Intermediate Accounting, 8/e 5–141

Problem 5–19 (continued)

2017

Installment receivables …………………………………………… 400,000

Inventory …………………………………………………………… 280,000

Requirement 3

Date

Cash Collected

Cost Recovery

Gross Profit

2016

2016 sales

$120,000

$120,000

– 0 –

2016 sales

2017 sales

$250,000

$210,000

Problem 5–19 (concluded)

2016

Installment receivables …………………………………………… 300,000

Cash …………………………………………………………………….. 120,000

2017

Installment receivables …………………………………………… 400,000

Cash …………………………………………………………………….. 250,000

Intermediate Accounting, 8/e 5–143

Problem 5–20

Requirement 1

Total profit = $500,000 – 300,000 = $200,000

Installment sales method: Gross profit % = $200,000 ÷ $500,000 = 40%

8/31/16

8/31/17

8/31/18

8/31/19

8/31/20

Cash collections

$100,000

$100,000

$100,000

$100,000

$100,000

$200,000

– 0 –

– 0 –

– 0 –

– 0 –

– 0 –

– 0 –

– 0 –

$100,000

$100,000

Problem 5–20 (continued)

Requirement 2

Point of

Delivery

Installment

Sales

Cost Recovery

Installment receivable

500,000

Sales revenue

500,000

Cost of goods sold

300,000

Inventory

300,000

Installment receivable

500,000

500,000

Inventory

300,000

300,000

Deferred gross profit

Cash

100,000

100,000

100,000

Installment receivable

100,000

100,000

100,000

Deferred gross profit

100,000

Intermediate Accounting, 8/e 5–145

Problem 5–20 (concluded)

Requirement 3

Point of

Delivery

Installment

Sales

Cost

Recovery

December 31, 2016

Assets

Installment receivables

400,000

400,000

400,000

Problem 5–21

Requirement 1

All jobs consist of four equal payments: one payment when the job is completed and

three payments over the next three years.

Bluebird:

Job completed in 2014, so down payment made in 2014, another payment in 2015,

and two payments remain. $400,000 gross receivable at 1/1/2016 implies

PitStop:

Job completed in 2013, so down payment made in 2013, another payment in 2014,

another in 2015, and one payment remains. $150,000 gross receivable at 1/1/2016

Problem 5–21 (concluded)

Intermediate Accounting, 8/e 5–147

Totals:

Requirement 2

If Dan is focused on 2016, he would not be happy with a switch to the installment

sales method, because that would produce gross profit of only $102,500, which is

Problem 5–22

Requirement 1

Year

Gross profit recognized

2016

– 0 –

2017

– 0 –

2018

Requirement 2

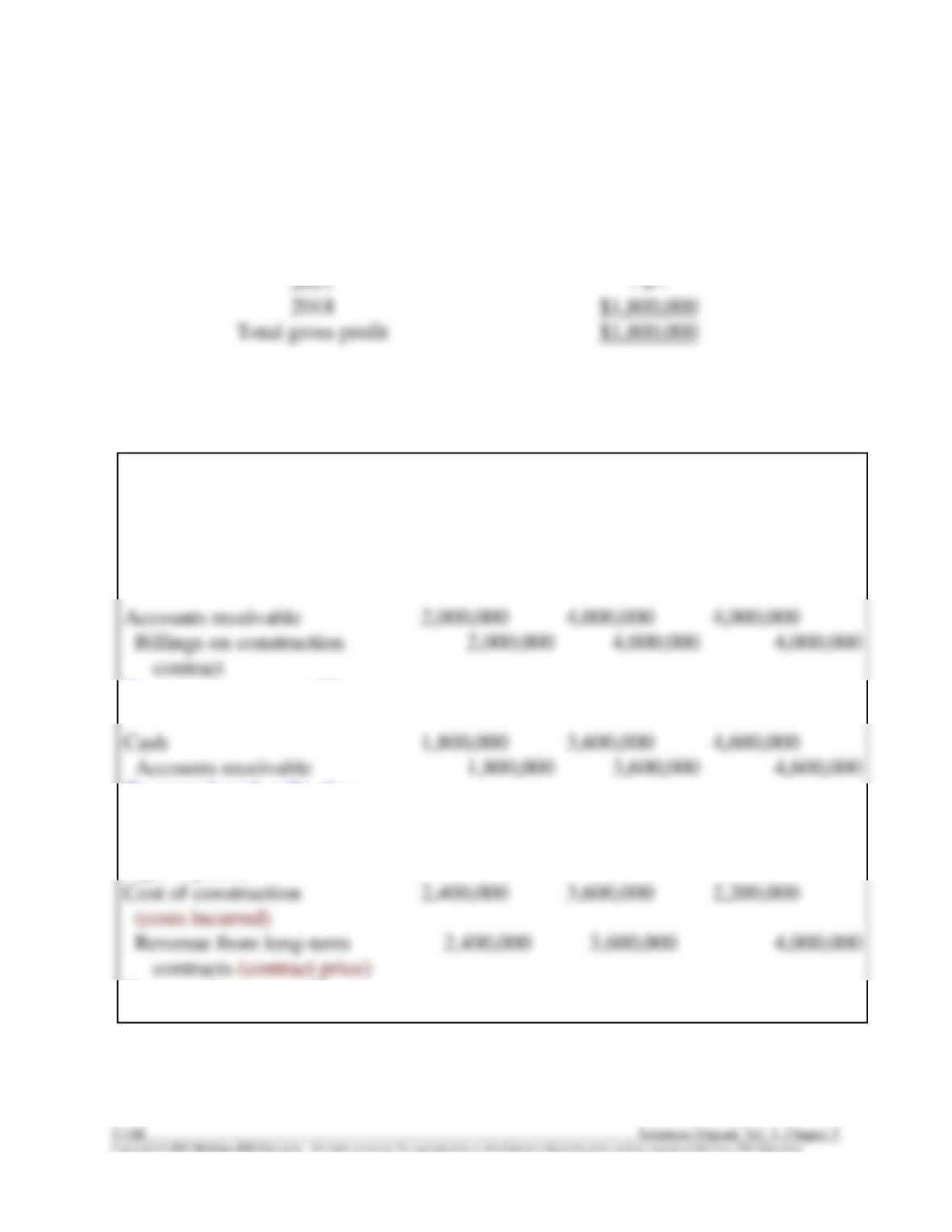

2016

2017

2018

Construction in progress

2,400,000

3,600,000

2,200,000

Various accounts

2,400,000

3,600,000

2,200,000

To record construction costs

Accounts receivable

2,000,000

4,000,000

4,000,000

To record progress billings

Cash

1,800,000

3,600,000

4,600,000

To record cash collections

Construction in progress

(gross profit)

1,800,000

To record gross profit

Intermediate Accounting, 8/e 5–149

Problem 5–22 (concluded)

Requirement 3

Balance Sheet

2016

2017

Current assets:

Accounts receivable

$ 200,000

$ 600,000

$2,400,000

$6,000,000

400,000

Requirement 4

2016 2017 2018

Costs incurred during the year $2,400,000 $3,800,000 $3,200,000

Requirement 5

2016 2017 2018

Costs incurred during the year $2,400,000 $3,800,000 $3,900,000

Estimated costs to complete

Problem 5–23

Requirement 1

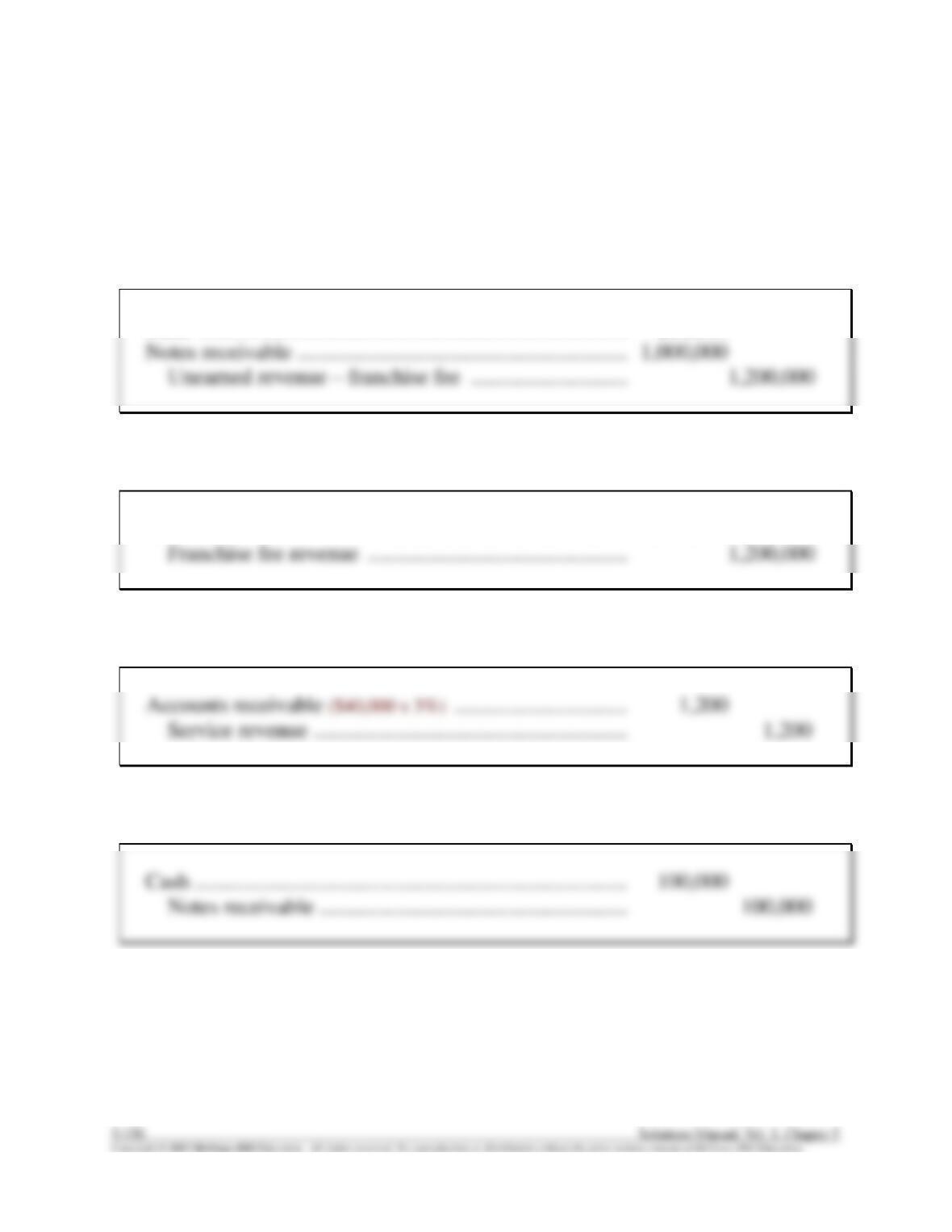

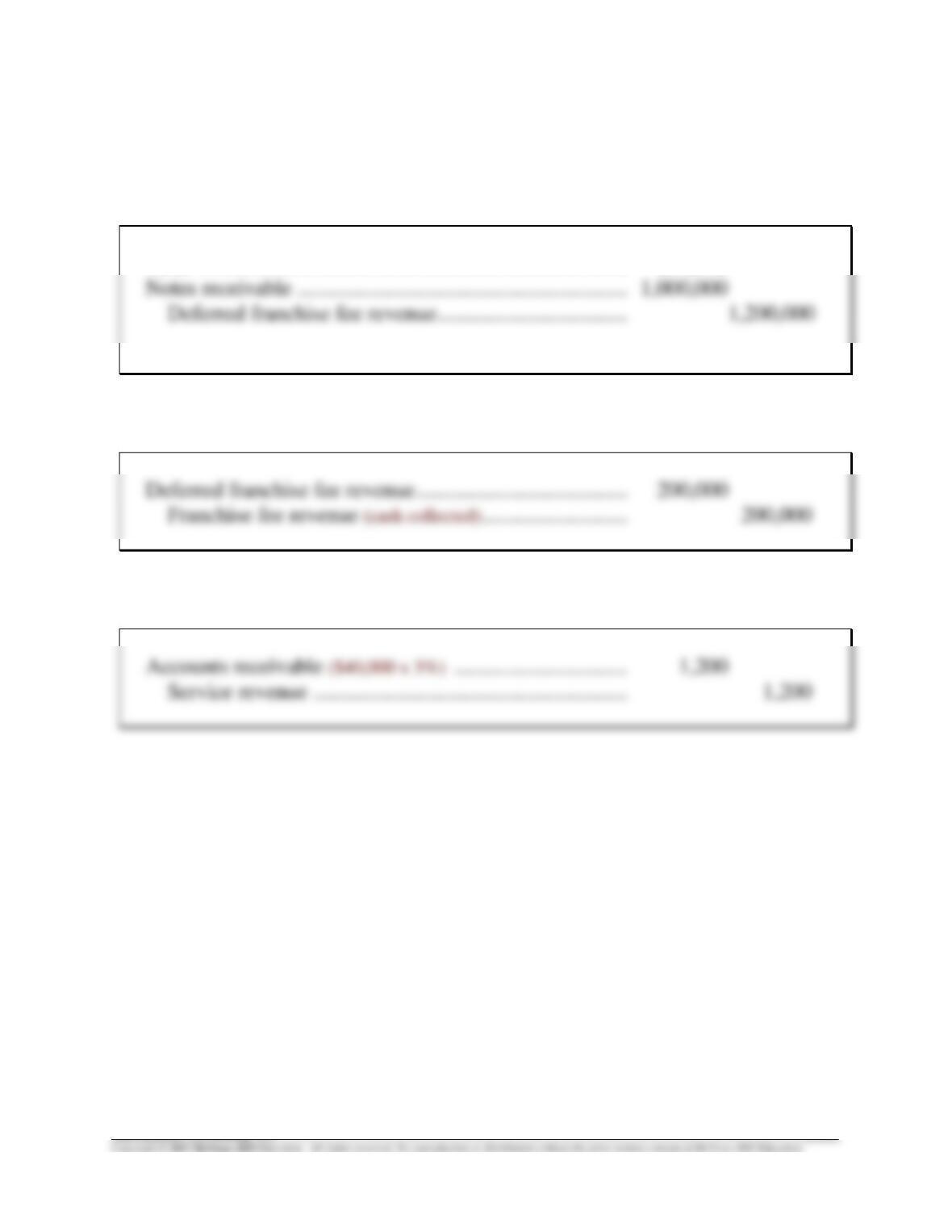

a. January 30, 2016

Cash ……………………………………………………………………. 200,000

b. September 1, 2016

Unearned revenue – franchise fee …………………………... 1,200,000

c. September 30, 2016

d. January 30, 2017

Intermediate Accounting, 8/e 5–151

Problem 5–23 (continued)

Requirement 2

a. January 30, 2016

Cash ……………………………………………………………………. 200,000

b. September 1, 2016

c. September 30, 2016

Problem 5-23 (concluded)

d. January 30, 2017

Cash …………………………………………………………………….. 100,000

Requirement 3

Balance Sheet

At December 31, 2016

Current assets:

Current liabilities:

Installment notes receivable

$ -0-

Intermediate Accounting, 8/e 5–153

CASES

Research Case 5–1

(Note: This case requires the student to reference a journal article.)

1.

Abuse

Explanation

1. Cutoff manipulation

The company either closes their books early (so some

2. Deferring too much

The company has an arrangement under which

3. Bill-and-hold sale

The company records sales even though it hasn’t yet

delivered the goods to the customer.

4. Right-of-return sale

The company sells to distributors or other customers

2. Manipulating estimates of percentage complete in order to manipulate gross

Judgment Case 5–2

Determining whether Toys4U satisfies the performance obligation requires the

company to consider indicators of whether McDonald’s has obtained control of the

dolls. Management should evaluate these indicators individually and in combination

to decide whether control has been transferred. The indicators include, but are not

limited to the following:

1. The customer has accepted the asset. There is no acceptance provision

3. The customer has physical possession of goods. McDonald’s has possession

4. The customer has the risks and rewards of ownership. Given that

5. The customer has an obligation to pay the seller. In this case, McDonald’s

In this case, Toys4U has not transferred control upon delivery because

McDonald’s has not accepted the asset, does not have the risks and rewards of

Intermediate Accounting, 8/e 5–155

Judgment Case 5–3

In this case, Kerry obtained the access code for Level I on December 1, meaning

that Kerry has obtained the control of the right to use the software for Level I on that

date. On that date Cutler should recognize $50 of revenue for Level I.

Ethics Case 5–4

Discussion should include these elements.

Facts:

Horizon Corporation, a computer manufacturer, reported profits from 2011

through 2014, but reported a $20 million loss in 2015 due to increased competition.

Ethical Dilemma:

Is Jim’s obligation to challenge the memo of the CFO and provide useful

information to users of the financial statements greater than the obligation to prevent

a company loss in 2016 that may lead to bankruptcy?

Who is affected?

Jim Fielding

CFO and other managers

Intermediate Accounting, 8/e 5–157

Judgment Case 5-5

Scenario 1: The terms of the contract and all the related facts and circumstances

indicate that Star controls the room as it is built. Crown is entitled to receive

payments throughout the contract as evidenced by the required progress payments

throughout the construction process.

Scenario 2: The terms of the contract and all the related facts and circumstances

indicate that Star does not obtain control of the gym until it is delivered. If the

Scenario 3: The terms of the contract and all the related facts and circumstances

indicate that Coco has the ability to direct the use of, and receive the benefit from,

Scenario 4: The terms of the contract and all the related facts and circumstances

indicate that Edwards, the customer, obtains control of the apartment upon

Judgment Case 5-6

The license granted by Pfizer is not a performance obligation, because it is not

separately identifiable. The only way to exploit the license is by utilizing ongoing

Intermediate Accounting, 8/e 5–159

Communication Case 5–7

The critical question that student groups should address is how to account for

punches in the punch card and the option to possibly receive a free ice cream cone

that it provides. Students should benefit from participating in the process, interacting

first with other group members, then with the class as a whole.

The preferred solution should include the idea that the sale of an ice cream cone

to a person who has a card involves two performance obligations:

1. Providing the ice cream cone

2. Eventually providing an additional ice cream cone, if and when a customer

reaches 10 punches on a card and redeems the card for the free cone.

Students should recognize that each punch on the punch card contributes to an

option to receive a future ice cream cone. That option is capable of being distinct

because it could be sold or provided separate from selling a cone, and it is separately