Long-Term Notes

(continued)

At Each of the Six Interest Dates

Skill Graphics (Borrower)

At Maturity

Skill Graphics (Borrower)

T14-11 (continued)

14-22 Intermediate Accounting, 8/e

Note Exchanged for Assets or Services

Occasionally the stated interest rate is not indicative of the

market rate at the time a note is negotiated. The value of the

asset (cash or noncash) or service exchanged for the note

establishes the market rate.

The accounting treatment is the same whether the amount is

T14-12

Note Exchanged for Assets or Services

(continued)

At the Purchase Date (January 1)

Skill Graphics (Buyer / Issuer)

Machinery (cash price) …………………………………… 666,633

At the First Interest Date (June 30)

Skill Graphics (Borrower)

Interest expense (market rate x outstanding bal.) …………. 46,664

T14-12 (continued)

14-24 Intermediate Accounting, 8/e

INSTALLMENT NOTES

Notes often are paid in installments, rather than a single amount

at maturity.

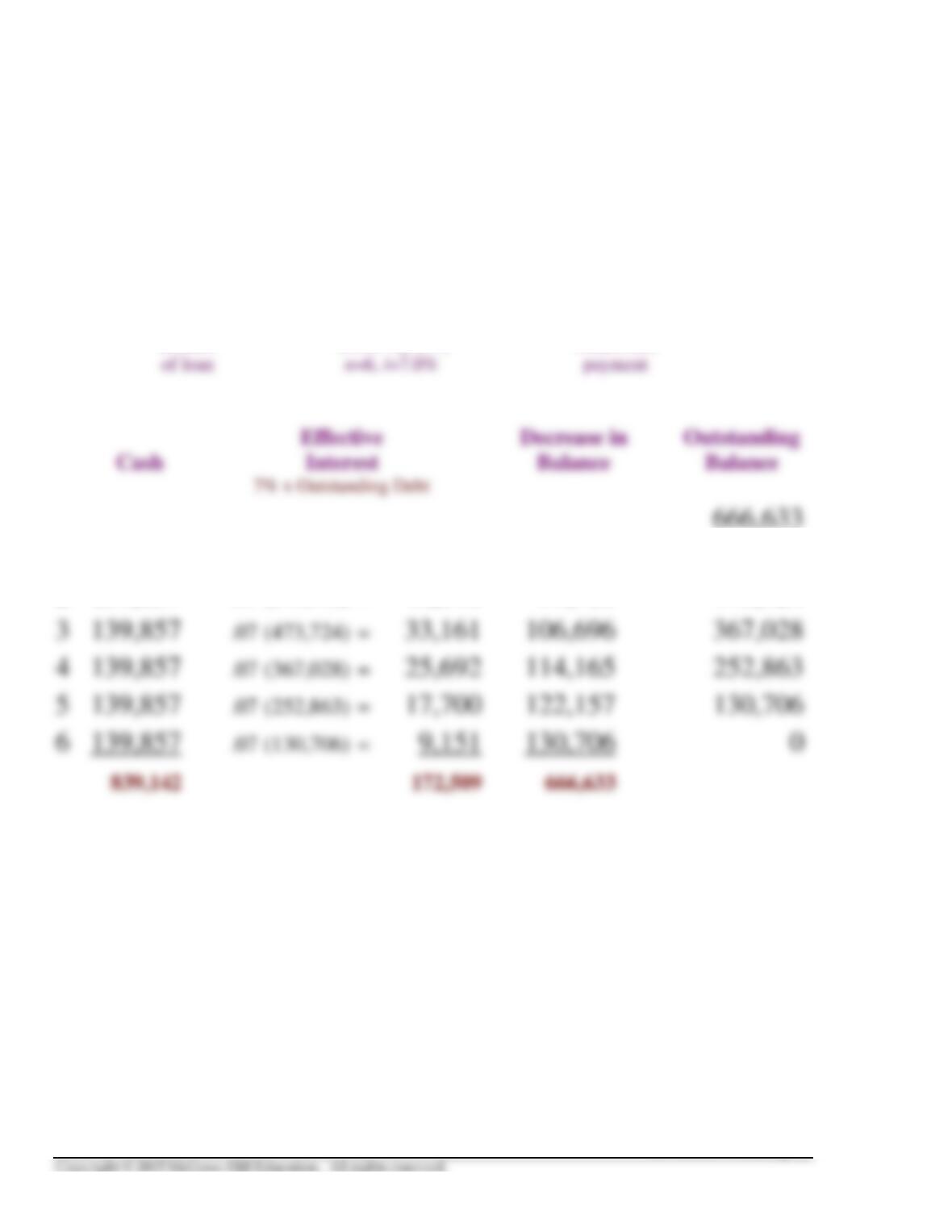

$666,633 ÷ 4.76654 = $139,857

amount (from Table 4) installment

1 139,857 .07 (666,633) = 46,664 93,193 573,440

2 139,857 .07 (573,440) = 40,141 99,716 473,724

T14-13

INSTALLMENT NOTES

(continued)

Skill Graphics (Buyer / Issuer)

Machinery …………………………..……………………. 666,633

Each payment includes both an amount that represents interest

and an amount that represents a reduction of principal.

At the First Interest Date (June 30)

Skill Graphics (Borrower)

Interest expense (market rate x outstanding bal.) ………. 46,664

14-26 Intermediate Accounting, 8/e

FINANCIAL STATEMENT DISCLOSURES

Disclosure requirements include:

• the fair value of all financial instruments

• For all LT liabilities, the aggregate amounts maturing and

sinking fund requirements (if any) for each of the next five

years.

Microsoft’s annual report for the fiscal year ended June 30, 2013

stated:

Maturities of our long-term debt for each of the next five years and

thereafter are as follows:

(In millions)

Year Ending June 30,

2014 $ 3,000

2015 0

EARLY EXTINGUISHMENT

Illustration – On January 1, 2017, Masterwear Industries called

its $700,000, 12% bonds when their book value was $676,290.

T14-15

14-28 Intermediate Accounting, 8/e

FAIR VALUE OPTION

A. A company is not required to, but has the option to, value

some or all of its financial assets and liabilities, including

bonds and notes, at fair value.

Illustration

HSA, Inc. chooses the fair value option for its bonds. Bonds

issued for $180,000 on July 1 were priced at $183,000 on

T14-16

APPENDIX A

BONDS ISSUED BETWEEN INTEREST DATES

All bonds sell at their price plus any interest that has accrued

since the last interest date.

Illustration – On March 1, 2016, Masterwear Industries issued

$700,000 of 12% bonds, dated January 1. Interest of $42,000

is payable semiannually on June 30 and December 31. The

bonds mature in three years. The entire bond issue was

T14-17

14-30 Intermediate Accounting, 8/e

BONDS ISSUED BETWEEN INTEREST DATES

(continued)

The issuer incurs interest expense, and the investor

recognizes interest revenue, for only the four months

the bonds are outstanding.

At the First Interest Date (June 30)

Masterwear (Issuer)

Interest expense (6 mo. – 2 mo. = 4 mo.) ……… 28,000

INTERNATIONAL FINANCIAL REPORTING STANDARDS

Distinction between debt and equity for preferred stock.

Differences in the definitions and requirements under these

standards can result in the same instrument being classified

T14-18

14-32 Intermediate Accounting, 8/e

INTERNATIONAL FINANCIAL REPORTING STANDARDS

Convertible bonds. Under IFRS, convertible debt is

T14-19

APPENDIX B

TROUBLED DEBT RESTRUCTURING

When changing the original terms of a debt agreement is

motivated by financial difficulties experienced by the debtor

T14-20

14-34 Intermediate Accounting, 8/e

DEBT IS SETTLED

Illustration – First Prudent Bank agrees to settle Brillard’s $30

million debt in exchange for property having a fair market value

of $20 million. The book value of the property on Brillard’s

books is $17 million

($ in millions)

Land ($20 million minus $17 million) …………………….. 3

DEBT CONTINUED, WITH MODIFIED TERMS:

WHEN TOTAL CASH PAYMENTS ARE

LESS THAN THE BOOK VALUE OF THE DEBT

Illustration – Brillard Properties owes First Prudent Bank $30

million, under a 10% note with 2 years remaining to maturity.

Due to financial difficulties of the developer, the previous year’s

interest ($3 million) was not paid. First Prudent Bank agrees to:

(1) forgive the interest accrued from last year,

(2) reduce the remaining two interest payments to $2 million

each,

(3) reduce the principal to $25 million.

Analysis:

Book value: $30 million + 3 million = $33 million

Future payments: ($2 million x 2) + $25 million = 29 million

Gain $ 4 million

($ in millions)

T14-22