Problem 17–16 (continued)

Requirement 5

To record gains and losses

($ in millions)

Requirement 6

SHAREHOLDERS’ EQUITY: ACCUMULATED

OTHER COMPREHENSIVE INCOME

Net Loss—AOCI

Balance, Jan. 1 42.0

New loss 5.0 12.0 New gain

Prior Service Cost–AOCI

Balance, Jan. 1 28.0

Problem 17–16 (concluded)

Requirement 7

( )s indicate credits; debits

otherwise

($ in millions)

PBO

Plan

Assets

Prior

Service

Cost

–AOCI

Net

Loss

–AOCI

Pension

Expense

Cash

Net

Pension

(Liability)

/ Asset

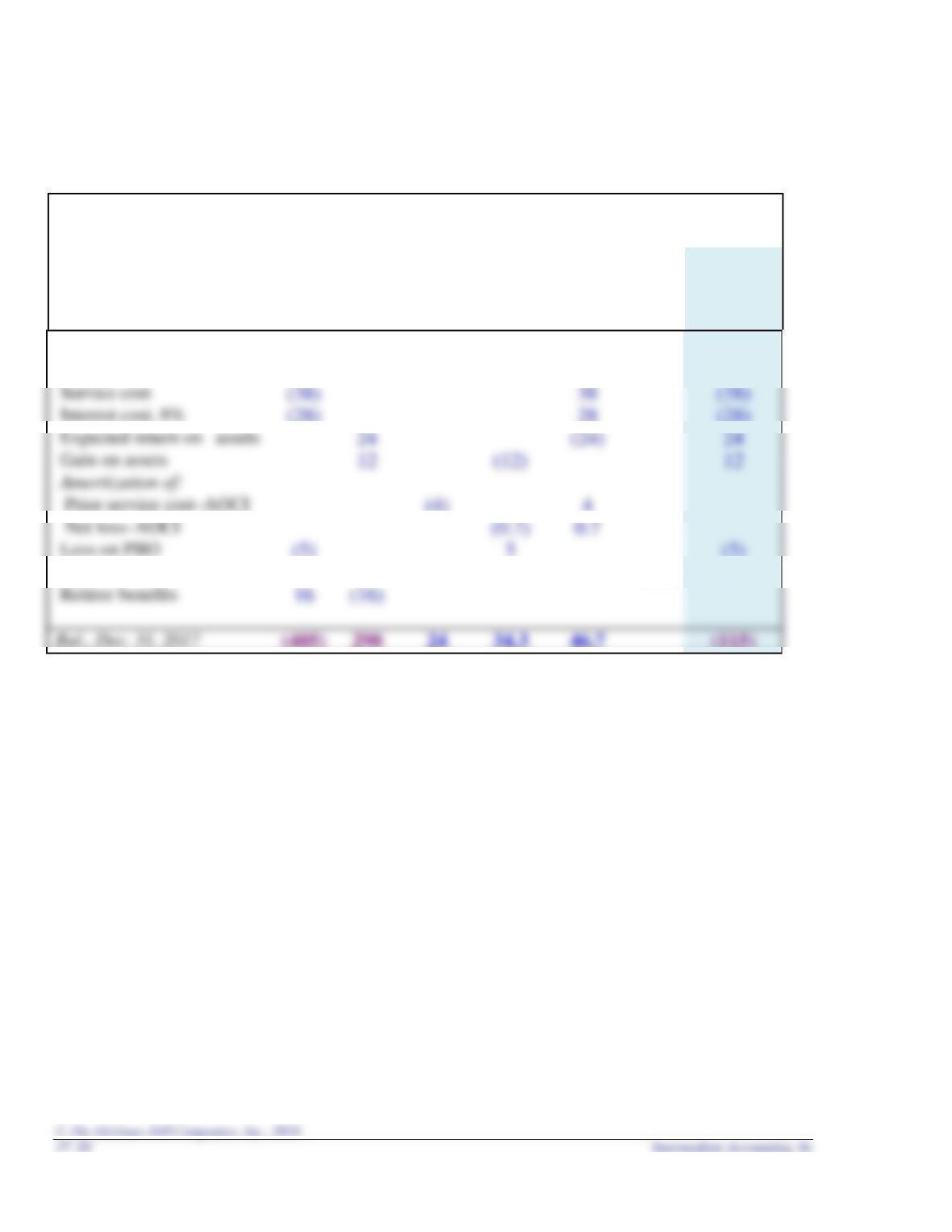

Bal., Jan. 1, 2017

(350)

240

28

42

(110)

Service cost

(38)

38

(38)

Interest cost, 8%

(28)

28

(28)

Expected return on assets

24

24

Gain on assets

12

12

Prior service cost–AOCI

(4)

4

Net loss–AOCI

0.7

Loss on PBO

(5)

5

(5)

Cash contributions

30

(30)

30

Retiree benefits

16

(16)

(405)

290

24

34.3

46.7

(115)

Problem 17–17

Requirement 1

To Record Pension Expense ($ in millions)

Deferred tax asset (40% x [$41 + 24 – 27]) ……………………………. 15.2

Pension expense ($41 + 24 – 27 + 4 + 1) ………………………………. 43.0

17–22 Intermediate Accounting, 8e

Problem 17–17 (continued)

To Record New Gains and Losses ($ in millions)

Deferred tax asset (40% x $23) ……………… 9.2

Loss—OCI ($23 loss, net of $9.2 tax benefit) 13.8

Problem 17–17 (continued)

To Record Funding and Payment of Benefits ($ in millions)

Plan assets ………………………………………… 48

Cash (contribution to plan assets) ………….. 48

Problem 17–17 (concluded)

Requirement 2

GLOBAL COMMUNICATIONS

Statement of Comprehensive Income

Year ended December 31, 2016

Problem 17–18

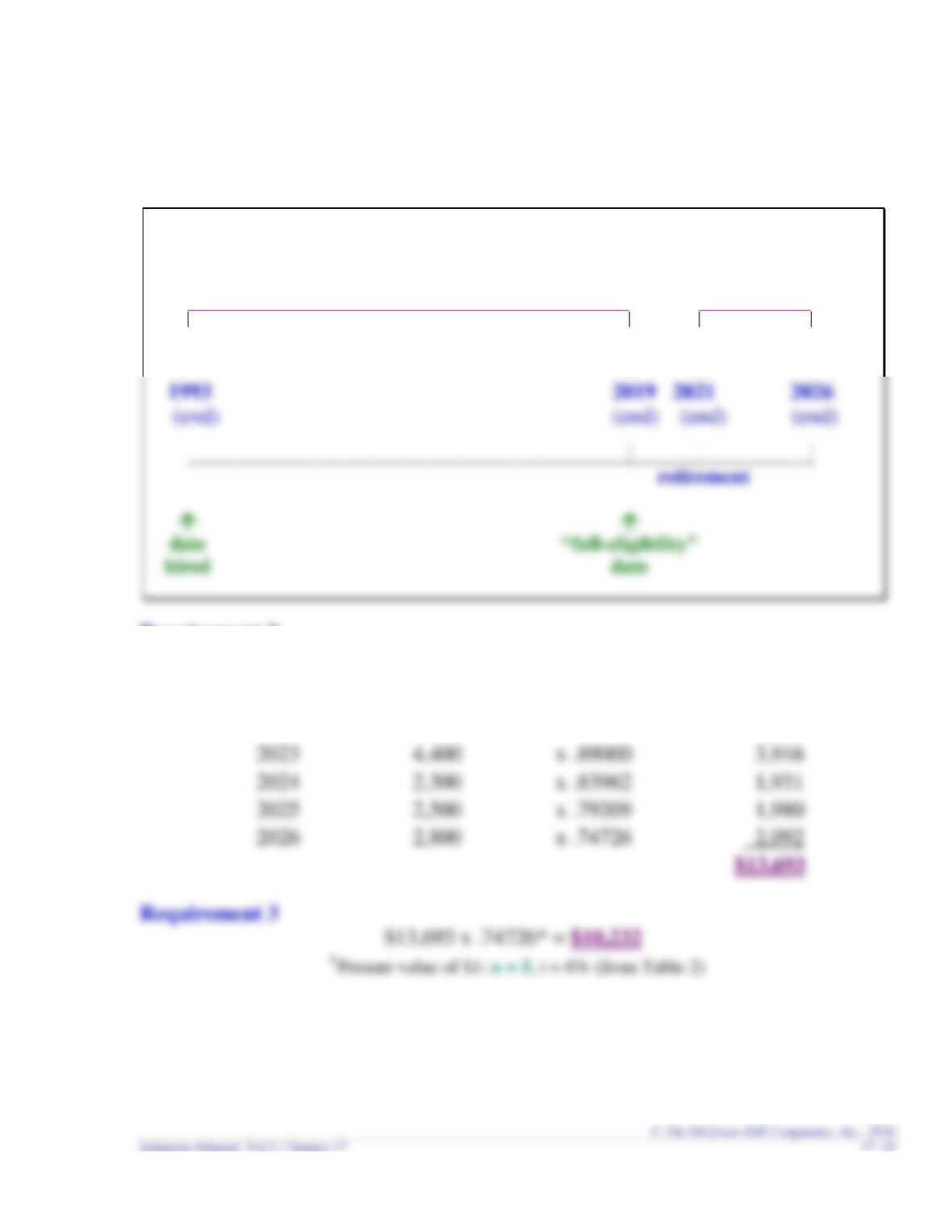

Requirement 1

Retirement

Attribution Period Period

26 years 5 years

age age age age

34 60 62 67

Requirement 2

Year Expected PV of $1 Present Value

End Net Cost n = 1–5, i = 6% at Dec. 31, 2018

2022 $4,000 x .94340 $ 3,774

17–26 Intermediate Accounting, 8e

Problem 17–18 (concluded)

Requirement 4

$10,232 x 23 yrs*/26 yrs** = $9,051

Problem 17–19

EPBO

Fraction

Earned

APBO

Service

Cost

Interest

Cost

Expense

10%

3/8

4/8

6/8

7/8

1/8

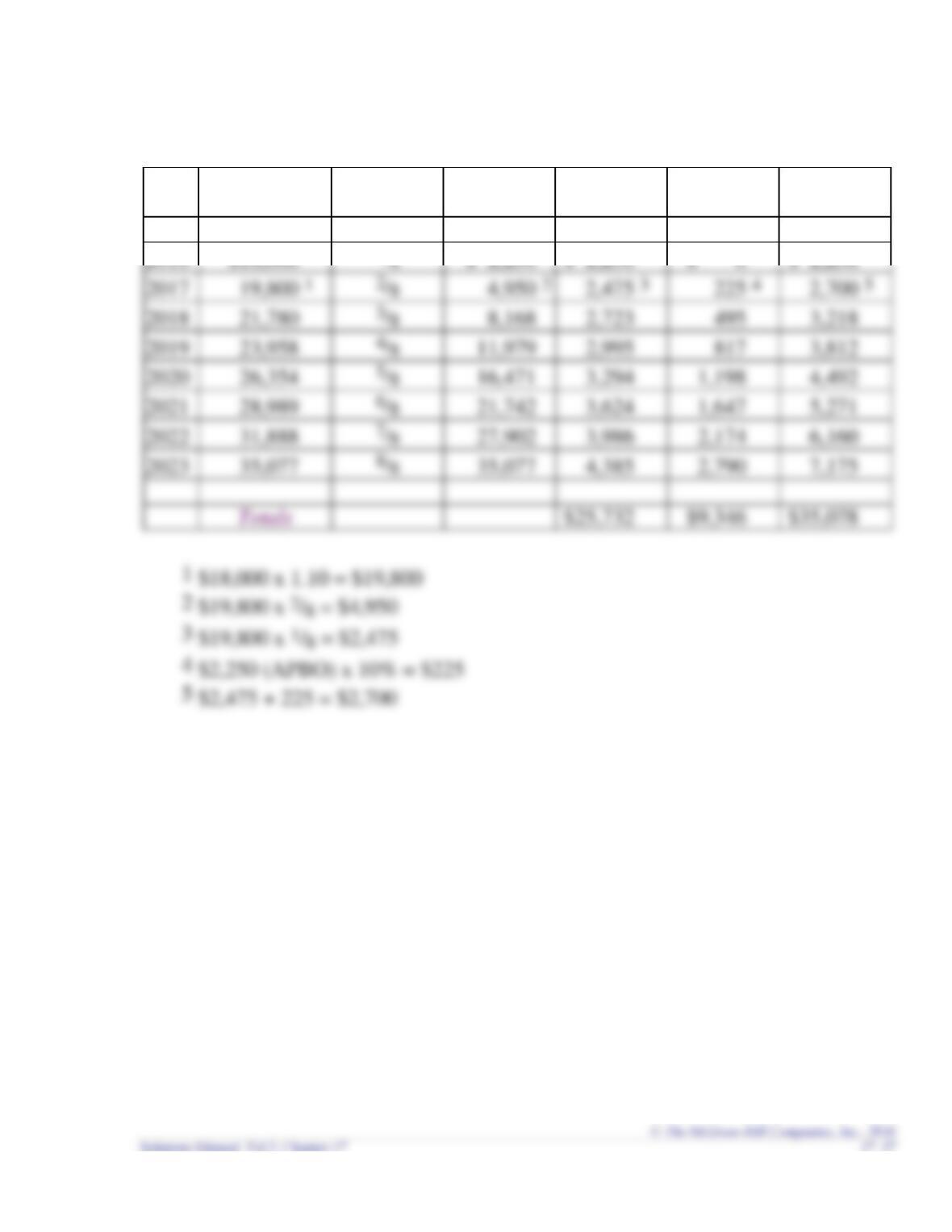

Problem 17–20

Requirement 1

($ in 000s)

APBO:

Beginning of 2016 $460

Requirement 2

($ in 000s)

Requirement 3

($ in 000s)

Problem 17–21

Requirement 1

The difference between an employer’s obligation (PBO) and the resources

available to satisfy that obligation (plan assets) is the funded status of the pension

plan. The employer must report the net difference between those two amounts,

17–30 Intermediate Accounting, 8e

Problem 17–21 (concluded)

Requirement 3 ($ in millions)

Service cost $ 5.0

Requirement 4

The pension liability, which is the difference between the PBO and plan assets,

increases by the combination of the service cost, interest cost, and the expected return

as is reflected in the following entry.

CASES

Judgment Case 17–1

Requirement 1

Here is a graphical depiction of your estimated service and retirement periods:

2016 2055 2075

_____________________________________________

Case 17–1 (continued)

Requirement 2

The value of your plan assets as of the anticipated retirement date is $1,872,981:

A

B

C

D

E

End of

Years to

Future Value

Year:

Retirement

Salary

Contribution

at Retirement

2016

39

100,000

77,628

2017

38

103,000

75,431

2018

37

106,090

73,296

2019

36

109,273

71,222

2020

35

112,551

69,206

2021

34

115,927

67,247

2022

33

119,405

65,344

2023

32

122,987

63,495

2024

31

126,677

10,134

61,698

2025

30

130,477

10,438

59,952

2026

29

134,392

10,751

58,255

2027

28

138,423

11,074

56,606

2028

27

142,576

11,406

55,004

2029

26

146,853

11,748

53,447

2030

25

151,259

12,101

51,935

2031

24

155,797

12,464

50,465

2032

23

160,471

12,838

49,037

2033

22

165,285

13,223

47,649

2034

21

170,243

13,619

46,300

2035

20

175,351

14,028

44,990

2036

19

180,611

14,449

43,717

2037

18

186,029

14,882

42,479

2038

17

191,610

15,329

41,277

2039

16

197,359

15,789

40,109

2040

15

203,279

16,262

38,974

2041

14

209,378

16,750

37,871

2042

13

215,659

17,253

36,799

2043

12

222,129

17,770

35,757

2044

11

228,793

18,303

34,745

2045

10

235,657

18,853

33,762

2046

242,726

19,418

32,806

2047

250,008

20,001

31,878

257,508

20,601

30,976

2049

265,234

21,219

30,099

2050

273,191

21,855

29,247

2051

281,386

22,511

28,419

2052

289,828

23,186

27,615

2053

298,523

23,882

26,834

2054

307,478

24,598

26,074

2055

316,703

25,336

25,336

Case 17–1 (concluded)

Requirement 3

Based on the calculations alone, the state’s defined benefit plan offers the larger

retirement annuity and, therefore, lump-sum equivalent of the retirement annuity. Be

17–34 Intermediate Accounting, 8e

Communication Case 17–2

Suggested Grading Concepts and Grading Scheme:

Content (80%)

25 The net periodic pension expense measures this compensation and

consists of the following five elements which can vary differently

from changes in employment. (5 each; maximum of 25 for this part)

The service cost component is the present value of the benefits

earned by the employees during the current period.

The interest cost component is the increase in the projected benefit

obligation due to the passage of time.

The return on plan assets reduces the pension expense. The actual

return on plan assets component is the difference between the fair

value of the plan assets at the beginning and the end of the period,

adjusted for contributions and benefit payments. This amount is

adjusted for any gain or loss, so it is the expected return that actually

affects the calculation.

Prior service cost is created when a pension plan is amended and

credit is given for employee service rendered in prior years. This

retroactive credit is not recognized as pension expense entirely in the

year the plan is amended, but is recognized in pension expense over

the time that the employees who benefited from this credit work for

the company.

Gains and losses arise from changes in estimates concerning the

amount of the projected benefit obligation or the return on the plan

assets being different from expected. These are not included in

pension expense as they occur. They are instead reported as other

comprehensive income.

20 Gains and losses occur when the PBO or the return on plan assets

turns out to be different than expected. (10 each; maximum of 20 for

this part)

Gains and losses are reported as they occur in the statement of

comprehensive income, not as part of pension expense. They

accumulate over time as a net gain or net loss, a component of

accumulated other comprehensive income.

A net gain or a net loss affects pension expense only if it exceeds an

amount equal to 10% of the PBO, or 10% of plan assets, whichever is

higher.

Case 17–2 (concluded)

When the corridor is exceeded, the excess is not charged to pension

expense all at once. Instead, the amount that should be included is the

excess divided by the average remaining service period of active

employees expected to receive benefits under the plan.

20 PBO and ABO compared (10 each; maximum of 20 for this part)

Both the accumulated benefit obligation and the projected benefit

obligation represent the present value of the benefits attributed by the

pension benefit formula to employee service rendered prior to a

specific date.

The accumulated benefit obligation is based on present salary levels

and the projected benefit obligation is based on estimated future salary

levels.

15 The projected benefit obligation in excess of plan assets:

This is the funded status of the plan and is reported in the balance

sheet as a pension liability (10 points)

If the plan assets exceed the PBO, it would be reported as a pension

asset. (5 points)

80 points

Writing (20%)

5 Terminology and tone appropriate to the audience of

assistant controllers.

6 Organization permits ease of understanding.

Introduction that states purpose.

Paragraphs separate main points.

9 English

Word selection.

Spelling.

Grammar.

20 points

Judgment Case 17–3

Requirement 1

Yes, it’s true that the pension expense is calculated as if the balance sheet

contained certain amounts it doesn’t individually report, specifically the projected

Requirement 2

Requirement 3