Exercise 14–4

1. January 1, 2016

Interest $4,000,000¥ x 11.46992 * = $45,879,680

2. June 30, 2016

3. December 31, 2016

14–22 Intermediate Accounting, 8/e

Exercise 14–5

1. Liability at December 31, 2016

Bonds payable (face amount) ……………………………….. $320,000,000

2. Interest expense for year ended December 31, 2016

3. Statement of cash flows for year ended December 31, 2016

Myriad would report the cash inflow of $283,294,720*** from the sale of the

Exercise 14–5 (concluded)

Calculations:

January 1, 2016***

Cash (price given) ………………………………………………. 283,294,720

14–24 Intermediate Accounting, 8/e

Exercise 14–6

1. June 30, 2016

2. December 31, 2016

3. June 30, 2017

Exercise 14–7

1. Price of the bonds at January 1, 2016

Interest $7,500,000¥ x 13.76483 * = $103,236,225

2. January 1, 2016

3. June 30, 2016

4. December 31, 2023

Interest expense ($7,500,000 + 688,243) …………………….. 8,188,243

14–26 Intermediate Accounting, 8/e

Exercise 14–8

1. January 1, 2016

Interest $7,500,000¥ x 13.76483 * = $103,236,225

Principal $150,000,000 x 0.17411 ** = 26,116,500

2. June 30, 2016

3. December 31, 2023

Cash (5% x $150,000,000) …………………………………….. 7,500,000

Exercise 14–9

1. Price of the bonds at January 1, 2016

Interest $18,000¥ x 6.87396 * = $123,731

2. January 1, 2016

3. Amortization schedule

Cash Effective Increase in Outstanding

Payment Interest Balance Balance

3% x Face Amount 3.5% x Outstanding Balance Discount Reduction

579,377

1 18,000 .035 (579,377) = 20,278 2,278 581,655

14–28 Intermediate Accounting, 8/e

Exercise 14–9 (concluded)

4. June 30, 2016

Interest expense (3.5% x $579,377) ……………….. 20,278

December 31, 2016**

Interest expense (3.5% x [$579,377 + 2,278]) …. 20,358

5. Liability at December 31, 2016

Bonds payable (face amount) ……………………………….. $600,000

6. Interest expense for year ended December 31, 2016

7. December 31, 2019

Interest expense (3.5% x $597,099) ……………….. 20,901*

Exercise 14–10

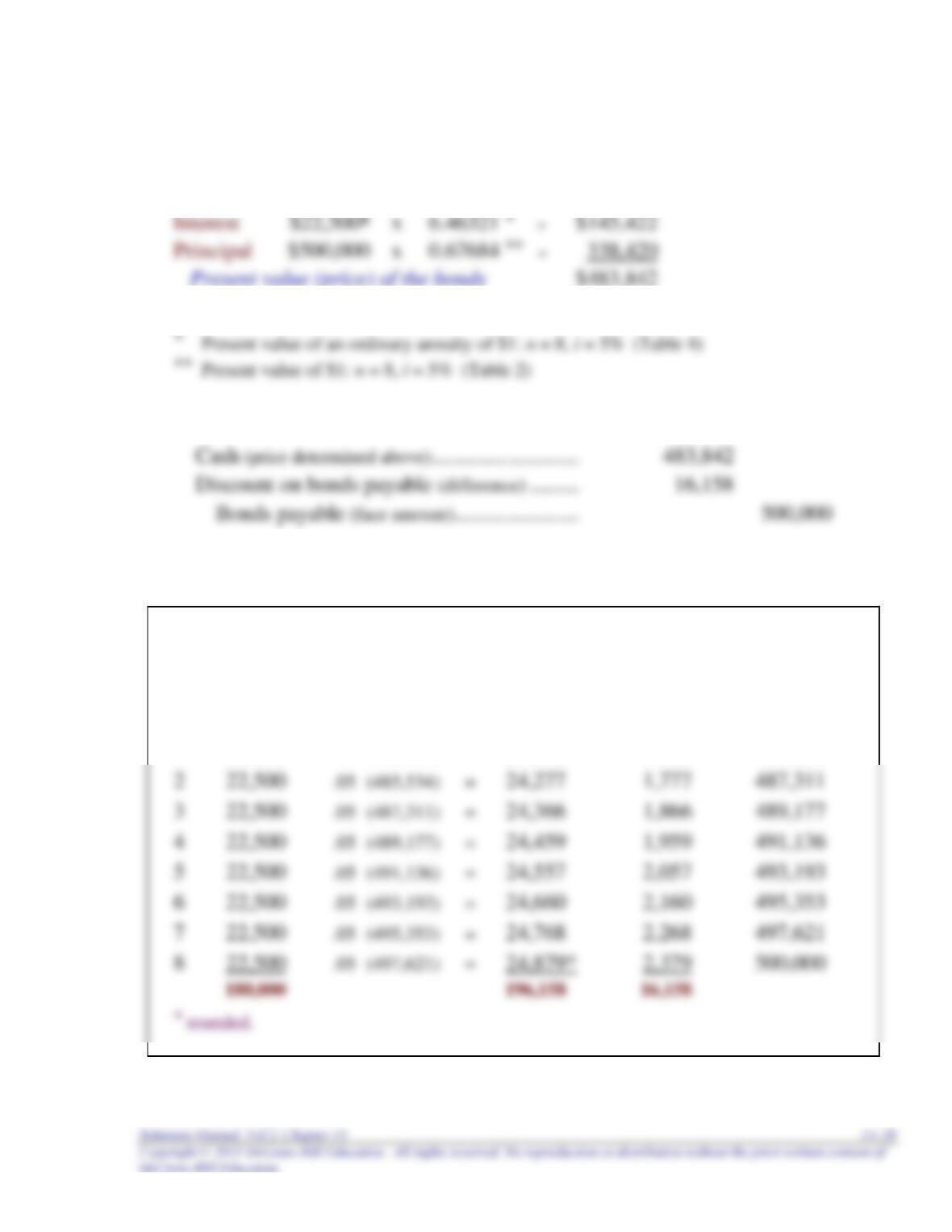

1. Price of the bonds at January 1, 2016

¥ 4.5% x $500,000

2. January 1, 2016

3. Amortization schedule

Cash Effective Increase in Outstanding

Payment Interest Balance Balance

4.5% x Face Amount 5% x Outstanding Balance Discount Reduction

483,842

1 22,500 .05 (483,842) = 24,192 1,692 485,534

14–30 Intermediate Accounting, 8/e

Exercise 14–10 (concluded)

4. June 30, 2016

5. December 31, 2019

Interest expense (5% x $497,621) ………………….. 24,879*

Exercise 14–11

1. February 1, 2016

2. July 31, 2016

3. December 31, 2016

4. January 31, 2017

Interest expense (1/6 x 5% x [$731,364 + 568]) .. 6,100*

14–32 Intermediate Accounting, 8/e

Exercise 14–12

1. March 1, 2016

2. August 31, 2016

3. December 31, 2016

4. February 28, 2017

Interest expense (2/6 x $21,150) …………………….. 7,050

Exercise 14–13

1. January 1, 2016

2. June 30, 2016

3. December 31, 2016

4. December 31, 2016

Federal will report the bonds among its liabilities in the December 31, 2016,

14–34 Intermediate Accounting, 8/e

Exercise 14–14

1. National Equipment Transfer Corporation

Cash (priced at par) ………………………………….. 200,000,000

2. National Equipment Transfer Corporation

Interest expense …………………………..……………… 7,460,000

Exercise 14–15

The 2016 interest expense is overstated by the extra interest recorded in

February. Similarly, retained earnings is overstated the same amount because 2015

interest expense was understated when the accrued interest was not recorded.

To correct the error:

Retained earnings ………………………………………………….. 61,000

2016 adjusting entry:

Interest expense (5/6 x $73,200) ……………………………. 61,000

14–36 Intermediate Accounting, 8/e

Exercise 14–16

Requirement 1

The error caused both 2014 net income and 2015 net income to be overstated, so

retained earnings is overstated by a total of $85,000. Also, the notes payable would be

understated by the same amount. Remember, the entry to record interest is:

Interest expense ……………………………………………………….…………….. xxx

Requirement 2

Requirement 3

The financial statements that were incorrect as a result of the error would be

Exercise 14–17

Requirement 1

Interest $24,000¥ x 2.40183 * = $ 57,644

Requirement 2

Cash Effective Increase in Outstanding

Payment Interest Balance Balance

4% x Face Amount 12% x Outstanding Balance Discount Reduction

484,712

1 24,000 .12 (484,712) = 58,165 34,165 518,877

Requirement 3

Interest expense (market rate x outstanding balance) …………….. 58,165

Discount on notes payable (difference) ……………………….. 34,165

14–38 Intermediate Accounting, 8/e

Exercise 14–18

Requirement 1

Interest $24,000¥ x 2.40183 * = $ 57,644

Requirement 2

Cash Effective Increase in Outstanding

Payment Interest Balance Balance

4% x Face Amount 12% x Outstanding Balance Discount Reduction

484,712

1 24,000 .12 (484,712) = 58,165 34,165 518,877

Exercise 14–18 (concluded)

Requirement 3

Cash (stated rate x face amount) ……………………………………….. 24,000

Discount on notes receivable (difference) ………………………. 34,165

14–40 Intermediate Accounting, 8/e

Exercise 14–19

1. January 1, 2016

2. Amortization schedule

$8,000,000 ÷ 2.67301 = $2,992,881

Cash Effective Decrease in Outstanding

Dec.31 Payment Interest Balance Balance

6% x Outstanding Balance Balance Reduction

8,000,000

2016 2,992,881 .06 (8,000,000) = 480,000 2,512,881 5, 487,119

3. December 31, 2016

Cash (payment determined above) ……………………………………. 2,992,881

4. December 31, 2018

Cash (payment determined above) ……………………………………. 2,992,881