Chapter 8 Inventories: Measurement

121. Bettencourt Clothing Corporation uses a periodic inventory system and the LIFO cost method.

The company began 2016 with the following inventory layers (listed in chronological order of

acquisition):

5,000 units @ $10 $50,000

8,000 units @ $12 96,000

Beginning inventory $146,000

During 2016, 20,000 units were purchased for $15 per unit. Sales for the year totaled 30,000

units at various prices, leaving 3,000 units in ending inventory.

Required:

1. Calculate cost of goods sold for 2016.

2. Determine the amount of LIFO liquidation profit that the company must report in a

disclosure note to its 2016 financial statements, assuming the amount is material. Assume

an income tax rate of 40%.

Answer:

122. The Foxworthy Corporation uses a periodic inventory system and the LIFO inventory cost

method for its one product. Beginning inventory of 40,000 units consisted of the following,

listed in chronological order of acquisition:

24,000 units at a cost of $6.00 per unit = $144,000

16,000 units at a cost of $7.00 per unit = 112,000

During 2016, inventory quantity declined by 18,000 units. All units purchased during 2016

cost $8.00 per unit.

Required:

Calculate the before-tax LIFO liquidation profit or loss that the company would report in a

disclosure note assuming the amount determined is material.

Chapter 8 Inventories: Measurement

123. Modern Day Appliances, Inc. is a wholesaler of kitchen appliances. The company uses a

periodic inventory system and the LIFO cost method. Modern Day’s December 31, 2016,

fiscal year-end inventory of its main product, double-door stainless steel refrigerators,

consisted of the following (listed in chronological order of acquisition):

Units Unit cost

100 $750

200 800

300 850

The replacement cost of the refrigerators throughout 2017 was $900. Modern Day sold 5,000

of these refrigerators during 2017. The company’s selling price throughout 2017 was $1,200.

Required:

1. Compute the gross profit (sales minus cost of goods sold) and the gross profit ratio for

2017 assuming that Modern Day purchased 5,200 units during the year.

2. Repeat requirement 1 assuming that Modern Day purchased only 4,500 units.

3. For requirements 1 and 2, what amount of before-tax LIFO liquidation profit or loss

would Modern Day report in its 2017 disclosure notes, if any, assuming any calculated

amount is material?

Chapter 8 Inventories: Measurement

124. Selected financial statement data from Western Colorado Stores is shown below.

2016

2015

Net sales

$625,000

$690,000

Cost of goods sold

500,000

490,000

Operating expenses

105,000

85,000

Inventory

90,000

70,000

Required:

1. Compute the gross profit ratio for 2016.

2. Compute the inventory turnover ratio for 2016.

Answer:

Net sales

Cost of goods sold

Gross profit

125. The inventories disclosure note in the 2014 financial statements for SUPERVALU Inc., one of

the largest grocery chains in the United States, included the following ($ in millions):

“Inventories are valued at the lower of cost or market. Substantially all of the Company’s

inventory consists of finished goods. As of February 22, 2014 and February 23, 2013,

approximately 57 percent and 60 percent, respectively, of the Company’s inventories were

valued under the LIFO method. If the FIFO method had been used to determine cost of

inventories for which the LIFO method is used, the Company’s inventories would have been

higher by approximately $202 and $211 as of February 22, 2014 and February 23, 2013,

respectively.”

Cost of goods sold for the fiscal year ended February 22, 2014 was $14,623 million.

Chapter 8 Inventories: Measurement

Required:

If SUPERVALU had used FIFO for all of its LIFO inventories, what would its cost of goods

sold have been for 2014?

126. The following information comes from the 2013 Occidental Petroleum Corporation annual

report to shareholders:

NOTE 4 INVENTORIES

Net carrying values of inventories valued under the LIFO method were approximately $205

million and $185 million at December 31, 2013 and 2012, respectively. Inventories consisted

of the following: ($ in millions)

2013

2012

Raw materials

$ 74

$ 70

Materials and supplies

628

612

Finished goods

589

763

1,291

1,445

LIFO reserve

(91)

(101)

Total

$1,200

$1,344

The LIFO reserve indicates that inventories would have been $91 million and 101 million

higher at the end of 2013 and 2012, respectively, if Occidental Petroleum had used FIFO to

value its entire inventory.

Required:

If Occidental Petroleum had used FIFO to value its entire inventory how would its 2013 pre-

tax income be affected?

Chapter 8 Inventories: Measurement

Use the following to answer questions 127 and 128:

The inventories disclosure note in the 2014 financial statements for SUPERVALU Inc., one of the

largest grocery chains in the United States, included the following:

“During fiscal 2014, 2013 and 2012, inventory quantities in certain LIFO layers were reduced. These

reductions resulted in a liquidation of LIFO inventory quantities carried at lower costs prevailing in

prior years as compared with the cost of fiscal 2014, 2013 and 2012 purchases. As a result, Cost of

sales decreased by $14, $6 and $9 in fiscal 2014, 2013 and 2012, respectively. All inventories are

stated at the lower of cost or current market values. Cost for inventories at the majority of our

operations is determined on a last-in, first-out (“LIFO”) basis.”

Required:

127. The disclosure note indicates an inventory liquidation during 2014, 2013, and 2012. By how

much did net income in 2014 increase due to the liquidation? Assume an income tax of 40%.

128. What additional income tax payments did the 2014 liquidation cost SUPERVALU?

129. Spando Apparel uses the LIFO inventory method for external reporting and for income

tax purposes but maintains its internal records using FIFO. The following disclosure

note was included in a recent annual report:

Chapter 8 Inventories: Measurement

Inventories ($ in millions):

2016 2015

Total inventories $625 $604

LIFO reserve (83) (51)

$542 $ 553

The company’s income statement reported cost of goods sold of $3,120 million for the

fiscal year ended December 31, 2016.

Required:

1. Spando adjusts the LIFO reserve at the end of its fiscal year. Prepare the

December 31, 2016, adjusting entry to record the cost of goods sold adjustment.

2. If Spando had used FIFO to value its inventories, what would cost of goods sold

have been for the 2016 fiscal year?

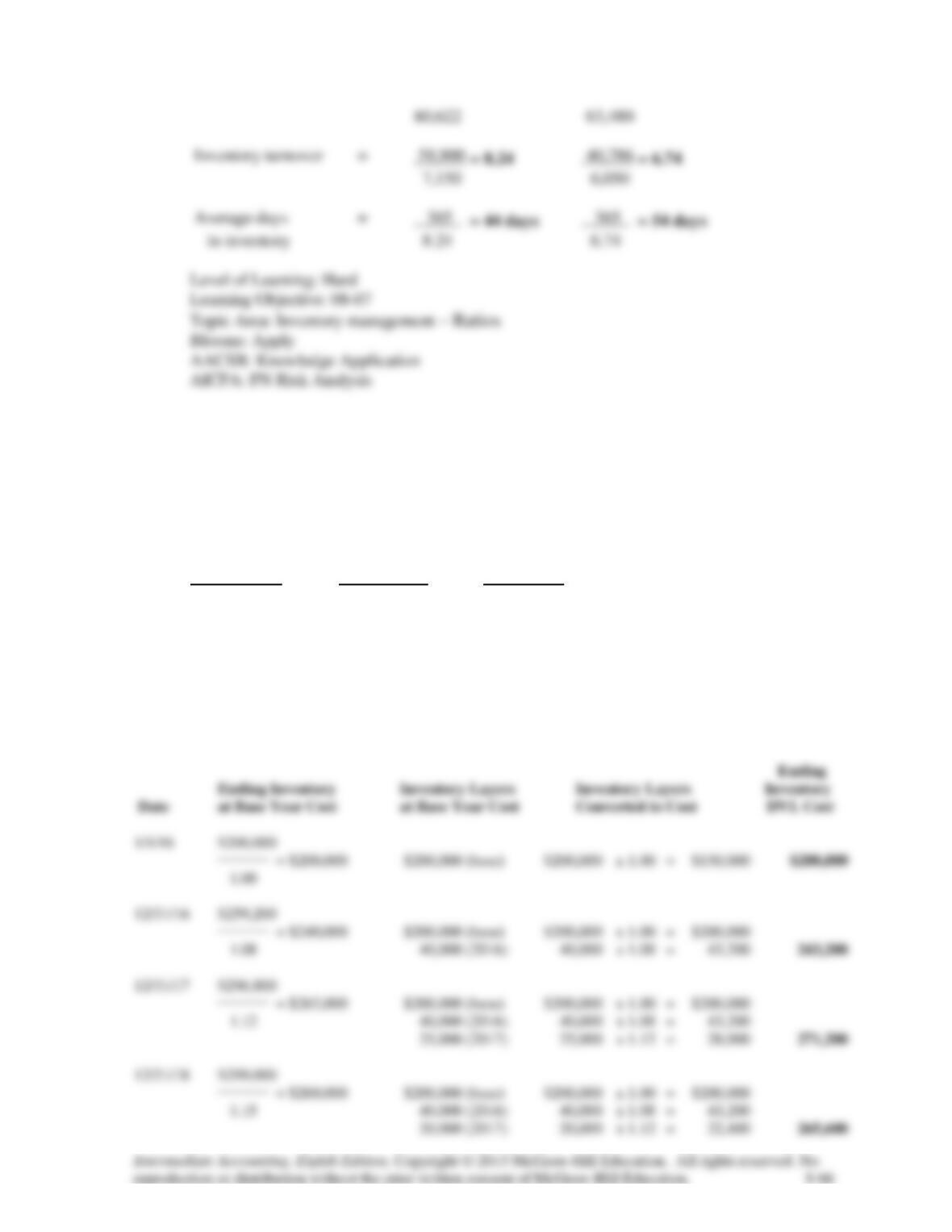

130. The table below contains selected financial information from recent financial statements of

KBI Toys and Little Tikes Adventure Toys, Inc., two toy manufacturing companies ($ in

thousands):

KBI Toys Little Tikes

12/31/16 12/31/15 12/31/16 12/31/15

Net sales $80,622 $72,120 $63,480 $68,900

Cost of goods sold 58,900 53,800 40,786 46,325

Year-end inventory 7,400 6,900 5,800 6,300

Required:

Calculate the 2016 gross profit ratio, inventory turnover ratio, and the average days in

inventory for the two companies (rounded).

Chapter 8 Inventories: Measurement

131. On January 1, 2016, the National Furniture Company adopted the dollar-value LIFO method

of computing inventory. An internal cost index is used to convert ending inventory to base

year. Inventory on January 1 was $200,000. Year-end inventories at year-end costs and cost

indexes for its one inventory pool were as follows:

Inventory at Cost Index

Year Ended Year-end (Relative to

December 31 Costs Base Year)

2016 $259,200 1.08

2017 296,800 1.12

2018 299,000 1.15

Required:

Compute inventory amounts at the end of each year.

Answer:

Chapter 8 Inventories: Measurement

132. Appleton Inc. adopted dollar-value LIFO on January 1, 2016, when the inventory value was

$1,200,000. The December 31, 2016, ending inventory at year-end costs was $1,430,000 and

the cost index for the year is 1.1.

Required:

Compute the dollar-value LIFO inventory valuation for the December 31, 2016, inventory.

133. Chavez Inc. adopted dollar-value LIFO on January 1, 2016, when the inventory value was

$850,000. The December 31, 2016, ending inventory at year-end cost was $950,000 and the

cost index for the year is 1.08.

Required:

Compute the dollar-value LIFO inventory valuation (rounded) for the December 31, 2016,

inventory.

134. Liquidated Corporation had a dollar-value LIFO (DVL) inventory of $800,000 at the

beginning of the current year when it adopted DVL. Its year-end inventory at year-end prices

was $850,000. The index for the current year was 1.08.

Required:

Compute the DVL inventory (rounded) to be reported at the end of the year.

135. On January 1, 2015, ECT Co. adopted the dollar-value LIFO method for its one inventory

pool. The pool’s value on this date was $600 million. The 2015 and 2016 ending inventory

valued at year-end costs were $702 million and $840 million, respectively. The appropriate

cost indexes are 1.08 for 2015 and 1.20 for 2016.

Required:

Calculate the inventory balance that ECT Co. would report on its year-end balance sheets for

2015 and 2016, using the dollar-value LIFO method.

Chapter 8 Inventories: Measurement

136. On January 1, 2015, RAY Co. adopted the dollar-value LIFO method for its one inventory

pool. The pool’s value on this date was $300 million. The 12/31/15 inventory valued at year-

end costs was $385 million. The 12/31/15 inventory, using dollar-value LIFO was $355

million.

Required:

Calculate 2015 cost index for RAY’s inventory.

Chapter 8 Inventories: Measurement

137. The Genworth Company adopted the dollar-value LIFO method on January 1, 2016 when the

inventory value of its one inventory pool was $450,000. The company decided to use an

external index, the Consumer Price Index (CPI), to adjust for changes in the cost level. On

January 1, 2016, the CPI was 280. On December 31, 2016, inventory valued at year-end cost

was $504,000 and the CPI was 294.

Required:

Calculate the inventory value at the end of 2016 using the dollar-value LIFO method.

Answer:

Chapter 8 Inventories: Measurement

Chapter 8 Inventories: Measurement

Essay

Instructions:

The following answers point out the key phrases that should appear in students’ answers. They are not

intended to be examples of complete student responses. It might be helpful to provide detailed

instructions to students on how brief or in-depth you want their answers to be.

138. Briefly describe why companies that use perpetual inventory systems must still perform

physical inventories.

139. It is the end of the accounting period, and your boss asks you to help determine the inventory

balance to place in the company’s balance sheet. Explain which physical quantities of

inventory that you will include and which you will exclude.

140. Briefly explain when there would be a tax benefit from electing LIFO rather than FIFO.

Chapter 8 Inventories: Measurement

141. Briefly explain how companies that use LIFO can both increase and decrease reported

earnings by “managing” ending inventories.

142. Costs and prices regularly fall every year in the microcomputer industry. Briefly indicate your

recommendation and rationale for an inventory method for a firm about to enter this industry.

Chapter 8 Inventories: Measurement

Chapter 8 Inventories: Measurement

143. Carmen Inc., producer of high-tech boating equipment, disclosed the following information in

its 2016 annual report to shareholders:

Inventories are valued at the lower of cost or net realizable value with cost determined by the

last-in, first-out (LIFO) method for inventories.

Inventories at May 31 were as follows:

(Dollars in thousands)

2016

2015

Raw materials and work in process

$ 70,458

$ 66,175

Finished goods

207,231

168,135

Total inventories

$277,689

$234,310

If the inventory had been valued using the first-in, first-out

(FIFO) method, inventories would have been higher by

$22,200 and $24,400 ($ in thousands) at the end of 2016 and

2015, respectively.

How does the supplemental LIFO information indicating what the value of ending inventory

would have been if measured using FIFO improve the quality of financial reporting by

Carmen?

144. Briefly explain the advantages of dollar-value LIFO (DVL).

Chapter 8 Inventories: Measurement