are accounted for by restating prior years’ financial

Question 4–12

Earnings per share (EPS) is the amount of income achieved during a period for

Question 4–13

Comprehensive income is the total change in equity for a reporting period other

Question 4–14

The purpose of the statement of cash flows is to provide information about the

Answers to Questions (continued)

Question 4–15

The three categories of cash flows reported on the statement of cash flows are:

1. Operating activities—Inflows and outflows of cash related to the transactions

entering into the determination of net income from operations.

Question 4–16

Noncash investing and financing activities are transactions that do not increase or

decrease cash but are important investing and financing activities. An example would

Question 4–17

The direct method of reporting cash flows from operating activities presents the

4–6 Intermediate Accounting, 8/e

Answers to Questions (concluded)

Question 4–18

These perspectives are referred to as the discrete and integral part approaches.

Current interim reporting requirements and existing practice generally view interim

Question 4–19

U.S. GAAP designates cash outflows for interest payments and cash inflows

Question 4–20

U.S. GAAP views interim reports as an integral part of the annual report, so

Brief Exercise 4–1

PACIFIC SCIENTIFIC CORPORATION

Income Statement

For the Year Ended December 31, 2016

($ in millions)

Revenues and gains:

Sales ………………………………………………………..

Gain on sale of investments ………………………..

Expenses and losses:

Cost of goods sold ……………………………………..

$1,240

Selling ………………………………………………………

126

General and administrative ………………………….

105

Interest ………………………………………………………

BRIEF EXERCISES

4–8 Intermediate Accounting, 8/e

Brief Exercise 4–2

(a) Sales revenue $2,106

Brief Exercise 4–3

PACIFIC SCIENTIFIC CORPORATION

Income Statement

For the Year Ended December 31, 2016

($ in millions)

Sales revenue ………………………………………………

$2,106

Cost of goods sold ……………………………………….

Gross profit …………………………………………………

Selling ………………………………………………………

Operating income ………………………………………..

Other income (expense):

Gain on sale of investments ………………………..

45

Interest expense …………………………………………

Income before income taxes ………………………….

Income tax expense* ……………………………………

Net income ………………………………………………….

4–10 Intermediate Accounting, 8/e

Brief Exercise 4–4

(a) Sales revenue $300,000

Less: Cost of goods sold (160,000)

(b) Operating income $25,000

(c)

Income before income taxes $ 7,000

Brief Exercise 4–5

WHITE AND SONS, INC.

Partial Income Statement

For the Year Ended December 31, 2016

Income from continuing operations before income taxes …

$ 850,000

Income tax expense* ………………………………………………….

340,000

Income from continuing operations ………………………………

Net income …………………………………………………………………

Earnings per share:

Income from continuing operations ……………………………….

Loss on discontinued operations ………………………………….

Net income ………………………………………………………………..

4–12 Intermediate Accounting, 8/e

Brief Exercise 4–6

CALIFORNIA MICROTECH CORPORATION

Partial Income Statement

For the Year Ended December 31, 2016

Income from continuing operations before income taxes …

$ 5,800,000

Income tax expense* …………………………………………………..

1,740,000

Income from continuing operations ……………………………..

Discontinued operations:

Loss on discontinued operations …………………………………..

Net income …………………………..……………………………………

* $5,800,000 x 30%

** Loss from operations of discontinued component:

Gain on sale of assets $ 2,000,000 ($10 million less $8 million)

Brief Exercise 4–7

CALIFORNIA MICROTECH CORPORATION

Partial Income Statement

For the Year Ended December 31, 2016

Income from continuing operations before income taxes …

$ 5,800,000

Income from continuing operations ………………………………

Discontinued operations:

Loss on discontinued operations …………………………………..

Net income …………………………………………………………………

4–14 Intermediate Accounting, 8/e

Brief Exercise 4–8

CALIFORNIA MICROTECH CORPORATION

Partial Income Statement

For the Year Ended December 31, 2016

Income from continuing operations before income taxes …

$ 5,800,000

Income tax expense* …………………………………………………..

Income from continuing operations ……………………………..

Discontinued operations:

Loss on discontinued operations …………………………………..

Net income …………………………..……………………………………

** Loss from operations of discontinued component:

Impairment loss ($8 million book value less

$7 million net fair value) $(1,000,000)

Brief Exercise 4–9

O’REILLY BEVERAGE COMPANY

Statement of Comprehensive Income

For the Year Ended December 31, 2016

Net income ………………………………………………….

$650,000

Other comprehensive income (loss):

Total other comprehensive loss ……………………..

Comprehensive income ………………………………..

4–16 Intermediate Accounting, 8/e

Brief Exercise 4–10

Cash flows from operating activities:

Collections from customers $ 660,000

Only these four cash flow transactions relate to operating activities. The others are

Brief Exercise 4–11

Cash flows from investing activities:

Proceeds from note receivable collection $100,000

Cash flows from financing activities:

Issuance of common stock $200,000

Brief Exercise 4–12

Cash flows from operating activities:

Net income $45,000

Adjustments for noncash effects:

Brief Exercise 4–13

Under IFRS, interest received and interest paid usually are classified as investing

Cash flows from operating activities:

Collections from customers $ 660,000

Cash flows from investing activities:

Proceeds from note receivable collection $100,000

Cash flows from financing activities:

Issuance of common stock $200,000

4–18 Intermediate Accounting, 8/e

Exercise 4–1

Sales revenue $12,500,000

Less operating expenses:

Cost of goods sold $6,200,000

Note: Interest revenue, loss on sale of investments, and interest expense are all

EXERCISES

Exercise 4–2

Requirement 1

GREEN STAR CORPORATION

Income Statement

For the Year Ended December 31, 2016

Revenues and gains:

Sales ………………………………………………………..

$1,300,000

Interest ……………………………………………………..

Expenses and losses:

Cost of goods sold ……………………………………..

$720,000

Selling ………………………………………………………

General and administrative ………………………….

Income before income taxes ………………………….

Income tax expense …………………………..…………

4–20 Intermediate Accounting, 8/e

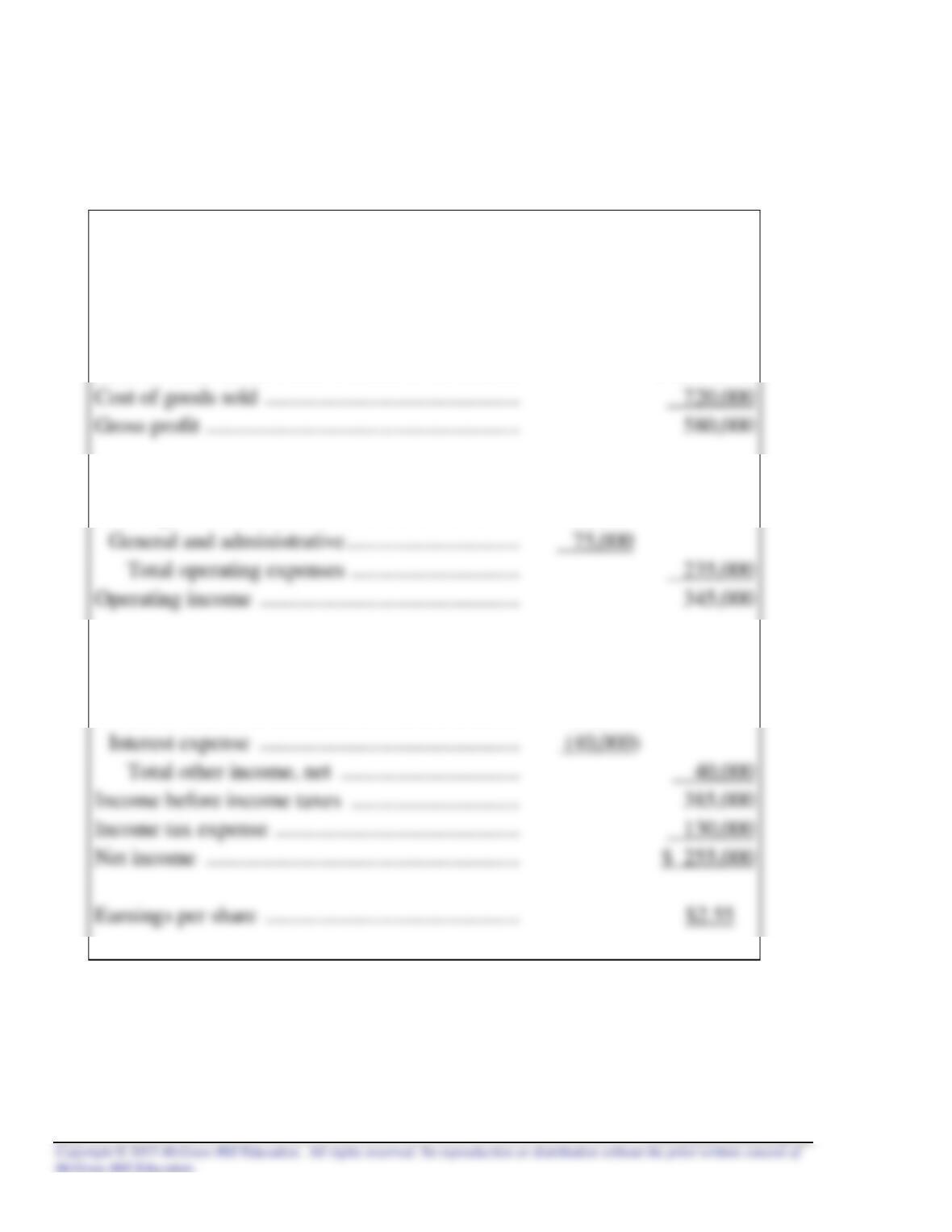

Exercise 4–2 (concluded)

Requirement 2

GREEN STAR CORPORATION

Income Statement

For the Year Ended December 31, 2016

Sales revenue ……………………………………………….

$1,300,000

Cost of goods sold ………………………………………..

Gross profit ………………………………………………….

Operating expenses:

Selling ……………………………………………………….

$160,000

Operating income …………………………..…………….

Other income (expense):

Interest revenue ………………………………………….

30,000

Gain on sale of investments …………………………

50,000

Income before income taxes ………………………….

Income tax expense …………………………..………….

Net income …………………………..……………………..