CHAPTER 9

INVENTORIES: ADDITIONAL ISSUES

Overview

We covered most of the principal measurement and reporting issues involving the asset inventory

and the corresponding expense cost of goods sold in the previous chapter. In this chapter we

complete our discussion of inventory measurement by explaining the lower of cost and net realizable

value rule used to value inventories. In addition, we investigate inventory estimation techniques,

methods of simplifying LIFO, changes in inventory method, and inventory errors.

Learning Objectives

LO9-1 Understand and apply the lower of cost and net realizable value rule used to value

inventories.

LO9-2 Estimate ending inventory and cost of goods sold using the gross profit method.

LO9-3 Estimate ending inventory and cost of goods sold using the retail inventory method,

applying the various cost flow methods.

LO9-4 Explain how the retail inventory method can be made to approximate the lower of cost and

net realizable value rule.

LO9-5 Determine ending inventory using the dollar-value LIFO retail inventory method.

LO9-6 Explain the appropriate accounting treatment required when a change in inventory method

is made.

LO9-7 Explain the appropriate accounting treatment required when an inventory error is

discovered.

LO9-8 Discuss the primary differences between U.S. GAAP and IFRS with respect to the lower of

cost and net realizable value rule for valuing inventory.

Lecture Outline

Part A: Reporting—Lower of Cost and Net Realizable Value

I. Determining Net Realizable Value (T9-1)

A. Inventories are reported at the lower of cost and net realizable value.

B. The lower of cost and net realizable value approach to valuing inventory recognizes losses

in the period when the value of inventory declines below cost.

C. Net realizable value (NRV) is the estimated selling price of the product in the ordinary

course of business reduced by reasonably predictable costs of completion, disposal, and

transportation.

D. Under international financial reporting standards, inventory also is valued at the lower of

cost and net realizable value. (T9-2)

II. Applying Lower of Cost and Net Realizable Value

A. The lower of cost and net realizable value rule can be applied to individual items, logical

inventory categories, or the entire inventory. (T9-3)

9-2 Intermediate Accounting,8/e

B. Applying the rule to groups of inventory items usually will cause a higher inventory

valuation than if applied item-by-item because group application permits decreases in the

net realizable value of some items to be offset by increases in others.

C. Each approach is acceptable but should be applied consistently from one period to another.

III. Adjusting Cost to Net Realizable Value

A. If inventory write-downs are commonplace for a company, losses usually are included in

cost of goods sold.

B. When a write-down is substantial and unusual, GAAP requires that the loss be expressly

disclosed.

Part B: Inventory Estimation Techniques

I. The Gross Profit Method (T9-4)

A. The gross profit method is useful in situations where estimates of inventory are desirable:

1. In determining the cost of inventory that has been lost, stolen, or destroyed.

2. In estimating inventory and cost of goods sold for interim periods.

3. In auditors’ testing of the overall reasonableness of inventory amounts reported by

clients.

4. In budgeting and forecasting.

B. The gross profit method provides only an approximation of inventory and is not acceptable

for the presentation of annual financial statements.

C. The technique estimates cost of goods sold by multiplying net sales for the period by a

historical gross profit percentage and then subtracting this amount from net sales. (T9-5)

D. An estimate of ending inventory is then obtained by subtracting estimated cost of goods

sold from cost of goods available for sale.

II. The Retail Inventory Method (T9-6)

A. The retail inventory method estimation technique is similar to the gross profit method in

that it relies on the relationship between cost and selling price to estimate ending inventory

and cost of goods sold, thus avoiding the necessity to take a physical count of inventory.

B. The retail inventory method tends to provide more accurate estimates than the gross profit

method because it’s based on the current cost-to–retail percentage (the reciprocal of the

gross profit ratio) rather than a historical gross profit ratio.

C. The technique requires a company to maintain records of inventory and purchases not only

at cost but also at current selling price (retail).

D. In its simplest form, the retail inventory method estimates the amount of ending inventory

(at retail) by subtracting sales (at retail) from goods available for sale (at retail). This

estimated ending inventory at retail is then converted to cost by multiplying it by the cost-

to-retail percentage. This ratio is found by dividing goods available for sale at cost by

goods available for sale at retail. (T9-7)

E. The retail inventory method can be used for financial reporting and for income tax

purposes.

F. Changes in selling prices must be included in the determination of ending inventory at

retail. Net markups and net markdowns are included in the retail column to determine

ending inventory at retail. (T9-8)

G. An advantage of the retail inventory method is that the various cost flow assumptions (in

particular average cost and LIFO) can be explicitly incorporated into the estimation

technique. We can even incorporate an approximation of the lower of cost and net

realizable value. (T9-9)

1. To approximate average cost, the cost-to-retail percentage is determined for all goods

available for sale. Net markups and net markdowns both are included in the retail

column before the cost-to–retail percentage is determined. (T9-10)

2. A commonly used variation of the retail method often is referred to as the

conventional retail method. This variation approximates average lower of cost and

net realizable value by excluding markdowns from the calculation of the cost-to-retail

percentage. (T9-11)

a. By not subtracting net markdowns from the denominator, the cost-to-retail

percentage is lower.

b. The logic for using this approximation is that a markdown is evidence of a

reduction in the utility of inventory.

c. The lower of cost and net realizable value variation also could be applied to the

FIFO method but is not generally used in combination with LIFO.

3. To approximate LIFO cost in its simplest form, we assume that the retail prices of

goods remained stable during the period. With this assumption, we can compare

beginning and ending inventory at retail to determine what happened to inventory

quantity. (T9-12)

a. If inventory at retail increases during the year, a new layer is added.

b. If inventory at retail decreases, LIFO layer(s) are liquidated.

c. Each period’s LIFO layer will carry its own cost-to-retail percentage. Therefore,

beginning inventory is not included in the calculation of the current year’s cost-to–

retail percentage.

H. Other issues pertaining to the retail method

1. Freight-in is added only to the cost side in determining net purchases.

2. Purchase returns are deduced from purchases on both the cost and retail side (at

different amounts).

3. If the gross method is used to record purchases, purchase discounts taken is deducted

in determining the cost of net purchases.

4. If sales are recorded net of employee discounts, the discounts are added to sales.

5. Normal shortage is deducted in the retail column after the calculation of the cost-to–

retail percentage. Abnormal shortage is deducted in both the cost and retail columns

before the calculation of the cost-to-retail percentage.

Part C: Dollar-Value LIFO Retail

A. Using the LIFO retail method in combination with dollar-value LIFO (DVL) is referred to

as the dollar-value LIFO retail method.

B. DVL retail improves on LIFO retail by first determining if there has been a real increase in

inventory quantity by eliminating any price changes before comparing beginning and

ending inventory at retail.

C. After determining year-end inventory at current retail prices, DVL retail employs a three–

step approach. (T9-13)

1. In step 1, the ending inventory at current retail prices is converted to base year retail by

dividing by the current year’s price index (relative to the base year).

2. In step 2, ending inventory at base year retail is then apportioned into layers, each at

base year retail.

3. In step 3, each layer is then converted to layer year cost using the layer year’s price

index and cost-to-retail percentage.

Part D: Change in Inventory Method and Inventory Errors

I. Change in Accounting Principle

A. Changes in inventory method, other than a change to LIFO, are accounted for

retrospectively. This means reporting all previous periods’ financial statements as if the

new inventory method had been used in all prior periods. (T9-14)

1. The first step is to revise prior years’ financial statements.

2. The second step is to create a journal entry to adjust book balances from their current

amounts to what those balances would have been using the new inventory method.

B. For changes to the LIFO method, accounting records usually are inadequate for a company

to calculate the income effect on prior years. (T9-15)

2. A disclosure note explains the nature of the change and justification for it, the effect of

the change on current year’s income and earnings per share, and why retrospective

application was impracticable.

II. Inventory Errors

A. If an inventory error is discovered in the same accounting period that it occurred, the

original erroneous entry should simply be reversed and the appropriate entry recorded.

B. If a material inventory error is discovered in an accounting period subsequent to the period

in which the error is made, any previous years’ financial statements that were incorrect as a

result of the error are retrospectively restated to reflect the correction. (T9-16)

1. Incorrect balances are corrected.

3. A disclosure note describes the nature and the impact of the error on income amounts.

Appendix 9: Purchase Commitments (T9-17)

A. Purchase commitments are contracts that obligate a company to purchase a specified

amount of merchandise or raw materials at specified prices on or before specified dates.

B. Purchases made pursuant to a purchase commitment are recorded at the lower of contract

price or market price on the date the contract is executed.

C. If the contract period is contained within a single fiscal year:

1. If market price is equal to or greater than the contract price, the purchase is recorded at

the contract price.

2. If market price is less than the contract price, the purchase is recorded at the market

price.

D. If the contract period extends beyond the fiscal year:

1. If the market price at year-end is less than the contract price for outstanding purchase

commitments, a loss and corresponding liability are recorded for the difference.

PowerPoint Slides

A PowerPoint presentation of the chapter is available in the Connect library.

Teaching Transparency Masters

The following can be reproduced on transparency film as they appear here, or

LOWER OF COST AND NET REALIZABLE VALUE

➢ Inventories are reported at the lower of cost and net realizable value

(NRV).

➢ NRV is the estimated selling price of the product in the ordinary

course of business reduced by reasonably predictable costs of

completion, disposal, and transportation.

➢ These costs could include things such as sales commissions and

shipping costs. Companies often estimate these “costs to sell” by

applying a predetermined percentage to the selling price.

The Collins Company has five inventory items on hand at the end of 2016. The year-end unit costs

(determined by applying the average cost method), current unit selling prices, and estimated costs to

sell for each of the items are presented below:

Selling Estimated Costs

Item Cost Price To Sell

A $ 50 $100 $15

For each item we first compute NRV, selling price less estimated costs to sell, and then compare it

with cost. The item is valued at the lower of these two amounts.

Inventory

Item Cost NRV Value

A $50 $85* $50

*$100 – 15

Illustration 9-1

T9-1

INTERNATIONAL FINANCIAL REPORTING STANDARDS

Lower of cost and net realizable value. You just learned that in the United States

inventory is valued at the lower of cost and net realizable value. International

standards also value inventory this way.

However, there are some differences between U.S. GAAP and IFRS in this area.

IAS No. 2 specifies that if circumstances indicate that an inventory write-down is no

longer appropriate, it should be reversed. Reversals are not permitted under U.S.

GAAP.

T9-2

9-8 Intermediate Accounting,8/e

APPLYING THE LOWER OF COST AND NET

REALIZABLE VALUE RULE

➢ The lower of cost and net realizable value rule can be applied

to individual items, logical inventory categories, or the entire

inventory.

Lower of Cost and NRV

Item

Cost

Net

Realizable

Value

By

Individual

Items

By

Product

Line

By Total

Inventory

A

$ 50,000

$ 85,000

$ 50,000

Total A + B

$150,000

$175,000

$150,000

D

E

95,000

96,000

95,000

Total

$415,000

$431,000

Illustration 9-2

T9-3

THE GROSS PROFIT METHOD

➢ The gross profit method is useful in situations where

estimates of inventory are desirable.

► In determining the cost of inventory that has been lost,

stolen, or destroyed.

► In estimating inventory and cost of goods sold for

interim reports, avoiding the expense of a physical

inventory count.

► In auditors’ testing of the overall reasonableness of

inventory amounts reported by clients.

► In budgeting and forecasting.

➢ Provides only an approximation of inventory and is not

acceptable for the preparation of annual financial statements.

➢ Estimates cost of goods sold by multiplying the period’s net

sales by a historical gross profit percentage and then

subtracting that amount from net sales.

T9-4

GROSS PROFIT METHOD ILLUSTRATION

Southern Wholesale Company began 2016 with inventory of

$600,000, and on March 17 a warehouse fire destroyed the entire

inventory. Company records indicate net purchases of $1,500,000

and net sales of $2,000,000 prior to the fire. The gross profit

percentage in each of the previous three years has been very close

to 40%.

Beginning inventory (from records) $ 600,000

Plus: Net purchases (from records) 1,500,000

Goods available for sale 2,100,000

Less: Cost of goods sold:

Illustration 9-3

T9-5

THE RETAIL INVENTORY METHOD

➢ Similar to the gross profit method, the retail inventory method

relies on the relationship between cost and selling price to

estimate ending inventory and cost of goods sold.

➢ Ideal for high-volume retailers selling many different items at

low unit prices.

T9-6

9-12 Intermediate Accounting,8/e

RETAIL INVENTORY METHOD ILLUSTRATION

Home Improvement Store’s bank has asked for monthly financial

statements as a condition attached to a loan dated May 31, 2016.

To avoid a physical count of inventory, the company intends to use

the retail inventory method to estimate ending inventory and cost

of goods sold for the month of June.

Cost

Retail

Beginning inventory

$ 60,000

$100,000

Plus: Net purchases

Less: Net sales

Estimated ending inventory at retail

$160,000

Illustration 9-4

RETAIL TERMINOLOGY

Initial markup Original amount of markup from

cost to selling price.

T9-8

9-14 Intermediate Accounting,8/e

COST FLOW METHODS

➢ An advantage of the retail inventory method is

that the various cost flow methods can be

explicitly incorporated into the estimation

technique.

Home Improvement Stores, Inc. uses a periodic inventory

system and the retail inventory method to estimate ending

inventory and cost of goods sold. The following data are

available from the company’s records for the month of July 2016:

Cost Retail

Beginning inventory $ 99,200 $160,000

Net purchases 305,280 1 470,000 2

Net markups 10,000

Net markdowns 8,000

Net sales 434,000 3

1 Purchases at cost less returns, plus freight-in.

2 Original selling price of purchased goods less returns at retail.

3 Gross sales less returns.

Illustration 9-8

➢ Net markups and net markdowns are included in the retail

column to determine ending inventory at retail.

T9-9

APPROXIMATING AVERAGE COST

➢ To approximate average cost, the cost–to-retail percentage is

determined for all goods available for sale.

Cost

Retail

Beginning inventory

$ 99,200

$160,000

Plus: Net purchases

Net markups

Less: Net markdowns

Goods available for sale

Less: Net sales

Estimated ending inventory at retail

$198,000

Estimated ending inventory at cost (64% x $198,000)

Illustration 9-9

T9–10

9-16 Intermediate Accounting,8/e

THE CONVENTIONAL RETAIL METHOD

➢ To approximate lower of cost and net realizable value,

markdowns are not included in the calculation of the cost–to–

retail percentage. They are subtracted in the retail column

after the percentage is calculated.

➢ The logic for using this approximation is that a markdown is

evidence of a reduction in the utility of inventory.

Cost

Retail

Beginning inventory

$ 99,200

$160,000

Plus: Net purchases

Net markups

Less: Net markdowns

Goods available for sale

Less: Net sales

Estimated ending inventory at retail

Estimated ending inventory at cost (63.2% x $198,000)

Estimated cost of goods sold

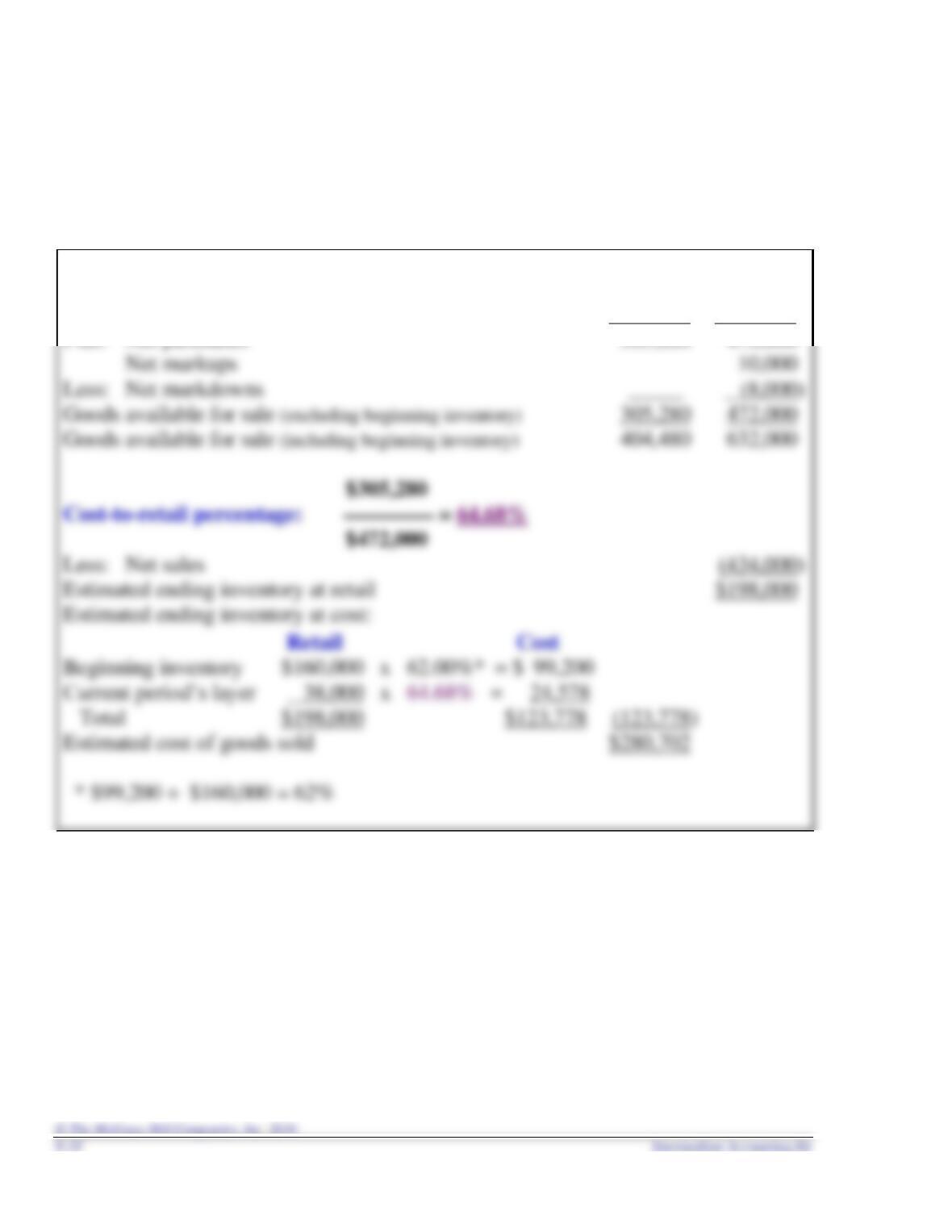

THE LIFO RETAIL METHOD

➢ In our illustration, the beginning inventory layer carries a

T9-12

THE LIFO RETAIL METHOD

(continued)

Cost

Retail

Beginning inventory

$ 99,200

$160,000

Plus: Net purchases

Less: Net markdowns

Goods available for sale (excluding beginning inventory)

Goods available for sale (including beginning inventory)

Less: Net sales

Estimated ending inventory at retail

$198,000

Estimated ending inventory at cost:

Beginning inventory $160,000 x 62.00%* = $ 99,200

Estimated cost of goods sold

$280,702

Illustration 9-11

T9-12(continued)