Exercise 13-16

The facility-level costs will continue even if the segment is eliminated. Accordingly, these

costs are not avoidable. The original cost, book value and depreciation for the building

avoidance of the real estate taxes. These and other relevant (avoidable) costs are listed below.

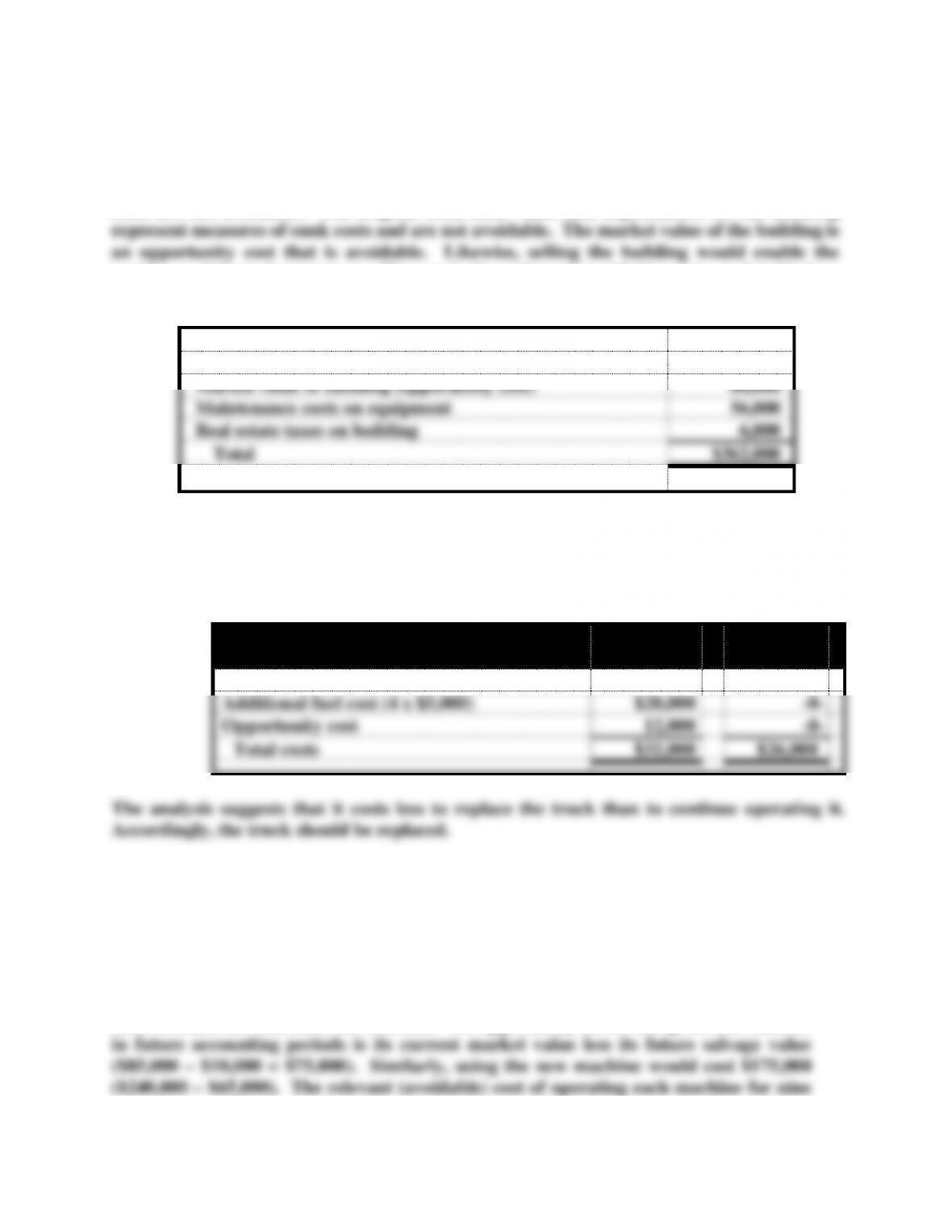

Advertising expense

$ 70,000

Supervisory salaries

150,000

Market value of building (opportunity cost)

80,000

Maintenance costs on equipment

56,000

Real estate taxes on building

6,000

Total

$362,000

Exercise 13-17

The original cost and book value of the old truck are not relevant because they are sunk costs.

The relevant costs are shown below:

Decision

Keep

Old

Replace

With New

Cost of the new truck

$26,000

Additional fuel cost (4 x $5,000)

$20,000

-0-

Opportunity cost

12,000

-0-

Total costs

$32,000

$26,000

Exercise 13-18

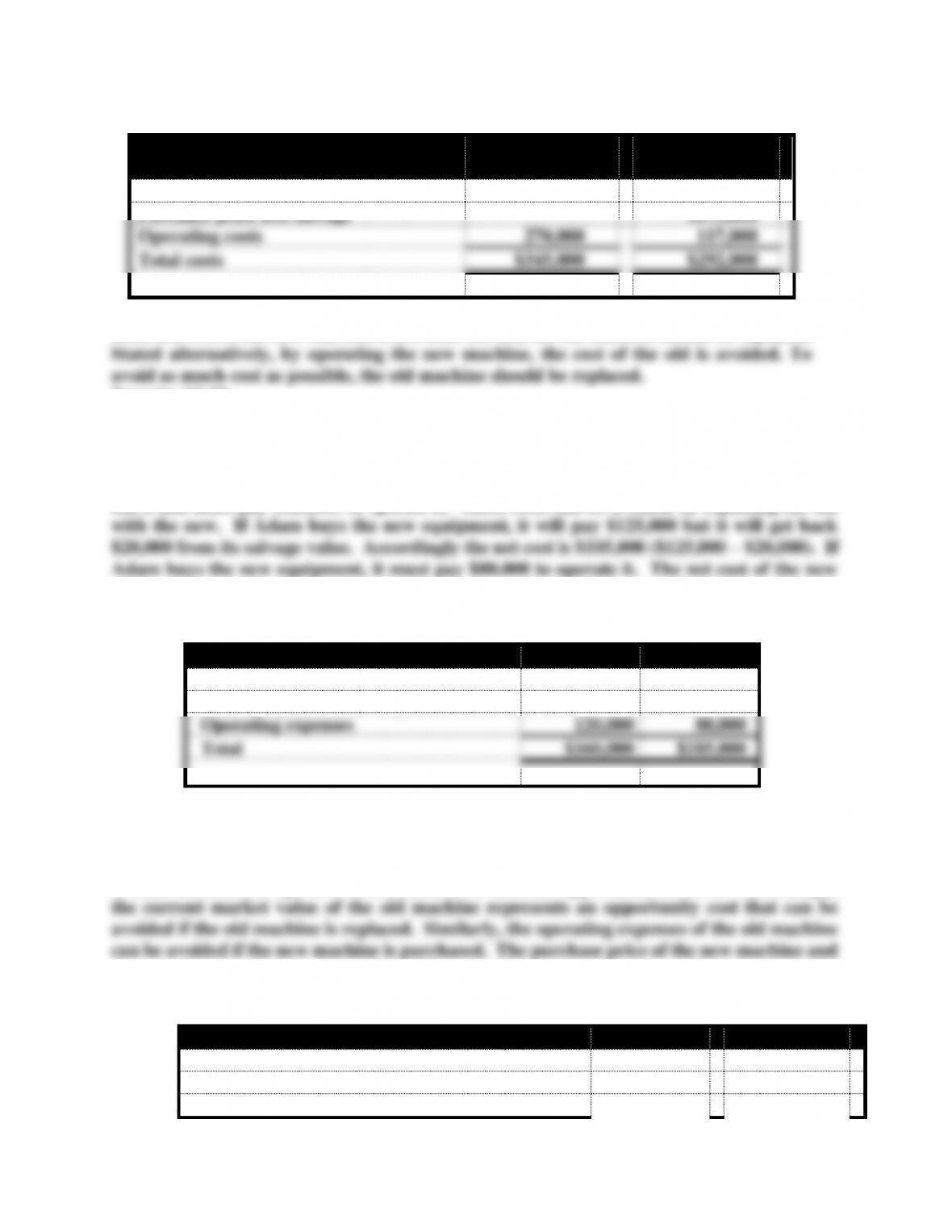

The original cost and book value of the old machine are different measures of the same

sunk cost and are therefore not relevant. The opportunity cost of using the old machine

years is shown below:

Decision

Keep Old Machine

Purchase New

Machine

Opportunity cost

$ 75,000

Purchase price less salvage

$175,000

Operating costs

270,000

117,000

Total costs

$345,000

$292,000

Since the cost of the new machine is less than the old, the old machine should be replaced.

Exercise 13-19

The opportunity cost of using the existing equipment is its market value less the salvage value

($60,000 – $20,000 = $40,000). If the old equipment is kept, Adam loses the opportunity to

sell it and must pay $120,000 to operate it. These costs can be avoided by replacing the old

equipment and its operating expenses can be avoided by keeping the old equipment.

Accordingly, the avoidable costs are summarized below.

Old

New

Opportunity cost less salvage

$ 40,000

Purchase price less salvage

$105,000

Operating expenses

120,000

80,000

Total

$160,000

$185,000

Since the relevant costs of operating the new equipment are higher, the old equipment should

be retained. Exercise 13-20

If Bach continues to operate the old machine, it loses the opportunity to sell it. Accordingly,

its operating expenses can be avoided if Bach continues to use the old machine. Accordingly,

the avoidable costs are summarized below.

Decision

Keep Old

Buy New

Opportunity cost of old machine

$ 40,000

Purchase price

$150,000

Operating expenses (4 x $50,000)

200,000

Operating expenses (4 x $18,000)

72,000

Total avoidable costs

$240,000

$222,000

Since the costs of operating the new machine are lower, the old machine should be replaced.

Exercise 13-21

a. The original cost and book value are sunk costs that are not relevant. The annual

opportunity cost computed on a straight-line basis is as follows: ($95,000 Current

b. The total lease cost over the four-year contract is $80,000 ($20,000 x 4). Since the

total cost of the lease is less than the total opportunity cost ($95,000 Current market

Problem 13-22

There are many possible answers for each requirement. The following represents a single

example of a correct solution for each part. Students’ answers may differ from the ones

supplied here.

a. Assume unit-level materials cost differs between two alternative products. A portion

of the materials cost would be avoidable with respect to a decision regarding which

b. Assume a special order requires starting a new batch of work. The setup costs could

be avoided by rejecting the special order. In contrast, assume that the special order

c. Suppose advertising cost is incurred for the benefit of a particular store of JCPenney.

The advertising cost could be avoided if the store were closed. In contrast, assume

d. Assume a company pays rent on its manufacturing facility. The rent would be

e. Consider a decision regarding the replacement of old manufacturing equipment with

Problem 13-23

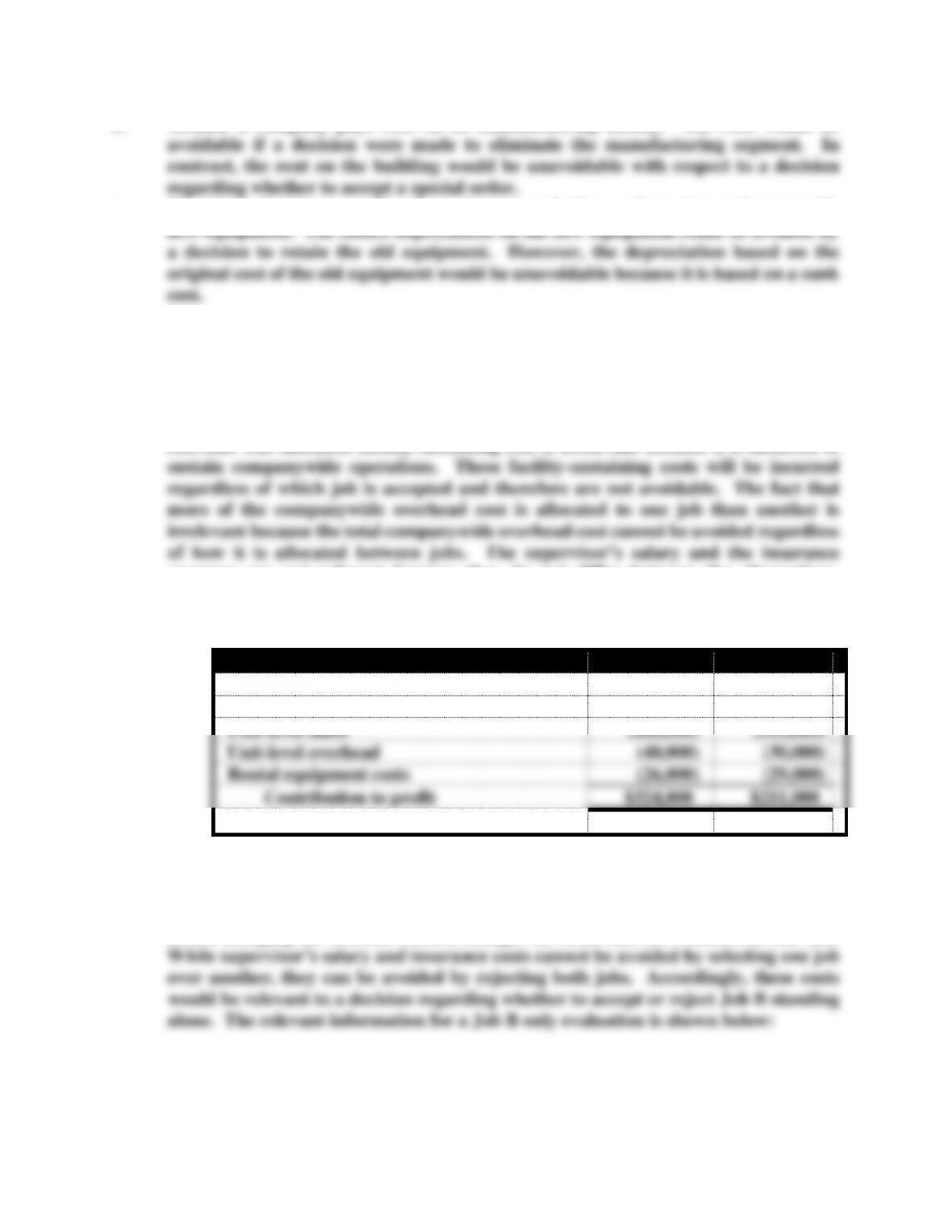

a. With respect to a decision regarding the selection of Job A versus Job B, the

differential revenue and the avoidable costs that differ between the alternatives are

relevant. The allocated facility-sustaining cost is irrelevant because it is incurred to

coverage are not relevant because they do not differ between the alternatives.

Depreciation is a sunk cost and is irrelevant. These costs will be the same regardless

of which alternative is accepted. The relevant information is summarized below:

Decision:

Job A

Job B

Contract price

$900,000

$800,000

Unit-level materials

(250,000)

(220,000)

Unit-level labor

(260,000)

(310,000)

Unit-level overhead

(40,000)

(30,000)

Rental equipment costs

(26,000)

(29,000)

Contribution to profit

$324,000

$211,000

Since Job A provides the higher contribution to profit, it should be accepted.

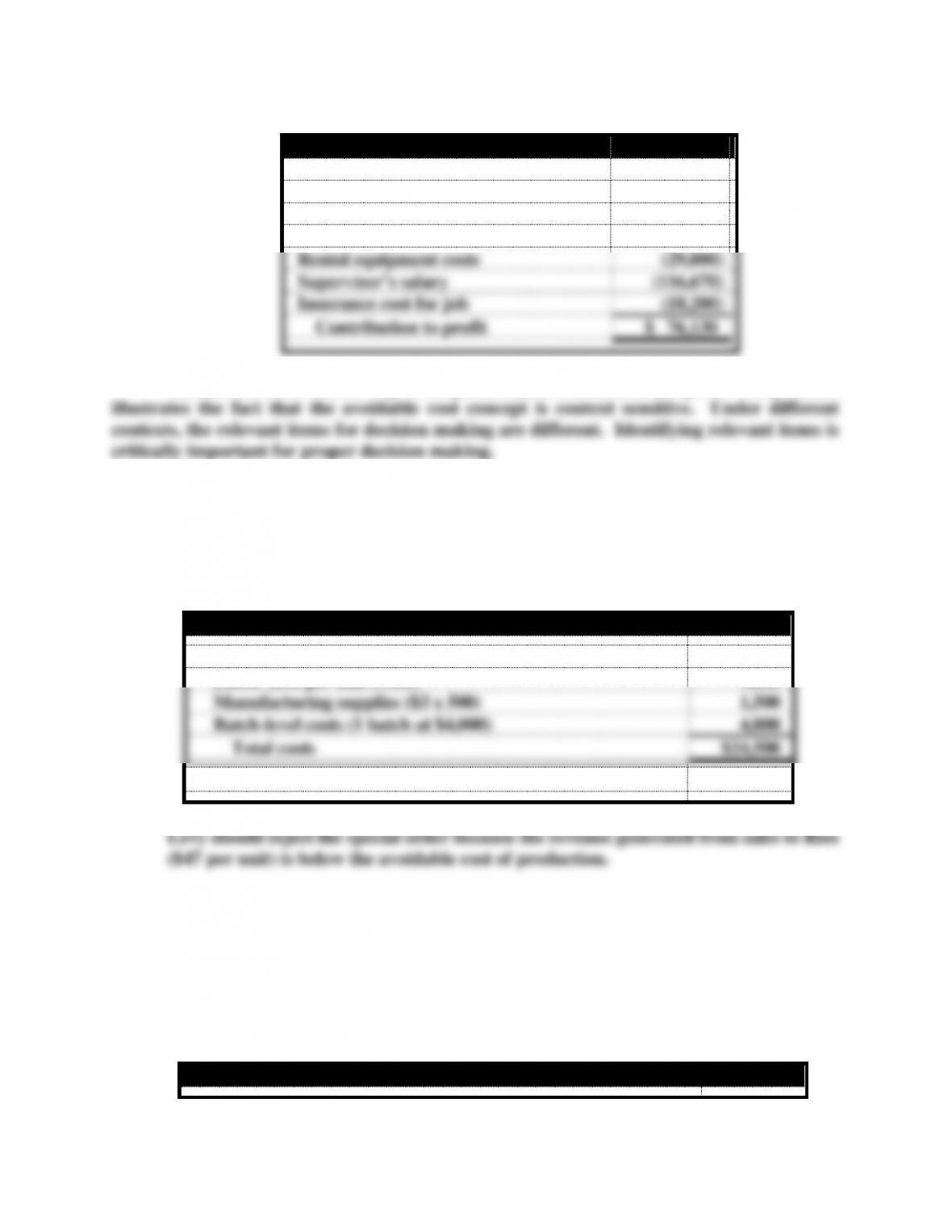

b. With respect to a decision regarding the acceptance or rejection of Job B standing

alone, changing the decision context changes the items that are considered relevant.

Problem 13-23 (continued)

Decision:

Job B

Contract price

$ 800,000

Unit-level materials

(220,000)

Unit-level labor

(310,000)

Unit-level overhead

(30,000)

Rental equipment costs

(29,000)

Supervisor’s salary

(116,670)

Insurance cost for job

(18,200)

Contribution to profit

$ 76,130

Because the contribution to profit is positive, Job B should be accepted. This problem

Problem 13-24

a. The product-level and facility-level costs are not avoidable because they will be

incurred regardless of whether the special order is accepted. The relevant (avoidable)

costs for 500 blankets are:

Production Cost for 500 Blankets

Materials ($20 per unit x 500)

$10,000

Labor ($18 per unit x 500)

9,000

Manufacturing supplies ($3 x 500)

1,500

Batch-level costs (1 batch at $4,000)

4,000

Total costs

$24,500

Cost per unit = $24,500 ÷ 500 = $49

Problem 13-24 (continued)

b. Since the batch-level costs are fixed relative to the number of units within the relevant

range of 1 to 1,000 units, the avoidable cost per unit will decrease when the number

of units increases from 500 to 1,000. The supporting computations are shown below:

Production Cost for 1,000 Blankets

Materials ($20 per unit x 1,000)

$20,000

Labor ($18 per unit x 1,000)

18,000

Manufacturing supplies ($3 x 1,000)

3,000

Batch-level costs (1 batch at $4,000)

4,000

Total costs

$45,000

Cost per unit = $45,000 ÷ 1,000 = $45

Now the avoidable cost per unit is below the revenue per unit ($47) that will be

c. Levy must exercise caution to avoid alienating its existing customer base. The fact

that a motel operator is outside Levy’s normal marketing channels is a good sign that

existing customers will not be affected. However, if the blankets are marked with an

Levy label, some association between the two markets may emerge. The association

could be positive. A customer may like the hotel blanket and want one for herself. In

Problem 13-25

a. The unit-level costs of production can be avoided if the skin cream is purchased. Also,

it is reasonable to assume that the cost of the production supervisor’s salary can be

avoided if the production process is eliminated. Since Koch will continue to market

Avoidable Production Costs for Koch Skin Cream

Unit-level materials costs (15,000 units x $2.00)

$ 30,000

Unit-level labor costs (15,000 units x $1.50)

22,500

Unit-level overhead costs (15,000 units x $0.50)

7,500

Skin cream production supervisor’s salary

60,000

Total avoidable costs

$120,000

b. The avoidable cost of making the skin cream is $8 per unit ($120,000 ÷ 15,000 units).

c. The cost of the supervisor’s salary is fixed relative to the number of units of skin

Supporting computations are shown below:

Avoidable Costs of Production

Unit-level materials costs (25,000 units x $2.00)

$ 50,000

Unit-level labor costs (25,000 units x $1.50)

37,500

Unit-level overhead costs (25,000 units x $0.50)

12,500

Skin cream production supervisor’s salary

60,000

Total avoidable costs

$160,000

Problem 13-25 (continued)

At this level of production the avoidable cost per unit is less to make ($6.40) than to

growth as well as current production.

d. Before committing to the outsourcing decision, Koch must consider the ability of the

supplier to provide the cream in accordance with the company’s quality standards.

Also, Koch must assure itself that the product will be delivered on a timely basis. By

Problem 13-26

a. The facility-sustaining costs and 20 percent of the inventory holding costs stay the

same regardless of whether frames are purchased or made. Since these costs do not

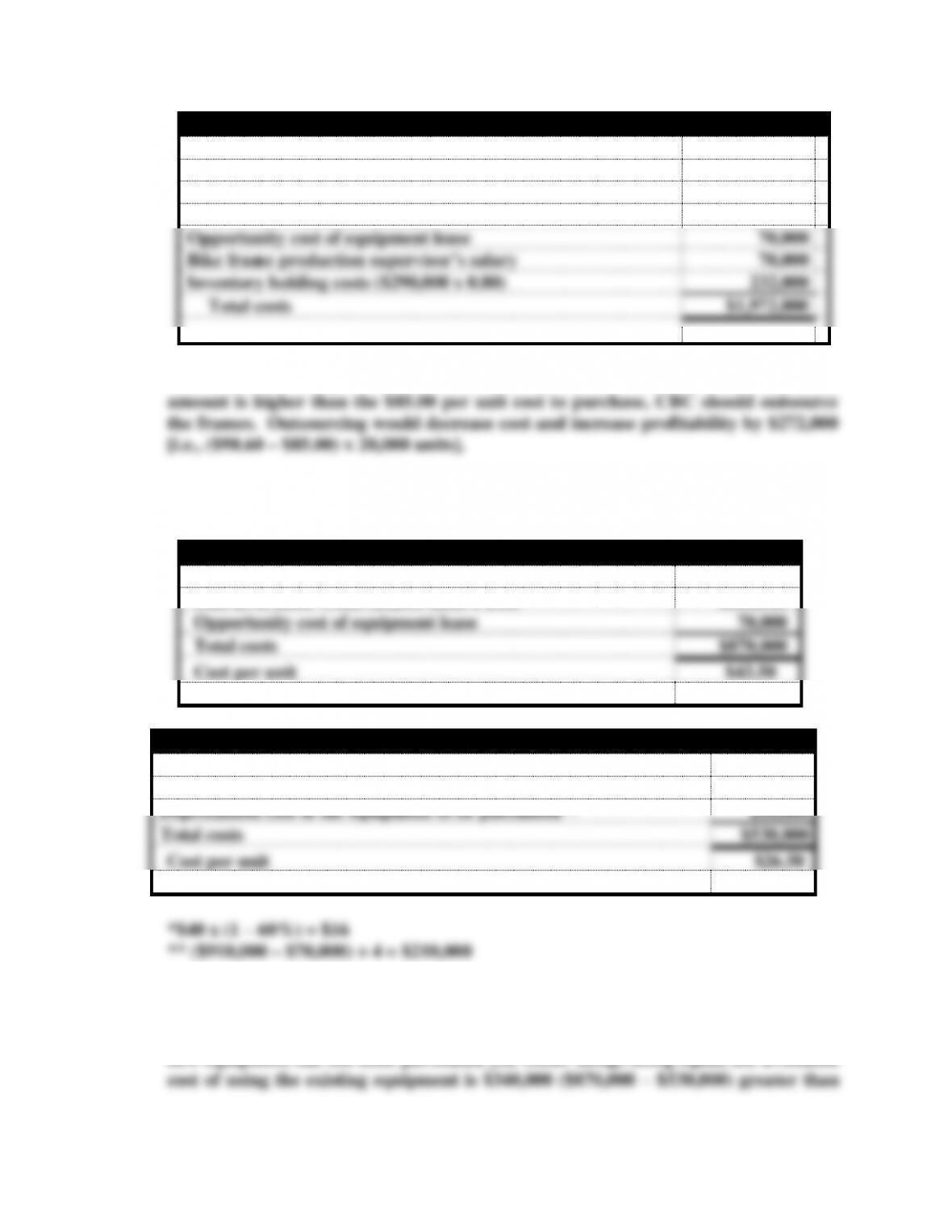

below:Problem 13-26 (continued)

Annual Avoidable Manufacturing Costs for Bicycle Frames

Unit-level materials costs (20,000 units x $30)

$ 600,000

Unit-level labor costs (20,000 units x $40)

800,000

Unit-level overhead costs (20,000 x $10)

200,000

Opportunity cost of equipment lease

70,000

Bike frame production supervisor’s salary

70,000

Inventory holding costs ($290,000 x 0.80)

232,000

Total costs

$1,972,000

The avoidable cost per unit is $98.60 (i.e., $1,972,000 ÷ 20,000 units). Since this

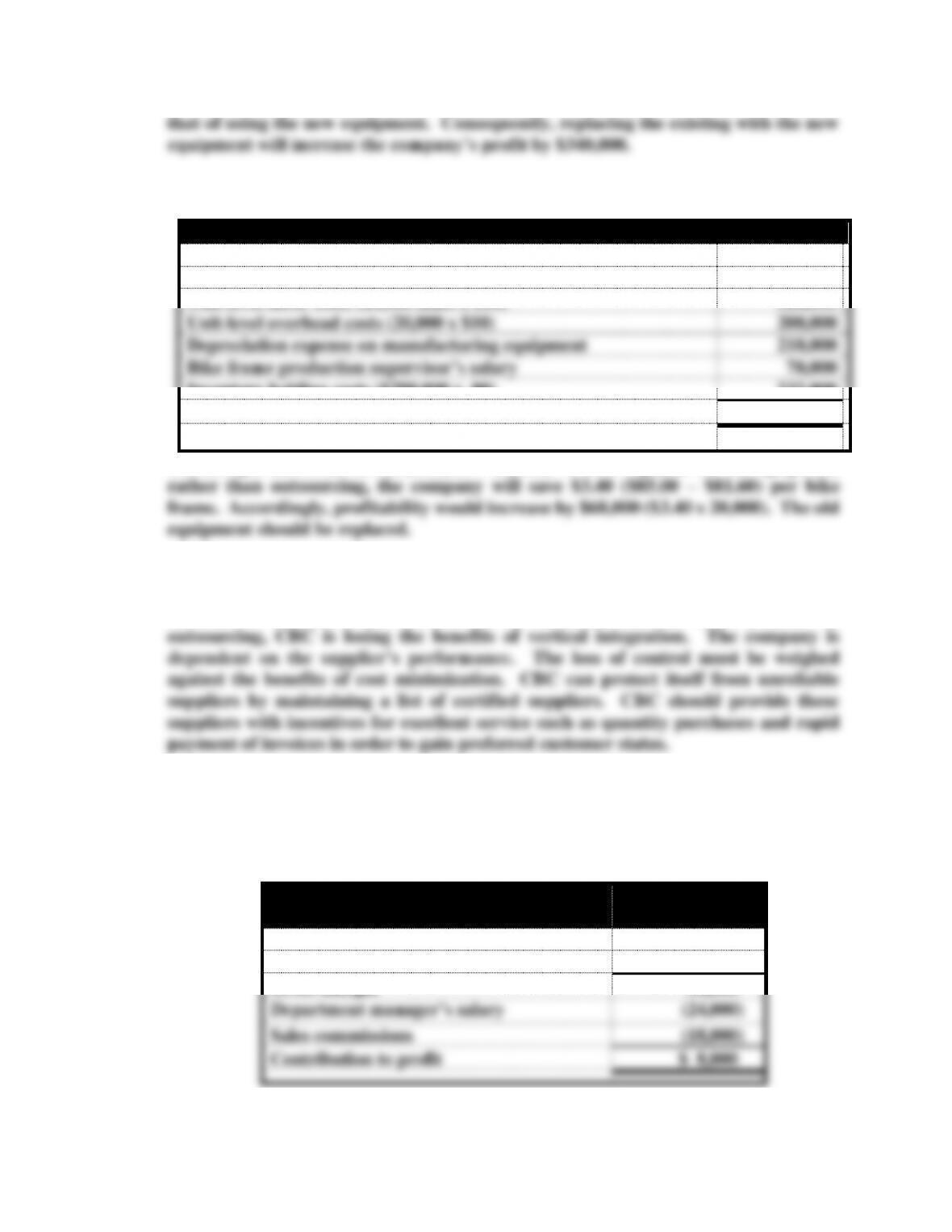

b. The avoidable costs of the two alternatives follow:

Avoidable Manufacturing Costs with the Existing Equipment

Unit-level labor Costs (20,000 units x $40)

$800,000

Opportunity cost of equipment lease

70,000

Total costs

$870,000

Cost per unit

$43.50

Avoidable Manufacturing Costs with the New Equipment

Unit-level labor costs (20,000 units x $16*)

$320,000

Depreciation cost of the equipment to be purchased**

210,000

Total costs

$530,000

Cost per unit

$26.50

Problem 13-26 (continued)

The depreciation cost of the new equipment is not a sunk cost in this case because the

new equipment has not been purchased yet. Other things being equal, the avoidable

c. If the old equipment will be replaced with the new equipment, the avoidable cost of

making the bike frames versus buying them would be as follows:

Avoidable Manufacturing Costs for Bicycle Frames

Unit-level materials costs (20,000 units x $30)

$ 600,000

Unit-level labor costs (20,000 units x $16)

320,000

Unit-level overhead costs (20,000 x $10)

200,000

Depreciation expense on manufacturing equipment

210,000

Bike frame production supervisor’s salary

70,000

Inventory holding costs ($290,000 x .80)

232,000

Total costs

$1,632,000

The cost per unit is $81.60 ($1,632,000 ÷ 20,000). If CBC replaces the old equipment

d. Before committing to the outsourcing decision, CBC must consider the ability of the

supplier to provide the frames in accordance with the company’s quality standards.

Also, CBC must assure itself that the frames will be delivered on a timely basis. By

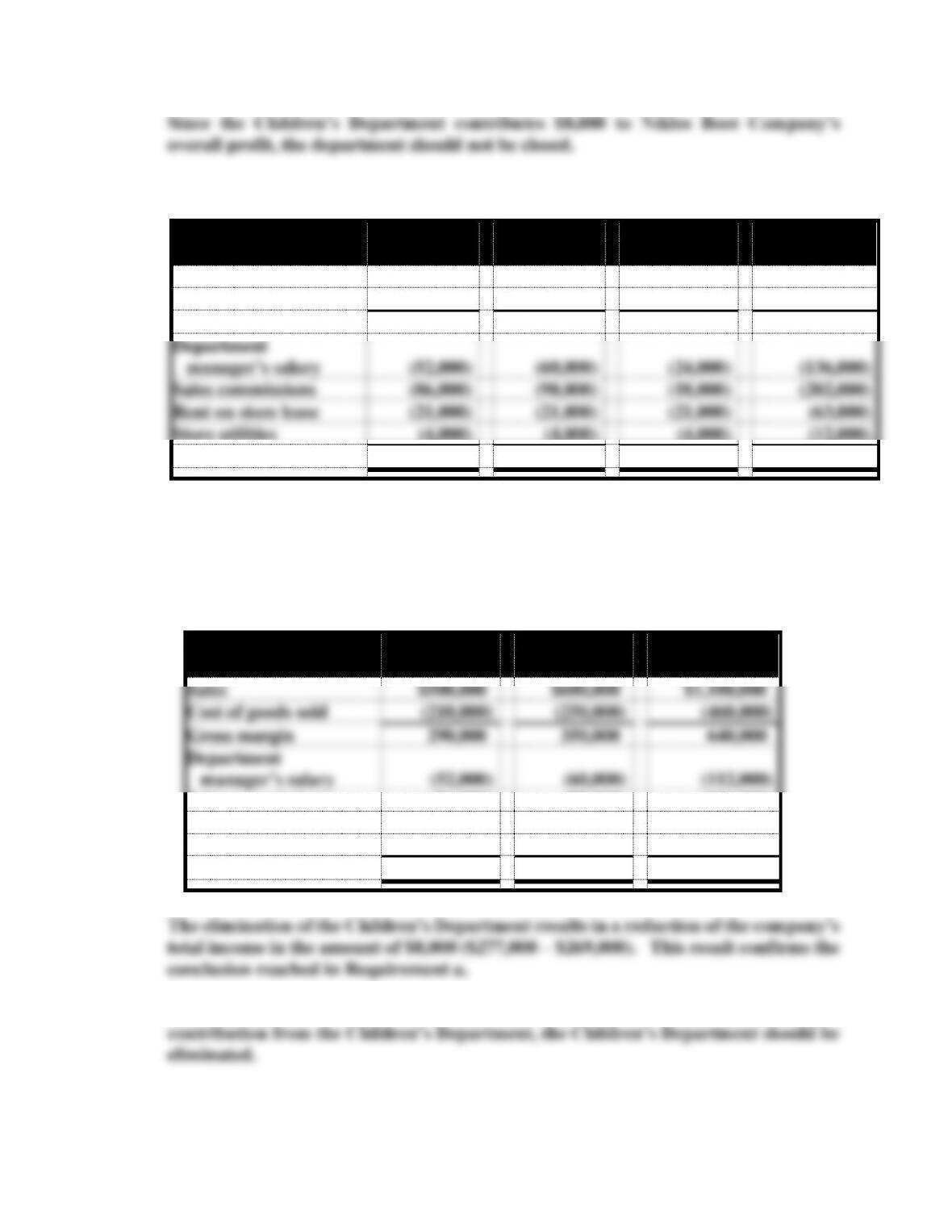

Problem 13-27

a.

Children’s

Department

Sales

$120,000

Cost of goods sold

(70,000)

Gross margin

50,000

Department manager’s salary

(24,000)

Sales commissions

(18,000)

Contribution to profit

$ 8,000

b. Income statements before the elimination of the Children’s Department

Men’s

Department

Women’s

Department

Children’s

Department

Company

Total

Sales

$500,000

$600,000

$120,000

$1,220,000

Cost of goods sold

(210,000)

(250,000)

(70,000)

(530,000)

Gross margin

290,000

350,000

50,000

690,000

Department

manager’s salary

(52,000)

(60,000)

(24,000)

(136,000)

Sales commissions

(86,000)

(98,000)

(18,000)

(202,000)

Rent on store lease

(21,000)

(21,000)

(21,000)

(63,000)

Store utilities

(4,000)

(4,000)

(4,000)

(12,000)

Net income (loss)

$127,000

$167,000

$ (17,000)

$ 277,000

Problem 13-27 (continued)

Income statements after the elimination of the Children’s Department

Men’s

Department

Women’s

Department

Company

Total

Sales

$500,000

$600,000

$1,100,000

Cost of goods sold

(210,000)

(250,000)

(460,000)

Gross margin

290,000

350,000

640,000

Department

manager’s salary

(52,000)

(60,000)

(112,000)

Sales commissions

(86,000)

(98,000)

(184,000)

Rent on store lease

(31,500)

(31,500)

(63,000)

Store utilities

(6,000)

(6,000)

(12,000)

Net income (loss)

$114,500

$154,500

$269,000

c. Since the additional income in the amount of $20,000 is greater than the $8,000 profit