Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Brief Exercise 15-17

Income Statement:

Lease revenue (straight-line amount) ........................... $25,000*

Journal entries (not required):

January 1, 2016

[No entry to record receivable or to derecognize asset]

December 31, 2016

Deferred lease revenue ............................................. 25,000

15–22 Intermediate Accounting, 8/e

Brief Exercise 15-18

Balance Sheet:

Lease Payable

Initial balance $158,373

Jan. 1, 2016 reduction (first lease payment) (25,000)

Right-of-Use Asset

Initial balance $158,373

Journal entries (not required):

January 1, 2016

Right-of-use asset ................................................ 158,373

December 31, 2016

Interest expense (10% x [$158,373 – 25,000]) ........... 13,337

Brief Exercise 15-19

Lease Payable

Initial balance $158,373

Right-of-Use Asset

Initial balance $158,373

Journal entries (not required):

January 1, 2016

December 31, 2016

Interest expense (10% x [$158,373 – 25,000]) ........... 13,337*

15–24 Intermediate Accounting, 8/e

Brief Exercise 15-20

The lease payable in the balance sheet will be $113,731:

Initial balance, January 1 (calculated below) ............. $140,000*

Brief Exercise 15-21

Pretax earnings will be reduced by $29,020 as calculated below:

January 1 interest expense ........................................... $ 0

Brief Exercise 15–22

The price at which the lessor is “selling” the asset being leased is the present

value of the lease payments:

$26,269 x 5.32948 = $140,000*

Journal entry (not required):

Lease receivable (present value) ........................................ 140,000

15–26 Intermediate Accounting, 8/e

Brief Exercise 15-23

The amount of interest expense the lessee would record in conjunction with the

second quarterly payment on October 1 is $2,892:

Initial balance, July 1 (given) ................................... $150,000

Journal entries (not required):

July 1

Lease payable ..................................................... 5,376

Brief Exercise 15-24

A lease that has a lease term (including options to terminate or renew that are

reasonably certain) of twelve months or less is considered a “short-term

lease.”

15–28 Intermediate Accounting, 8/e

EXERCISES

Exercise 15-1

(a) Nath-Langstrom Services, Inc. (Lessee)

June 30, 2016

Rent expense .................................. 10,000

(b) ComputerWorld Corporation (Lessor)

June 30, 2016

Cash ................................................ 10,000

Exercise 15-2

January 1, 2016

Prepaid rent (advance payment) ....................... 96,000

Cash .......................................................... 96,000

December 31, 2016

Rent expense (annual rent) .............................. 80,000

15–30 Intermediate Accounting, 8/e

Exercise 15-3

Present Value of Minimum Lease Payments:

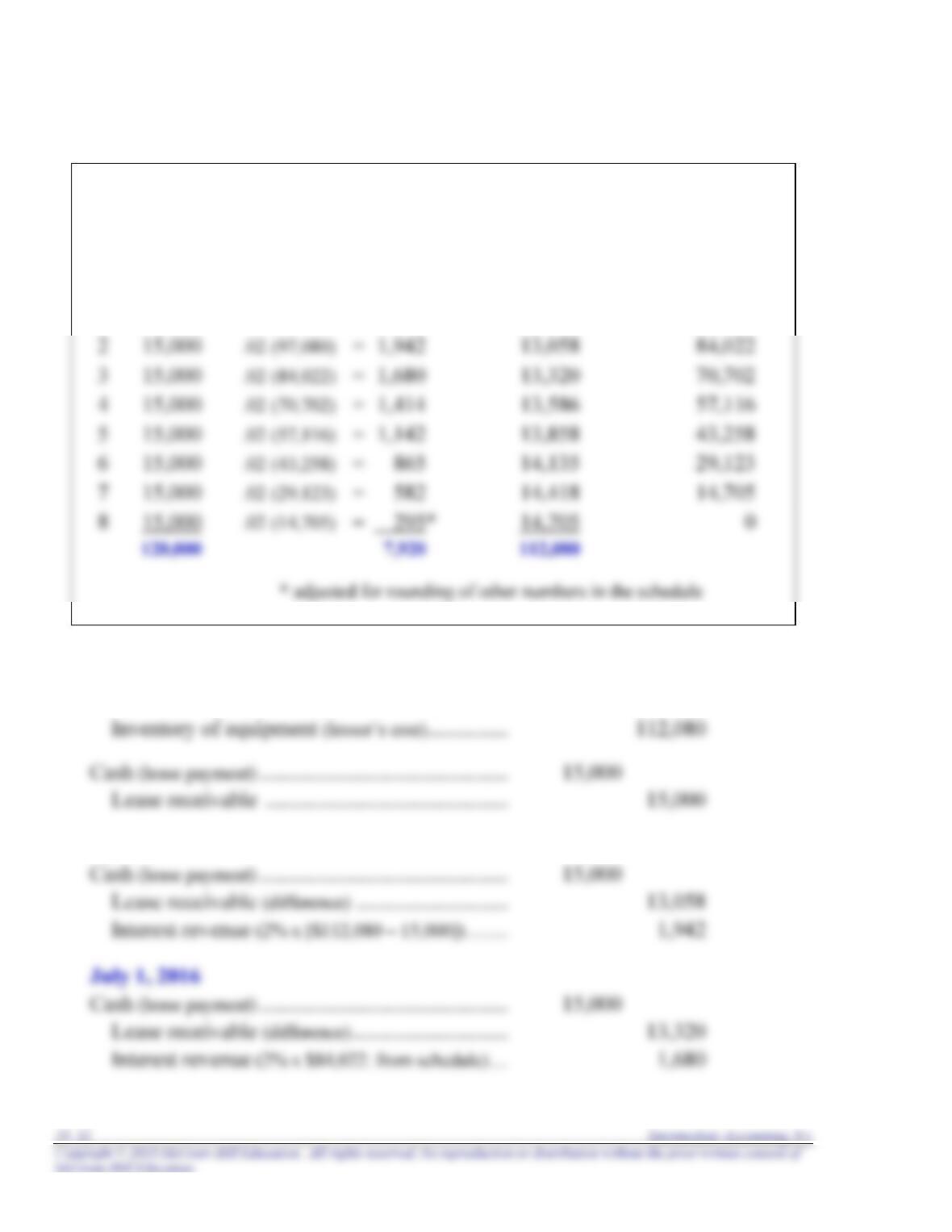

($15,000 x 7.47199*) = $112,080

Lease Amortization Schedule

Lease Effective Decrease Outstanding

Payments Interest in Balance Balance

2% x Outstanding Balance

112,080

1 15,000 15,000 97,080

January 1, 2016

Leased equipment (calculated above) ..................... 112,080

Exercise 15-3 (concluded)

April 1, 2016

Interest expense (2% x [$112,080 – 15,000]) ............. 1,942

Lease payable (difference) .................................... 13,058

Cash (lease payment) ......................................... 15,000

July 1, 2016

Exercise 15-4

Lease Amortization Schedule

Lease Effective Decrease Outstanding

Payments Interest in Balance Balance

2% x Outstanding Balance

112,080

1 15,000 15,000 97,080

January 1, 2016

Lease receivable (fair value).................................. 112,080

April 1, 2016

Exercise 15-4 (concluded)

October 1, 2016

Cash (lease payment).............................................. 15,000

15–34 Intermediate Accounting, 8/e

Exercise 15-5

Requirement 1

Lessor’s Calculation of Lease Payments

Amount to be recovered (fair value) $112,080

Requirement 2

January 1, 2016

Lease receivable (fair value / present value) ............. 112,080

April 1, 2016

Exercise 15-6

Situation 1

Since none of the criteria is met, this is an operating lease to the lessee:

Lessee’s Application of Classification Criteria

1 Does the agreement specify that

ownership of the asset transfers

to the lessee? NO

Exercise 15-6 (continued)

Situation 2

Since at least one (two in this case: #2 and #3) classification criterion is met, this

is a capital lease.

Lessee’s Application of Classification Criteria

1 Does the agreement specify that

ownership of the asset transfers

Exercise 15-6 (continued)

Situation 3

Since at least one (#4 in this case) classification criterion is met, this is a capital

lease.

Lessee’s Application of Classification Criteria

1 Does the agreement specify that

ownership of the asset transfers

to the lessee? NO

15–38 Intermediate Accounting, 8/e

Exercise 15-6 (concluded)

Situation 4

Since at least one (#4 in this case) classification criterion is met, this is a capital

lease.

Lessee’s Application of Classification Criteria

1 Does the agreement specify that

ownership of the asset transfers

to the lessee? NO

Exercise 15-7

Requirement 1 January 1, 2016

Leased assets ....................................................... 4,000,000

Lease payable ................................................. 4,000,000

Requirement 2

Requirement 3 December 31, 2016

Requirement 4 December 31, 2018

15–40 Intermediate Accounting, 8/e

Exercise 15-8

1. Calculation of the present value of lease payments

2. Liability at December 31, 2016

Initial balance, June 30, 2016 .................................. $3,000,000

June 30, 2016 reduction ........................................... (562,907)*

3. Expenses for year ended December 31, 2016

June 30, 2016 interest expense ................................. $ 0*

Calculations:

June 30, 2016*

Leased equipment (calculated in req. 1) ............................ 3,000,000