Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 16 Planning for Capital Investments

16-1

must sit idle, then Alternative 2 may be the better option if Speedy Delivery actually has that

much money. The information provided is insufficient to determine which the better

alternative is.

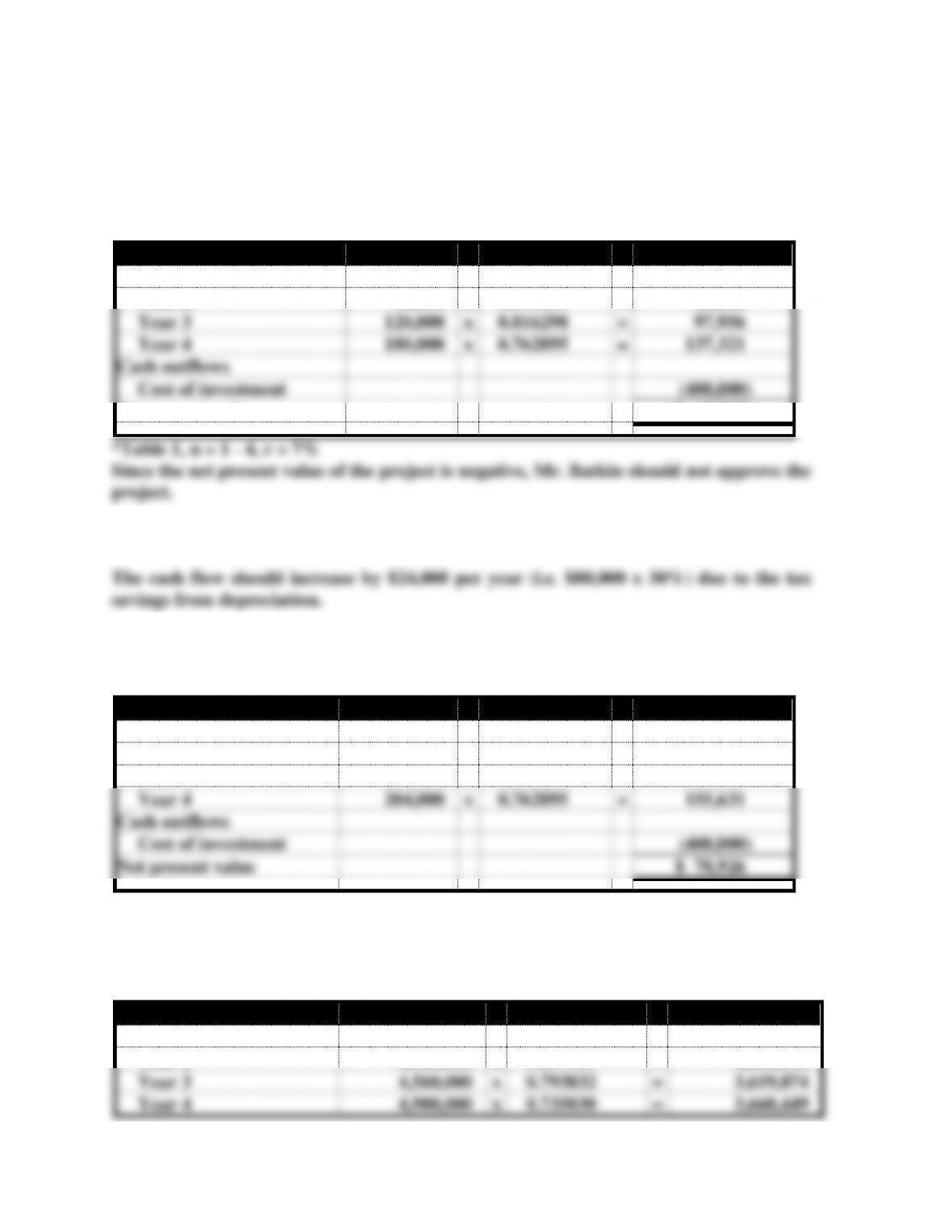

Problem 16-17

a.

Cash Inflows

Table Value*

Present Value

Year 1

$ 84,000

x

0.934579

=

$ 78,505

Year 2

96,000

x

0.873439

=

83,850

Year 3

120,000

x

0.816298

=

97,956

Year 4

180,000

x

0.762895

=

137,321

Cash outflows

Cost of investment

(400,000)

Net present value

$ (2,368)

b. & c.

The revised cash flow forecast and the net present value computation should be as

follows:

Cash Inflows

Table Value

Present Value

Year 1

$108,000

x

0.934579

=

$ 100,935

Year 2

120,000

x

0.873439

=

104,813

Year 3

144,000

x

0.816298

=

117,547

Year 4

204,000

x

0.762895

=

155,631

Cash outflows

Cost of investment

(400,000)

Net present value

$ 78,926

Since the net present value with the revised cash flow is positive, Mr. Batkin should

approve the project.

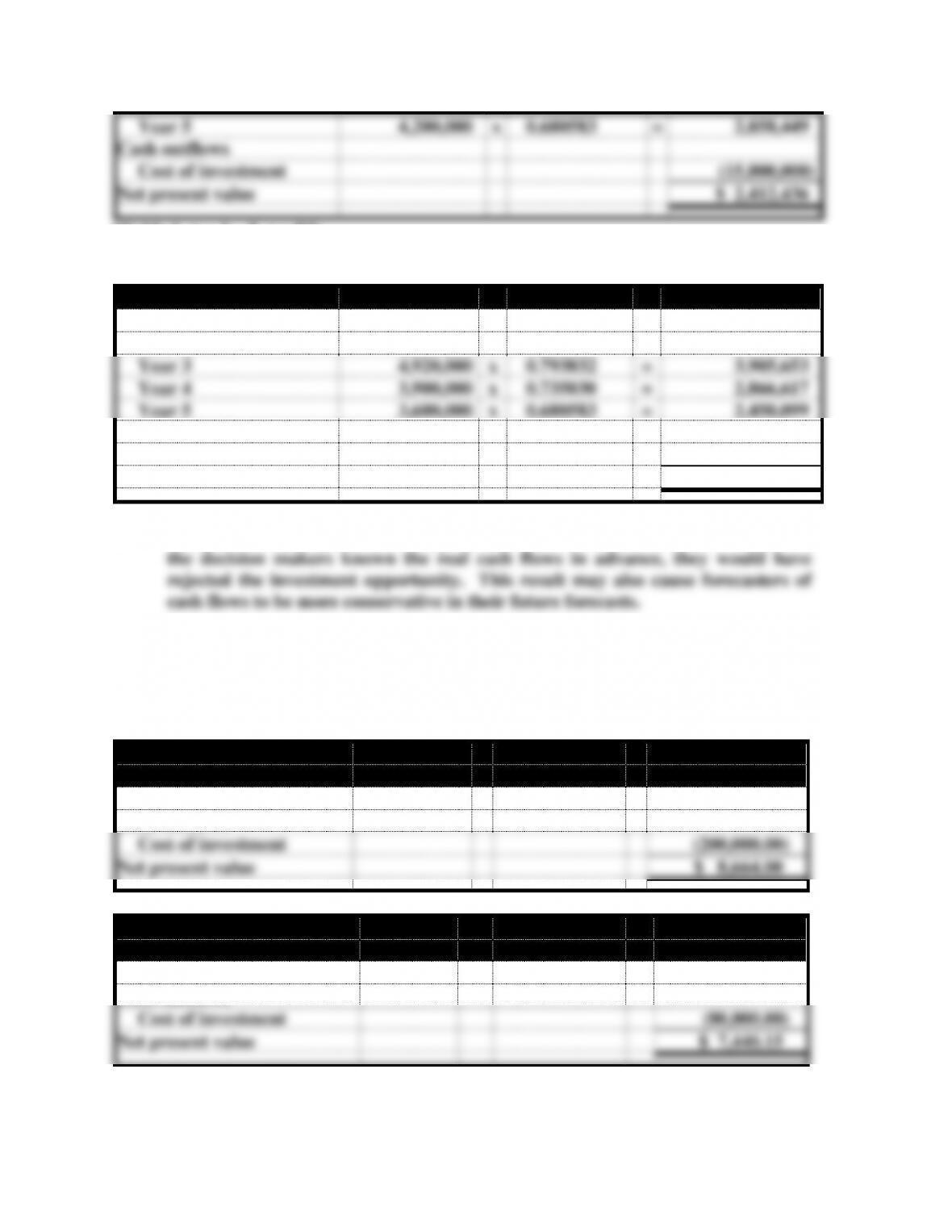

Problem 16-18

a.

Cash Inflows

Table Value*

Present Value

Year 1

$3,300,000

x

0.925926

=

$ 3,055,556

Year 2

4,920,000

x

0.857339

=

4,218,108

Year 3

4,560,000

x

0.793832

=

3,619,874

Year 4

4,980,000

x

0.735030

=

3,660,449

Chapter 16 Planning for Capital Investments

16-2

Year 5

4,200,000

x

0.680583

=

2,858,449

Cash outflows

Cost of investment

(15,000,000)

Net present value

$ 2,412,436

*Table 1, n = 1 – 5, r = 8%

b.

Cash Flows

Table Value

Present Value

Year 1

$2,700,000

x

0.925926

=

$ 2,500,000

Year 2

3,060,000

x

0.857339

=

2,623,457

Year 3

4,920,000

x

0.793832

=

3,905,653

Year 4

3,900,000

x

0.735030

=

2,866,617

Year 5

3,600,000

x

0.680583

=

2,450,099

Cash outflows

Cost of investment

(15,000,000)

Net present value

$ (654,174)

c. The postaudit reveals that the original cash flow estimates were inaccurate. Had

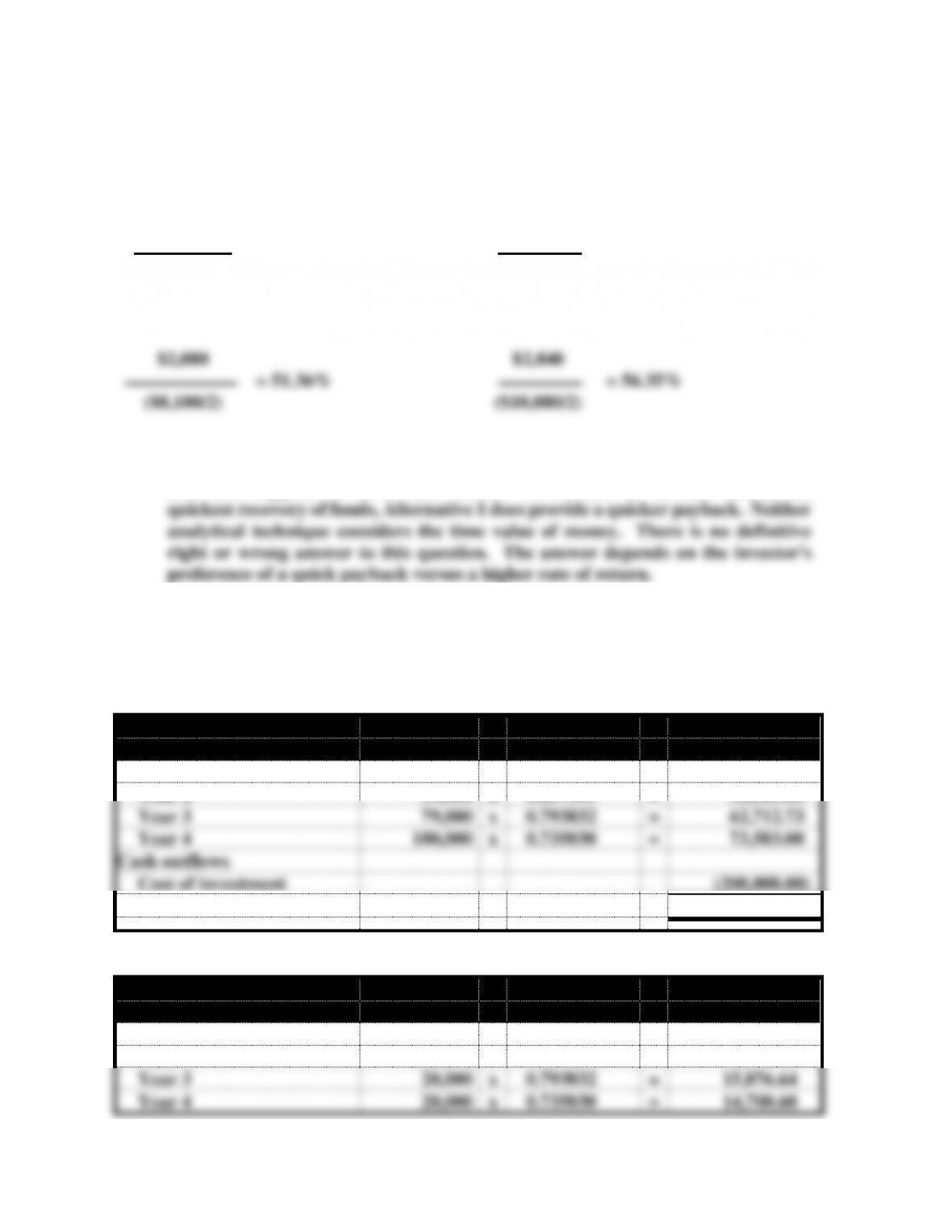

Problem 16-19

a.

Project A

Cash Inflows

Table Value

Present Value

Annual cash inflows

$63,000

x

3.312127*

=

$208,664.00

Cash outflows

Cost of investment

(200,000.00)

Net present value

$ 8,664.00

Project B

Cash Inflows

Table Value

Present Value

Annual cash inflows

$26,400

x

3.312127*

=

$87,440.15

Cash outflows

Cost of investment

(80,000.00)

Net present value

$ 7,440.15

*Table 2, n = 4, r = 8%

Chapter 16 Planning for Capital Investments

16-3

b.

Project A:

Present value table factor x $63,000 = $200,000

approximate internal rate of return.

Problem 16-19 (continued)

Project B:

Present value table factor x $26,400 = $80,000

Present value table factor = $80,000 $26,400

Present value table factor = 3.030303

c. Each method has its own strengths and weaknesses. Project A generates a greater

net present value, resulting from a greater initial investment. If the company has

remaining $120,000 for a similar rate of return, Project B would be preferable to

Project A.Problem 16-20

a.

Alternative 1

Alternative 2

Revenues

$6,200

$8,500

Operating expenses

(900)

(2,430)

Depreciation expense

(2,700)

(2,520)

Income before taxes

2,600

3,550

Tax expense @ 20%

(520)

(710)

Net income

2,080

2,840

Add back depreciation

2,700

2,520

Cash flow per year

$4,780

$5,360

Chapter 16 Planning for Capital Investments

16-4

Alternative 1

Alternative 2

Payback Period

Payback Period

$8,100

$10,080

= 1.69 years

= 1.88 years

$4,780

$5,360

Unadjusted rate of return:

Unadjusted rate of return:

$2,080

$2,840

= 51.36%

= 56.35%

($8,100/2)

($10,080/2)

b. Because of its longer useful life and its higher unadjusted rate of return, the second

alternative appears to be a better choice. However, if an investor desires the

Problem 16-21

a.

Opportunity 1

Cash Inflows

Table Value*

Present Value

Year 1

$55,000

x

0.925926

=

$ 50,925.93

Year 2

59,000

x

0.857339

=

50,583.00

Year 3

79,000

x

0.793832

=

62,712.73

Year 4

100,000

x

0.735030

=

73,503.00

Cash outflows

Cost of investment

(200,000.00)

Net present value

$ 37,724.66

*Table 1, n = 1– 4, r = 8%

Opportunity 2

Cash Inflows

Table Value*

Present Value

Year 1

$102,000

x

0.925926

=

$ 94,444.45

Year 2

108,000

x

0.857339

=

92,592.61

Year 3

20,000

x

0.793832

=

15,876.64

Year 4

20,000

x

0.735030

=

14,700.60

Chapter 16 Planning for Capital Investments

16-5

Cash outflows

Cost of investment

(200,000.00)

Net present value

$ 17,614.30

*Table 1, n = 1– 4, r = 8%

net present value method.

b. Payback:

The cash flows in this problem are not evenly distributed. Project 1 has major cash inflows

concentrated in the second half of the investment period. On the other hand, Project 2 has

Problem 16-21 (continued)

Project 1:

Average annual cash flow:

$55,000 + $59,000 + $79,000 = $193,000 < $200,000

Project 2:

The sum of cash inflows for year 1 and year 2 =

$102,000 + $108,000 = $210,000 > $200,000

c. The net present value represents the net cash profit with the consideration of the

time value of money for a particular investment opportunity. The payback period,

on the other hand, measures how fast the original investment can be recovered

Chapter 16 Planning for Capital Investments

16-6

If an investor is very concerned about the risk of an investment, he/she should

probably use the payback method as the primary decision tool and the net present

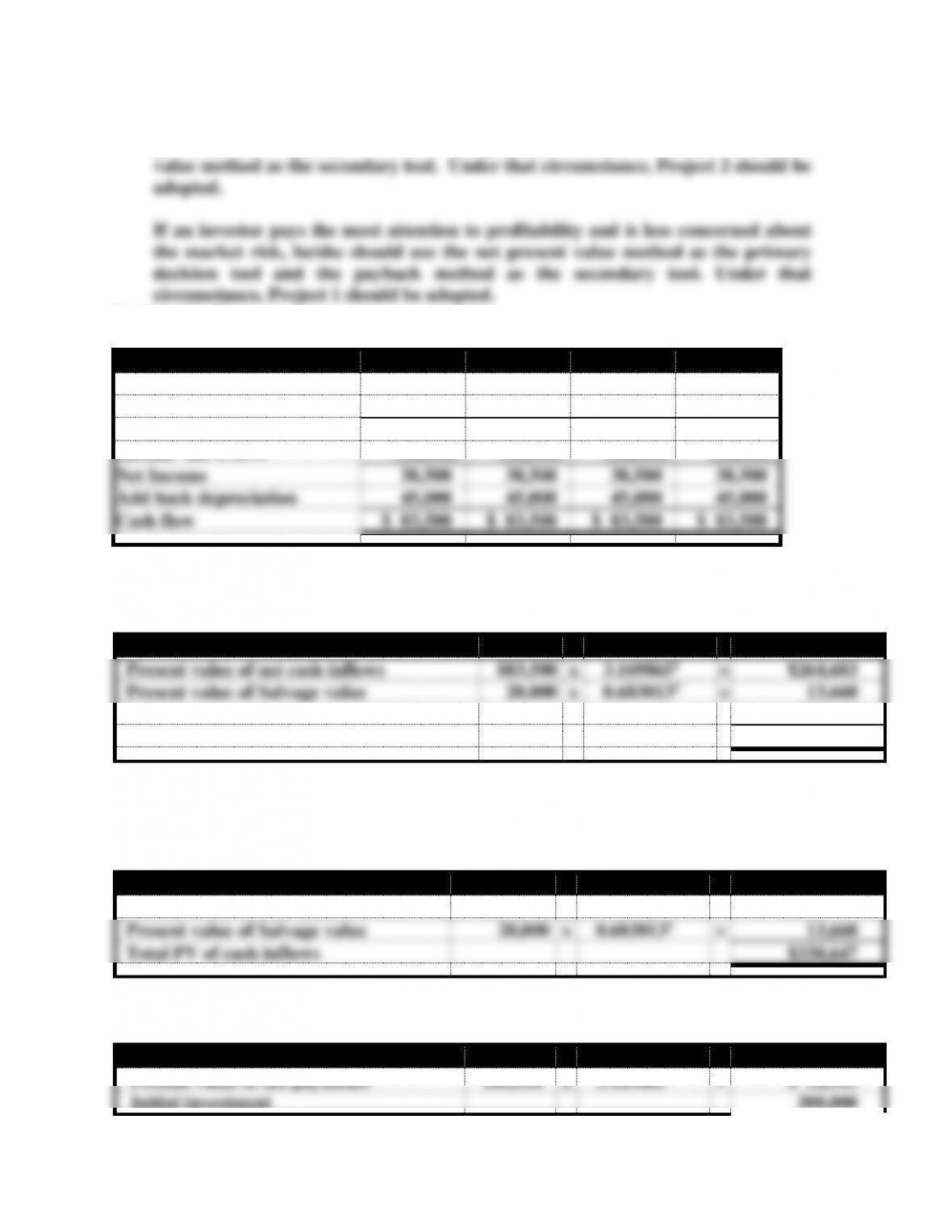

Problem 16-22

a.

Year

1

2

3

4

Revenue

$100,000

$100,000

$100,000

$100,000

Depreciation

(45,000)

(45,000)

(45,000)

(45,000)

Income before tax

55,000

55,000

55,000

55,000

Income tax @30%

(16,500)

(16,500)

(16,500)

(16,500)

Net Income

38,500

38,500

38,500

38,500

Add back depreciation

45,000

45,000

45,000

45,000

Cash flow

$ 83,500

$ 83,500

$ 83,500

$ 83,500

1Table 2, n=4, r=10%

2Table 1, n=4, r=10%

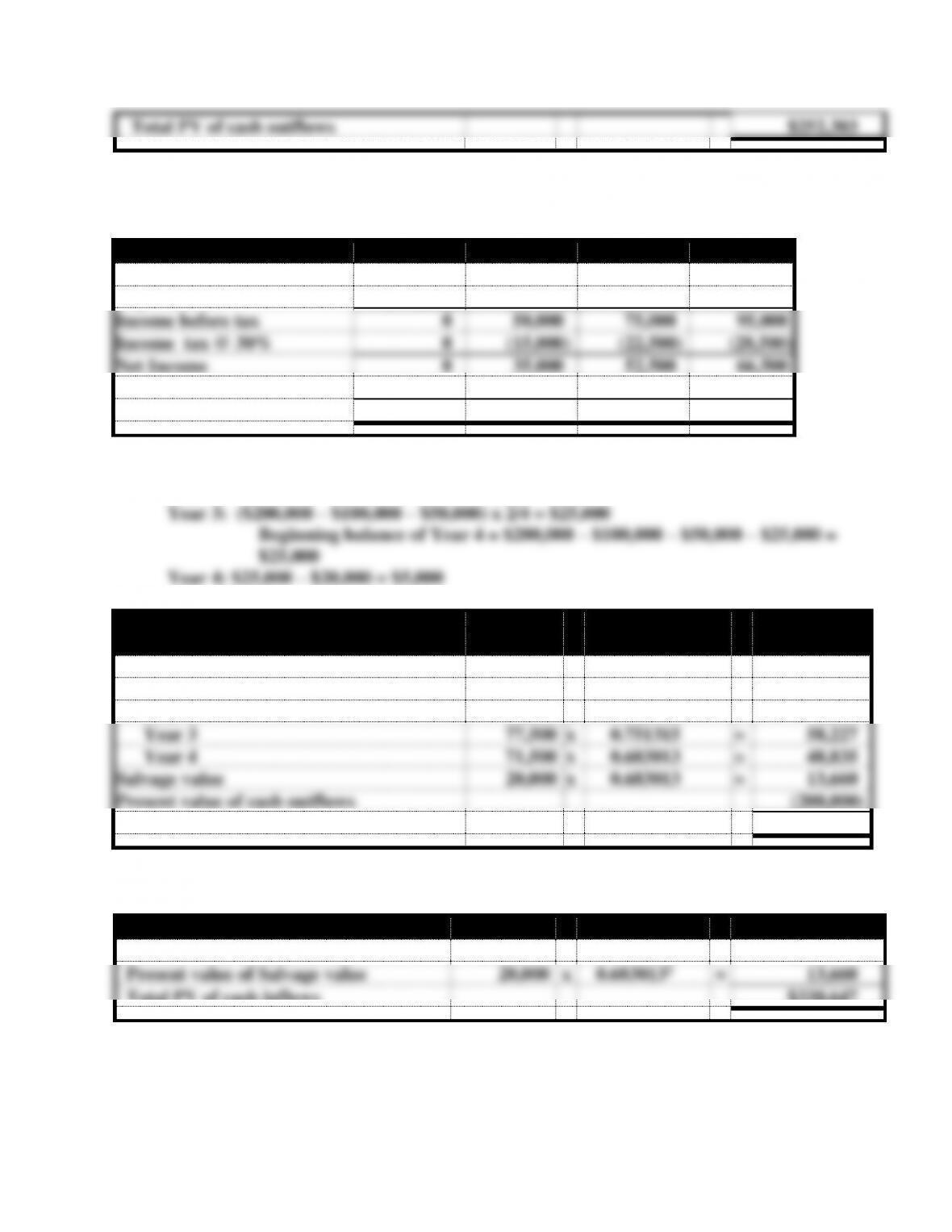

Net Present Value

Table Value

Present Value

Present value of net cash inflows

$83,500

x

3.1698651

=

$264,683

Present value of Salvage value

20,000

x

0.6830132

=

13,660

Initial investment

(200,000)

Net present value

$ 78,343

1Table 2, n=4, r=10%

2Table 1, n=4, r=10%

Present value index computation:

Present Value of Cash Inflows

Table Value

Present Value

Present value of cash inflows

$100,000

x

3.1698651

=

$316,987

Present value of Salvage value

20,000

x

0.6830132

=

13,660

Total PV of cash inflows

$330,647

1Table 2, n=4, r=10%

2Table 1, n=4, r=10%

Present Value of Cash Outflows

Table Value

Present Value

Present value of tax payments

$16,500

x

3.1698651

=

$ 52,303

Initial investment

200,000

Chapter 16 Planning for Capital Investments

16-7

Total PV of cash outflows

$252,303

1Table 2, n=4, r=10%

Present value index

$330,647

/

$252,303

=

1.31

Problem 16-22 (continued)

b.

Year

1

2

3

4

Revenue

$100,000

$100,000

$100,000

$100,000

Depreciation*

(100,000)

(50,000)

(25,000)

(5,000)

Income before tax

0

50,000

75,000

95,000

Income tax @ 30%

0

(15,000)

(22,500)

(28,500)

Net Income

0

35,000

52,500

66,500

Add back depreciation

100,000

50,000

25,000

5,000

Cash flow

$100,000

$ 85,000

$ 77,500

$ 71,500

*Double-declining-balance depreciation:

Year 1: $200,000 x 2/4 = $100,000

Year 2: ($200,000 – $100,000) x 2/4 = $50,000

Net Present Value

Table Value*

Present Value

Present value of net cash inflows

Year 1

$100,000

x

0.909091

=

$ 90,909

Year 2

85,000

x

0.826446

=

70,248

Year 3

77,500

x

0.751315

=

58,227

Year 4

71,500

x

0.683013

=

48,835

Salvage value

20,000

x

0.683013

=

13,660

Present value of cash outflows

(200,000)

Net present value

$ 81,879

*Table 1, n= 1 – 4, r=10%

Present value index computation:

Present Value of Cash Inflows

Table Value

Present Value

Present value of cash inflows

$100,000

x

3.1698651

=

$316,987

Present value of Salvage value

20,000

x

0.6830132

=

13,660

Total PV of cash inflows

$330,647

1Table 2, n=4, r=10%

2Table 1, n=4, r=10%%

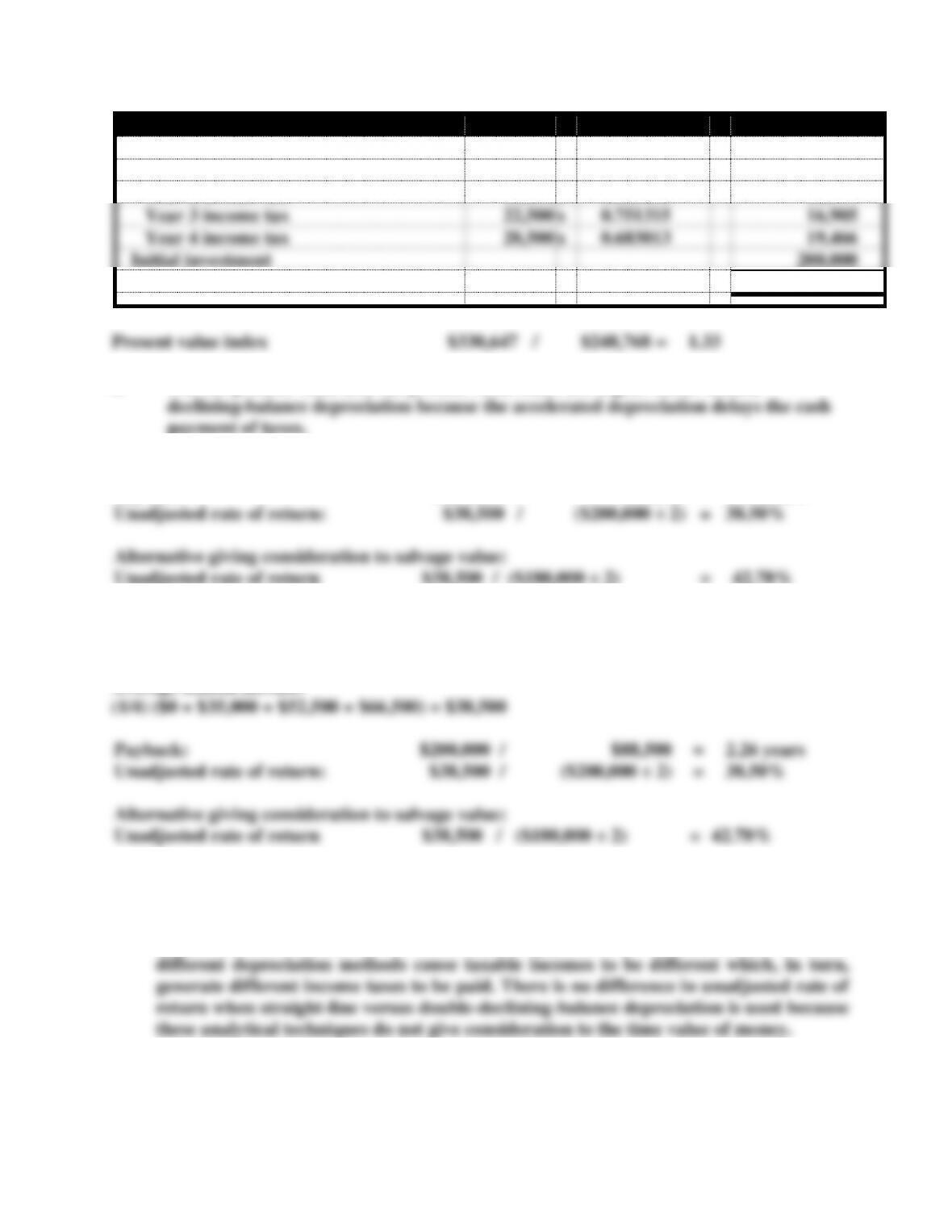

Problem 16-22 (continued)

Chapter 16 Planning for Capital Investments

Present Value of Cash Outflows

Table Value

Present Value

Present value of tax payments

Year 1 income tax

0

x

0.909091

$0

Year 2 income tax

15,000

x

0.826446

12,397

Year 3 income tax

22,500

x

0.751315

16,905

Year 4 income tax

28,500

x

0.683013

19,466

Initial investment

200,000

Total PV of cash outflows

$248,768

Present value index

$330,647

/

$248,768

=

1.33

c. The net present value and the present value index are higher under double-

payment of taxes.

d.

Payback:

$200,000

/

$83,500

=

2.40 years

Unadjusted rate of return:

$38,500

/

($200,000 ÷ 2)

=

38.50%

Alternative giving consideration to salvage value:

Unadjusted rate of return

$38,500

/

($180,000 ÷ 2)

=

42.78%

e.

Average annual cash flow under the double declining depreciation:

(1/4) ($100,000 + $85,000 + $77,500 + $91,500) =$88,500

Average annual income:

Payback:

$200,000

/

$88,500

=

2.26 years

Unadjusted rate of return:

$38,500

/

($200,000 ÷ 2)

=

38.50%

Alternative giving consideration to salvage value:

Unadjusted rate of return

$38,500

/

($180,000 ÷ 2)

=

42.78%

Problem 16-22 (continued)

(f) The difference in the payback period when straight-line versus double-declining-balance

depreciation are caused by the differences in payments for income taxes. The two

different depreciation methods cause taxable incomes to be different which, in turn,

generate different income taxes to be paid. There is no difference in unadjusted rate of

return when straight-line versus double-declining-balance depreciation is used because

these analytical techniques do not give consideration to the time value of money.

Problem 16-23

Chapter 16 Planning for Capital Investments

16-9

a. Unadjusted Rate of Return:

Average increase in net income Average net cost of original investment

$7,000 $50,000 = 14%

b. Internal Rate of Return:

Present value table factor x $27,700 = $100,000

Present value table factor = $100,000 $27,700

Present value table factor = 3.610108

c. The internal rate of return is the better method for this capital investment decision

ATC 16-1

a. Annual payment to retirees $ 3,300,000,000

x PV factor for 8%, 20 period annuity x 9.818147

= Gross pension liability $32,399,885,100

c. By assuming the investments in their pension plans will earn a higher, versus a lower,

rate of return, states’ pensions plans will report a smaller gross liability, and thus a lower

ATC 16-2

Computations rounded to nearest whole dollar:

Harding Properties