Exercise 4–21 (concluded)

TIGER ENTERPRISES

Statement of Cash Flows

For the Year Ended December 31, 2016

($ in thousands)

Cash flows from operating activities:

Collections from customers $ 7,080

Prepayment of insurance (130)

4–42 Intermediate Accounting, 8/e

Exercise 4–22

Requirement 1

Requirement 2

The specific citation that describes the additional information for earnings per

Requirement 3

For each period for which an income statement is presented, an entity discloses

all of the following:

a. A reconciliation of the numerators and the denominators of the basic and diluted

Exercise 4–22 (concluded)

For the latest period for which an income statement is presented, an entity must

provide a description of any transaction that occurs after the end of the most recent

Exercise 4–23

1. The calculation of the weighted average number of shares for basic

earnings per share purposes:

FASB ASC 260–10–55–2: “Earnings per Share–Overall–Implementation

Exercise 4–23 (continued)

2. The alternative formats permissible for reporting comprehensive income:

FASB ASC 220–10–45–1: “Comprehensive Income–Overall–Other

Presentation Items–Reporting Comprehensive Income.”

1A. An entity reporting comprehensive income in a single continuous financial

statement shall present its components in two sections, net income and other

comprehensive income. If applicable, an entity shall present the following in

that financial statement:

4–46 Intermediate Accounting, 8/e

3. The classifications of cash flows required in the statement of cash flows:

FASB ASC 230–10–45–1: “Statement of Cash Flows–Overall–Other

Presentation Matters–Form and Content.”

Exercise 4–24

List A List B

f 1. Intraperiod tax allocation a. An other comprehensive income item.

4–48 Intermediate Accounting, 8/e

Exercise 4–25

Quarter

First Second Third

Cumulative income before taxes $50,000 $90,000 $190,000

Exercise 4–26

Exercise 4–27

Quarters Ending

March 31 June 30 Sept. 30 Dec. 31

Advertising $200,000 $200,000 $200,000 $200,000

Exercise 4–28

Quarters Ending

March 31 June 30 Sept. 30 Dec. 31

Advertising $800,000 $ – 0 – $ – 0 – $ – 0 –

4–50 Intermediate Accounting, 8/e

CPA / CMA REVIEW QUESTIONS

CPA Exam Questions

2. d. Other than sales, COGS, and administrative expenses, only the gain or loss

3. a. In a single-step income statement, revenues include sales as well as other

revenues and gains.

Sales revenue $187,000

4. a. The $400,000 impairment loss and the $1,000,000 loss from operations

should be combined for a total loss of $1,400,000.

CMA Exam Questions

2. c. The operating section of a retailer’s income statement includes all

revenues and costs necessary for the operation of the retail establishment, for

4–52 Intermediate Accounting, 8/e

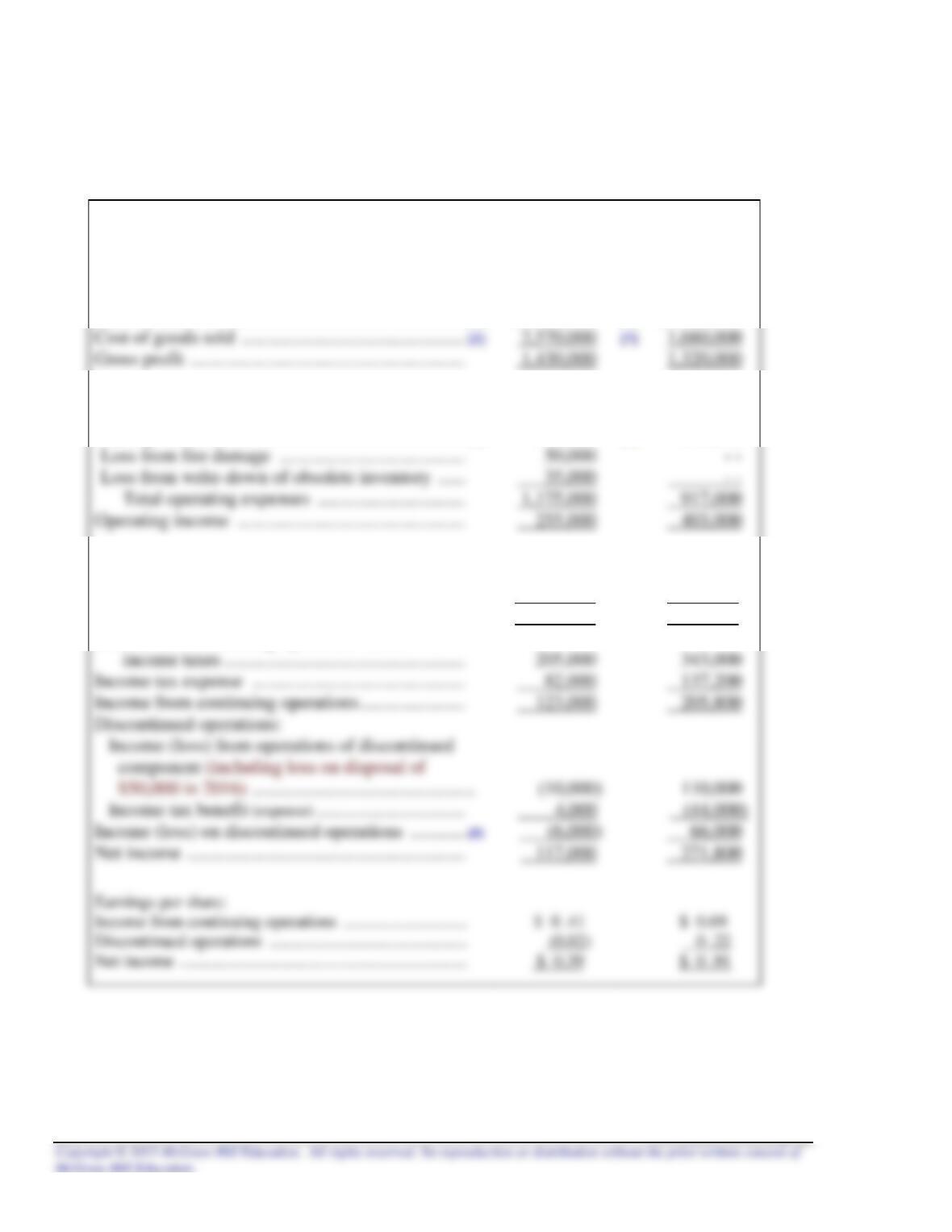

Problem 4–1

REED COMPANY

Comparative Income Statements

For the Years Ended December 31

2016

2015

Sales revenue ……………………………………………….. [1]

$4,000,000

[6] $3,000,000

Cost of goods sold ………………………………………… [2]

2,570,000

[7] 1,680,000

Gross profit …………………………………………………..

1,430,000

Operating expenses:

Administrative ……………………………………………. [3]

750,000

[8] 635,000

Selling ………………………………………………………. [4]

340,000

[9] 282,000

Loss from fire damage ………………………………….

Loss from write-down of obsolete inventory ……

Total operating expenses …………………………..

1,175,000

Operating income ………………………………………….

255,000

Other income (expense):

Interest revenue ……………………………………………

150,000

140,000

Interest expense ……………………………………………

(200,000)

(200,000)

Total other expenses (net) …………………………

(50,000)

(60,000)

Income tax expense ……………………………………….

82,000

Income from continuing operations …………………..

123,000

Discontinued operations:

Income tax benefit (expense) …………………………..

Income (loss) on discontinued operations ………… [5]

Net income ……………………………………………………

117,000

Income from continuing operations before

PROBLEMS

Problem 4–1 (concluded)

[1] $4,400,000 – 400,000

4–54 Intermediate Accounting, 8/e

Problem 4–2

Requirement 1

JACKSON HOLDING COMPANY

Comparative Income Statements (in part)

For the Years Ended December 31

2016

2015

Income from continuing operations before

income taxes [1] ……………………………………

$3,000,000

$1,300,000

Income tax expense …………………………………..

1,200,000

520,000

Income from continuing operations …………….

1,800,000

780,000

Discontinued operations:

Income tax benefit (expense) …………………….

Income (loss) on discontinued operations …….

120,000

Net Income ………………………………………………

$ 600,000

[1] Income from continuing operations before income taxes:

2016 2015

Unadjusted $2,600,000 $1,000,000

[2] Income from discontinued operations:

2016 2015

Loss from operations $(400,000) $(300,000)

Problem 4–2 (concluded)

Requirement 2

The 2016 income from discontinued operations would include only the loss from

Requirement 3

The 2016 income from discontinued operations would include the loss from

4–56 Intermediate Accounting, 8/e

Problem 4–3

MICRON CORPORATION

Partial Income Statement

For the Year Ended December 31, 2016

Income from continuing operations before

income taxes ……………………………………..

[1] $1,300,000

Income tax expense ………………………………

390,000

Discontinued operations:

Loss on discontinued operations …………….

Net income ………………………………………….

[1] Income from continuing operations before taxes:

Unadjusted $1,200,000

[2] Loss on discontinued operations:

Income from operations $ 160,000

Deduct: Loss on sale of assets (300,000)

Problem 4–4

1. Restructuring is an example of an event that is material and unusual. Restructuring

costs should be included in income from continuing operations but reported on a

2. The income from the discontinued operation should be presented, net of tax, in the

3. The correction of the error should be treated as a prior period adjustment to

beginning retained earnings, not as an adjustment to current year’s cost of goods

4–58 Intermediate Accounting, 8/e

Problem 4–5

ALEXIAN SYSTEMS, INC.

Income Statement

For the Year Ended December 31, 2016

($ in millions except per share data)

Net sales revenue …………………………………………………….

$425

Cost of goods sold …………………………………………………..

Gross profit …………………………………………………………….

Operating expenses:

Selling and administrative ……………………………………..

[2] $128

Restructuring costs ……………………………………………….

26

Total operating expenses …………………………………….

Operating income ……………………………………………………

Other income:

Interest revenue ……………………………………………………

3

Gain on sale of investments ……………………………………

6

Total other income ……………………………………………..

9

Income tax expense …………………………………………………

[3] 6

$ 81

$ 4.05

Problem 4–6

REMBRANDT PAINT COMPANY

Income Statement

For the Year Ended December 31, 2016

($ in thousands, except per share amounts)

Sales revenue ………………………………………………

$18,000

Cost of goods sold ……………………………………….

10,500

Gross profit …………………………………………………

7,500

Operating expenses:

Operating income ………………………………………..

4,200

Interest income (expense), net ……………………….

Income from continuing operations ………………..

Discontinued operations:

120

Income on discontinued operations ………………..

Net income ………………………………………………….

Earnings per share:

Income from continuing operations ………………..

Income on discontinued operations ………………..

Net income ………………………………………………….

4–60 Intermediate Accounting, 8/e

Problem 4–7

Requirement 1

SCHEMBRI MANUFACTURING CORPORATION

Statement of Comprehensive Income

For the Year Ended December 31, 2016

($ in 000s)

Sales revenue …………………………………………………………

$15,300

Cost of goods sold …………………………………………………..

6,200

Gross profit ……………………………………………………………

Operating expenses:

Selling ………………………………………………………………..

General and administrative ……………………………………

Restructuring costs …………………………..…………………..

Total operating expenses …………………………………..

Operating income ……………………………………………………

5,800

Other income (expense):

Loss on sales of investments …………………………………………………..

$(220)

Interest expense ……………………………………………………….

(180)

Interest revenue ……………………………………………………….

Other income (expense) ………………………………………………………

Income from continuing operations before income taxes

Income tax expense …………………………………………………

2,194

Income from continuing operations ………………………….

Discontinued operations:

Income from operations of discontinued component

Income tax expense ………………………………………………

(336)

Income on discontinued operations …………………………..

Net income …………………………………………………………….

Other comprehensive income:

Unrealized gains from investments, net of tax …………

Loss from foreign currency translation, net of tax …..

(144)

Total other comprehensive income ………………………….

Comprehensive income ………………………………………….

$3,843