Question 9–1

Question 9–2

Question 9–3

Question 9–4

The gross profit method estimates cost of goods sold, which is then subtracted

Chapter 9 Inventories: Additional Issues

QUESTIONS FOR REVIEW OF KEY TOPICS

GAAP generally requires the use of historical cost to value assets, but a departure

from cost is necessary when the utility of an asset is no longer as great as its cost. The

utility or benefits from inventory result from the ultimate sale of the goods. This

If inventory write-downs are commonplace for a company, losses usually are

included in cost of goods sold. However, when a write-down is substantial and

9–2 Intermediate Accounting, 8/e

Answers to Questions (continued)

Question 9–5

The key to obtaining accurate estimates when using the gross profit method is the

Question 9–6

The retail inventory method first determines the amount of ending inventory at

Question 9–7

The main difference between the gross profit method and the retail inventory

Question 9–8

Initial markup—Original amount of markup from cost to selling price.

Question 9–9

When using the retail method to estimate average cost, the cost–to-retail

Answers to Questions (continued)

Question 9–10

The lower of cost and net realizable value retail variation combined with the

Question 9–11

When applying LIFO, if inventory increases during the year, none of the

Question 9–12

Freight-in is added to purchases in the cost column. Net markups are added in

Question 9–13

The dollar-value LIFO retail method eliminates the stable price assumption of

regular retail LIFO. In effect, it combines dollar–value LIFO (Chapter 8) with LIFO

Question 9–14

Changes in inventory methods, other than a change to the LIFO method, are

9–4 Intermediate Accounting, 8/e

Answers to Questions (continued)

Question 9–15

When a company changes to the LIFO inventory method from any other method,

Question 9–16

If a material inventory error is discovered in an accounting period subsequent to

the period in which the error is made, any previous years’ financial statements that

Answers to Questions (concluded)

Question 9–17

2014: Cost of goods sold overstated

Question 9–18

When applying the lower of cost and net realizable value rule for valuing inventory

according to IFRS, if circumstances reveal that an inventory write-down is no longer

Question 9–19

Purchase commitments are contracts that obligate the company to purchase a

Question 9–20

Purchases made pursuant to a purchase commitment are recorded at the lower of

contract price or market price on the date the contract is executed. A loss is

9–6 Intermediate Accounting, 8/e

Brief Exercise 9–1

Brief Exercise 9–2

(1)

(2)

Product

Cost

NRV (*)

Per Unit

Inventory

Value

[Lower of

(1) and (2)]

$50

$64

34

32

* Selling price less costs to sell.

Lower of

Cost and

Cost NRV

Product 1 (1,000 units) $50,000 $50,000

BRIEF EXERCISES

Brief Exercise 9–3

Beginning inventory (from records) $220,000

Plus: Net purchases (from records) 400,000

9–8 Intermediate Accounting, 8/e

Brief Exercise 9–4

Beginning inventory (from records) $150,000

Less: Cost of goods sold:

Net sales $700,000

Brief Exercise 9–5

Cost

Retail

Beginning inventory

$ 300,000

$ 450,000

Plus: Net purchases

861,000

1,210,000

Freight-in

22,000

Net markups

Less: Net markdowns

Goods available for sale

1,183,000

Less: Net sales

(1,200,000)

Estimated ending inventory at retail

$ 490,000

Estimated ending inventory at cost (70% x $490,000)

Estimated cost of goods sold

$ 840,000

9–10 Intermediate Accounting, 8/e

Brief Exercise 9–6

Cost

Retail

Beginning inventory

$ 300,000

$ 450,000

Plus: Net purchases

861,000

1,210,000

Freight-in

22,000

Net markups

Less: Net markdowns

Goods available for sale (excluding beg. Inventory)

Goods available for sale (including beg. Inventory)

1,183,000

Less: Net sales

(1,200,000)

Estimated ending inventory at retail

$ 490,000

Estimated ending inventory at cost:

Retail Cost

Beginning inventory $ 450,000 $ 300,000

Estimated cost of goods sold

$ 854,516

Brief Exercise 9–7

Cost

Retail

Beginning inventory

$ 300,000

$ 450,000

Plus: Net purchases

861,000

1,210,000

Freight-in

22,000

Net markups

48,000

Goods available for sale

1,708,000

Less: Net markdowns

Goods available for sale

1,183,000

1,690,000

Less: Net sales

Estimated cost of goods sold

$ 843,626

9–12 Intermediate Accounting, 8/e

Brief Exercise 9–8

Cost

Retail

Beginning inventory

$220,000

Freight-in

Plus: Net markups

1,596,000

$877,800

Cost-to-retail percentage: = 55%

$1,596,000

Less: Net markdowns

_______

(6,000)

Goods available for sale

877,800

1,590,000

Less:

Estimated ending inventory at retail

Estimated cost of goods sold

Brief Exercise 9–9

Cost

Retail

Beginning inventory

$ 40,800

$ 68,000

Plus: Net purchases

155,440

270,000

Net markups

Less: Net markdowns

_______

Goods available for sale (excluding beginning inventory)

155,440

268,000

Goods available for sale (including beginning inventory)

Less: Net sales

(250,000)

Estimated ending inventory at current year retail prices

$ 86,000

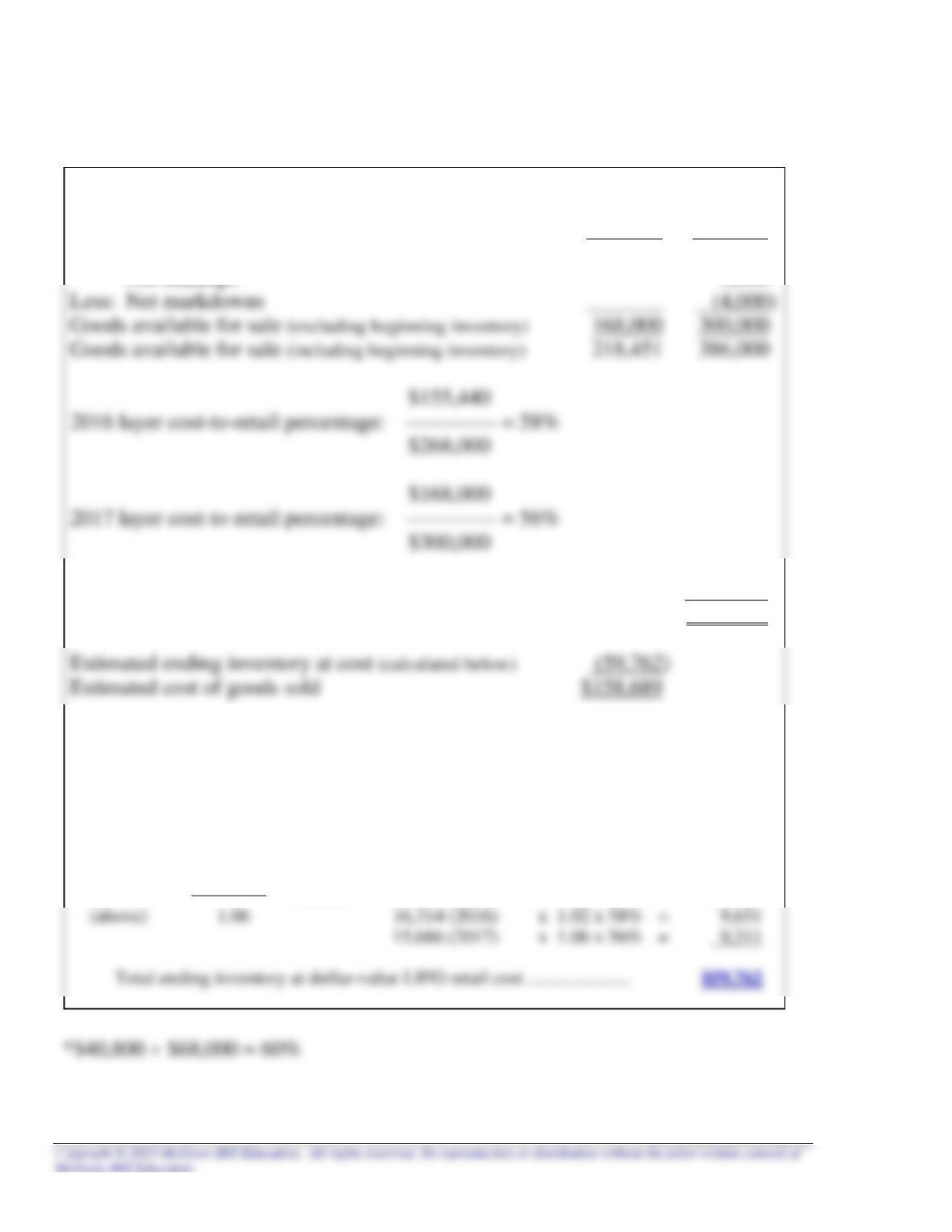

Estimated ending inventory at cost (calculated below)

(50,451)

Estimated cost of goods sold

$145,789

___________________________________________________________________________

Step 1 Step 2 Step 3

Ending Ending Inventory Inventory

Inventory Inventory Layers Layers

at Year-End at Base Year at Base Year Converted to

Retail Prices Retail Prices Retail Prices Cost

9–14 Intermediate Accounting, 8/e

Brief Exercise 9–10

Cost

Retail

Beginning inventory

$ 50,451

$ 86,000

Plus: Net purchases

168,000

301,000

Net markups

3,000

Less: Net markdowns

_______

Goods available for sale (excluding beginning inventory)

168,000

300,000

Goods available for sale (including beginning inventory)

218,451

386,000

Less: Net sales

(280,000)

Estimated ending inventory at current year retail prices

$106,000

Estimated ending inventory at cost (calculated below)

Estimated cost of goods sold

$158,689

___________________________________________________________________________

Step 1 Step 2 Step 3

Ending Ending Inventory Inventory

Inventory Inventory Layers Layers

at Year-End at Base Year at Base Year Converted to

Retail Prices Retail Prices Retail Prices Cost

$106,000

$106,000 = $100,000 $68,000 (base) x 1.00 x 60%* = $40,800

Brief Exercise 9–11

Hopyard applies the FIFO cost method retrospectively; that is, to all prior periods

as if it always had used that method. In other words, all financial statement amounts

for individual periods that are included for comparison with the current financial

statements are revised for period-specific effects of the change.

Then, the cumulative effects of the new method on periods prior to those

presented are reflected in the reported balances of the assets and liabilities affected as

Brief Exercise 9–12

When a company changes to the LIFO inventory method from any other method,

it usually is impossible to calculate the income effect on prior years. To do so would

require assumptions as to when specific LIFO inventory layers were created in years

prior to the change. As a result, a company changing to LIFO usually does not report

9–16 Intermediate Accounting, 8/e

Brief Exercise 9–13

The 2014 error caused 2014 net income to be overstated, but since 2014 ending

Analysis of 2014 ending inventory error effects:

U = Understated

O = Overstated

2014 2015

Beginning inventory → Beginning inventory O

Plus: net purchases Plus: net purchases

Brief Exercise 9–13 (concluded)

However, the 2015 error has not yet self-corrected. Both retained earnings and

inventory still are overstated as a result of the second error.

Analysis of 2015 ending inventory error effects:

U = Understated

O = Overstated

2015

Beginning inventory

Plus: net purchases

Brief Exercise 9–14

The financial statements that were incorrect as a result of both errors (effect of

one error in 2014 and effect of two errors in 2015) would be retrospectively restated

9–18 Intermediate Accounting, 8/e

Exercise 9–1

(1)

(2)

Product

Cost

NRV (*)

Per Unit

Inventory Value

[Lower of (1)

and (2)]

1

$ 20

$34

$20

2

90

80

80

3

50

60

50

EXERCISES

Exercise 9–2

Requirement 1

(1)

(2)

Product

Cost

NRV

Inventory

Value

[Lower of

(1) and (2)]

101

$120,000

$100,000

$100,000

90,000

50,000

$300,000

9–20 Intermediate Accounting, 8/e

Exercise 9–3

(1)

(2)

Product

Cost

NRV (*)

Per Unit

Inventory

Value

[Lower of (1)

and (2)]

A

$40

$52**

$40

B

90

86

86

C

40

70

40

D

100

112

100

E

20

26

20