IMPAIRMENT OF VALUE – A SUMMARY

Type of

Asset

When to Test

for Impairment

Impairment Test

To Be Held and Used:

Tangible and finite-

life intangible assets

When events or

circumstances indicate

Step 1 – An impairment loss is required only

when book value is not recoverable

Indefinite life

intangible assets

(other than goodwill)

At least annually, and

more frequently if

indicated. Option to

avoid annual testing by

making qualitative

evaluations of the

likelihood of asset

impairment.

If book value exceeds fair value, an

impairment loss is recognized for the

difference.

Goodwill

indicated. Option to

avoid annual testing by

making qualitative

evaluations of the

likelihood of goodwill

impairment to determine

if step one is necessary.

book value.

Step 2 – An impairment loss is measured as

At least annually, and

more frequently if

Step 1 – A loss is indicated when the fair

value of the reporting unit is less than its

Illustration 11-25

T11-21

11-38 Intermediate Accounting, 8/e

EXPENDITURES SUBSEQUENT TO ACQUISITION

➢ Any expenditure must be either capitalized or expensed.

➢ Expenditures that simply maintain a given level of benefits

are expensed in the period they are incurred.

➢ Expenditures related to long-lived, revenue-producing assets

can increase future benefits in the following ways:

2. An increase in the operating efficiency of the asset

3. An increase in the quality of the goods or services

produced by the asset.

➢ Theoretically, expenditures that cause any of these results

T11-22

IMPROVEMENTS

➢ Improvements involve the replacement of a major component

of an asset.

➢ The replacement can be a new component with the same

characteristics as the old component or a new component with

enhanced operating capabilities.

➢ Three methods are used to record the cost of improvements:

1. Substitution. The improvement can be recorded as both (1) a

disposition of the old component and (2) the acquisition of the new

2. Capitalization of new cost. Include the cost of the improvement

(net of any consideration received) as a debit to the related asset

3. Reduction of accumulated depreciation. Increase an asset’s book

value by leaving the asset account unaltered but decrease its related

T11-23

11-40 Intermediate Accounting, 8/e

IMPROVEMENTS

(continued)

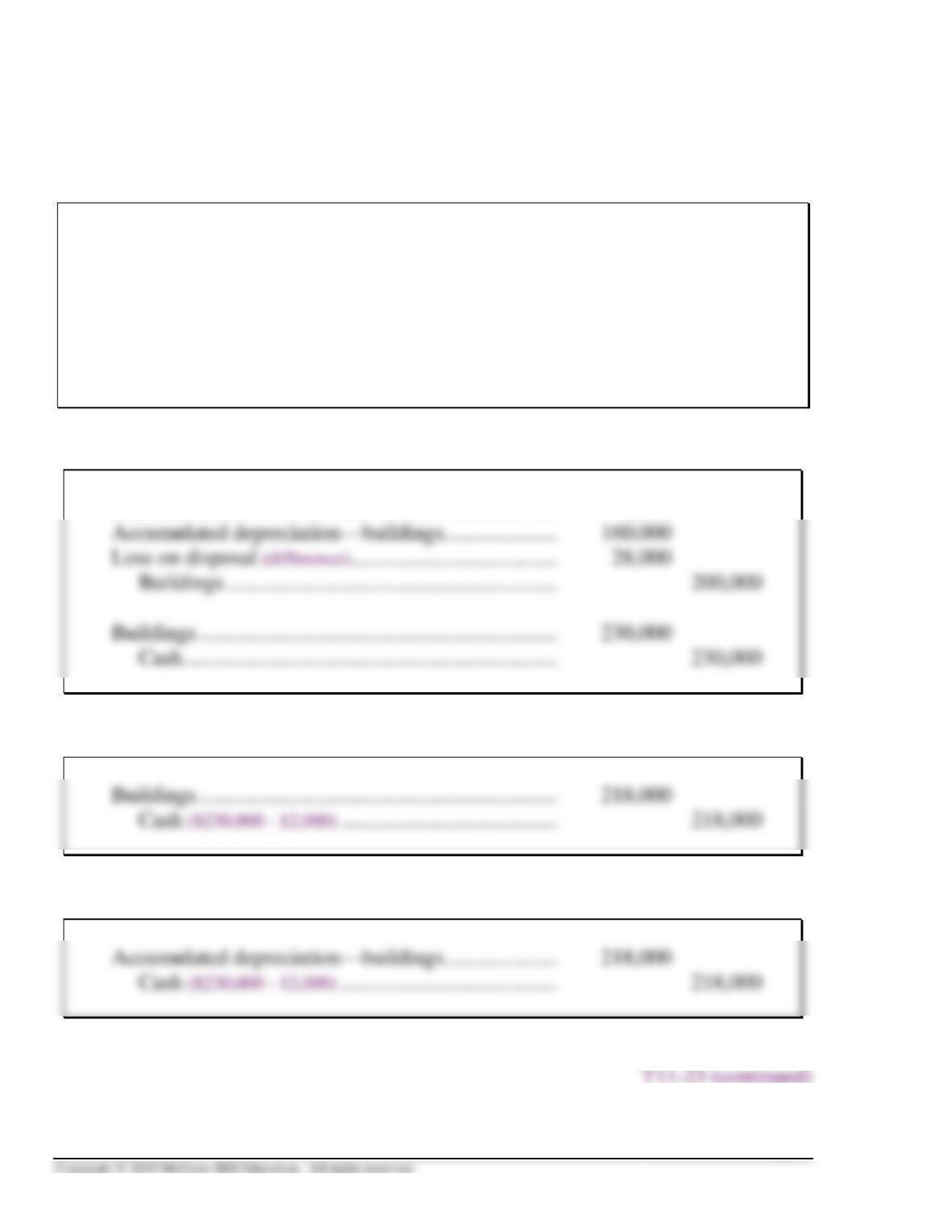

The Palmer Corporation replaced the air conditioning system in one of its office

buildings that it leases to tenants. The cost of the old air conditioning system,

$200,000, is included in the cost of the building. However, the company has

separately depreciated the air conditioning system. Depreciation recorded up to the

date of replacement totaled $160,000. The old system was removed and the new

system installed at a cost of $230,000, which was paid in cash. Parts from the old

system were sold for $12,000.

SUBSTITUTION

Cash ……………………………………………………………….. 12,000

CAPITALIZATION OF NEW COST

REDUCTION OF ACCUMULATED DEPRECIATION

Illustration 11-26

REARRANGEMENTS

➢ Rearrangements are expenditures made to restructure an asset

without addition, replacement, or improvement.

T11-24

11-42 Intermediate Accounting, 8/e

INTERNATIONAL FINANCIAL REPORTING STANDARDS

T11-25

COMPARISON WITH MACRS

➢ Tax rules allow taxpayers to compute depreciation for their tax

returns using the modified accelerated cost recovery system

(MACRS).

➢ Under MACRS, each asset is placed within a recovery period

category.

➢ According to the category, fixed percentage rates are applied to

the original cost of the asset. The rates for the five-year asset

category are as follows:

Year Rate

1 20.00%

T11-26

11-44 Intermediate Accounting, 8/e

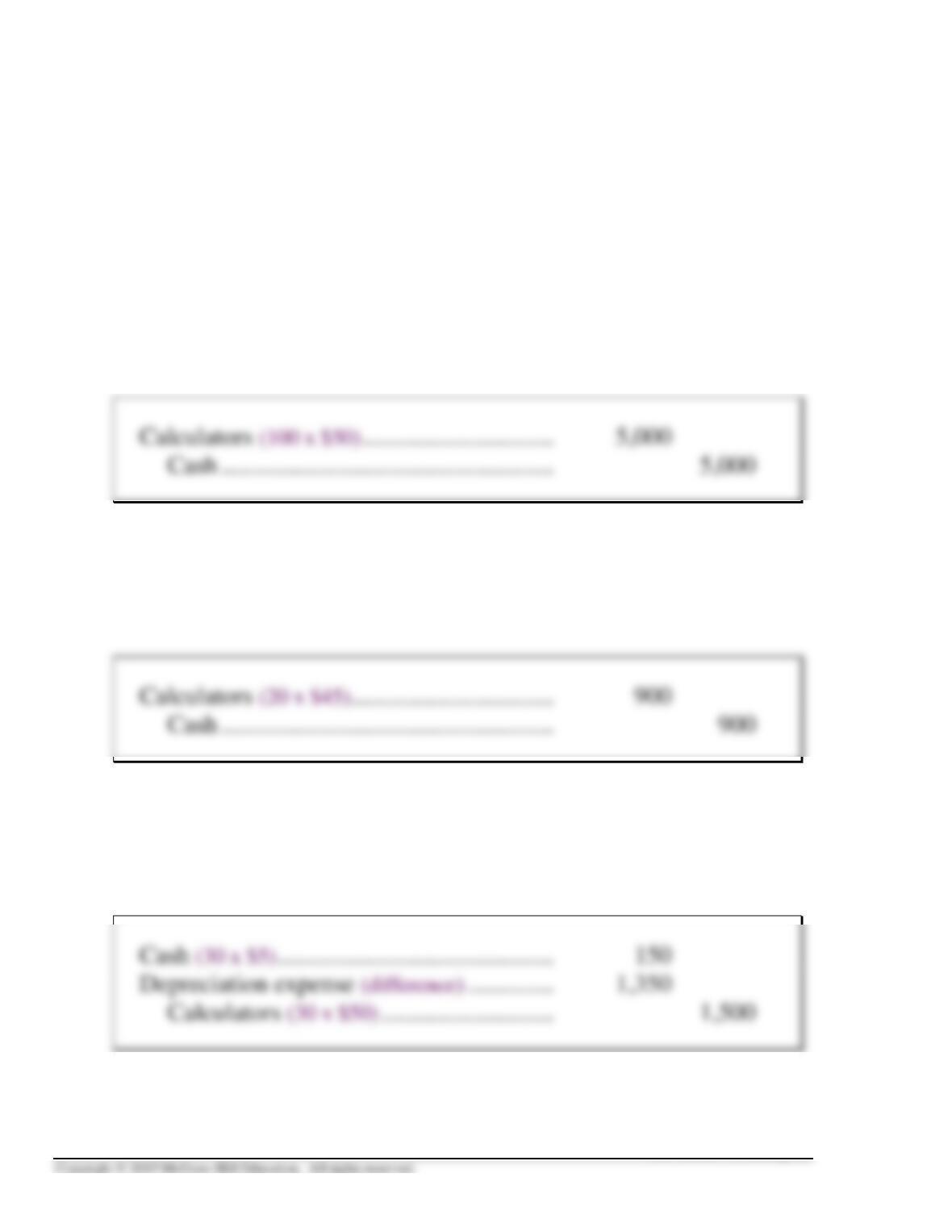

RETIREMENT DEPRECIATION METHOD

➢ Records depreciation when assets are disposed of and

measures depreciation as the difference between the proceeds

received and cost.

▶ For example, the following entry records the purchase of

100 hand-held calculators at $50 each:

▶ If 20 new calculators are acquired at $45 each, the asset

account is increased.

▶ If 30 calculators are sold for $5 each, the following entry

reflects the sale:

T11-27

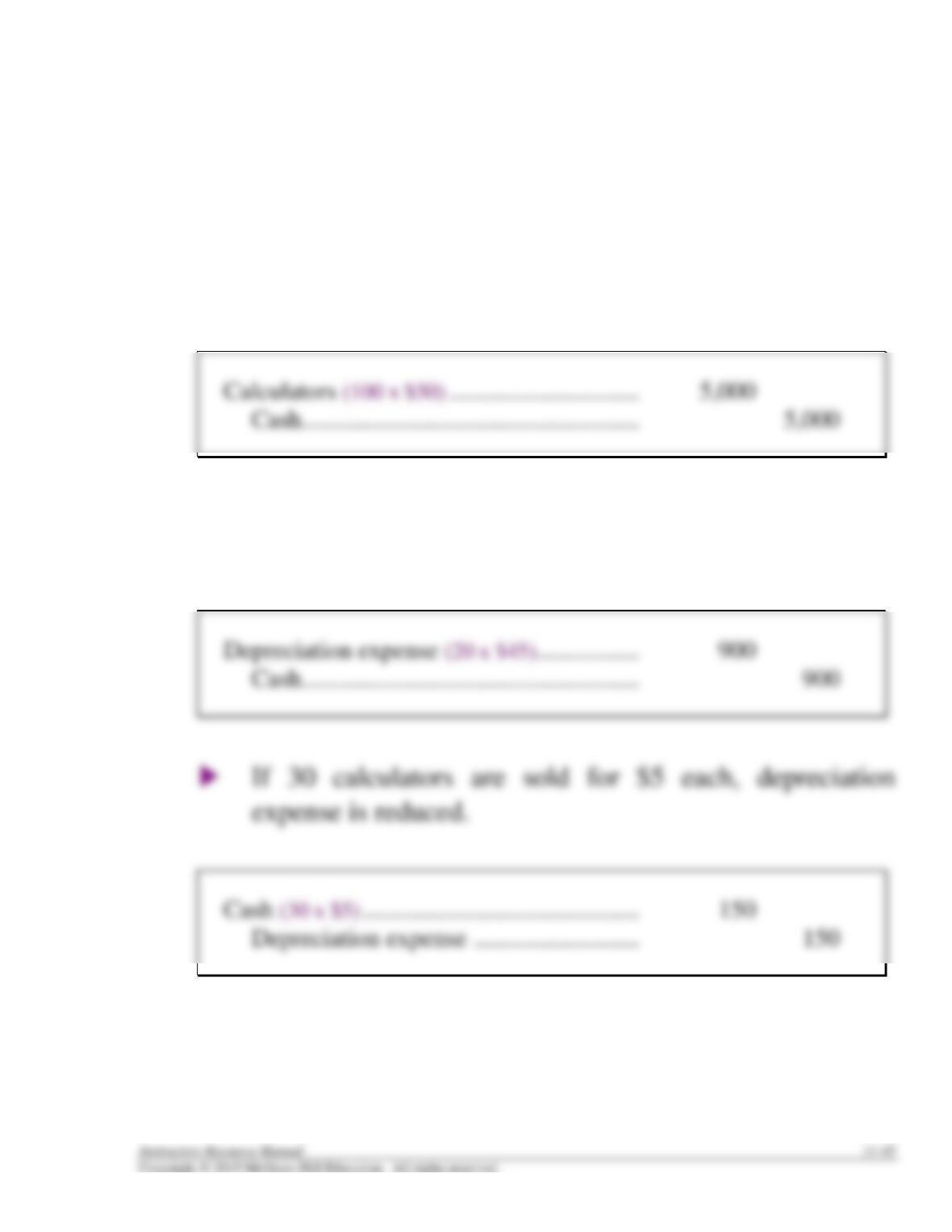

REPLACEMENT DEPRECIATION METHOD

➢ Depreciation is recorded when assets are replaced.

▶ For example, the following entry records the purchase of

100 hand-held calculators at $50 each:

▶ The acquisition of 20 new calculators at $45 each is

recorded as depreciation expense.

T11-28

11-46 Intermediate Accounting, 8/e

Suggestions for Class Activities

1. Research Activity

In the late 1990s, the stock prices of many companies were unusually high. These often-inflated

stock prices meant high purchase prices for many business acquisitions and, in many cases,

incredibly high values allocated to goodwill. When stock prices retreated in the new century, it

became obvious that the book value of goodwill for many companies would never be recovered.

2. Research Activity

A research activity in Chapter 10 suggested you require the class to investigate the property, plant,

and equipment and intangible assets reported by Toro Company in the company’s financial

statement for the 2013 fiscal year. Toro reported approximately $185 million in property, plant, and

equipment and another $120 million in intangible assets in its balance sheet. Continue that activity

by having your students investigate Toro’s depreciation and amortization methods as well as the

useful lives assigned to the various types of assets.

Suggestions:

Have the class access Toro’s 2013 financial statements using EDGAR at: www.sec.gov.

Ask them to answer the following questions:

1. What depreciation method(s) does Toro employ?

2. What estimated lives does Toro use for its plant and equipment?

3. What are the estimated useful lives of the intangible assets?

Points to Note:

Toro provides for depreciation of plant and equipment utilizing the straight-line method over the

estimated useful lives of the assets. Buildings, including leasehold improvements, are generally

3. Case Activity

The August 2004 issue of Issues in Accounting Education contains a case entitled “A & B

4. PetSmart Analysis

Have students, individually or in groups, go to the most recent PetSmart annual report using

EDGAR at: www.sec.gov. Ask them to:

Determine the company’s depreciation method and the amount of depreciation and

amortization recorded during the most recent year. Does the income statement report any asset

impairment losses? If so, describe the losses and the events or circumstances that triggered the

5. Professional Skills Development Activities

The following are suggested assignments from the end-of-chapter material that will help your

students develop their communication, research, analysis and judgment skills.

Communication Skills. In addition to Communication Case 11-2, Judgment Case 11-4 can be

adapted to ask students to write a memo to Patrick Company’s controller. Communication

Research Skills. In their careers, our graduates will be required to locate and extract relevant

information from available resource material to determine the correct accounting practice,

Analysis Skills. The “Broaden Your Perspective” section includes Analysis Cases that direct

students to gather, assemble, organize, process, or interpret data to provide options for making

Judgment Skills. The “Broaden Your Perspective” section includes Judgment Cases that require

students to critically analyze issues to apply concepts learned to business situations in order to

CPA Simulation. Students can test their knowledge of the concepts discussed in this chapter and

at the same time practice critical professional skills necessary for career success and

preparation for the computer-based CPA Exam. The simulation for this chapter, Fukisan Inc.,

11-48 Intermediate Accounting, 8/e

Assignment Chart

Learning Est. time

Questions Objective(s) Topic (min.)

11-1

1

Depreciation, depletion, and amortization

5

11-2

1

Depreciation

5

11-3

1

Depreciation, depletion, and amortization

5

11-4

1

Estimation or service life

5

11-5

1

Depreciable base

5

11-6

2

Activity-based versus time-based methods

5

11-7

2

Straight-line versus accelerated methods

5

11-8

2

Straight-line versus accelerated methods

5

11-9

2

Motivation for straight-line depreciation

5

11-10

2

Group versus composite depreciation

5

11-11

3

Depletion

5

11-12

2,3,4

Amortization, depletion, and depreciation

5

11-13

2

Partial year depreciation

5

11-14

5

Change in service life

5

11-15

6

Change in depreciation method

5

11-16

7

Error correction

5

11-17

8

Impairment of value

5

11-18

9

Subsequent expenditures

5

11-19

10

IFRS; subsequent valuation

5

11-20

10

IFRS; measurement of impairment loss

5

11-21

10

IFRS; impairment loss for goodwill

5

11-22

10

IFRS; litigation costs to defend a right

5

Brief Learning Est. time

Exercises Objective(s) Topic (min.)

11-1

1

Cost allocation

5

11-2

2

Depreciation methods

10

11-3

2

Depreciation methods; partial periods

10

11-4

2

Group depreciation

10

11-5

3

Depletion

10

11-6

4

Amortization

10

11-7

5

Change in estimate; useful life of equipment

15

11-8

6

Change in depreciation method

10

11-9

7

Error correction

10

11-10

8

Impairment; property, plant, and equipment

10

11-11

8

Impairment; property, plant, and equipment

10

11-12

8,10

IFRS; impairment; PP&E

10

11-13

8

Impairment; goodwill

10

11-14

8

Impairment; goodwill

10

11-15

10

IFRS; impairment; goodwill

10

11-16

9

Subsequent expenditures

5

11-50 Intermediate Accounting, 8/e

Learning Est. time

Exercises Objective(s) Topic (min.)

11-1

2

Depreciation methods

30

11-2

2

Depreciation methods

25

11-3

2

Depreciation methods; partial years

35

11-4

2,9

Depreciation methods; asset addition

15

11-5

2

Depreciation methods; solving for unknowns

30

11-6

2

Depreciation methods

20

11-7

2

Depreciation methods; partial years

15

11-8

2,10

IFRS; depreciation

15

11-9

10

IFRS; revaluation of machinery; depreciation

20

11-10

2

Group depreciation

20

11-11

2,6

Double-declining-balance method; switch to S-L

20

11-12

3

Depletion

10

11-13

2,3

Depletion and depreciation

15

11-14

2,3

Cost of a natural resource; depletion and

depreciation; Chapters 10 and 11

20

11-15

4,5

Amortization

20

11-16

4,9

Patent amortization; patent defense

15

11-17

4,5

Change in estimate; useful life of patent

10

11-18

10

IFRS; revaluation of patent; amortization

20

11-19

2,5

Change in estimate; useful life and residual value of

equipment

20

11-20

2,6

Change in principle; change in depreciation methods

15

11-21

2,6

Change in principle; change in depreciation methods

10

11-22

2,7

Error correction

15

11-23

8

Impairment; property, plant, and equipment

15

11-24

10

IFRS; impairment; property, plant, and equipment

10

11-25

8,10

IFRS; ; impairment; property, plant, and equipment

10

11-26

8

Impairment; property, plant, and equipment

20

11-27

8

Impairment; goodwill

15

11-28

10

IFRS; impairment; goodwill

15

11-29

8

Goodwill valuation and impairment; Chapters 10 and

11

20

11-30

8

FASB codification research

20

11-31

2,4,6,8

FASB codification research

20

11-32

9

Subsequent expenditures

15

11-33

4,9,10

IFRS; amortization; cost to defend a patent

15

11-34

2

Depreciation methods; disposal; Chapters 10 and 11

15

11-35

1,2,3,4,5,6,8

Concepts; terminology

15

11-36

B

Retirement and replacement depreciation [Based on

Appendix B]

15

CPA/CMA Learning Est. time

Exam Questions Objective(s) Topic (min.)

CPA-1

2

Double-declining-balance method

3

CPA-2

2

Depreciation

3

CPA-3

3

Depletion

3

CPA-4

4

Amortization

3

CPA-5

4

Amortization

3

CPA-6

5

Change in estimate of useful life

3

CPA-7

8

Impairment

3

CPA-8

9

Subsequent expenditures

3

CPA-9

10

IFRS

3

CPA-10

10

IFRS

3

CPA-11

10

IFRS

3

CPA-12

10

IFRS

3

CPA-13

10

IFRS

3

CPA-14

10

IFRS

3

CMA-1

3

Depletion

3

CMA-2

4

Goodwill

3

CMA-3

9

Subsequent expenditures; patent

3

Learning Est. time

Problems Objective(s) Topic (min.)

11-1

2,6

Depreciation methods; change in methods

25

11-2

2,4

Comprehensive problem; chapters 10 and 11

60

11-3

2

Depreciation methods

40

11-4

2,5,9

Partial year depreciation; asset addition, increase

in useful life

20

11-5

2

Property, plant, and equipment and intangible

assets; comprehensive

60

11-6

2

Depreciation methods; partial year depreciation;

sale of assets

30

11-7

3,5

Depletion; change in estimate

40

11-8

4

Amortization

25

11-9

2,5

Straight-line depreciation; change in useful life

and residual value

35

11-10

2,5,6

Accounting changes; three accounting situations

30

11-11

2,6,7

Error correction; change in depreciation method

30

11-12

2,4,8

Depreciation and amortization; impairment

30

11-13

2,3,5

Chapters 10 and 11; depreciation and depletion;

change in useful life; asset retirement obligation

60

Star Problems

11-52 Intermediate Accounting, 8/e

Learning Est. time

Cases Objective(s) Topic (min.)

Analysis Case 11-1

1

Depreciation, depletion, and amortization

10

Communication Case 11-2

1

Depreciation

45

Judgment Case 11-3

1,2

Straight-line method; composite depreciation

15

Judgment Case 11-4

1,2

Depreciation

15

Judgment Case 11-5

9

Capitalize or expense; materiality

20

Communication Case 11-6

9

Capitalize or expense; materiality

20

Integrating Case 11-7

5,6,7

Errors; change in estimate; change in principle;

inventory, patent and equipment

30

Judgment Case 11-8

5,6

Accounting changes

25

Research Case 11-9

8

FASB codification research; impairment

45

Ethics Case 11-10

8

Asset impairment

35

Judgment Case 11-11

5,6,8

Earnings management and accounting changes;

impairment

20

Trueblood Accounting

Case 1-12

8

Accounting for impairment losses; property,

plant, and equipment

45

Judgment Case 11-13

9

Subsequent expenditures

15

Real World Case 11-14

1

Disposition and depreciation; Caterpillar

35

Real World Case 11-15

2,3,8,9

Depreciation and depletion method; asset

impairment; subsequent expenditures; Chevron

45

IFRS Case 11-16

10

IFRS; subsequent valuation of property, plant,

and equipment; comparison of U.S. GAAP and

IFRS; GlaxoSmithKline

25

Analysis Case 11-17

2,4

Depreciation and amortization; PetSmart

20

Air France-KLM Case

10

IFRS; property; plant, and equipment and

intangible assets; Air France-KLM

30

CPA Simulation 11-1 Depreciation methods; change in useful lives