Question 7–1

Question 7–2

Internal control procedures involving accounting functions are intended to

Question 7–3

Management must document the company’s internal controls and assess their

Question 7–4

A compensating balance is an amount of cash a depositor (debtor) must leave on

deposit in an account at a bank (creditor) as security for a loan or a commitment to

lend. The classification and disclosure of a compensating balance depends on the

Chapter 7 Cash and Receivables

Questions for Review of Key Topics

7–2 Intermediate Accounting, 8/e

Answers to Questions (continued)

Question 7–5

Yes, IFRS and U.S. GAAP differ in how bank overdrafts are treated. Under

Question 7–6

Trade discounts are reductions below a list price and are used to establish a final

Question 7–7

The gross method of accounting for cash discounts considers discounts not taken

Question 7–8

Companies estimate sales returns and reduce revenue to account for them. If the

company has received cash from the customer, the company credits a refund liability

Question 7–9

Even when specific customer accounts haven’t been proven uncollectible by the

end of the reporting period, bad debt expense should properly be matched with sales

Answers to Questions (continued)

Question 7–10

The income statement approach to estimating bad debts determines bad debt

Question 7–11

Question 7–12

Question 7–13

The accounting treatment of receivables factored with recourse depends on

7–4 Intermediate Accounting, 8/e

Question 7–14

U.S. GAAP focuses on whether control of assets has shifted from the transferor

to the transferee. In contrast, IFRS focuses on whether the company has transferred

“substantially all of the risks and rewards of ownership,” as well as whether the

company has transferred control. Under IFRS:

1. If the company transfers substantially all of the risks and rewards of

ownership, the transfer is treated as a sale.

3. If neither conditions 1 or 2 hold, the company accounts for the transaction

Question 7–15

When a note is discounted, a financial institution, usually a bank, accepts the note

and gives the seller cash equal to the maturity value of the note reduced by a discount.

The discount is computed by applying a discount rate to the maturity value and

represents the financing fee the bank charges for the transaction.

The four-step process used to account for a discounted note receivable is as

follows:

1. Accrue any interest revenue earned since the last payment date (or date of the

note).

3. Subtract the discount the bank requires (discount rate times maturity value

4. Compute the difference between the proceeds and the book value of the note

and related interest receivable. The treatment of the difference will depend on

Answers to Questions (concluded)

Question 7–16

A company’s investment in receivables is influenced by several related variables,

Question 7–17

The items necessary to adjust the bank balance might include deposits

Question 7–18

A petty cash fund is established by transferring a specified amount of cash from

Question 7–19

When a creditor’s investment in a receivable becomes impaired, due to a troubled

debt restructuring or for any other reason, the receivable is remeasured based on the

Question 7–20

No. Under both U.S. GAAP and IFRS, a company can recognize in net income

the recovery of impairment losses of accounts and notes receivable.

7–6 Intermediate Accounting, 8/e

Brief Exercise 7–1

The company could improve its internal control procedure for cash receipts by

Brief Exercise 7–2

Under IFRS the cash balance would be $245,000, because they could offset the

Brief Exercise 7–3

All of these items would be included as cash and cash equivalents except the U.S.

Brief Exercise 7–4

Income before tax in 2017 will be reduced by $2,500, the amount of the cash

discounts.

Brief Exercise 7–5

Income before tax in 2016 will be reduced by $2,500, the anticipated amount of

cash discounts.

BRIEF EXERCISES

Brief Exercise 7–6

Estimated returns = $10,600,000 x 8% = $848,000

Brief Exercise 7–7

Estimated returns = $10,600,000 x 8% = $848,000

Brief Exercise 7–8

Singletary cannot combine the two types of receivables under U.S. GAAP, as the

director is a related party. Under IFRS a combined presentation would be allowed.

7–8 Intermediate Accounting, 8/e

Brief Exercise 7–9

(2) Allowance for uncollectible accounts:

Beginning balance $25,000

Brief Exercise 7–10

(1) Allowance for uncollectible accounts:

Beginning balance $ 25,000

Accounts receivable:

Beginning balance $ 300,000

Brief Exercise 7–11

Allowance for uncollectible accounts:

Beginning balance $30,000

Brief Exercise 7–12

Credit sales $8,200,000

Deduct: Cash collections (7,950,000)

Brief Exercise 7–13

2016 interest revenue:

Brief Exercise 7–14

Sales revenue = present value of the note receivable

7–10 Intermediate Accounting, 8/e

Brief Exercise 7–15

Assets decrease by $7,000:

Cash increases by $100,000 x 85% = $ 85,000

The journal entry to record the transaction is as follows:

Cash (85% x $100,000) ………………………………………………. 85,000

Brief Exercise 7–16

Logitech would account for the transfer as a secured borrowing. The receivables

Brief Exercise 7–17

Under IFRS Huling would treat this transaction as a secured borrowing, because

it retains substantially all of the risks and rewards of ownership. Under U.S. GAAP

Brief Exercise 7–18

$30,000 Face amount

450 Interest to maturity ($30,000 x 6% x 3/12)

Brief Exercise 7–19

Receivables turnover = $320,000 = 5.33 times

$60,000*

Brief Exercise 7–20

Balance per books $22,340

Add:

Error in recording cash receipt ($550 – 500) 50

7–12 Intermediate Accounting, 8/e

Brief Exercise 7–21

Balance per bank statement $47,582

Add:

Exercise 7–1

Requirement 1

Cash and cash equivalents includes:

a. Balance in checking account $13,500

Requirement 2

d. The $400,000 savings account will be used for future plant expansion and

EXERCISES

7–14 Intermediate Accounting, 8/e

Exercise 7–2

Requirement 1

Cash and cash equivalents includes:

Cash in bank—checking account $22,500

Requirement 2

The $10,000 in 6-month treasury bills should be classified as a current asset

Exercise 7–3

The FASB Accounting Standards Codification represents the single source of

authoritative U.S. generally accepted accounting principles. The specific citation for

each of the following items is:

1. Accounts receivables from related parties should be shown separately from

trade receivables: FASB ACS 210–10–S99–1: “Balance Sheet—Overall—SEC

2. Definition of Cash Equivalents: FASB ACS 305–10–20: “Cash and Cash

Equivalents—Overall—Glossary.”

3. Notes exchanged for cash are valued at the cash proceeds: FASB ACS 310–

4. The two conditions that must be met to accrue a loss on an account

Exercise 7–4

Requirement 1: U.S. GAAP

Current Assets:

Requirement 2: IFRS

Current Assets:

Exercise 7–5

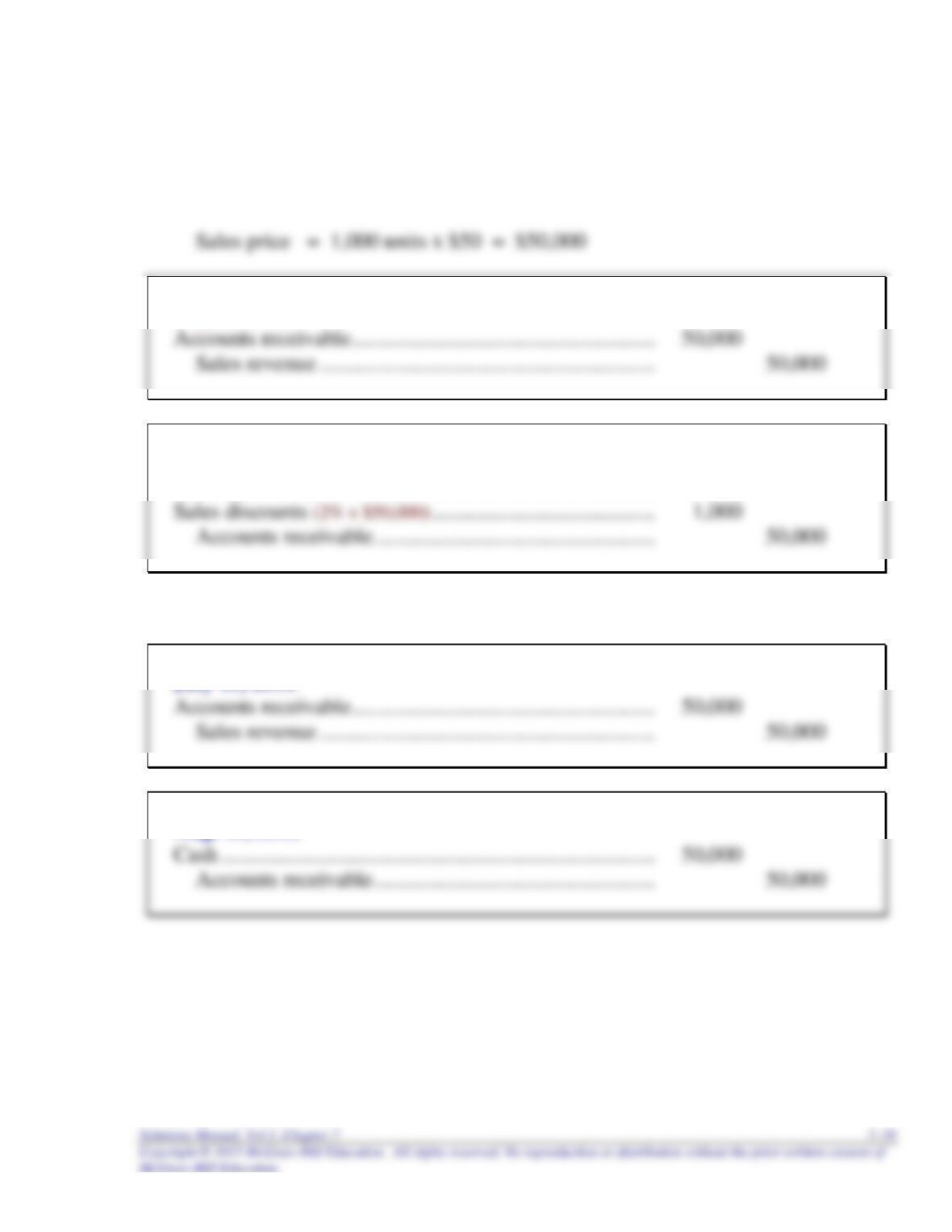

Requirement 1

November 17, 2016

Accounts receivable ……………………………………………….. 42,000

Requirement 2

November 17, 2016

Accounts receivable ……………………………………………….. 42,000

7–18 Intermediate Accounting, 8/e

Exercise 7–5 (concluded)

Requirement 3

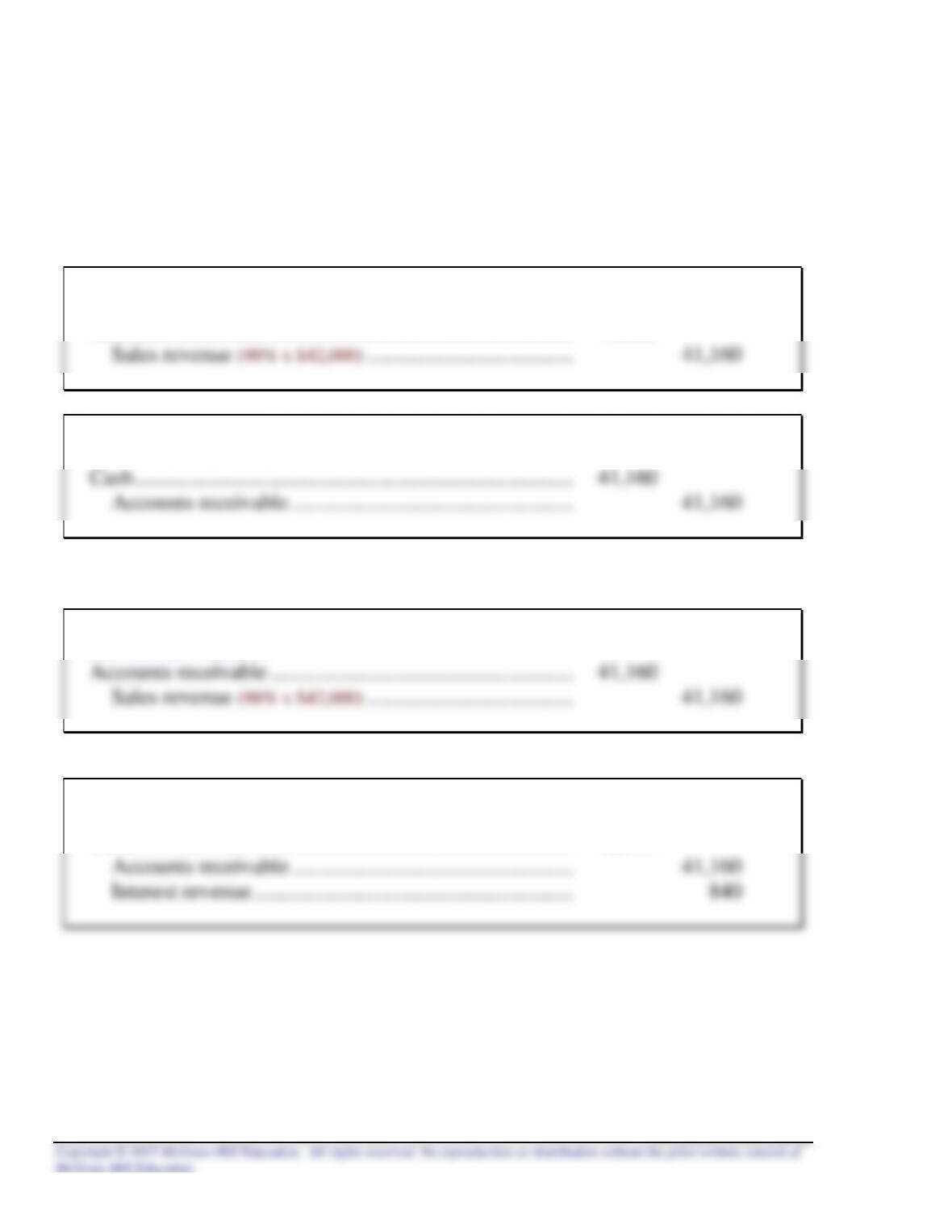

Requirement 1, using the net method:

November 17, 2016

Accounts receivable ……………………………………………….. 41,160

November 26, 2016

Requirement 2, using the net method:

November 17, 2016

December 15, 2016

Cash ……………………………………………………………………… 42,000

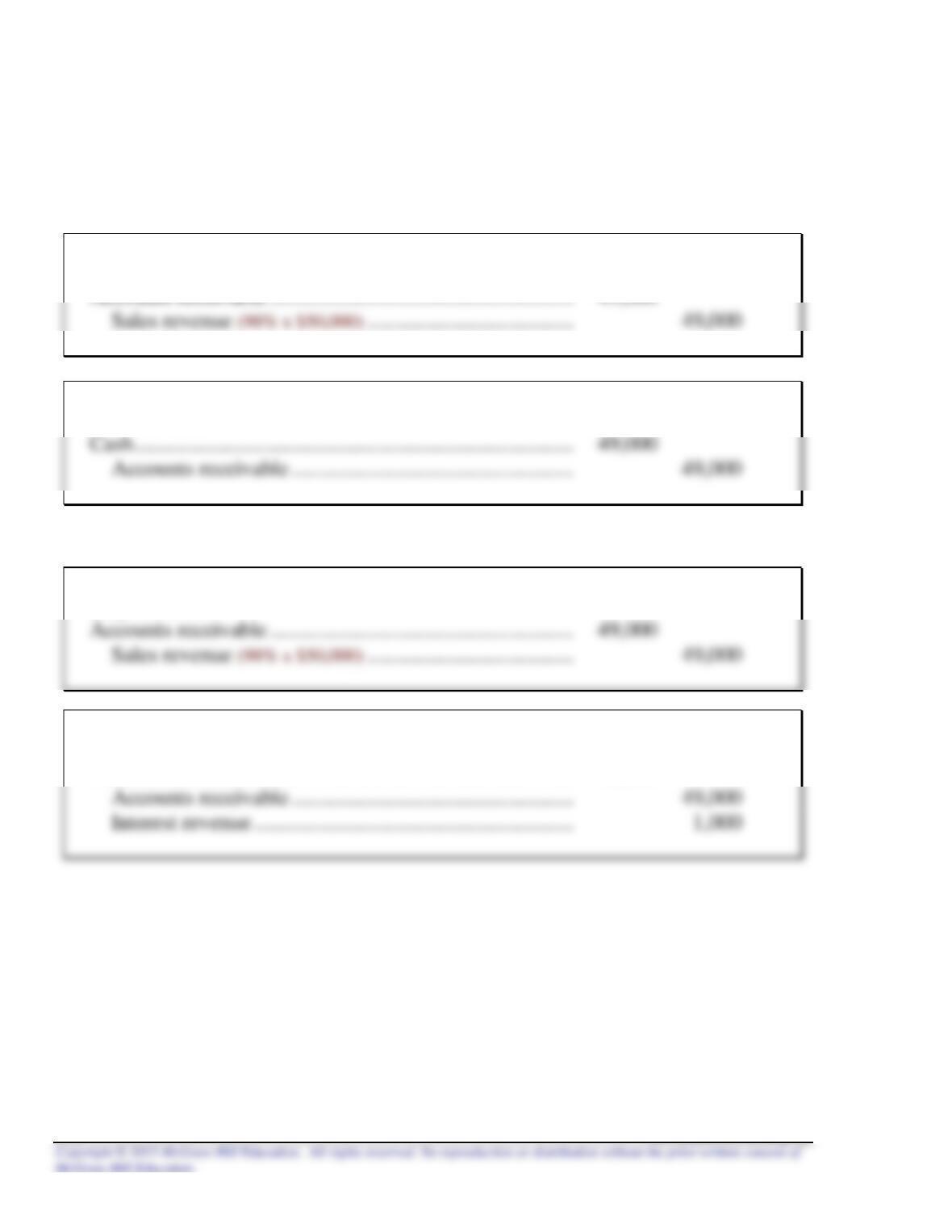

Exercise 7–6

Requirement 1

July 15, 2016

July 23, 2016

Cash (98% x $50,000) ……………………………………………….. 49,000

Requirement 2

July 15, 2016

Aug. 15, 2016

7–20 Intermediate Accounting, 8/e

Exercise 7–7

Requirement 1

July 15, 2016

July 23, 2016

Requirement 2

July 15, 2016

August 15, 2016

Cash ……………………………………………………………………… 50,000