Problem 9–10

Requirement 1

Cost

Retail

Beginning inventory

$ 27,500

$ 45,000

Plus: Purchases

282,000

490,000

Freight-in

Less: Purchase returns

Purchase discounts

Plus: Net markups

550,000

Less: Net markdowns

_______

Goods available for sale

540,000

Less:

Estimated ending inventory at retail

$ 50,000

Estimated ending inventory at cost (59% x $50,000)

9–62 Intermediate Accounting, 8/e

Problem 9–10 (continued)

Requirement 2

Cost

Retail

Beginning inventory

$ 27,500

$ 45,000

Plus: Purchases

282,000

490,000

Freight-in

26,500

Less: Purchase returns

(6,500)

(10,000)

Plus: Net markups

25,000

Less: Net markdowns

Goods available for sale (excluding beg. inventory)

495,000

Goods available for sale (including beg. inventory)

$324,500

540,000

Less:

Employee discounts

Estimated ending inventory at cost:

Problem 9–10 (concluded)

Requirement 3

2015

Step 1 Step 2 Step 3

Ending Ending Inventory Inventory

Inventory Inventory Layers Layers

at Year-End at Base Year at Base Year Converted to

Retail Prices Retail Prices Retail Prices Cost

2016

9–64 Intermediate Accounting, 8/e

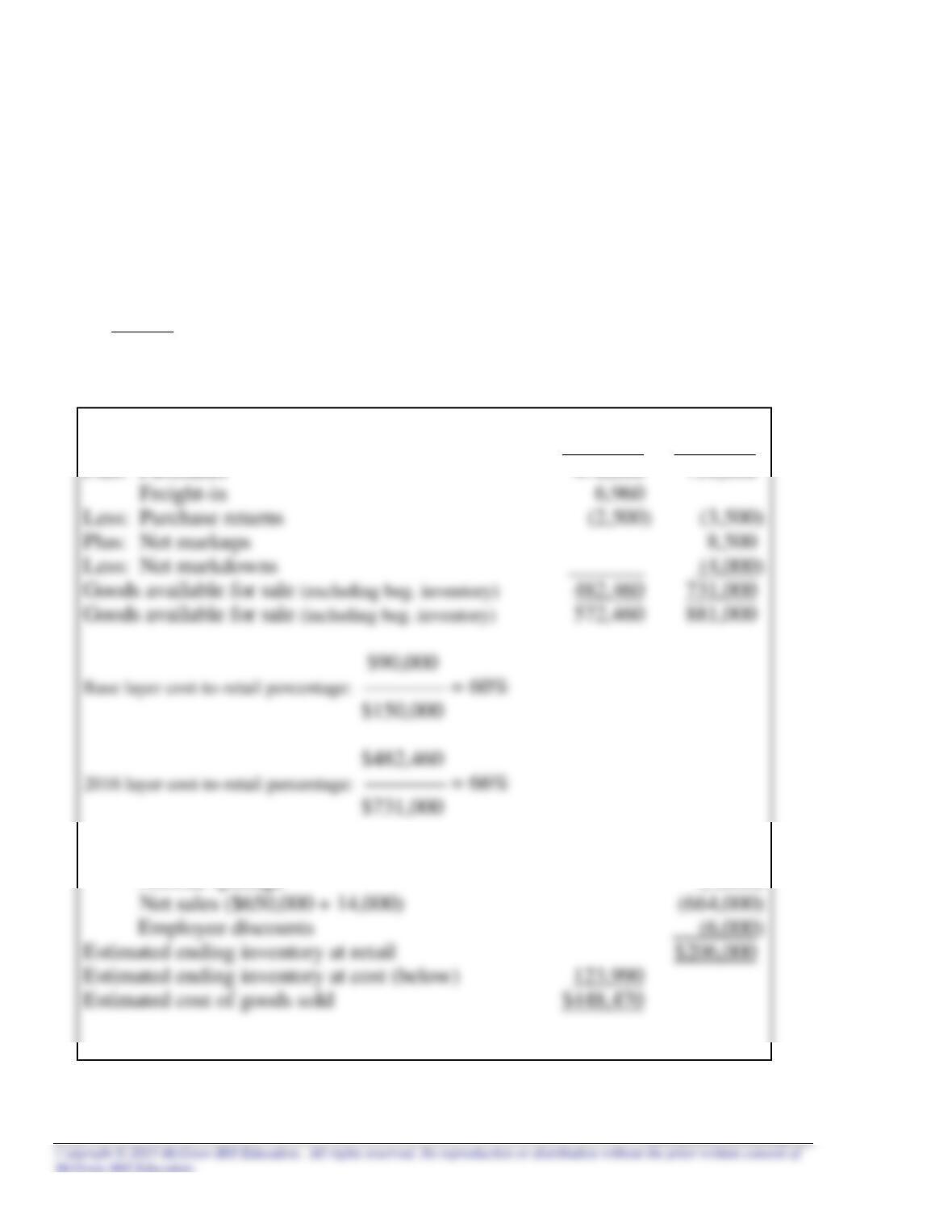

Problem 9–11

Requirement 1

Employee discounts must be deducted in the retail column.

2016:

$14,000

= $20,000 – 14,000 = $6,000 = Employee discounts

.70

Cost

Retail

Beginning inventory

$ 90,000

$150,000

Plus: Purchases

478,000

730,000

Freight-in

Less: Purchase returns

(2,500)

(3,500)

Plus: Net markups

Less: Net markdowns

Goods available for sale (excluding beg. inventory)

482,460

731,000

Goods available for sale (including beg. inventory)

572,460

881,000

Less:

Normal spoilage

(5,000)

Estimated ending inventory at retail

$206,000

Estimated ending inventory at cost (below)

123,990

Estimated cost of goods sold

Problem 9–11 (continued)

2016

Step 1 Step 2 Step 3

Ending Ending Inventory Inventory

Inventory Inventory Layers Layers

at Year-End at Base Year at Base Year Converted to

Retail Prices Retail Prices Retail Prices Cost

9–66 Intermediate Accounting, 8/e

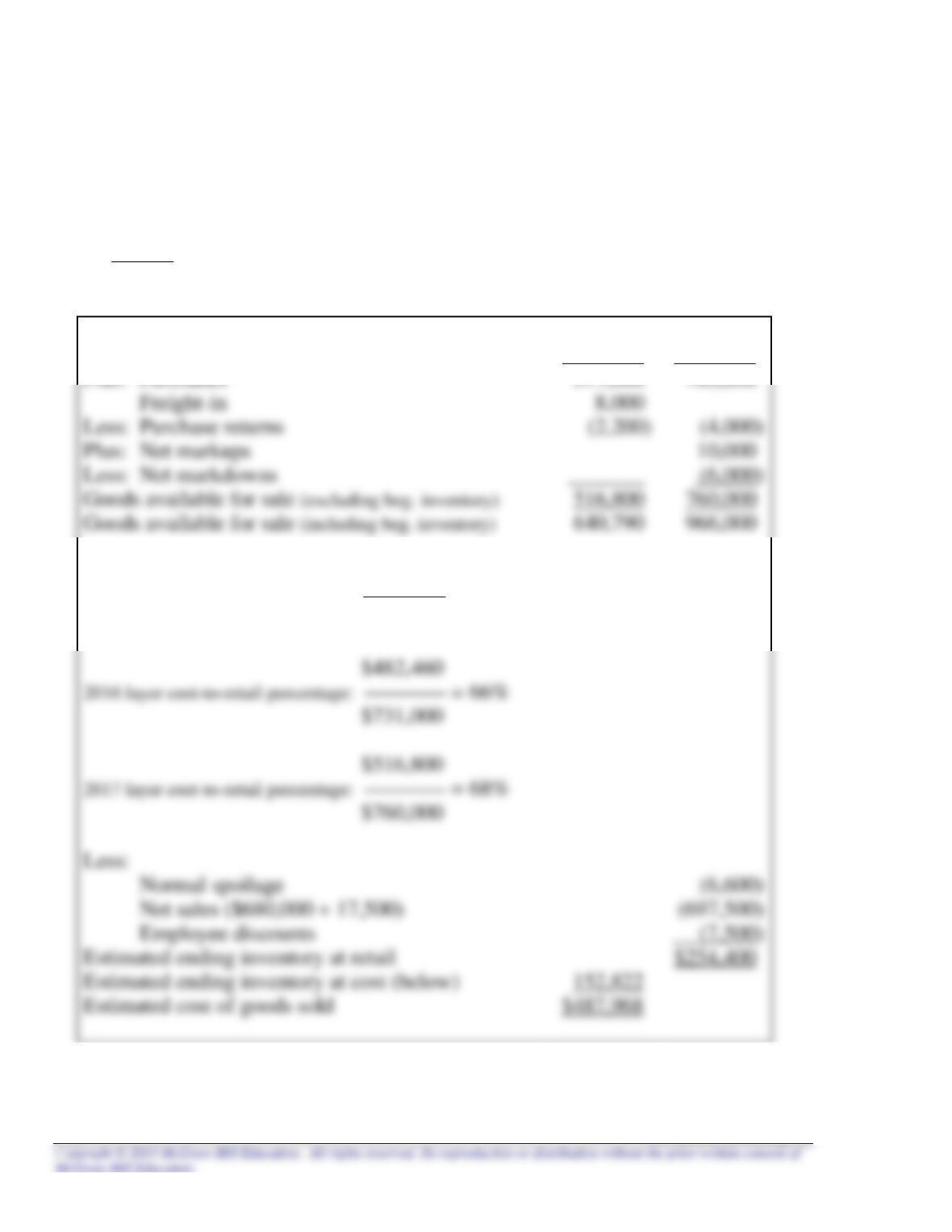

Problem 9–11 (continued)

Employees must be deducted in the retail column.

2017:

$17,500

= $25,000 – 17,500 = $7,500 = Employee discounts

.70

Cost

Retail

Beginning inventory

$123,990

$206,000

Freight-in

Less: Purchase returns

Plus: Net markups

Less: Net markdowns

Goods available for sale (including beg. inventory)

$90,000

Base layer cost-to-retail percentage: = 60%

$150,000

Employee discounts

Estimated ending inventory at retail

$254,400

Estimated cost of goods sold

$487,968

Problem 9–11 (continued)

2017

Step 1 Step 2 Step 3

Ending Ending Inventory Inventory

Inventory Inventory Layers Layers

at Year-End at Base Year at Base Year Converted to

Retail Prices Retail Prices Retail Prices Cost

$254,400

$254,400 = $240,000 $150,000 (base) x 1.00 x 60% = $90,000

9–68 Intermediate Accounting, 8/e

Problem 9–11 (continued)

Requirement 2

Employee discounts must be deducted in the retail column.

2016:

$14,000

= $20,000 – 14,000 = $6,000 = Employee discounts

.70

Cost

Retail

Beginning inventory

$ 90,000

$150,000

Plus: Purchases

Freight-in

Less: Purchase returns

Plus: Net markups

Less: Net markdowns

Goods available for sale

Less:

Normal spoilage

Estimated ending inventory at retail

$206,000

Estimated ending inventory at cost (64.98% x $206,000)

Estimated cost of goods sold

$438,601

$572,460

Problem 9–11 (concluded)

Requirement 3

Employee discounts must be deducted in the retail column.

2016:

Cost

Retail

Beginning inventory

$ 90,000

$150,000

Plus: Purchases

478,000

730,000

Freight–in

Plus: Net markups

572,460

885,000

$572,460

Cost-to-retail percentage: = 64.68%

$885,000

Less: Markdowns

(4,000)

Goods available for sale

881,000

Normal spoilage

Estimated ending inventory at retail

$206,000

Estimated cost of goods sold

$439,219

9–70 Intermediate Accounting, 8/e

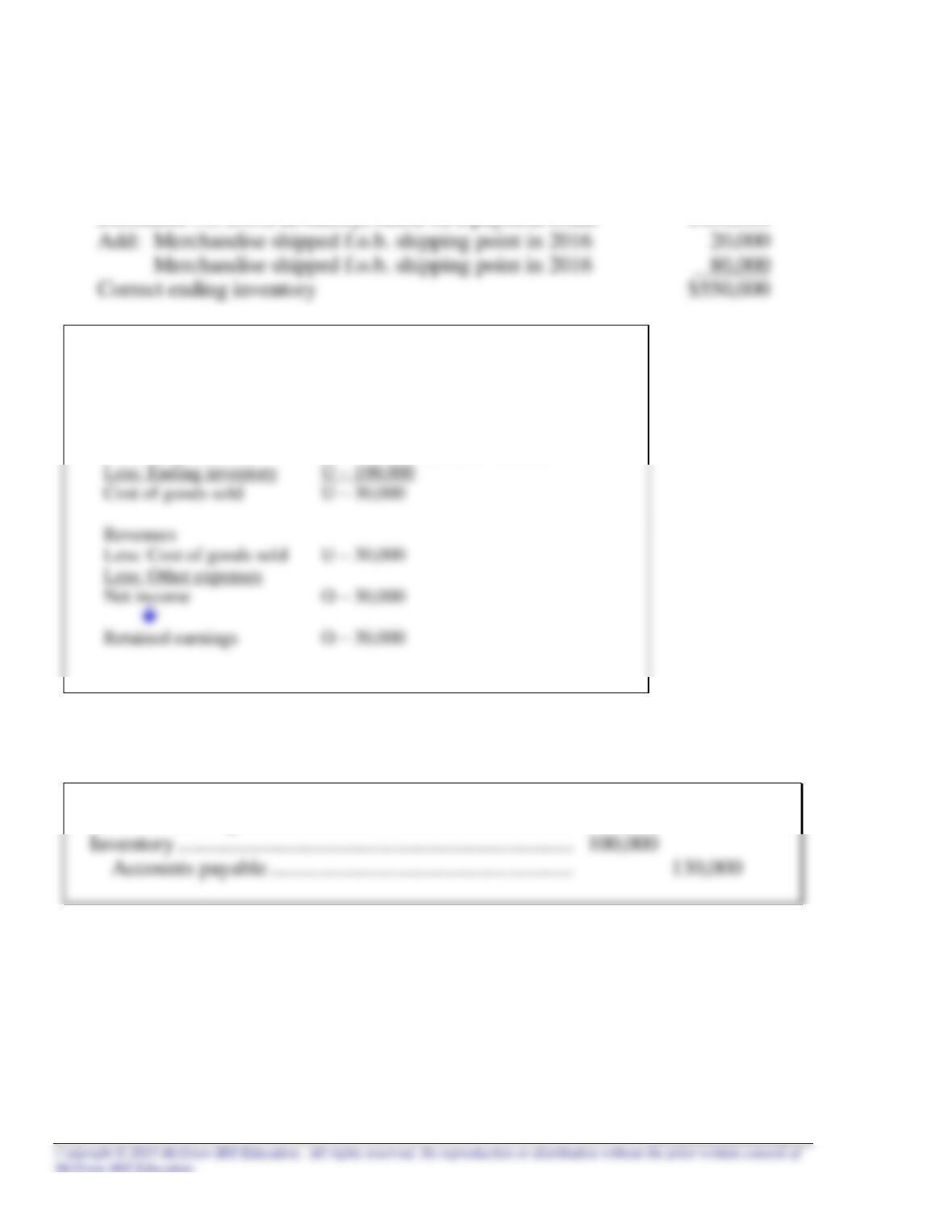

Problem 9–12

Requirement 1

Retained earnings ………………………………………………………… 20,000

Inventory ($150,000 – 130,000) …………………………………. 20,000

Requirement 2

FIFO method cost of goods sold:

Cost of goods available for sale $530,000

Less ending inventory:

Average cost method cost of goods sold:

Beginning inventory (5,000 units) $130,000

Cost of ending inventory:

$510,000

Weighted average unit cost = = $34

Problem 9–13

Requirement 1

Analysis: U = Understated

O = Overstated

2014 2015

Beginning inventory Beginning inventory U-6,000

Requirement 2

Retained earnings ………………………………………………….. 12,000

Requirement 3

The financial statements that were incorrect as a result of both errors (effect of

one error in 2014 and effect of three errors in 2015) would be retrospectively restated

9–72 Intermediate Accounting, 8/e

Problem 9–14

Requirement 1

December 31, 2016, inventory, based on a physical count $450,000

Analysis: U = Understated

O = Overstated

2016

Beginning inventory

Plus: Net purchases U – 130,000 ($50,000 + 80,000)

Requirement 2

Retained earnings …………………………………………………… 30,000

Problem 9–15

Requirement 1

Accounts Accounts Sales

Inventory Purchases payable receivable revenue

Unadjusted balance $326,000 $620,000 $210,000 $225,000 $840,000

Item:

1. (32,000)

2. (27,000) (27,000)

Requirement 2

Beginning inventory ($352,000 + 62,000) $414,000

Requirement 3

The 2015 financial statements that were incorrect as a result of the error would be

retrospectively restated to report the correct inventory amounts, cost of goods sold,

9–74 Intermediate Accounting, 8/e

Problem 9–16

Requirement 1

a. $10.50

If market price is equal to or greater than the contract price, the purchase is

recorded at cost.

If market price is less than the contract price, the purchase is recorded at the

market price.

Requirement 2

a. $12.50

December 31, 2016

Estimated loss on purchase commitment