CHAPTER 5

Revenue Recognition and Profitability Analysis

Overview

In Chapter 4 we discussed net income and its presentation in the income statement. In Chapter

5 we focus on revenue recognition, which determines when and how much revenue appears in

the income statement. In Part A of this chapter we discuss the general approach for recognizing

Note to Instructors: Using Chapter 5 to Teach Revenue Recognition

Given the FASB’s new approach to revenue recognition, Chapter 5 was completely revised

and carefully structured to facilitate instruction, starting off by making clear to students how the

five-step revenue recognition process works and then discussing how various business

arrangements affect the five-step process.

• Part A is designed to provide a simple introduction to the five-step revenue-recognition

• Part B follows Part A with in-depth coverage applying the revenue recognition process in

various circumstances. Part B is structured to maximize flexibility by allowing instructors to

cover whatever subset of these topics they prefer. Topics include estimating variable

• Part C likewise maximizes instructor flexibility as it covers accounting for long-term

contracts under ASU 2014-09. Given the importance of long-term contracts, we continue to

Learning Objectives

● LO5-1 State the core revenue recognition principle and the five key steps in applying it.

● LO5-2 Explain when it is appropriate to recognize revenue at a single point in time.

● LO5-3 Explain when it is appropriate to recognize revenue over a period of time.

● LO5-4 Allocate a contract’s transaction price to multiple performance obligations.

● LO5-5 Determine whether a contract exists, and whether some frequently encountered

features of contracts qualify as performance obligations.

● LO5-6 Understand how variable consideration and other aspects of contracts affect the

calculation and allocation of the transaction price.

● LO5-7 Determine the timing of revenue recognition with respect to licenses, franchises, and

other common arrangements.

● LO5-8 Understand the disclosures required for revenue recognition, accounts receivable,

contract assets, and contract liabilities.

● LO5-9 Demonstrate revenue recognition for long-term contracts, both at a point in time

when the contract is completed and over a period of time according to the percentage

completed.

● LO5–10 Identify and calculate the common ratios used to assess profitability.

Lecture Outline

Part A: Introduction to Revenue Recognition

I. Revenue Recognition in General

A. FASB definition: “Revenues are inflows or other enhancements of assets of an entity

or settlements of its liabilities (or a combination of both) from delivering or producing

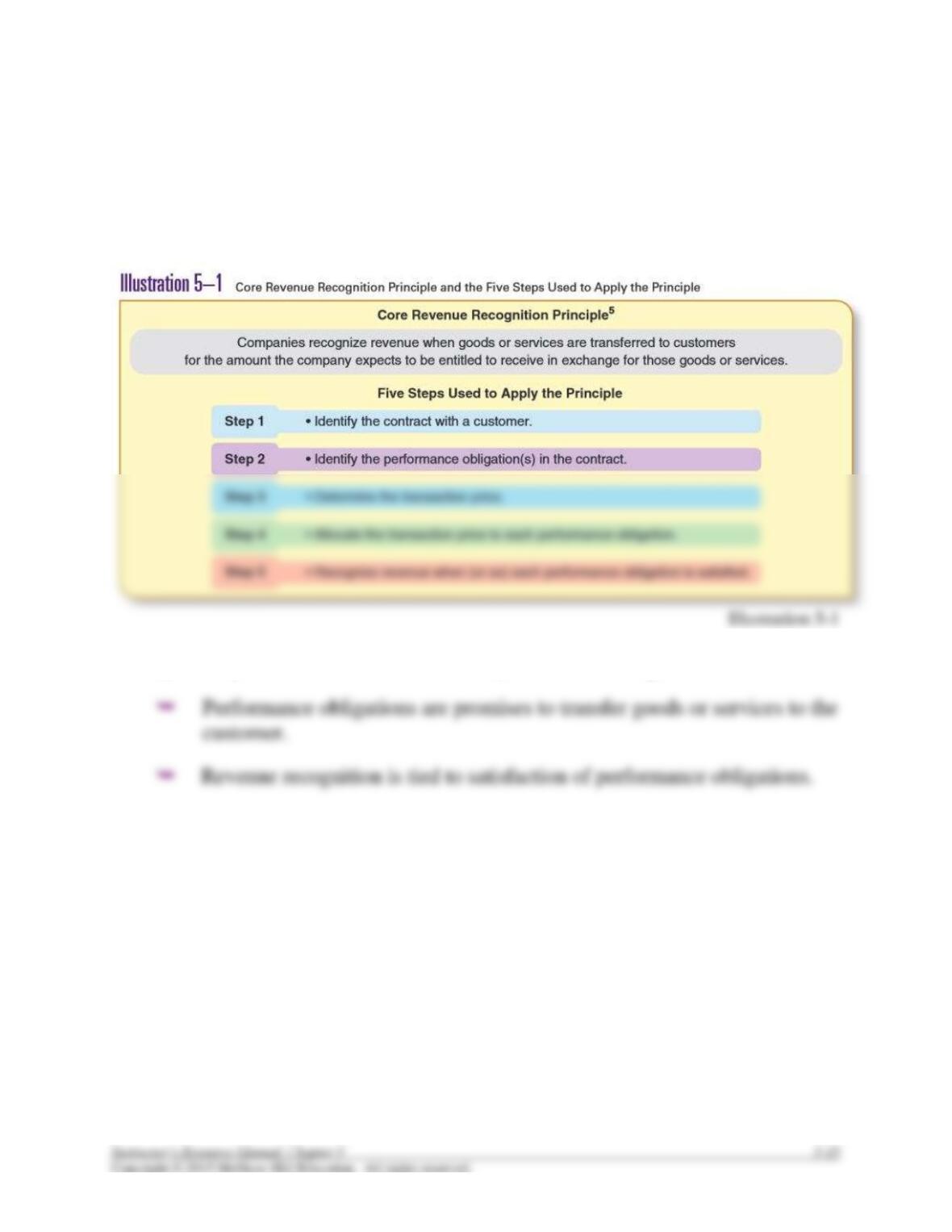

B. To determine how much revenue to recognize and when to recognize it, we apply the

core revenue recognition principal: Companies recognize revenue when goods or

services are transferred to customers for the amount the company expects to be entitled

to receive in exchange for those goods or services. (T5-2)

1. Key concept: the seller has one or more performance obligations.

C. Five steps are used to apply the principle: (T5-2)

1. Identify the contract with a customer.

5. Recognize revenue when (or as) each performance obligation is satisfied.

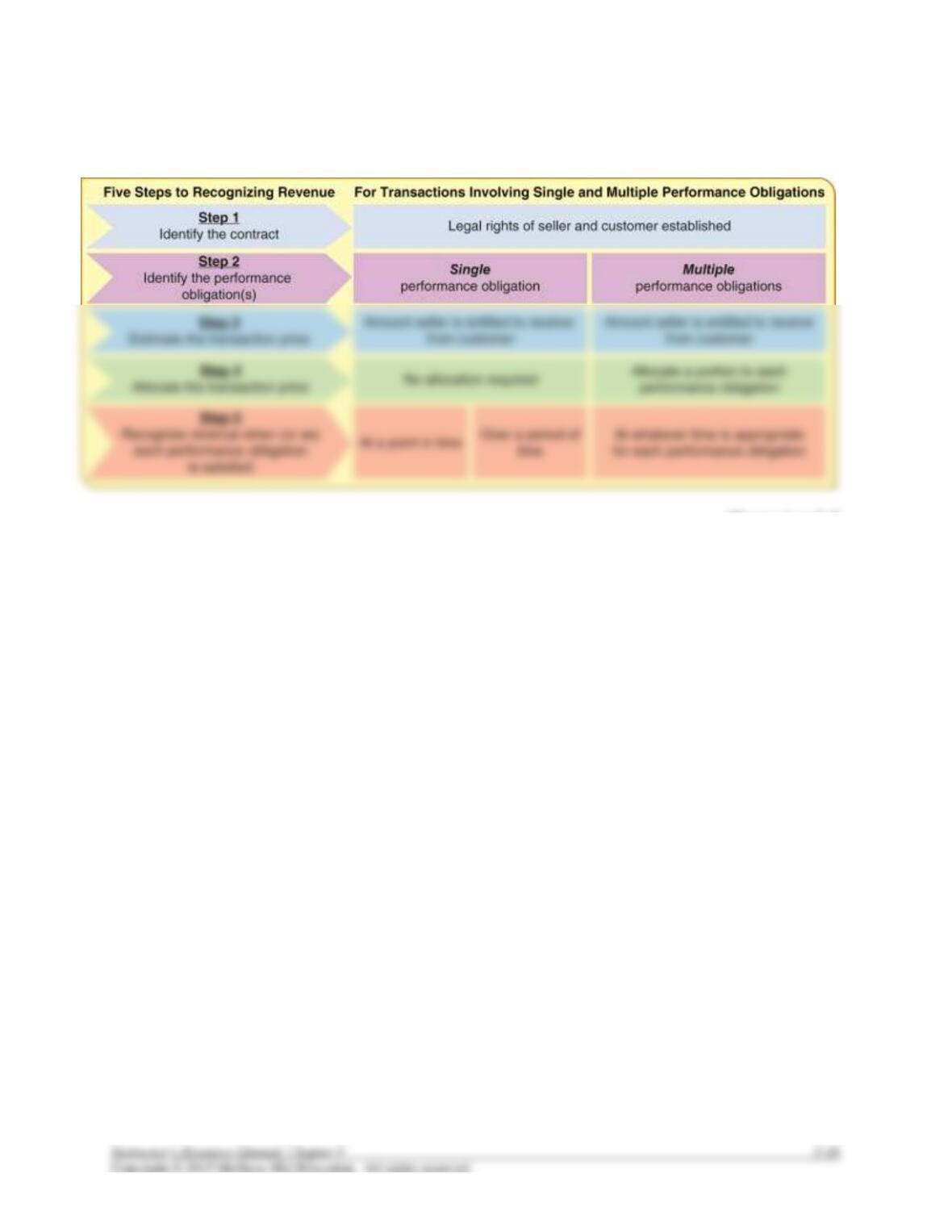

D. Key considerations for each of the five steps that we will learn about: (T5-3)

1. A contract establishes the legal rights and obligations of the seller and the

customer.

3. The transaction price is the amount the seller is entitled to receive from the

customer.

5. Recognize revenue for each performance obligation at a point in time or over

time, depending on how that performance obligation is satisfied.

II. Revenue Recognition at a Point in Time

A. We recognize revenue at a point in time when we don’t qualify for recognizing revenue

over time.

B. The performance obligation is satisfied when control of the goods or services is

transferred from the seller to the customer.

C. Usually transfer of control is obvious, and coincides with delivery.

D. Other indicators of transfer of control: the customer has (T5-4, T5-5)

1. An obligation to pay the seller.

3. Physical possession of the asset.

5. Accepted the asset.

III. Revenue Recognition over a Period of Time

A. Revenue should be recognized over time if goods and services are transferred over time

to the customer.

B. Revenue can be recognized over time if one of the following conditions hold: (T5-6,

T5-7)

2. The customer controls the asset as it is created, or

3. The seller is creating an asset that has no alternative use to the seller, and the

seller has the legal right to receive payment for progress to date.

C. If revenue is recognized over time, we can measure progress towards completion by

using:

2. Output measures. Examples include the passage of time and the amount of

finished product delivered.

IV. Revenue Recognition for Contracts with Multiple Performance Obligations

A. The objective is to separate complex contracts into parts that can be viewed on a stand–

alone basis. Steps 2 and 4 are critical to this process. (T5-8 – T5-12)

B. Step 2: Identify the performance obligation(s) in the contract.

1. A promise to provide a good or service is a performance obligation if the good or

service is distinct from other goods and services in the contract.

2. A good or service is distinct if it is both:

a. Capable of being distinct. The customer could use the good or service on its

C. Step 4: Allocate the transaction price to each performance obligation based on relative

stand-alone selling prices. If stand-along selling prices aren’t observable, estimate

them.

V. Illustration 5-11 Sumarizes the Revenue Recognition Concepts Covered in Part A (T5-

13)

Part B: Special Topics in Revenue Recognition

I. Special Issues for Step 1: Identify the Contract (T5-14, T5-15)

A. A contract is an agreement that creates legally enforceable rights and obligations.

2. Can be oral or written.

B. A contract exists for purposes of revenue recognition only if it

2. has been approved by both the seller and the customer, indicating commitment to

fulfilling their obligations,

4. specifies payment terms, and

5. is probable that the seller will collect the amount it is entitled to receive.

C. A contract does not exist if both of the following are true.

1. neither the seller nor the customer has performed any obligations under the

contract, and

2. both the seller and the customer can terminate the contract without penalty.

II. Special Issues for Step 2: Identify the Performance Obligation(s) (T5-16, T5-17)

A. Examples of common parts of contracts that are not performance obligations:

2. Quality-assurance warranties (it’s part of the performance obligation to deliver

goods and services that are free of defects).

3. Right of return (it’s part of the performance obligation to deliver acceptable

goods and services).

B. Examples of common parts of contracts that are performance obligations:

1. Extended warranties (it’s a separate obligation distinct from delivering

2. Options that provide a material right (a material right is something the customer

wouldn’t get otherwise, so the seller is obligated to provide it).

III. Special Issues for Step 3: Determine the Transaction Price

A. Variable Consideration: (T5-18 – T5-22)

1. Occurs when some of the contract price depends on the outcome of a future

event. Examples:

a. Incentive payments.

2. Estimate variable consideration using either

a. Expected value, calculated as the sum of each possible amount multiplied

3. Sellers only include an estimate of variable consideration in the transaction price

to the extent it is probable that a significant revenue reversal will not occur when

the uncertainty associated with the variable consideration is resolved.

a. Intended to avoid severe revenue overstatements due to estimation error.

b. Indicators that a significant reversal could occur:

i. poor evidence on which to base an estimate,

4. The seller should update estimates of variable consideration (and of whether the

5. Regarding sales with a right of return,

a. If sales are for cash, companies record estimated returns by debiting a

contra-revenue account called “sales returns” and crediting a refund

liability.

B. Principal or Agent (T5-23, T5-24)

1. If the company is a principal, it records revenue equal to the total sales price paid

3. We view the seller as a principal if it obtains control of the goods or services

before they are transferred to the customer. Control is evident if the principal

C. Time Value of Money (T5-23)

1. If payment happens before or after delivery, the transaction has a financing

component. If the financing component is significant, the seller has to account

for it.

2. We presume the financing component is not significant if payment and delivery

are separated by less than one year.

D. Payments by the Seller to the Customer (T5-23)

1. If the seller is purchasing distinct goods or services from the customer at the fair

2. If a seller pays more for distinct goods or services purchased from their customer

IV. Special Issues for Step 4: Allocate the Transaction Price to the Performance

Obligations

A. Three methods are recommended for estimating stand-alone selling prices that are not

observable: (T5-25, T5-26)

1. Adjusted market assessment approach: The seller considers what it could sell the

2. Expected cost plus margin approach: The seller estimates its costs of satisfying a

performance obligation and then adds an appropriate profit margin.

3. Residual approach: The seller estimates an unknown (or highly uncertain) stand–

alone selling price by subtracting the sum of the known or estimated stand-alone

selling prices from the total transaction price. The residual approach is allowed

V. Special Issues for Step 5: Recognize Revenue When (Or As) Each Performance

Obligation Is Satisfied (T5-27, T5-28)

A. Licenses

1. Right of use: Some licenses transfer a right to use the seller’s intellectual

property as it exists when the license is granted. Revenue for those licenses is

B. Franchises

1. The franchisor grants to the franchisee the right to sell the franchisor’s products

and use its name for a specified period of time.

2. A franchise typically involves a license to use the franchisor’s intellectual

C. Bill-and-hold sales

1. Exist when a customer purchases goods but requests that the seller not ship the

product until a later date.

D. Consignment arrangements

1. Exist when a “consignor” physically transfers the goods to the other company

E. Gift Cards

1. Seller records a deferred revenue liability when the card is sold.

VI. Disclosures (T5-29)

A. Income Statement reports revenue, bad debt expense, and interest revenue and interest

expense associated with significant finance components.

B. Balance Sheet

1. Accounts Receivable: Unconditional right to receive payment, depending only

on the passage of time.

3. Contract Liabilities: Deferred revenue.

C. Disclosure:

1. The objective is to help investors understand the nature, amount, timing and

uncertainty of revenues and cash flows.

2. Required disclosures include:

a. Separation of revenue into meaningful categories (product lines, geographic

VII. Illustration 5-22 Sumarizes the Revenue Recognition Special Topics Covered in Part

B (T5-30)

Part C: Accounting for Long-Term Contracts (T5-31)

I. Two of the five revenue recognition steps are especially critical for long-term contracts:

(T5-32)

A. Step 2, “Identify the performance obligation(s) in the contract,” is important because

long-term contracts typically include many products and services that could be viewed

B. Step 5, “Recognize revenue when (or as) each performance obligation is satisfied,” is

important because there can be a considerable difference for long-term contracts

between recognizing revenue over time and recognizing revenue only when the

contract has been completed. Most long-term contracts qualify for revenue recognition

over time, either because

1. the seller is creating an asset that the customer controls as it is completed, or

C. If a contract doesn’t qualify for revenue recognition over time, revenue is recognized

upon completion of the contract. (In prior GAAP, this was called the completed

II. Much of the accounting is the same, regardless of whether revenue is recognized over

time or upon contract completion. (T5-33 – T5-37)

A. All costs of construction are recorded in an asset (inventory) account called

construction in progress.

B. Period billings are credited to billings on construction contract, a contra account to the

construction in progress account. This serves to reduce the book value of the physical

asset (construction in progress) when a financial asset (accounts receivable) is also

recognized; otherwise the project would be double-counted on the balance sheet.

C. Construction in progress is debited for the amount of gross profit recognized. The

same total amount of gross profit is recognized over the life of the contract regardless

of the timing of revenue recognition – the only difference is timing.

D. Recognizing revenue at a point in time is equivalent to recognizing revenue at the

point of delivery, that is, when the project is complete.

E. Recognizing revenue over time allocates a fair share of a project’s revenues and

expenses to each reporting period during construction. How is that fair share

determined? (T5-13)

1. The allocation of project profit is accomplished by estimating progress to date.

2. Progress to date (the percentage of completion) can be estimated as the

3. To determine revenue, the percentage of completion is multiplied by estimated

total revenue to determine revenue that should be recognized to date, and then

the current period’s revenue is determined by subtracting from this amount the

revenue recognized in previous periods.

4. In most cases, the cost of construction equals the construction costs incurred

during the period. Therefore, the same approach used to estimate revenue can be

used to estimate gross profit.

III. Balance sheet effects: Construction in progress is compared to billings on construction

contract. (T5-38)

A. A debit balance indicates costs (plus profits if revenue is recognized over time

IV. Long-term contract losses (T5-39)

A. A loss could occur on a profitable project if the estimated costs to complete were

underestimated in prior periods.

C. Recognized losses on long-term contracts reduce the construction in progress account.

Part D: Profitability Analysis

I. Activity Ratios (T5-40)

A. Activity ratios measure a company’s efficiency in managing its assets.

B. The asset turnover ratio measures a company’s efficiency in using assets to generate

revenue and is calculated by dividing a company’s net sales or revenues by the average

total assets available for use during the period.

C. The receivables turnover ratio offers an indication of how quickly a company is able to

collect its accounts receivable.

2. An extension of this ratio is the average collection period, which is computed by

dividing 365 days by the receivable turnover ratio.

D. The inventory turnover ratio measures a company’s efficiency in managing its

investment in inventory.

1. The ratio is calculated by dividing the period’s cost of goods sold by the average

II. Profitability Ratios (T5-41)

A. Profitability ratios assist in evaluating various aspects of a company’s profit-making

activities.

B. The profit margin on sales measures the amount of net income achieved per sales

dollar and is computed by dividing net income by net sales.

C. The return on assets (ROA) indicates a company’s overall profitability.

1. It is calculated by dividing net income by average total assets.

III. DuPont Framework (T5-42)

A. The DuPont Framework helps identify how profitability, activity, and financial

leverage trade off to determine return to shareholders.

Appendix (Covering Key Areas of GAAP Superceded by ASU 2014-09) (T5-43)

I. Revenue Recognition in General

A. The realization principle requires that two criteria be satisfied before revenue can be

recognized: (T5-44)

B. Staff Accounting Bulletin No.’s 101 and 104 summarized the SEC’s views on revenue

recognition. The bulletins provide additional criteria for judging whether or not the

realization principle is satisfied:

2. Delivery has occurred or services have been rendered.

4. Collectibility is reasonably assured.

C. IFRS revenue recognition concepts focus on transfer of economic benefits. IFRS

allows revenue to be recognized when the following conditions have been satisfied:

1. The amount of revenue and costs associated with the transaction can be

measured reliably.

3. (for sales of goods) the seller has transferred to the buyer the risks and rewards

of ownership, and doesn’t effectively manage or control the goods.

5. These requirements are similar to U.S. GAAP, and revenue typically is

recognized at a similar point under IFRS and U.S. GAAP. (T5-45)

D. Under prior GAAP, it was useful to characterize revenue from the perspective of

the point of delivery. (T5-46, 47)

E. Revenue recognition prior to delivery is covered in the main chapter (that is,

revenue recognition over time for long-term contracts).

1. Under prior GAAP, use of the percentage-of-completion method was required

II. Revenue Recognition after Delivery

A. Significant uncertainties about cash collection could cause a delay in recognizing

revenue from the sale of a product or a service.

B. Installment sales

1. Revenue recognition for most installment sales takes place at the point of

2. When exceptional uncertainty exists, two accounting methods are available:

3. The installment sales method recognizes gross profit by applying the gross profit

percentage on the sale to the amount of cash actually received. (T5-49)

4. The cost recovery method defers all gross profit recognition until cash equal to

the cost of the item sold has been received. (T5-50)

C. Under IFRS, IAS No. 11 governs revenue recognition for long-term construction

contracts.

(T5-17)

1. Like U.S. GAAP, the international standard requires the use of percentage-of-

completion accounting when estimates can be made precisely.

2. Unlike U.S. GAAP, the international standard requires the use of the cost

recovery method rather than the completed contract method when estimates

cannot be made precisely enough to allow percentage-of-completion accounting.

a. Under the cost recovery method, contract costs are expensed as incurred,

III. Industry-Specific Revenue Issues

A. Multiple-element arrangements (T5-51)

1. If a software arrangement (sale) includes multiple elements, the revenue from the

2. More generally, if an arrangement contains multiple elements, revenue should be

allocated to individual deliverables if that qualify for separate revenue

3. IAS No. 18 is the general revenue recognition standard in IFRS. There is not

much guidance about multiple-element contracts or industry-specific revenue

recognition in IFRS.

B. In a franchise sale, the fees to be paid by the franchisee to the franchisor usually

comprise (1) the initial franchise fee, and (2) continuing franchise fees. (T5-52)

1. GAAP requires that the franchisor has substantially performed the services

2. Continuing franchise fees are paid to the franchisor for continuing rights as well

as for advertising and promotion and other services over the life of the agreement

and are recognized by the franchisor as revenue in the period received, which

corresponds to the periods the services are performed.

PowerPoint Slides

A PowerPoint presentation of the chapter is available in the Connect library.

Teaching Transparency Masters

The following can be reproduced on transparency film as they appear here, or you

DEFINITION OF REVENUE

➢ According to the FASB, “Revenues are inflows or other enhancements of assets

of an entity or settlements of its liabilities (or a combination of both) from

T5-1

CORE REVENUE RECOGNITION PRINCIPLE

AND THE 5 STEPS TO IMPLEMENTING IT

➢ Key concept: The seller has one or more performance obligations

T5-2

OVERVIEW OF THE 5 STEPS

Illustration 5-2

T5-3

RECOGNIZING REVENUE AT A SINGLE POINT IN TIME

➢ We recognize revenue at a point in time when we don’t qualify for recognizing

revenue over time.

Criteria for Recognizing Revenue at a Point in Time

The customer is more likely to control a good or service if the customer has:

• An obligation to pay the seller.

Illustration 5-3

T5-4

RECOGNIZING REVENUE AT A SINGLE POINT IN TIME

(continued)

TrueTech Industries sells the Tri-Box, a gaming console that allows users to play

video games individually or in multi-player environments over the Internet. A

Tri-Box is only a gaming module and includes no other goods or services. When

should TrueTech recognize revenue for the following sale of 1,000 Tri-Boxes to

CompStores?

• December 20, 2015: CompStores orders 1,000 Tri-Boxes at a price of $240

each, promising payment within 30 days after delivery. True Tech has

• January 1, 2016: TrueTech delivers 1,000 Tri-Boxes to CompStores, and

title to the Tri-Boxes transfers to CompStores. TrueTech has delivered the

Tri-Boxes, and CompStores has accepted delivery, so CompStores has physical

• January 25, 2016: TrueTech receives $240,000 from CompStores. This

transaction does not affect revenue. We recognize revenue when performance

T5-5

1 TrueTech also would debit cost of goods sold and credit inventory to recognize the cost of inventory sold.

RECOGNIZING REVENUE OVER TIME

➢ We recognize revenue over time when performance obligations are satisfied

over time. That is the case if we transfer goods and services over time.

Criteria for Recognizing Revenue over Time

Revenue is recognized over time if either:

• The customer consumes the benefit of the seller’s work as it is performed,

as when a company provides cleaning services to a customer for a period of

time, or

Illustration 5-5

T5-6

RECOGNIZING REVENUE

OVER A PERIOD OF TIME

TrueTech Industries sells one-year subscriptions to the Tri-Net multiuser platform

of Internet-based games. TrueTech sells 1,000 subscriptions for $60 each on

January 1, 2016. TrueTech has a single performance obligation – to provide a

service to subscribers by allowing them access to the gaming platform for one

year. Because Tri-Net users consume the benefits of access to that service over

time, under the first criterion in Illustration 5-5 TrueTech recognizes revenue from

the subscriptions over the one-year time period.

On January 1, 2016, TrueTech records the following journal

entry:

1/31

2/28

12/31

12/31

1/1

-0-

1/31

2/28

5,000

12/31

5,000

12/31

60,000

Illustration 5-6

T 5-7

Deferred

Revenue

1/1

60,000

Service

Revenue