Alternate Exercises and Problems 5–1

Chapter 5 Revenue Recognition and Profitability Analysis

EXERCISES

Exercise 5–1

Happy first must identify each performance obligation’s share of the sum of the

stand-alone selling prices of all performance obligations:

Patio:

$3,400

= 85%

$3,400 + 200 + 400

Happy would allocate the total selling price of the package ($1,900) based on

stand-alone selling prices, as follows:

Patio:

$3,800

×

85%

=

$3,230

5–2 Intermediate Accounting, 8/e

Exercise 5-2

Requirement 1

Requirement 2

The most likely amount is $30,000, because the probability of exceeding the

Requirement 3

Because Mohan is very uncertain of its estimate, Mohan can’t argue that it is

Alternate Exercises and Problems 5–3

Exercise 5-3

Requirement 1

2016 2017

Contract price $2,600,000 $2,600,000

Actual costs to date 360,000 2,010,000

Revenue recognition:

2016: $ 360,000

= 18.75% x $2,600,000 = $487,500

Gross profit recognition:

2016: $487,500 – 360,000 = $127,500

Requirement 2

5–4 Intermediate Accounting, 8/e

Exercise 5-3 (concluded)

Requirement 3

Balance Sheet

At December 31, 2016

Current assets:

Accounts receivable

$ 110,000

Requirement 4

Balance Sheet

At December 31, 2016

Current assets:

Accounts receivable

$ 110,000

Current liabilities:

Alternate Exercises and Problems 5–5

Exercise 5-4

Requirement 1

2016 2017 2018

Contract price $12,000,000 $12,000,000 $12,000,000

Actual costs to date 3,000,000 7,000,000 12,800,000

Revenue recognition:

2016: $3,000,000

Gross profit (loss) recognition:

2016: $4,000,000 – 3,000,000 = $1,000,000

5–6 Intermediate Accounting, 8/e

Exercise 5-4 (continued)

Requirement 2

2016

2017

Construction in progress

3,000,000

4,000,000

Various accounts

3,000,000

4,000,000

To record construction costs.

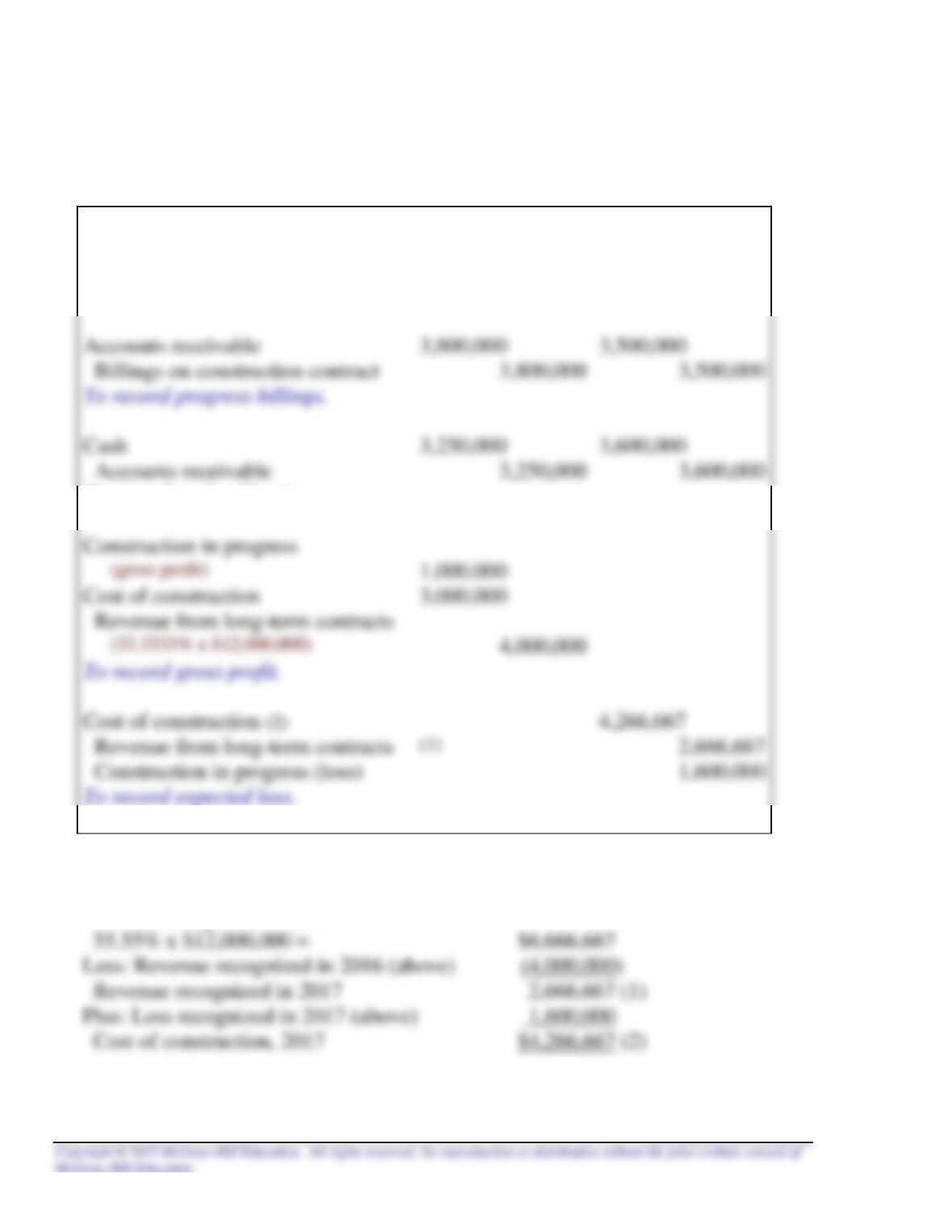

Accounts receivable

3,800,000

3,500,000

Billings on construction contract

3,800,000

3,500,000

To record progress billings.

Cash

3,250,000

3,600,000

To record cash collections.

Cost of construction

3,000,000

To record gross profit.

Cost of construction (2)

4,266,667

Revenue from long-term contracts

2,666,667

Construction in progress (loss)

1,600,000

(1) and (2):

Percent complete = $7,000,000 ÷ $12,600,000 = 55.55%

Revenue recognized to date:

Alternate Exercises and Problems 5–7

Exercise 5-4 (concluded)

Requirement 3

Balance Sheet

2016

2017

Current assets:

Accounts receivable

$550,000

$450,000

Current liabilities:

5–8 Intermediate Accounting, 8/e

Exercise 5-5

Turnover ratios for Garret & Sons Music Company for 2016:

[$800,000 + 600,000] ÷ 2

The company turns its inventory over 7 times per year compared to the industry

average of 6 times per year. The asset turnover ratio also is slightly better than the

Inventory turnover ratio = $6,000,000

[$850,000 + 700,000] ÷ 2

Alternate Exercises and Problems 5–9

Exercise 5-6

Requirement 1

a. Profit margin on sales $360 ÷ $7,200 = 5%

b. Return on assets $360 ÷ [($2,900 + 2,700) ÷ 2] = 12.86%

5–10 Intermediate Accounting, 8/e

Exercise 5-7

Requirement 1

Year Income recognized

2013 $250,000 ($400,000 – 150,000)

2014 – 0 –

Requirement 2

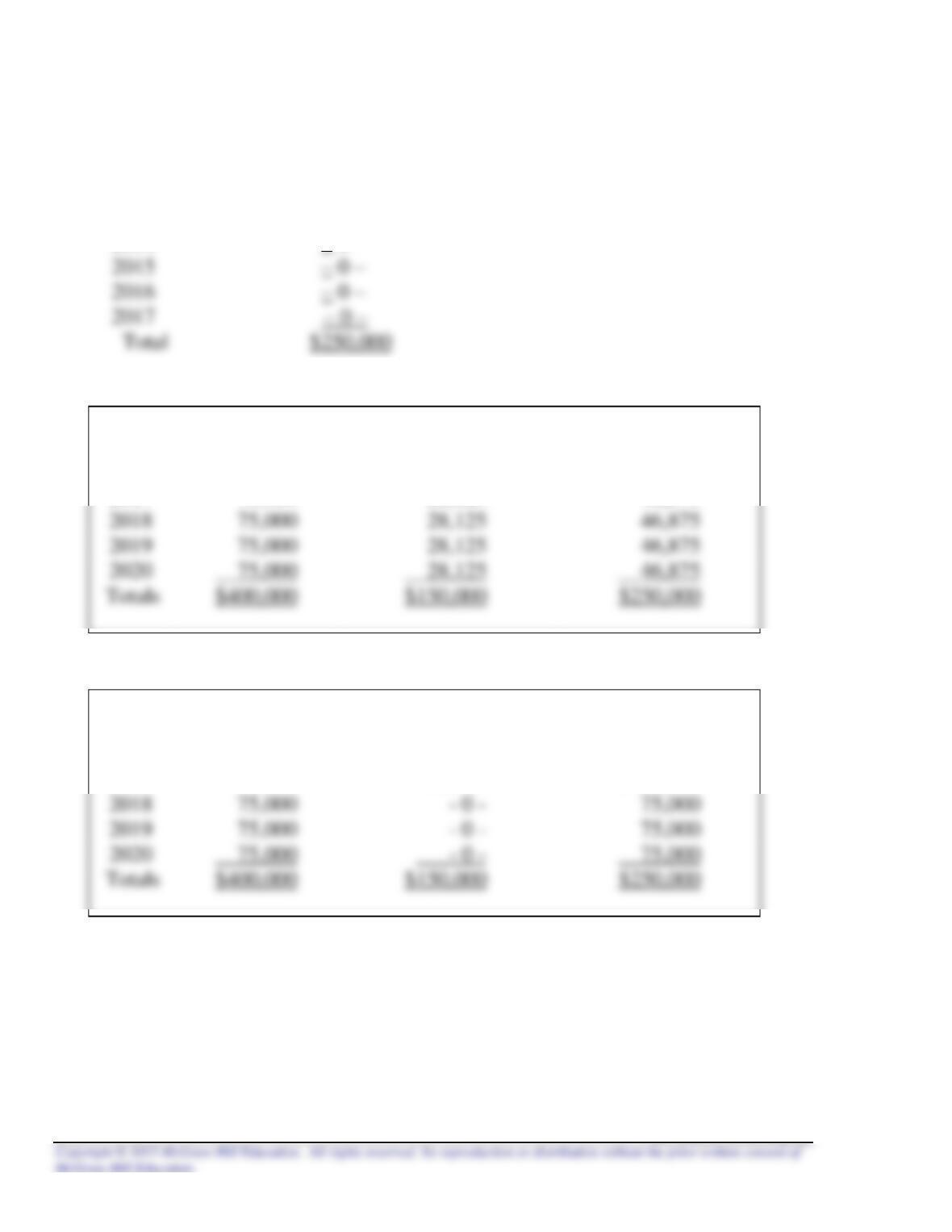

Year

Cash Collected

Cost Recovery(37.5%)

Gross Profit(62.5%)

2016

$100,000

$ 37,500

$ 62,500

2017

75,000

28,125

46,875

2018

75,000

2019

2020

$400,000

$150,000

$250,000

Requirement 3

Year

Cash Collected

Cost Recovery

Gross Profit

2016

$100,000

$100,000

– 0 –

2017

75,000

50,000

$ 25,000

2018

2019

2020

$400,000

$150,000

$250,000

Alternate Exercises and Problems 5–11

Exercise 5-8

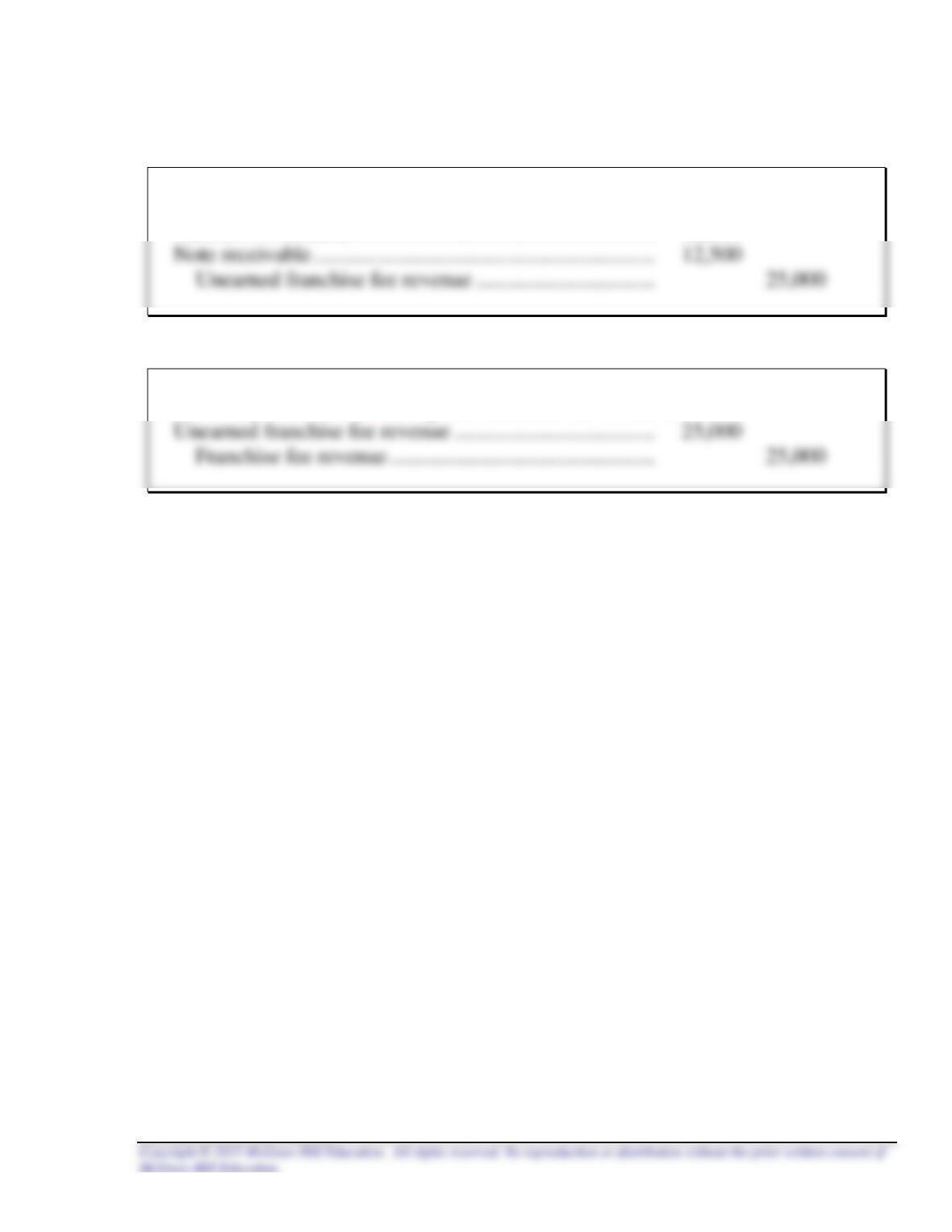

November 15, 2016 To record franchise agreement and down payment

Cash (50% x $25,000) ……………………………………………….. 12,500

February 15, 2017 To recognize franchise fee revenue