Exercise 9–4

1. The accounting treatment required for a correction of an inventory

error in previously issued financial statements:

FASB ASC 250–10–50–7: “Accounting Changes and Error Corrections–

Overall–Disclosure–Other Presentation Matters.”

Any error in the financial statements of a prior period discovered after the

financial statements are issued or are available to be issued (as discussed

in Section 855-10–25) shall be reported as an error correction, by

restating the prior-period financial statements. Restatement requires all of

the following:

• a. The cumulative effect of the error on periods prior to those

presented shall be reflected in the carrying amounts of assets and

liabilities as of the beginning of the first period presented.

2. The use of the retail method to value inventory:

FASB ASC 330–10–30–13: “Inventory–Overall–Initial Measurement–

Determination of Inventory Costs.”

9–22 Intermediate Accounting, 8/e

Exercise 9–5

Beginning inventory (from records) $140,000

Plus: Net purchases (from records) 370,000

Exercise 9–6

Beginning inventory (from records) $100,000

Less: Cost of goods sold:

Net sales $220,000

Exercise 9–7

Merchandise inventory, January 1, 2016 $1,900,000

Purchases 5,800,000

9–24 Intermediate Accounting, 8/e

Exercise 9–8

Requirement 1

Beginning inventory (from records) $ 58,500

Plus: Net purchases ($110,000 – 4,000) 106,000

Freight-in (from records) 3,000

Requirement 2

Beginning inventory (from records) $ 58,500

Plus: Net purchases ($110,000 – 4,000) 106,000

Freight-in (from records) 3,000

Exercise 9–9

Beginning inventory + Net purchases – Ending inventory = Cost of goods sold

$27,000 + 31,000 – 28,000 = $30,000 = Cost of goods sold

Exercise 9–10

Cost

Retail

Beginning inventory

$35,000

$50,000

Plus: Net purchases

19,120

31,600

Net markups

Less: Net markdowns

______

Goods available for sale

Less: Net sales

Estimated ending inventory at retail

Estimated ending inventory at cost (66% x $50,000)

Estimated cost of goods sold

9–26 Intermediate Accounting, 8/e

Exercise 9–11

Cost

Retail

Beginning inventory

$190,000

$ 280,000

Plus: Purchases

600,000

840,000

Freight-in

Net markups

Less: Net markdowns

Goods available for sale

Less: Net sales

Exercise 9–12

Cost

Retail

Beginning inventory

$160,000

$ 280,000

Plus: Net purchases

Net markups

Less: Net markdowns

Goods available for sale (excluding beg. inventory)

Goods available for sale (including beg. inventory)

Less: Net sales

(800,000)

Estimated ending inventory at retail

$ 336,000

Estimated ending inventory at cost:

Beginning inventory $280,000 $160,000

Estimated cost of goods sold

9–28 Intermediate Accounting, 8/e

Exercise 9–13

Cost

Retail

Beginning inventory

$ 12,000

$ 20,000

Plus: Purchases

102,600

165,000

Freight-in

Less: Purchase returns

Plus: Net markups

184,000

Less: Net markdowns

_______

Goods available for sale

114,080

181,000

Less:

Normal spoilage

Net sales

Estimated ending inventory at retail

$ 24,800

Estimated ending inventory at cost (62% x $24,800)

Estimated cost of goods sold

$ 98,704

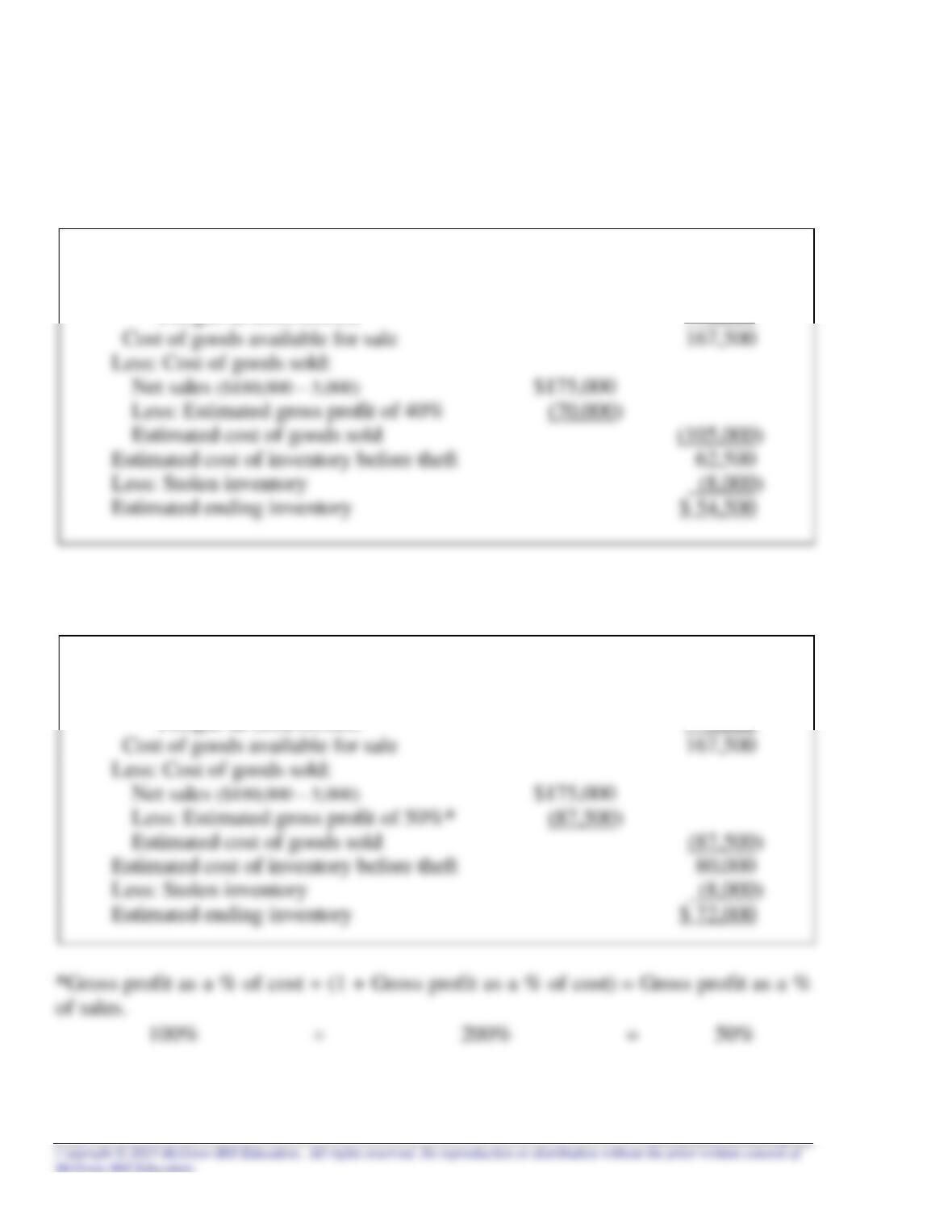

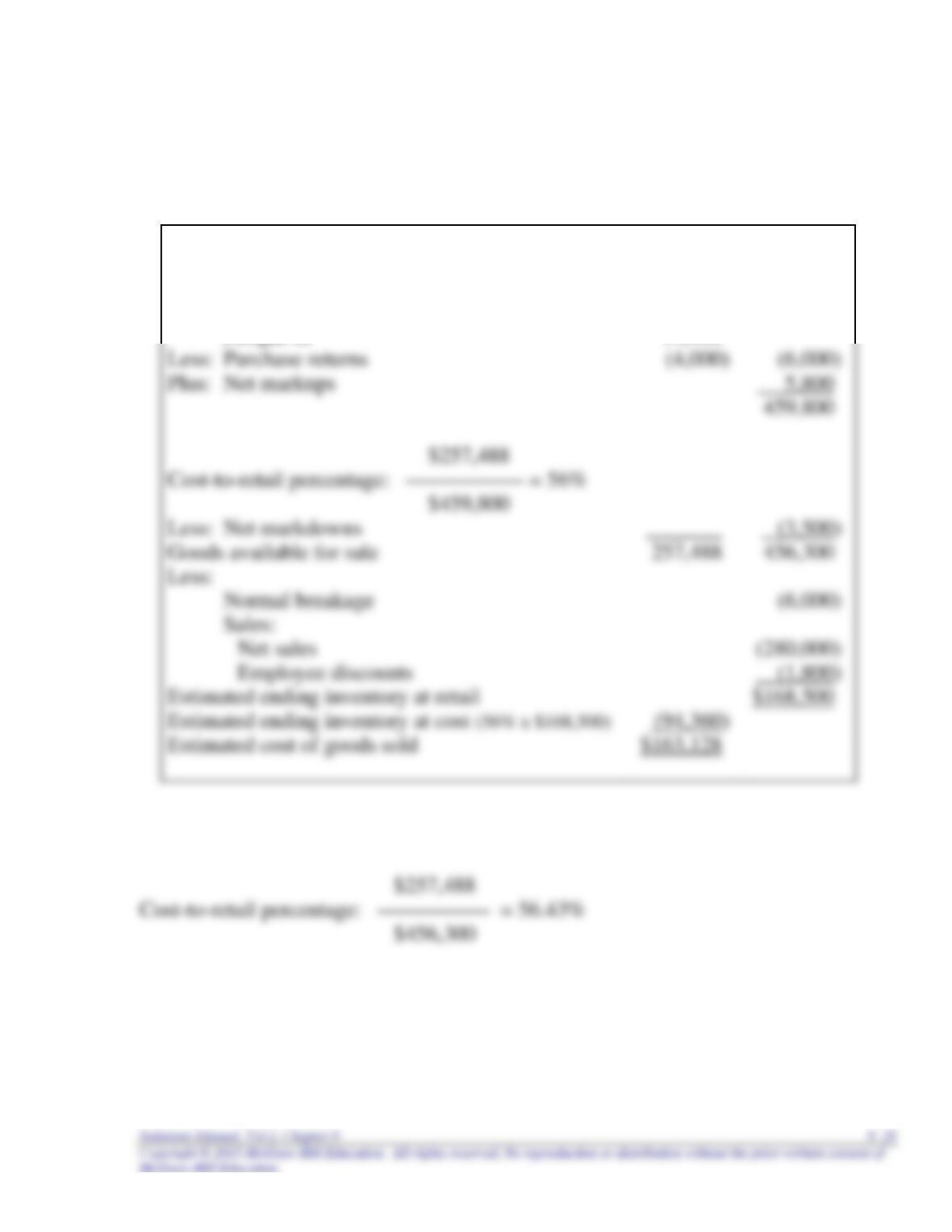

Exercise 9–14

Requirement 1

Cost

Retail

Beginning inventory

$ 40,000

$ 60,000

Plus: Purchases

207,000

400,000

Freight-in

14,488

Less: Purchase returns

459,800

Less: Net markdowns

_______

Goods available for sale

257,488

456,300

Less:

Normal breakage

Sales:

Net sales

Employee discounts

Estimated ending inventory at retail

$168,500

Estimated ending inventory at cost (56% x $168,500)

Estimated cost of goods sold

Requirement 2

Net markdowns are included in the cost-to-retail percentage:

9–30 Intermediate Accounting, 8/e

Exercise 9–15

Net purchases:

Using LIFO, the beginning inventory is excluded from the calculation of the cost–to–

retail percentage:

Cost of goods available (excluding beg. inventory)

Cost-to-retail percentage =

Net sales:

The cost-to-retail percentage can be calculated as follows:

Cost

Retail

Beginning inventory

$21,000.00

$ 35,000

Net markups

Less: Net markdowns

_________

Goods available for sale

Less: Net sales

Estimated ending inventory at retail

Estimated ending inventory at cost (56.25% x ?) =

$17,437.50

Estimated ending inventory at retail is:

$17,437.50

= $31,000

Exercise 9–16

Cost

Retail

Beginning inventory

$ 71,280

$132,000

Plus: Net purchases

112,500

255,000

Net markups

6,000

Less: Net markdowns

Goods available for sale (excluding beginning inventory)

112,500

250,000

Goods available for sale (including beginning inventory)

183,780

382,000

Less: Net sales

Estimated ending inventory at current year retail prices

$150,000

Estimated ending inventory at cost (below)

Estimated cost of goods sold

$106,776

___________________________________________________________________________

Step 1 Step 2 Step 3

Ending Ending Inventory Inventory

Inventory Inventory Layers Layers

at Year-End at Base Year at Base Year Converted to

Retail Prices Retail Prices Retail Prices Cost

$150,000

$150,000 = $144,231 $132,000 (base) x 1.00 x 54% = $71,280

9–32 Intermediate Accounting, 8/e

Exercise 9–17

Requirement 1

Requirement 2

2016

Step 1 Step 2 Step 3

Ending Ending Inventory Inventory

Inventory Inventory Layers Layers

at Year-End at Base Year at Base Year Converted to

Retail Prices Retail Prices Retail Prices Cost

$25,000

$25,000 = $20,000 $18,750 (base) x 1.00 x 80% = $15,000

Exercise 9–18

Cost

Retail

Beginning inventory

$160,000

$250,000

Plus: Net purchases

350,200

510,000

Net markups

7,000

Less: Net markdowns

Goods available for sale (excluding beginning inventory)

350,200

515,000

Goods available for sale (including beginning inventory)

510,200

765,000

Less: Net sales

Estimated ending inventory at current year retail prices

$385,000

Estimated ending inventory at cost (calculated below)

Estimated cost of goods sold

$275,400

Step 1 Step 2 Step 3

Ending Ending Inventory Inventory

Inventory Inventory Layers Layers

at Year-End at Base Year at Base Year Converted to

Retail Prices Retail Prices Retail Prices Cost

$385,000

$385,000 = $350,000 $250,000 (base) x 1.00 x 64% = $160,000

9–34 Intermediate Accounting, 8/e

Exercise 9–19

Cost-to-retail percentage, 1/1/16:

$21,000

= 75%

Exercise 9–19 (concluded)

2017 ending inventory:

Cost

Retail

Beginning inventory

$22,792

$ 33,600

Plus: Net purchases

60,000

88,400

Goods available for sale (including beginning inventory)

$82,792

122,000

Less: Net sales

Estimated ending inventory at cost (below)

$26,864

___________________________________________________________________________

Step 1 Step 2 Step 3

Ending Ending Inventory Inventory

Inventory Inventory Layers Layers

at Year-End at Base Year at Base Year Converted to

Retail Prices Retail Prices Retail Prices Cost

Exercise 9–20

Requirement 1

To record the change: ($ in millions)

Requirement 2

CPS applies the average cost method retrospectively; that is, to all prior periods

as if it always had used that method. In other words, all financial statement amounts

for individual periods that are included for comparison with the current financial

Exercise 9–21

Requirement 1

Requirement 2

Effect on cost of goods sold:

9–38 Intermediate Accounting, 8/e

Exercise 9–22

Requirement 1

The 2014 error caused 2014 net income to be understated, but since 2014 ending

Analysis of 2014 ending inventory effects:

U = Understated

O = Overstated

2014 2015

Beginning inventory → Beginning inventory U

Exercise 9–22 (concluded)

However, the 2015 error has not yet self-corrected. Both retained earnings and

inventory still are overstated as a result of the second error.

Analysis of 2015 ending inventory error effects:

U = Understated

O = Overstated

2015

Beginning inventory

Plus: net purchases

Requirement 2

Retained earnings (overstatement of 2015 income) ………….. 150,000

Requirement 3

The financial statements that were incorrect as a result of both errors (effect of

9–40 Intermediate Accounting, 8/e

Exercise 9–23

U = understated

O = overstated

NE = no effect

Cost of Net Retained

Goods Sold Income Earnings

1. Overstatement of ending inventory U O O