Problem 17–7

Requirement 1

($ in 000s)

Net gain (previous gains exceeded previous losses) $170

Requirement 2

Requirement 3

17–62 Intermediate Accounting, 8/e

Problem 17–8

( )s indicate

credits; debits

otherwise

($ in millions)

PBO

Plan

Assets

Prior

Service

Cost

–AOCI

Net

Loss

–AOCI

Pension

Expense

Cash

Net

Pension

(Liability) /

Asset

Balance, Jan.

1, 2016

(830)

680

20

93

(150)

Service cost

(74)

74

(74)

(83)

83

(83)

(7)

Interest

Amortization of:

Prior

service

cost

(5)

5

Net loss

(1)

1

(13)

(13)

(40)

(40)

(50)

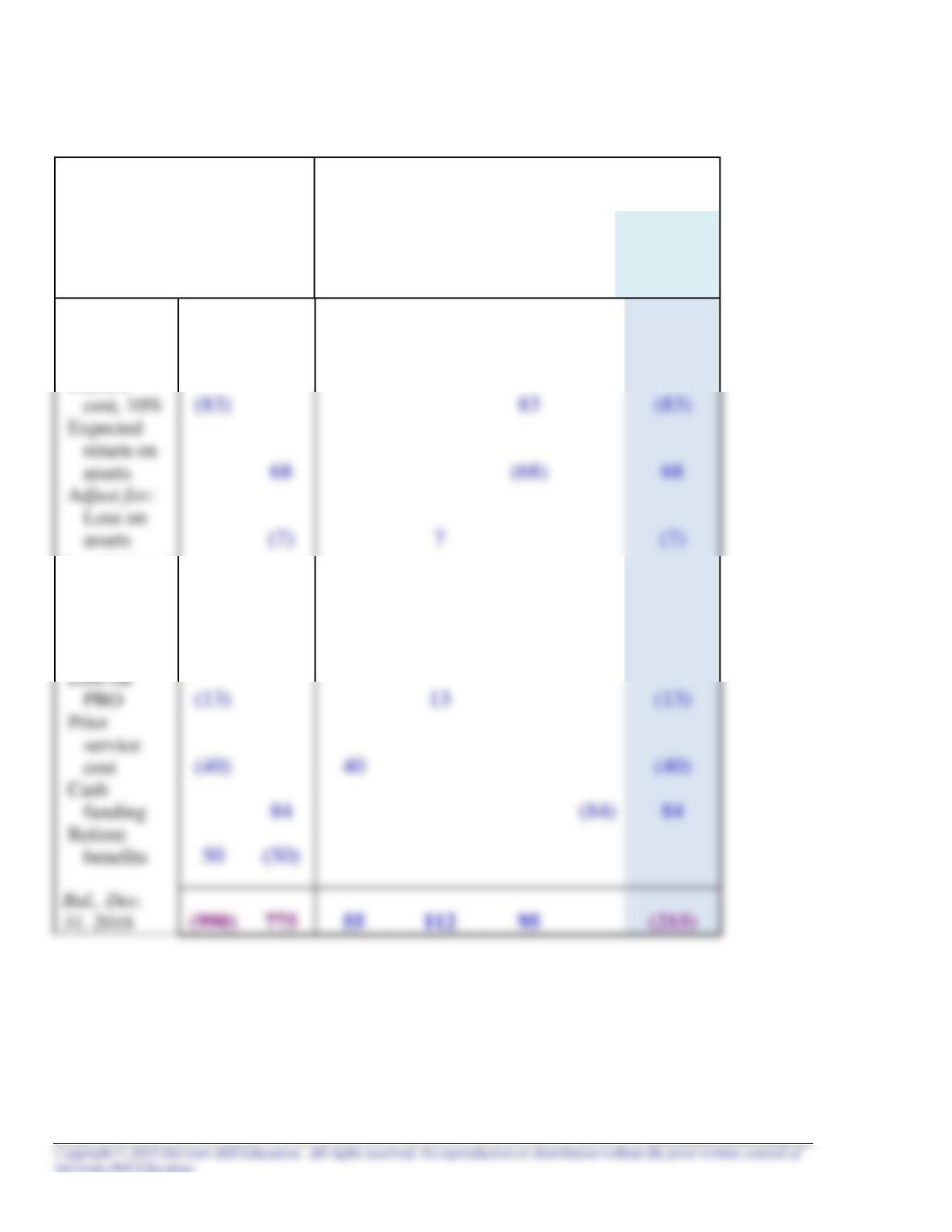

Problem 17–8 (concluded)

Calculations:

Interest cost = $830 x 10% = $83

Amortization of net loss:

Requirement 2

($ in millions)

Pension expense (total) …………………………………………………….. 95

Requirement 3

Record gains and losses and new prior service cost

($ in millions)

Loss—OCI ($61 actual return on assets less than $68 expected return) 7

Requirement 4

($ in millions)

Plan assets 84

17–2 Intermediate Accounting, 8e

Problem 17–9

1. Pension expense ($ in 000s)

Service cost $60

2. Projected Benefit Obligation

Balance, January 1 $320

3. Plan Assets

Balance, January 1 $400

4. Net Pension Asset or Net Pension Liability

Problem 17–9 (concluded)

5. Journal Entries

($ in 000s)

Pension expense (total) …………………………………………………….. 40

* Because Prior service cost—AOCI and Net loss—AOCI have debit balances, we amortize them with credits.

We would amortize a Net gain—AOCI (credit balance) with a debit. After the two amortization amounts are

reported as OCI in this year’s statement of comprehensive income, the respective AOCI amounts in the balance

sheet are reduced.

17–4 Intermediate Accounting, 8e

Problem 17–10

Requirement 1

($ in millions)

Service cost $ 75

Requirement 2

($ in millions)

Pension expense (calculated above) 96

Problem 17–10 (concluded)

Requirement 3

($ in millions)

PBO balance, January 1 $480

Service cost 75

17–6 Intermediate Accounting, 8e

Problem 17–11

Requirement 1

($ in millions)

Reported in income statement:

Problem 17–11 (continued)

Requirement 2

($ in millions)

Service cost 87

DBO (Service cost—2016) 75

Problem 17–11 (concluded)

Requirement 3

($ in millions)

DBO balance, January 1 $480

Service cost 75

Problem 17–12

Requirement 1 ($ in millions)

2016 2017

Service cost (given) $520 $570

*** Net Gain—AOCI

2016

Net gain—AOCI at 1-1-2016 $230

No amortization for 2017

17–10 Intermediate Accounting, 8e

Problem 17–12 (continued)

Requirement 2

($ in millions)

2016

Pension expense (total) ……………………………………………………… 583

Requirement 3

($ in millions)

2016

Loss—OCI ($180 actual return on assets less than $192 expected return) 12

Problem 17–12 (concluded)

Requirement 4

($ in millions)

2016

Plan assets 540

Cash (contribution to plan assets) 540

Problem 17–13

Projected Benefit Pension

Obligation Plan Assets Expense

Balance at Jan. 1 $ 0 $ 0

Prior service cost 2,000,000 2,000,000

Amortization of prior service cost

Note: The $40,000 gain ($220,000 – 180,000), while not included in pension

expense, is reported as a gain—OCI in the statement of comprehensive

Problem 17–14

1. Actual return on plan assets

($ in 000s)

Plan assets

Beginning of 2016 $2,400

2. Loss or gain on plan assets

3. Service cost

PBO:

Beginning of 2016 $2,300

Service cost ?

17–14 Intermediate Accounting, 8e

Problem 17–14 (concluded)

4. Pension expense

($ in 000s)

Service cost $310

5. Average remaining service life of active employees

Net gain, Jan. 1 $330

Problem 17–15

( )s indicate

credits; debits

otherwise

($ in 000s)

PBO

Plan

Assets

Prior

Service

Cost

–AOCI

Net

Loss

–AOCI

Pension

Expense

Cash

Net

Pension

(Liability)

/ Asset

Balance, Jan.

1, 2016

(4100)

4530

840

477

430

Service

cost2

(332)

332

(332)

Amortization of:

Prior

service

cost5

(70)

70

4975

770

484

238

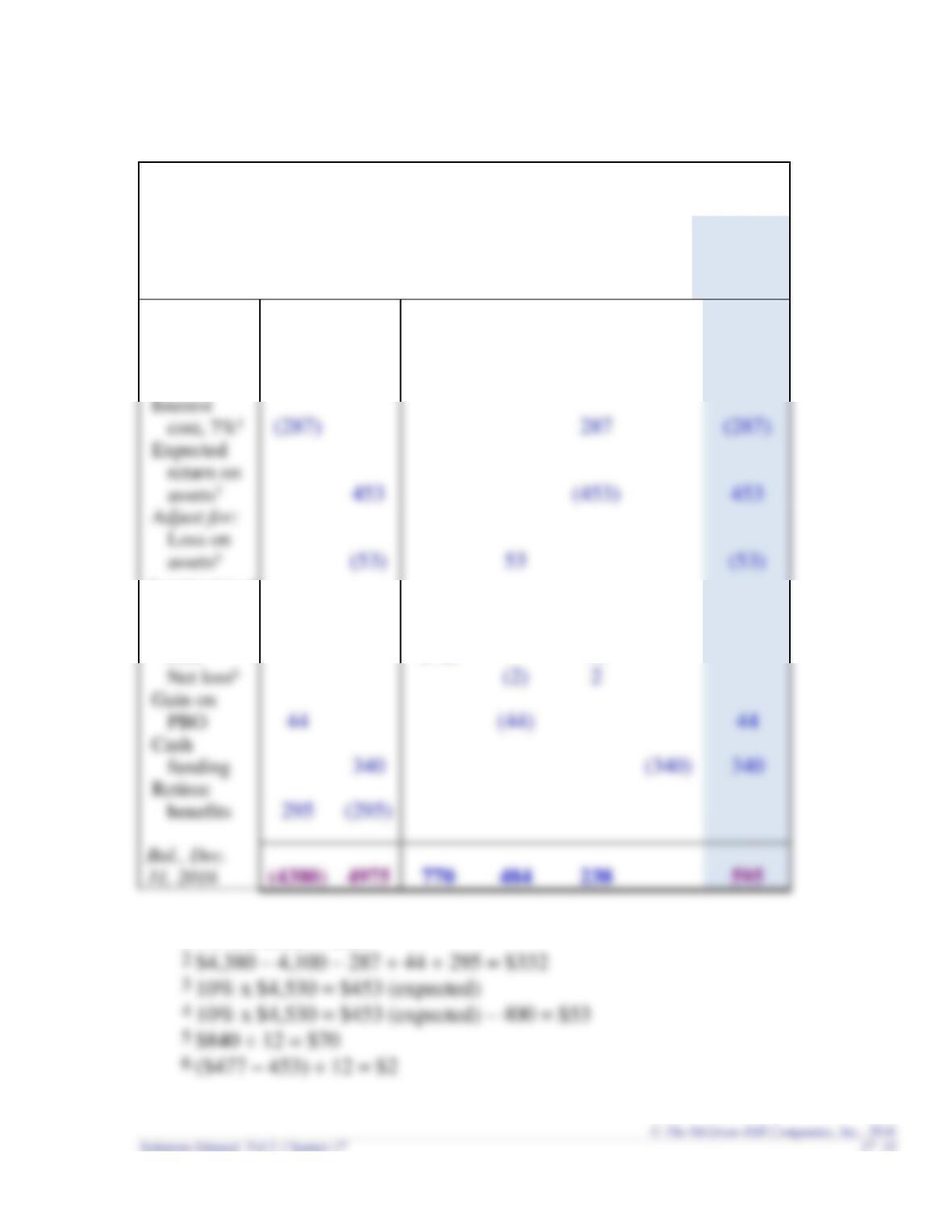

1 7% x $4,100 = $287

Problem 17–16

Requirement 1

Calculation of pension expense: ($ in millions)

Service cost (given) $48

* Amortization of the net loss:

Net loss—AOCI (previous losses exceeded previous gains) $40

To record expense

($ in millions)

Pension expense (total) ……………………………………………………… 57

To record funding and benefit payment

Problem 17–16 (continued)

Requirement 2

To record gains and losses

($ in millions)

Requirement 3

( )s indicate credits; debits

otherwise

($ in millions)

PBO

Plan

Assets

Prior

Service

Cost

–AOCI

Net

Loss

–AOCI

Pension

Expense

Cash

Net

Pension

(Liability)

/ Asset

17–18 Intermediate Accounting, 8e

Problem 17–16 (continued)

Requirement 4

Calculation of pension expense: ($ in millions)

Service cost (given) $38

Interest cost (given) 28

To record expense

($ in millions)

To record funding and benefit payments

($ in millions)