Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

111. On March 15, 2016, Ellis Corporation issued 5,000 shares of its no-par common stock in

exchange for a patent. On the date of the transaction, the market price of the common stock

was $22 per share. Ellis also received a tract of land from the City of Montrose as an

enticement to build a new office building on the site. The land had a fair value of $510,000

and Ellis was required to pay only $200,000 to secure title to the land.

Required:

1. Prepare the journal entries to record the transactions under U.S. GAAP.

2. Prepare the entry to record the government grant assuming Ellis prepares its financial

statements according to International Financial Reporting Standards. Prepare the entry

according to each of the alternatives available under IFRS.

Answer:

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

112. Kerry, Inc., exchanged land and cash of $8,000 for equipment. The land had a book value of

$55,000 and a fair value of $60,000.

Required:

Prepare the journal entry to record the exchange. Assume the exchange has commercial

substance.

113. Peanut Corporation exchanged land and cash of $6,500 for equipment. The land had a book

value of $45,000 and a fair value of $34,000. Assume the exchange has commercial

substance.

Required:

Prepare the journal entry to record the exchange.

114. Ford Inc. exchanged land and $7,500 cash for material handling equipment. The land had a

book value of $75,000 and a fair value of $105,000. Assume the exchange has commercial

substance.

Required:

Prepare the journal entry to record the exchange.

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

115. Walker Corporation exchanged land and $4,500 cash for material handling equipment. The

land had a book value of $45,000 and a fair value of $58,000. Assume the exchange has

commercial substance.

Required:

Prepare the journal entry to record the exchange.

116. Cheney Company sold a 20-ton mechanical draw press for $60,000. The old draw press cost

$77,000 and had a book value of $55,000.

Required:

Prepare the journal entry to record the disposition.

117. McLean Mfg. Company sold a three-speed lathe for $24,000 cash. The lathe cost $66,200 and

had a book value of $23,200.

Required:

Prepare the journal entry to record the sale.

118. Champion Industries exchanged a dust-scrubbing piece of equipment for another version of

the same type of equipment and received $12,000 cash. The old dust scrubber cost $76,200

and had a book value of $54,500. The new dust scrubber had a fair value of $58,500.

Required:

Prepare the journal entry to record the exchange. Assume the exchange has commercial

substance.

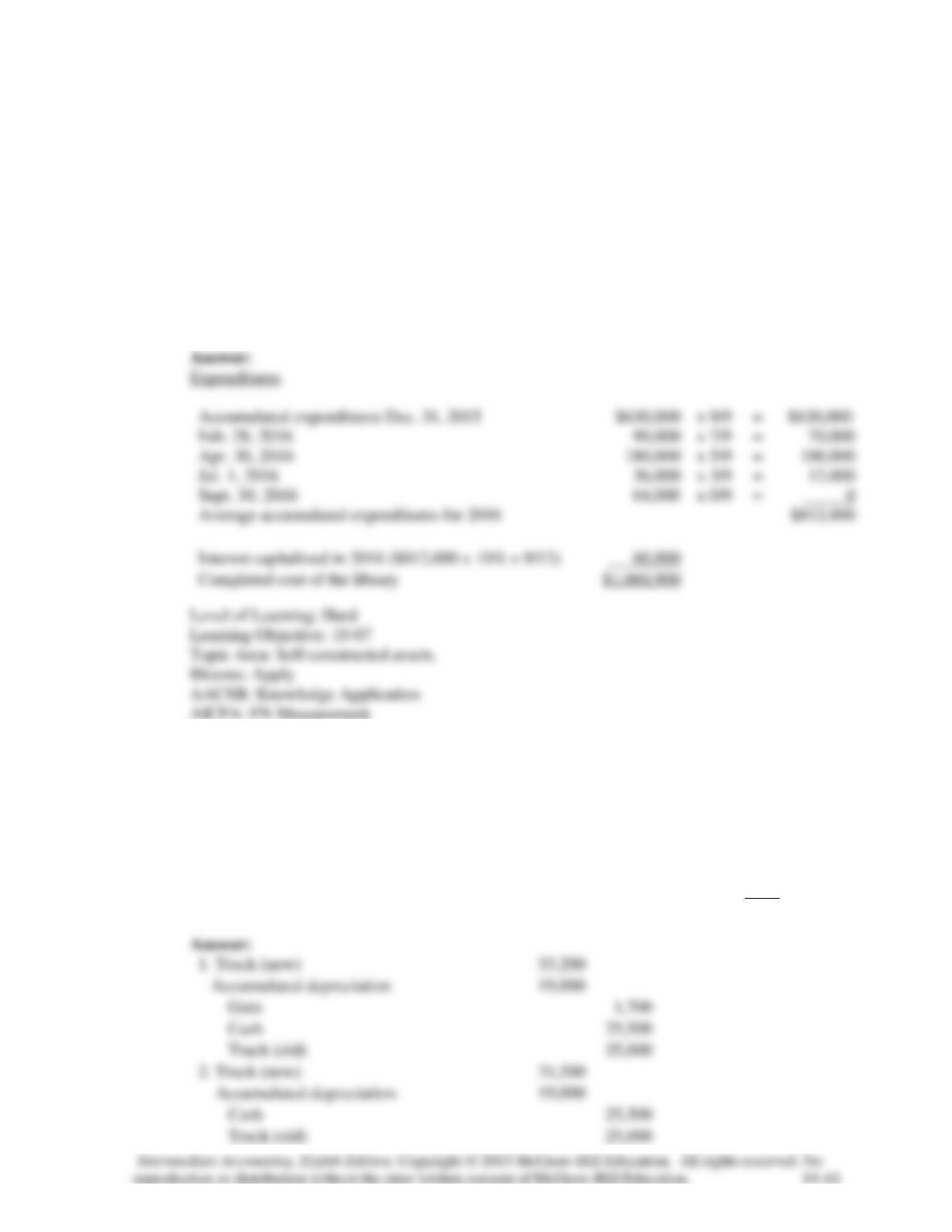

119. Montgomery Industries spent $600,000 in 2015 on a construction project to build a library.

Montgomery also capitalized $30,000 of interest on the project in 2015. Montgomery financed

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

100% of the construction with a 10% construction loan. The project was completed on

September 30, 2016. Additional expenditures in 2016 were as follows:

Feb. 28

$ 90,000

Apr. 30

180,000

Jul. 1

36,000

Sept. 30

64,000

Required:

Determine the completed cost of the library. Show supporting computations.

Accumulated expenditures Dec. 31, 2015

x 9/9

Feb. 28, 2016

x 7/9

Apr. 30, 2016

x 5/9

Jul. 1, 2016

x 3/9

Sept. 30, 2016

x 0/9

120. Wendell Corporation exchanged an old truck and $25,500 cash for a new truck. The old truck

had a book value of $6,000 (original cost of $25,000 less $19,000 in accumulated

depreciation) and a fair value of $7,700.

Required:

1. Prepare the journal entry to record the exchange. Assume the exchange has commercial

substance.

2. Prepare the journal entry to record the exchange assuming that the exchange lacks

commercial substance.

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

121. Agasse Industries began construction of a new facility and took out a $1,500,000, 8%

construction loan on April 1, 2016. Agasse made payments to the general contractor of

$400,000 on April 1, $900,000 on August 31, and $500,000 on December 31.

Required:

Compute the amount of interest that Agasse would capitalize in 2016.

122. Hawkins Corporation began construction of a motel on March 31, 2016. The project was

completed on April 31, 2017. No new loans were required to fund construction. Hawkins

does have the following two interest-bearing liabilities that were outstanding throughout the

construction period:

$ 4,000,000, 6% note

$16,000,000, 10% bonds

Construction expenditures incurred were as follows:

March 31, 2016 $4,000,000

June 30, 2016 6,000,000

November 30, 2016 1,800,000

February 28, 2017 3,000,000

The company’s fiscal year-end is December 31.

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

Required:

Calculate the amount of interest capitalized for 2016 and 2017.

Answer:

123. On August 1, 2016, Reliable Software began developing a software program to allow

individuals to customize their investment portfolios. Technological feasibility was established

on January 31, 2017, and the program was available for release on March 31, 2017.

Development costs were incurred as follows:

August 1 through December 31, 2016 $6,300,000

January 1 through January 31, 2017 1,200,000

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

February 1 through March 31, 2017 1,600,000

Reliable expects a useful life of five years for the software and total revenues of $8,000,000

during that time. During 2017, revenue of $2,000,000 was recognized.

Required:

1. Prepare the journal entries to record the development costs in 2016 and 2017.

2. Calculate the required amortization for 2017.

Answer:

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

124. AstroTech Semiconductor incurred the following costs in 2016 related to a new product

design:

Research for new semiconductor design $3,220,000

Development of the new product 856,000

Legal and filing fees for a patent for the new design 110,000

Total $4,186,000

The development costs were incurred after technological and commercial feasibility was

established and after the future economic benefits were deemed probable. The project was

successfully completed, and the new product was patented before the end of the 2016 fiscal

year.

Required:

1. Calculate the amount of research and development expense AstroTech should report in its

2016 U.S. GAAP income statement related to this project.

2. Repeat Requirement 1 assuming that AstroTech prepares its financial statements

according to International Financial Reporting Standards (IFRS).

Answer:

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

Essay

Instructions:

The following answers point out the key phrases that should appear in students’ answers. They are not

intended to be examples of complete student responses. It might be helpful to provide detailed

instructions to students on how brief or in-depth you want their answers to be.

125. Kellogg Company and its subsidiaries are engaged in the manufacture and marketing of ready-

to-eat cereal and convenience foods. In its annual report to shareholders, Kellogg disclosed

the following:

DISPOSITIONS

Last year, the Company sold certain assets and liabilities of the Lender’s Bagels business to

Aurora Foods Inc. for $275 million in cash. As a result of this transaction, the Company

recorded a pretax charge of $178.9 million ($119.3 million after tax or $.29 per share). This

charge included approximately $57 million for disposal of other assets associated with the

Lender’s business, which were not purchased by Aurora. Disposal of these other assets was

completed during the current year. The original reserve of $57 million exceeded actual losses

from asset sales and related disposal costs by approximately $9 million. This amount was

recorded as a credit to other income (expense), net during the current year.

Required:

Explain how the Kellogg transactions described could be interpreted as an example of

earnings management.

126. Explain the appropriate accounting method used to account for lump-sum purchases of a

group of long-term assets.

127. Casper Chemical recently acquired a building located on two acres of land for a lump-sum

price of $3.2 million. In your job as assistant controller, you determined the allocation of the

price using the relative fair values to be $1 million and $2.2 million for the land and building,

respectively. When you reported these initial values to Jake Reese, the company’s controller,

he told you to change the allocation to $1.5 million for the land and $1.7 million for the

building. When you asked him why the change, he explained that the company is having a

difficult time meeting profitability goals and that his proposed allocation will help the bottom

line for future years.

Required:

1. How will the controller’s proposed allocation help the bottom line in future years?

2. Discuss the ethical dilemma faced by the assistant controller.

Answer:

128. How are donated assets recorded?

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

129. How are assets valued when they are acquired by issuing stock?

130. What disclosures are required relative to interest costs incurred during the year?

131. When is interest capitalized? Briefly describe how the amount to be capitalized is computed.

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

132. Why are software development costs treated differently than other types of R&D?

133. Briefly explain how R&D is reported in financial statements.

134. It’s not unusual for one company to buy another company in order to obtain technology that

the acquired company has developed or is in the process of developing.

Required:

Explain the accounting treatment of purchased technology.

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

135. Briefly explain the differences between U.S. GAAP and International Financial Reporting

Standards in accounting for research and development expenditures other than software

development costs.

136. Why would an oil company argue to use the full-cost method of accounting for oil and gas

exploration costs?

Chapter 10 Property, Plant, and Equipment and Intangible Assets:

Acquisition and Disposition

137. Briefly explain the differences between U.S. GAAP and International Financial Reporting

Standards (IFRS) in accounting for government grants for the purchase of assets.