Archives

978-0077862374 Appendix B

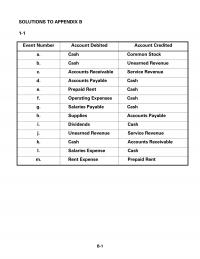

B-1 SOLUTIONS TO APPENDIX B 1-1 Event Number Account Debited Account Credited a. Cash Common Stock b. Cash Unearned Revenue c. Accounts Receivable Service Revenue d. Accounts Payable Cash e. Prepaid Rent Cash f. Operating Expenses Cash g. Salaries Payable […]

978-0077862374 Chapter 1 Lecture Note Part 1

Chapter 01 – An Introduction to Accounting Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1-1 General Comments for Chapter 1 An Introduction to Accounting The primary objective […]

978-0077862374 Chapter 1 Lecture Note Part 2

Chapter 01 – An Introduction to Accounting Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1-1 Demonstration Problem 1-1: Solution, part a. Equation Approach Effect of Events on […]

978-0077862374 Chapter 1 Solution Manual Part 1

1-7 ANSWERS TO QUESTIONS – CHAPTER 1 1. Stakeholders are the parties that use accounting information. Stakeholders with a direct interest include owners, managers, creditors, suppliers, and employees. These individuals are directly affected by what happens to the business. All […]

978-0077862374 Chapter 1 Solution Manual Part 2

EXERCISE 1-12 a. Investors put assets into the company with the expectation of sharing profits. Creditors lend assets to the company with the expectation of repayment of the principal plus interest on the loan. b. Clinton Company Accounting Equation Event […]

978-0077862374 Chapter 1 Solution Manual Part 3

1-7 XERCISE 1-21 g.(cont.) Wilson Company Statement of Cash Flows For the Year Ended December 31, 2014 Cash Flows From Operating Activities: Cash Receipts from Customers $500 Cash Payments for Expenses (300) Net Cash Flow from Operating Activities $ 200 […]

978-0077862374 Chapter 1 Solution Manual Part 4

1-1 PROBLEM 1-32 b. (cont.) Susan’s Consulting Balance Sheet As of December 31, 2015 Assets Cash $115,000 Land 40,000 Total Assets $155,000 Liabilities Notes Payable $ 5,000 Stockholders’ Equity Common Stock $70,000 Retained Earnings 80,000 Total Stockholders’ Equity 150,000 Total […]

978-0077862374 Chapter 10 Lecture Note

Chapter 10 – An Introduction to Management Accounting 10-1 Teaching Notes for Chapter 10 Managerial accounting requires teaching methods different from those used in financial accounting. In the introductory financial accounting course, instructors teach students about accounting standards. A primary […]

978-0077862374 Chapter 10 Solution Manual Part 1

10-1 If an effective JIT system is implemented, Ms. Connor would not have to keep any Exercise 10-16 a. The new inventory system is an approximate just–in-time system since it does not eliminate all inventory. b. Reduced cost of inventory: […]

978-0077862374 Chapter 10 Solution Manual Part 2

10-1 Problem 10-24 Event Assets = Equity Rev. – Exp. = N. Inc. Cash Flow No. Cash + Raw M. + WIP + Finished Goods + Office Furn. + Manuf. Equip. = Com. Stk. + Ret. Ear. BB 660,000 + […]

978-0077862374 Chapter 10 Solution Manual Part 3

Chapter 10 – Management Accounting: A Value-added Discipline Answers to questions 1. Financial accounting deals with regulated, historical, financial information that pertains to the whole company and is designed primarily to meet the information 2. The value-added principle means that […]

978-0077862374 Chapter 11 Lecture Note Part 2

12. What amount of sales in dollars must Boxware achieve each month in order to break even? a. $95,000 b. $190,000 c. $285,000 d. $380,000 13. How many units per month must Boxware sell in order to make a $110,000 […]

978-0077862374 Chapter 11 Lecture Note Part 3

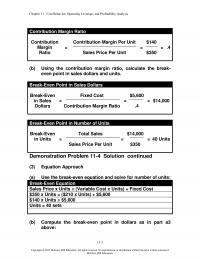

Chapter 11 – Cost Behavior, Operating Leverage, and Profitability Analysis 11-1 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Contribution Margin Ratio Contribution Contribution Margin Per Unit $140 […]

978-0077862374 Chapter 11 Solution Manual Part 1

Chapter 11 Cost Behavior, Operating Leverage, and Profitability Analysis Answer to questions 1. A fixed cost is a cost that in total remains constant as volume of activity changes but on a per unit basis varies inversely with changes in […]

978-0077862374 Chapter 11 Solution Manual Part 2

Exercise 11-16 a. Contribution margin Operating leverage = —–––——————— Net income $6,000 Operating leverage = ——————— = 1.5 $4,000 b. (10% Change in rev. x 1.5 Oper. leverage) = 15% change in net inc. 15% x $4,000 = $600 change […]

978-0077862374 Chapter 11 Solution Manual Part 3

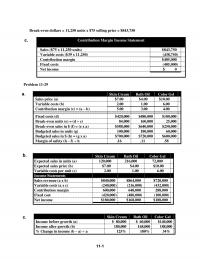

11-1 Break-even dollars = 11,250 units x $75 selling price = $843,750 Contribution Margin Income Statement Sales ($75 x 11,250 units) $843,750 Variable costs ($39 x 11,250) (438,750) Contribution margin $405,000 Fixed costs (405,000) Net income $ 0 Problem 11-29 […]

978-0077862374 Chapter 12 Lecture Note Part 1

Chapter 12 – Cost Accumulation, Tracing, and Allocation 12-1 Teaching Notes for Chapter 12 The topics in this chapter are critical. The need to make allocations causes widespread problems. A parent with one candy bar and two children has an […]

978-0077862374 Chapter 12 Lecture Note Part 2

Chapter 12 – Cost Accumulation, Tracing, and Allocation 12-1 Demonstration Problem 12-1 Solution b. continued Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. $84,000 ⎯⎯⎯⎯⎯ = $0.12 per […]

978-0077862374 Chapter 12 Solution Manual Part 1

Answers to questions 1. A cost object is something whose cost one is trying to determine the cost. Cost objects 2. Managers need timely cost information. They may have to sacrifice accuracy in order to get the information in time […]

978-0077862374 Chapter 12 Solution Manual Part 2

Chapter 12 Cost Accumulation, Tracing, and Allocation 12-1 Exercise 12-12 The allocation rate is computed below: Cost ÷ Base Computation Allocation Rate Rental cost ÷ No. units $360,000 ÷ 40,000 = $9 per unit Allocation Rate x Weight of Base […]

978-0077862374 Chapter 12 Solution Manual Part 3

Chapter 12 Cost Accumulation, Tracing, and Allocation 12-1 ATC 12-1 a. 1. Product 2. Fixed 3. Indirect b. Based on “actual” costs and actual production levels for each month independently, the cost per unit for February and March would be: […]

978-0077862374 Chapter 13 Lecture Note

Chapter 13 – Relevant Information for Special Decisions 13-1 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of Teaching Notes for Chapter 13 In this chapter, students learn to identify information […]

978-0077862374 Chapter 13 Solution Manual Part 1

Chapter 13 Relevant Information for Special Decisions Problem 13-28 a. Decision Division B Sales $ 600,000 Unit-level manufacturing costs (400,000) Rent on manufacturing facility (150,000) Unit-level selling and admin. expenses (28,000) Division-level fixed selling and admin. expenses (40,000) Contribution to […]

978-0077862374 Chapter 13 Solution Manual Part 2

Answers to Questions 1. Information that is relevant for decision making differs between the alternatives and is future oriented. 2. A variable cost may or may not be relevant. The fact that a cost is variable has no bearing on […]

978-0077862374 Chapter 13 Solution Manual Part 3

Exercise 13-16 The facility-level costs will continue even if the segment is eliminated. Accordingly, these costs are not avoidable. The original cost, book value and depreciation for the building avoidance of the real estate taxes. These and other relevant (avoidable) […]

978-0077862374 Chapter 14 Lecture Note Part 1

Chapter 14 – Planning for Profit and Cost Control Teaching Notes for Chapter 14 To simplify describing the budgeting process, this chapter focuses on a retail sales company that sells only one inventory item. Even so, the components of the […]

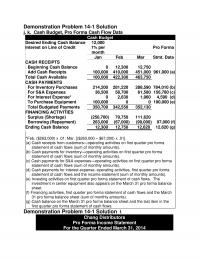

978-0077862374 Chapter 14 Lecture Note Part 2

Demonstration Problem 14-1 Solution j. k. Cash Budget, Pro Forma Cash Flow Data Cash Budget Desired Ending Cash Balance 12,000 Interest on Line of Credit 1% per month Pro Forma Jan Feb Mar Stmt. Data CASH RECEIPTS Beginning Cash Balance […]

978-0077862374 Chapter 14 Solution Manual Part 1

Chapter 14 Planning for Profit and Cost Control 14-1 Answers to Questions 1. Budgets are useful for large companies with complex activities as well as small companies. Budgets act as a vehicle for communication by formalizing management’s 2. The budget […]

978-0077862374 Chapter 14 Solution Manual Part 2

a. Schedule of Cash Payments for S&A Expenses July August September Salary expense $24,000 $24,000 $24,000 Prior month’s sales commissions, 100% 0 2,000 2,000 Supplies expense 360 390 420 Prior month’s utilities, 100% 0 1,100 1,100 Rent 6,600 6,600 6,600 […]

978-0077862374 Chapter 14 Solution Manual Part 3

ATC 14-1 a. Budgeted Financial Statements Income Statement Amounts Computations Sales Revenue $300,000 12 x $25,000 Cost of Goods Sold (264,000) 12 x $22,000 Depreciation Expense (3,000) ($18,000 – $6,000) ÷ 4 Other Expense (4,000) $22,000 – $18,000 Operating Income […]

978-0077862374 Chapter 15 Lecture Note Part 1

Chapter 15 – Performance Evaluation 15-1 Teaching Notes for Chapter 15 This chapter begins with the fundamental concepts underlying responsibility accounting and also provides students with a minimal explanation of flexible budgeting and variance analysis. Students need to know that […]

978-0077862374 Chapter 15 Lecture Note Part 2

Chapter 15 – Performance Evaluation 15-1 d. Suppose Murdoch changes its performance assessment measure from ROI to residual income (RI). Murdoch’s desired rate of return is 14%. Under these circumstances, should Hydride’s manager accept or reject the opportunity to invest […]

978-0077862374 Chapter 15 Solution Manual Part 1

Chapter 15 Performance Evaluation 15-1 Answers to questions 1. People, not budgets, control costs. Ms. Kelly needs to use the budget system to build maintain the desired control. 2. A responsibility center is the point in an organization where the […]

978-0077862374 Chapter 15 Solution Manual Part 2

Chapter 15 Performance Evaluation 15-1 Sales revenue $45.00 $1,350,000 $1,305,000 $1,395,000 Variable manufacturing costs Materials $9.00 (270,000) (261,000) (279,000) Labor $4.50 (135,000) (130,500) (139,500) Overhead $6.30 (189,000) (182,700) (195,300) Variable S,G,&A $7.20 (216,000) (208,800) (223,200) Contribution margin 540,000 522,000 558,000 […]

978-0077862374 Chapter 16 Lecture Note

Chapter 16 – Planning for Capital Investments 16-1 Teaching Notes for Chapter 16 Before this chapter, many students have not studied the time value of money concept. Although students have some intuitive sense of the concept (they want their money […]

978-0077862374 Chapter 16 Solution Manual Part 1

Chapter 16 Planning for Capital Investments 16-1 Answers to Questions 1. A capital investment is an investment in a long-term operational asset. Stocks and bonds are not operational assets but rather intangible legal agreements of ownership in another company or […]

978-0077862374 Chapter 16 Solution Manual Part 2

Chapter 16 Planning for Capital Investments 16-1 must sit idle, then Alternative 2 may be the better option if Speedy Delivery actually has that much money. The information provided is insufficient to determine which the better alternative is. Problem 16-17 […]

978-0077862374 Chapter 16 Solution Manual Part 3

Chapter 16 Planning for Capital Investments 16-1 a (1) Cash Inflow Table Value* Present Value Year 1 $ 360,000 0.892857 $ 321,429 Year 2 502,500 0.797194 400,590 Year 3 865,000 0.711780 615,690 Year 3 5,175,000 0.711780 3,683,462 Present value of […]

978-0077862374 Chapter 2 Lecture Note Part 2

Demonstration Problem 2-2 Solution, part A. Horizontal Financial Statements Model for 2014 A spreadsheet is embedded to reflect the solution to this question. This spreadsheet covers both 2014 and 2015. The workpaper for students’ use in answering this question would […]

978-0077862374 Chapter 2 Solution Manual Part 1

ANSWERS TO QUESTIONS – CHAPTER 2 1. Accrual accounting attempts to record the effects of accounting events in the period 2. Recognition is the act of recording an event in the financial statements. When accruals are used, events are recognized […]

978-0077862374 Chapter 2 Solution Manual Part 2

2-1 EXERCISE 2-6 a. & c. Event Revenue Expense Statement of Cash Flows 1. NA NA $50,000 FA 2. $67,000 NA NA 3. NA NA (5,000) FA 4. NA NA 45,000 OA 5. NA $49,000 (49,000) OA 6. 10,000 NA […]

978-0077862374 Chapter 2 Solution Manual Part 3

2-1 EXERCISE 2-16 a. Ed Arnold Personal Financial Planning Horizontal Statements Model for 2014 Assets = Liabilities + Stk. Equity Income Statement Statement Event Cash = Unearned Revenue + Retained Earnings Rev. − Exp. = Net Income of Cash Flows […]

978-0077862374 Chapter 2 Solution Manual Part 4

2–1 SOLUTIONS TO PROBLEMS – CHAPTER 2 PROBLEM 2-32 James Cleaning Company Effect of Events on the Financial Statements Balance Sheet Income Statement Stmt. of Assets = Liabilities + Stock. Equity Rev. − Exp. = Net Inc. Cash Flows Even […]

978-0077862374 Chapter 2 Solution Manual Part 5

2-1 PROBLEM 2-38. (cont.) Alabama Service Company Accounting Equation for 2015 Assets = Liabilities + Stk. Equity Event Type of Event Cash Accts. Rec. Supp. Prepd. Rent Int. Rec. Land = Accts. Pay. Salaries Payable Unearn. Revenue + Com. Stock […]

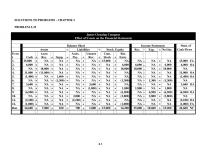

978-0077862374 Chapter 3 Lecture Note Part 1

General Comments for Chapter 3 Accounting for Merchandising Businesses Chapter 3 introduces accounting for inventory transactions using the perpetual method. In today’s high-technology environment, the perpetual system has become the predominant method of accounting for inventories. Because the periodic method […]

978-0077862374 Chapter 3 Lecture Note Part 2

Chapter 03 – Accounting for Merchandising Businesses 3-1 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of Quiz Questions for Chapter 3 1. Under the perpetual inventory method, a. assets increase […]

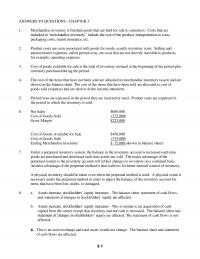

978-0077862374 Chapter 3 Solution Manual Part 1

3-1 ANSWERS TO QUESTIONS – CHAPTER 3 1. Merchandise inventory is finished goods that are held for sale to customers. Costs that are 2. Product costs are costs associated with goods for resale, usually inventory costs. Selling and administrative expenses, […]

978-0077862374 Chapter 3 Solution Manual Part 2

3-1 EXERCISE 3-3 (cont.) b. Justin Swords Merchandising Income Statement For the Year Ended December 31, 2014 Net Sales $82,000 Cost of Goods Sold (48,000) Gross Margin 34,000 Operating Expenses -0- Net Income $34,000 c. Total assets: $104,000 (Cash $92,000 […]

978-0077862374 Chapter 3 Solution Manual Part 3

3-1 EXERCISE 3-12 a. Annual rate = Discount rate x (365 days ÷ Discount term*) b. Since the annualized discount rate (36.5%) is significantly higher than the cost of borrowing (7%) Jordan should borrow the money and payoff the liability […]

978-0077862374 Chapter 3 Solution Manual Part 4

3-1 PROBLEM 3-23 (cont.) b. & c. Yang’s Imports Financial Statements For the Month Ended September 30, 2014 Income Statement Net Sales $19,000 Cost of Goods Sold (10,000) Gross Margin 9,000 Operating Expenses Selling and Adm. Expense (2,450) Net Income […]

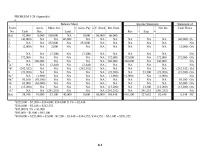

978-0077862374 Chapter 3 Solution Manual Part 5

3-1 PROBLEM 3-28 (Appendix) a. Balance Sheet Income Statement Statement of Event No. Cash Accts. Rec. Mdse. Inv. Land = Accts. Pay + C. Stock Ret. Earn. Rev. − Exp. = Net Inc. Cash Flows Bal. 52,000 8,000 100,000 NA […]

978-0077862374 Chapter 4 Lecture Note

Chapter 04 – Internal Controls, Accounting for Cash, and Ethics 4-1 General Comments for Chapter 4 Internal Controls, Accounting for Cash, and Ethics This chapter explains internal controls, which are the policies and procedures used to provide reasonable assurance that […]

978-0077862374 Chapter 4 Solution Manual Part 1

ANSWERS TO QUESTIONS – CHAPTER 4 2. Internal control is the process designed to ensure reliable financial reporting, effective and efficient operations, and compliance with applicable laws and regulations. 3. Section 404 of Sarbanes-Oxley requires a statement of management’s responsibility […]

978-0077862374 Chapter 4 Solution Manual Part 2

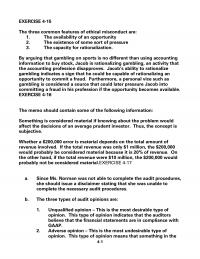

4-1 1 EXERCISE 4-15 The three common features of ethical misconduct are: 1. The availability of an opportunity By arguing that gambling on sports is no different than using accounting information to buy stock, Jacob is rationalizing gambling, an activity […]

978-0077862374 Chapter 5 Lecture Note Part 2

Chapter 05 – Accounting for Receivables and Inventory Cost Flow 5-1 WORK PAPERS FOR DEMONSTRATION PROBLEMS Demonstration Problem 5-1: Work Paper, part a. Statements Model, 2014 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the […]

978-0077862374 Chapter 5 Solution Manual Part 1

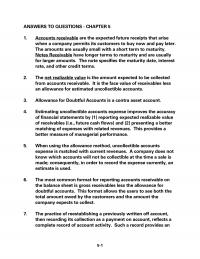

5-1 ANSWERS TO QUESTIONS – CHAPTER 5 1. Accounts receivable are the expected future receipts that arise when a company permits its customers to buy now and pay later. rate, and other credit terms. 2. The net realizable value is […]

978-0077862374 Chapter 5 Solution Manual Part 2

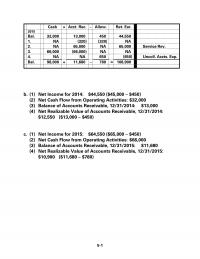

5-1 Cash + Acct. Rec. − Allow. Ret. Ear. 2015 Bal. 32,000 13,000 450 44,550 1. NA (320) (320) NA 2. NA 65,000 NA 65,000 Service Rev. 3. 66,000 (66,000) NA NA 4. NA NA 650 (650) Uncoll. Accts. Exp. […]

978-0077862374 Chapter 5 Solution Manual Part 3

5-1 EXERCISE 5-11 Balance Sheet Income Statement Statement of Date Assets = Equity Rev. − Exp. = Net Inc. Cash Flows Cash + Note Rec. + Int. Rec. = Ret. Ear. 1. 9/1/14 (30,000) 30,000 NA NA NA NA NA […]

978-0077862374 Chapter 5 Solution Manual Part 4

5-1 Net Income $34,790 LIFO Sales (3,500 @ $50) $175,000 Cost of Goods Sold: From 10/1 Purchase 1,000 units @ $32 = $32,000 From 4/1 Purchase 2,500 units @ $30 = 75,000 Cost of Goods Sold (107,000) Gross Margin 68,000 […]

978-0077862374 Chapter 5 Solution Manual Part 5

5-1 PROBLEM 5-25 b. (cont.) Frankel Inc. Balance Sheet As of the End of the Year 2014 Assets Cash $ 40,000 Accounts Receivable $32,000 Less, Allowance for Doubtful Accounts (2,102) 29,898 Merchandise Inventory 45,000 Total Assets $114,898 Liabilities Accounts Payable […]

978-0077862374 Chapter 5 Solution Manual Part 6

5-1 PROBLEM 5-30 b. (cont.) Iupe Supply Company Balance Sheet As of the End of the Year 2014 Assets Cash $51,350 Accounts Receivable $3,700 Less, Allowance for Doubtful Accounts (185) 3,515 Merchandise Inventory 25,000 Total Assets $79,865 Liabilities $ -0- […]

978-0077862374 Chapter 5 Solution Manual Part 7

5-1 1 ACT 5-2 a. Robin Co. Goods Available for Sale Beginning Inventory 100 @ $50 = $ 5,000 70 @ 55 = 3,850 First Purchase 100 @ 54 = 5,400 Second Purchase 250 @ 58 = 14,500 Total 520 […]

978-0077862374 Chapter 6 Lecture Note Part 1

Chapter 06 – Accounting for Long-Term Operational Assets 6-1 General Comments for Chapter 6 Accounting for Long-Term Operational Assets This chapter explains how acquiring, using, and disposing of long-term operational assets affect financial statements. Because these activities span several accounting […]

978-0077862374 Chapter 6 Lecture Note Part 2

Chapter 06 – Accounting for Long-Term Operational Assets 6-1 Demonstration Problem 6-1: Work Paper, Scenario 2 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Double-Declining-Balance Depreciation Income Statements […]

978-0077862374 Chapter 6 Solution Manual Part 1

6-1 ANSWERS TO QUESTIONS – CHAPTER 6 1. Long-term operational assets are those assets that are used by a business to generate 2. Tangible assets are those assets that have a physical existence. Some examples include buildings and equipment. Intangible […]

978-0077862374 Chapter 6 Solution Manual Part 2

6-1 2016: ($47,000 − $30,080) x (2 x .20) = 6,768 *Since the total depreciable cost is $40,000 ($47,000 − $7,000), the total depreciation taken in 2017 is $3,152 ($40,000 − $36,848). Consequently, there is no depreciation deducted in 2018. […]

978-0077862374 Chapter 6 Solution Manual Part 3

6-1 PROBLEM 6-25 Zhao Company Financial Statements For the Year Ended December 31 Income Statements 2014 2015 2016 2017 2018 Revenue $9,500 $10,000 $10,500 $8,500 $ -0– Depr. Expense* (9,000) (9,000) (9,000) (9,000) -0- Oper. Income (Loss) 500 1,000 1,500 […]

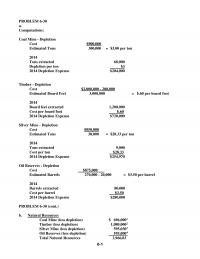

978-0077862374 Chapter 6 Solution Manual Part 4

6-1 PROBLEM 6-30 a. Computations: Coal Mine – Depletion Cost $900,000 = $3.00 per ton Estimated Tons 300,000 2014 Tons extracted 68,000 Depletion per ton $3 2014 Depletion Expense $204,000 Timber – Depletion Cost $2,000,000 – 200,000 = $.60 per […]

978-0077862374 Chapter 7 Lecture Note Part 1

General Comments for Chapter 7 Accounting for Liabilities Chapter 7 introduces the accounting for both current and long-term liabilities and the preparation of a classified balance sheet. Throughout the chapter, the focus is on how liabilities and interest expense affect […]

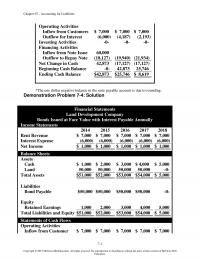

978-0077862374 Chapter 7 Lecture Note Part 2

Chapter 07 – Accounting for Liabilities 7-1 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Operating Activities Inflow from Customers $ 7,000 $ 7,000 $ 7,000 Outflow for […]

978-0077862374 Chapter 7 Solution Manual Part 1

7-1 ANSWERS TO QUESTIONS – CHAPTER 7 1. Cash payments to creditors is an asset use transaction. This type of transaction will reduce both assets and liabilities. 3. The entry to record accrued interest consists of an increase to Interest […]

978-0077862374 Chapter 7 Solution Manual Part 2

7-1 (3) Cash Flows From Financing Activities: Inflow from Issue of Note $50,000 Outflow to Repay Note (8,959) Net Cash Flow from Financing Activities $41,041 d. Principal 1/1/15: $41,041 (see schedule in book) Interest Expense: $41,041 x 5% = $2,052.05 […]

978-0077862374 Chapter 7 Solution Manual Part 3

$21,928 − $20,000 = $1,928 Beginning Discount − Amortization = Ending Discount $30,723 − $1,928 = $28,795 Bond Carrying Value as of December 31, 2014 Bond Payable (Face Value) $250,000 Discount on Bonds Payable 28,795 Carrying Value $221,205 EXERCISE 7-24 […]

978-0077862374 Chapter 7 Solution Manual Part 4

7-1 April $210,000 x 6% x 1/12 $1,050 May $380,000 x 7% x 1/12 2,217 June $250,000 x 7% x 1/12 1,458* *rounded b. The amount of cash paid for interest is the same as interest expense. Interest is paid […]

978-0077862374 Chapter 8 Lecture Note

Chapter 08 – Proprietorships, Partnerships, and Corporations 8-1 General Comments for Chapter 8 Proprietorships, Partnerships, and Corporations Chapter 8 explains accounting for equity transactions. It describes the three primary forms of business organizations (sole proprietorship, partnership, and corporation), along with […]

978-0077862374 Chapter 8 Solution Manual Part 1

ANSWERS TO QUESTIONS – CHAPTER 8 1. The three major forms of business organizations are the sole proprietorship, the partnership, and the corporation. The sole proprietorship is a business owned by one individual. The partnership is a business that is […]

978-0077862374 Chapter 8 Solution Manual Part 2

Stockholders’ Equity Common Stock, $10 par value, 10,000 shares issued and outstanding $100,000 Paid-In Capital in Excess of Par 60,000 Total Paid-In Capital 160,000 Retained Earnings 19,500 Total Liabilities and Stockholders’ Equity $179,500 Statement of Cash Flows For the Year […]

978-0077862374 Chapter 8 Solution Manual Part 3

8-1 PROBLEM 8-22 a. NC = Net Change in Cash Concord Corp. Statements Model For 2014 Balance Sheet Income Statement Statement of Event Assets = Stockholders’ Equity Rev. − Exp. = Net Inc. Cash Flows Pfd. Stk. + Com. Stk. […]

978-0077862374 Chapter 8 Solution Manual Part 4

11-8 Investments 72,000 48,000 120,000 Net Income* 9,600 14,400 24,000 Withdrawals (3,500) (1,500) (5,000) Ending Capital Balances $78,100 $60,900 $139,000 *Moore: $24,000 x 40% = $9,600 Pounds: $24,000 x 60% = $14,400 PROBLEM 8-18 b. (cont.) Auto Spa Company Financial […]

978-0077862374 Chapter 9 Lecture Note Part 1

Chapter 09 – Financial Statement Analysis 9-1 Teaching Notes for Chapter 9 We have provided a comprehensive demonstration problem for Chapter 9. The requirements of the demonstration problem coincide with the flow of material covered in the chapter. We suggest […]

978-0077862374 Chapter 9 Lecture Note Part 2

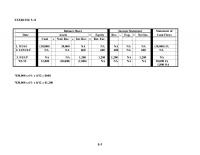

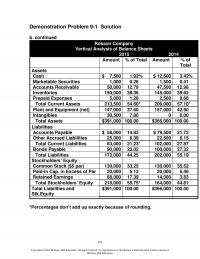

9-9 Demonstration Problem 9-1 Solution b. continued Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Rosson Company Vertical Analysis of Balance Sheets 2015 2014 Amount % of Total […]

978-0077862374 Chapter 9 Solution Manual Part 1

9-1 Answers to Questions 1. Ratios and trends are useful tools for analyzing financial statements because they give the analyst a basis for comparing companies of different sizes and characteristics. 2. “Liquidity” is the short-term ability to convert assets to […]

978-0077862374 Chapter 9 Solution Manual Part 2

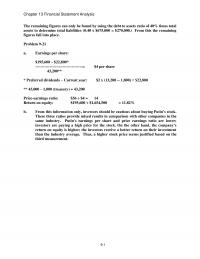

Chapter 13 Financial Statement Analysis 9-1 The remaining figures can only be found by using the debt to assets ratio of 40% times total assets to determine total liabilities (0.40 x $675,000 = $270,000.) From this the remaining figures fall […]

AC 174

How should liabilities (except for deferred income taxes) be reported by a company using fresh start accounting? A.at the undiscounted sum of future cash payments. B.at book value prior to the reorganization. C.as partially secured liabilities. D.at the present value […]

AC 193 Test 1

The goals of the SEC include all except which one of the following? A.prohibiting the dissemination of materially misstated information. B.controlling the number of companies whose stock is listed on major stock exchanges. C.regulating the operation of securities markets. D.ensuring […]

AC 250

Which of the following costs should be recorded as an expense? A.Administrative employee salaries B.Depreciation of manufacturing equipment C.Insurance for the factory building D.All of these are expenses. The following balance sheet information was provided by Western Company: Assuming 2014 […]

AC 352 Test 2

Ashley projects that she can get $100,000 cash per year for 5 years on a real estate investment project. If Ashley wants to earn a rate of return of 12%, what is the maximum that she should pay for the […]

AC 469 Quiz 1

The cost of capital is sometimes referred to as the hurdle or discount rate. A payment to an employee in settlement of salaries payable decreases an asset and decreases a liability. Answer: TRUE The event decreases assets (cash) and decreases […]

AC 691

Cleary, Wasser, and Nolan formed a partnership on January 1, 2012, with investments of $100,000, $150,000, and $200,000, respectively. For division of income, they agreed to (1) interest of 10% of the beginning capital balance each year, (2) annual compensation […]

AC 816 Quiz 2

The SEC’s operating costs are supported through A.tax revenues of the federal government. B.registration fees charged to issuers offering securities to the public. C.fees paid by stock exchanges. D.fees paid by stock brokers. E.fees paid by accounting firms that practice […]

ACC 238 Final

What is the effect on the balance sheet of making cash sales of inventory to customers on profit? A.Assets and equity increase. B.Assets and equity decrease. C.Assets decrease and equity increases. D.Assets increase and equity decreases. Cash inflows generated by […]

ACC 405 Quiz

A company that incurred $1,000 in production costs reported cost of goods sold of $800 and selling costs of $100. Its ending finished goods inventory was $300. The assumption regarding ordinary annuities is that cash flows occur at the end […]

Acc 504 Grayson Company is

Grayson Company is considering purchase of equipment that costs $49,000 and is expected to offer annual cash inflows of $13,000. Grayson’s minimum required rate of return is 10%. How many years must the cash flows last, for the investment to […]

ACC 560

On January 1, 2013, Baird Company had beginning balances as lows: Assets = $2,250 Liabilities = $620 Common Stock = $800 During 2013, Baird paid dividends to its stockholders of $900. Given that ending retained earnings was $600, what was […]

Acc 593

Long-term creditors are usually most interested in evaluating: A.Liquidity. B.Managerial effectiveness. C.Solvency. D.Profitability. In countries of Latin America: A.accounting practice is designed to provide adequate information to investors and creditors. B.accounting standards emphasize accounting for high inflation situations. C.banks are […]

ACC 801 Homework

Which of the following events would not require an end-of-year adjusting entry? A.Purchasing supplies for cash B.Providing services on account C.Purchasing a 12-month insurance policy on July 1 D.All of these would require an end-of-year adjustment Which of the following […]

Accounting 262

Cleary, Wasser, and Nolan formed a partnership on January 1, 2012, with investments of $100,000, $150,000, and $200,000, respectively. For division of income, they agreed to (1) interest of 10% of the beginning capital balance each year, (2) annual compensation […]

Accounting 313 Quiz 2

Mackie Company provided $25,500 of services on account, and collected $18,000 from customers during the year. The company also incurred $17,000 of expenses on account, and paid $15,400 against its payables. As a result of these events. A.total assets would […]

Accounting 497 Quiz 2 Donald

Donald, Anne, and Todd have the following capital balances; $40,000, $50,000 and $30,000 respectively. The partners share profits and losses 20%, 40%, and 40% respectively. Anne retires and is paid $80,000 based on the terms of the original partnership agreement. […]

ACCT 119 Peter Roberts and Dana

Peter, Roberts, and Dana have the following capital balances; $80,000, $100,000 and $60,000, respectively. The partners share profits and losses 20%, 40%, and 40% respectively. Roberts retires and is paid $160,000 based on an independent appraisal of the business. If […]

ACCT 131 Quiz 2

Select the incorrect statement regarding the analysis of absolute amounts of various accounts reported on the financial statements. A.Financial statement users with expertise in particular industries can look at absolute amounts and assess a company’s performance in a certain area. […]

Acct 161 Quiz 2

Norris Company experienced the following transactions during 2013, its first year in operation. 1) Issued $6,000 of common stock to stockholders. 2) Provided $2,300 of services on account. 3) Paid $1,600 cash for operating expenses. 4) Collected $1,900 of cash […]

Acct 485 Final

Finnegan Company plans to invest in a new operating plant that is expected to cost $500,000. The projected incremental income from the investment is as follows: The unadjusted rate of return on the initial investment would be approximately: A.8.0%. B.6.0%. […]

ACCT 513

The capital account balances for Donald & Hanes LLP on January 1, 2013, were as follows: Donald and Hanes shared net income and losses in the ratio of 3:2, respectively. The partners agreed to admit May to the partnership with […]

ACCT 673 Quiz 3

Indicate whether each of the following statements is true or false. 1> Some forms of financial statement analysis involve identifying changes in the same item for the same company over a period of time. 2> Some forms of financial statement […]

Acct 748 Test 2

A business’s temporary accounts include revenues, expenses, and retained earnings. A company may recognize a revenue or expense without a corresponding cash collection or payment in the same accounting period. Answer: TRUE Accrual basis companies recognize revenue when earned and […]

ACT 465 Midterm

A partnership began its first year of operations with the following capital balances: Young, Capital: $143,000 Eaton, Capital: $104,000 Thurman, Capital: $143,000 The Articles of Partnership stipulated that profits and losses be assigned in the following manner: Young was to […]

ACT 554 Midterm 2

Cleary, Wasser, and Nolan formed a partnership on January 1, 2012, with investments of $100,000, $150,000, and $200,000, respectively. For division of income, they agreed to (1) interest of 10% of the beginning capital balance each year, (2) annual compensation […]

ACT 835 Test 1

Indicate whether each of the following statements is true or false. 1) Deposits in transit appear on the bank statement as credit memos 2) Service fees charged by a bank appear on bank statements as debit memos 3) Credit memos […]

ACT 837 Quiz 1

The following balance sheet information is provided for Apex Company for 2014: What is the company’s working capital? A.$20,300 B.$4,900 C.$22,900 D.$24,500 Which one of the following is not a prescribed event for the filing of Form 8-K? A.bankruptcy or […]

MET MG 360 Midterm

Foreign companies whose stock is listed on a U.S. stock exchange and using foreign GAAP other than IFRS must file their annual report with the SEC on: A.Form 8-A. B.Form 10-A. C.Form 16-K. D.Form 20-F. E.Form 20-K. Which of the […]

MET MG 368 Quiz 3

Ruiz Company provided services for $15,000 cash during the 2013 accounting period. Ruiz incurred $12,000 expenses on account during 2013, and by the end of the year, $3,000 of that amount had been paid with cash. Assuming that these are […]

MET MG 479 Midterm 2

Current financial reporting standards assume that users of accounting information: A.Have an expert’s understanding of economic and financial events and conditions. B.Have a reasonably informed knowledge of business. C.Have widely differing levels of knowledge about business, and that financial reporting […]

SMG AC 132 Test 1

Cleary, Wasser, and Nolan formed a partnership on January 1, 2012, with investments of $100,000, $150,000, and $200,000, respectively. For division of income, they agreed to (1) interest of 10% of the beginning capital balance each year, (2) annual compensation […]

SMG AC 236 Midterm 2

A U.S. company has many foreign subsidiaries and wants to convert its consolidated financial statements from U.S. GAAP to IFRS. Which of the following items is not one of the likely accounting issues to resolve for the opening IFRS balance […]

SMG AC 278 Midterm 1

Which of the following transactions would cause net income for the period to decrease? A.Paid $2,500 cash for raw material cost B.Purchased $8,000 of merchandise inventory C.Recorded $5,000 of depreciation on production equipment D.Paid $2,000 for production supplies On January […]

SMG AC 406 Quiz 1

Mary needs to have $20,000 one year from today. The formula to compute the amount of money that must be invested today is future value/(1 – interest rate). Equity represents the future obligations of a business entity. Answer: FALSE This […]

SMG AC 607 Test

Matt needs to compute the present value of $5,000 to be received four years from now. He should multiple $5,000 by the appropriate present value interest factor obtained from the present value of $1 table. After closing, only balance sheet […]

SMG AC 653 Quiz 3

As of December 31, 2013, Gant Corporation had a current ratio of 1.29, quick ratio of 1.05, and working capital of $18,000. The company uses a perpetual inventory system and sells merchandise for more than it cost. On January 1, […]

SMG AC 671 Quiz 2

Yi Company began operations on January 1, 2013. During 2013, the company engaged in the following cash transactions: 1) issued stock for $40,000 2) borrowed $25,000 from its bank 3) provided consulting services for $38,000 4) paid back $15,000 of […]