General Comments for Chapter 7

Accounting for Liabilities

Chapter 7 introduces the accounting for both current and long-term liabilities and the

preparation of a classified balance sheet. Throughout the chapter, the focus is on how liabilities

and interest expense affect the financial statements, rather than on specific procedural details.

The current liabilities covered in the chapter include notes payable, sales tax liabilities, warranty

liabilities, and contingent liabilities. Students will also explore longer-term debt financing:

installment notes, lines of credit, and bonds payable.

You should focus on how the recognition and payment of interest affects the income

statement and statement of cash flows differently. Use a note payable that is issued in one

accounting period and matures in the following period. Record the borrowing event, the accrual

of interest expense in the first period, the recognition of interest expense in the second period, the

cash payment of interest, and the repayment of principal in a statements model. Highlight the

differences between the amounts of expense recognized versus the amount of cash paid in the

two accounting periods.

The information on contingent liabilities provides an opportunity to discuss the broader topic

of expense recognition and matching of expenses to revenues. What should and should not be

shown in the financial statements? When should the expense for product warranties be reported

on the income statement?

This chapter covers accounting for long-term debt. It includes term notes and lines of credit

as well as bond liabilities. Coverage of bonds is limited to issuance of bonds at face value;

premium and discount on bonds are not mentioned in the text. In an ideal world we would have

time to pursue both conceptual understanding and procedural proficiency. Instructors, however,

do not teach in an ideal world. We are forced to make choices about how to allocate the scarce

resource known as class time.

Detailed Outline of a Lesson Plan for Chapter 7

I. Use Demonstration Problem 7-1 to introduce accrued interest payable. The following

description of the transactions includes explanatory comments (in italics) for the

instructor.

A. Events for 2014 are as follows:

1. Canton Company borrowed $10,000 cash from the National Bank on September

1, 2014. This problem focuses on borrowing money, using the borrowed money

to invest in land, and matching the rent revenue from the land with the interest

expense.

2. Canton invested the borrowed money in land.

3. Canton leased the land and earned rental revenue of $600 cash.

4. As of December 31, 2014, accrued interest payable (interest expense) on

Canton’s bank loan was $400. The amount of interest is provided. This

example focuses on how interest expense affects the financial statements.

Have students record the events under an accounting equation and prepare financial

statements for the accounting period ended December 31, 2014.

B. After preparing the 2014 statements, assume these 2015 events:

1. Canton earned rent revenue of $1,350 cash in 2015.

2. Canton sold its land for $10,000 cash.

3. Canton accrued interest of $800 on the bank loan. The accrual of interest and

the payment of interest are shown as separate transactions. While combining

transactions reduces recording time in a manual accounting system, doing so

masks the logic behind the steps.

4. Canton paid cash for the interest due on the bank loan.

5. Canton repaid the $10,000 bank loan (see Event 1 in Part A above) with cash.

II. Hand out Demonstration Problem 7-2. After you have shown students how accrued

interest affects the accounting equation and the financial statements in Demonstration

Problem 7-1, use Demonstration Problem 7-2 to show them how to compute accrued

interest.

Demonstration Problem 7-2: Accrued Interest Computations

Johnson Company borrowed $1,000 cash by issuing a one-year note to McCoy Company.

McCoy charged Johnson interest on the note at a 12 percent annual rate. Both companies

close their books on December 31, 2014. Determine the amount of accrued interest

expense Johnson would report and the amount of accrued interest revenue McCoy would

report at December 31, 2014, under each of the three following independent assumptions

of the note issue date. The note was issued (money was borrowed) on (1) April 1, 2014;

(2) June 1, 2014; and (3) October 1, 2014.

Solution:

Date Principal x Rate x Time = Accrued Interest

April 1, 2014 $1,000 x .12 x 9/12 = $90

June 1, 2014 $1,000 x .12 x 7/12 = $70

Oct. 1, 2014 $1,000 x .12 x 3/12 = $30

Point out that the interest expense on Johnson’s books equals the interest revenue on

McCoy’s books. Students should learn to handle both interest expense and interest

revenue.

III. Use an exercise in the text to demonstrate sales taxes. Exercise 7-3 serves as a good

demonstration problem. Exercise 7-4 works well as a reinforcement exercise for

homework.

IV. Use exercises in the text to demonstrate contingent liabilities and product

warranties. The topic of contingent liabilities can serve as a forum for a broader

discussion of expense recognition. Exercise 7-5 provides a good basis for discussion.

The text discusses warranty obligations. Exercises 7-6 and 7-7 provide comprehensive

problems dealing with warranties. They serve as excellent demonstration problems for a

brief lecture on how to report warranty obligations.

V. Demonstration Problem 7-3 illustrates accounting for a term loan repaid with equal

annual payments of principal and interest. Work this problem in class. Use the work

papers to save time and focus attention on financial statement effects. (Refer to

Demonstration Problem 7-3 for data used to determine the following amounts.)

A. Get your students started by showing them how to construct the amortization table.

Record the 2014 entries in the table. Have the students complete the entries in the

amortization table for 2015 and 2016.

B. Walk your students through the 2014 statements line by line. Then have them

continue the problem as an in-class assignment while you circulate through the room

helping those with questions.

Year 2014

1. Revenue. The problem specifies the 2014 revenue as $7,000.

2. Expense. Compute the 2014 interest expense: multiply the principal balance that

was outstanding during the year by the interest rate ($60,000 x .10). Have the

students record the interest expense in the income statement and determine the

amount of net income.

3. Cash. The December 31, 2014 cash balance is determined as follows: cash

increased $60,000 from issuing the note. Cash also increased by $7,000 from

receiving rent revenue. Cash decreased by the $24,127 payment on December 31

for interest and principal reduction. The ending cash balance is therefore $42,873

($60,000 + $7,000 − $24,127).

4. Note Payable. The amount of the note payable reported on the year-end balance

sheet is the beginning balance less the principal repayment portion of the annual

payment ($60,000 − $18,127 = $41,873) at December 31, 2014.

5. Retained Earnings. Because no dividends were paid, the total amount of net

income was retained in the business. Retained earnings are $1,000.

6. Cash Flow. Because revenue was collected in cash, the amount of cash received

from customers was $7,000. The $60,000 inflow from issuing the note is a

financing activity. Finally, cash decreased by $24,127 ($6,000 for interest and

$18,127 for principal) because of the December 31 payment of interest and

principal. The net result was a $42,873 ($60,000 + $7,000 − $24,127) cash

inflow.

Year 2015

Because the second year differs significantly from the first, you may want to walk

your students through it as well. Revenue is given as $7,000 and the amount of

interest expense is determined by multiplying the principal balance that was

outstanding during 2015 by the interest rate ($41,873 x .10 = $4,187). The cash

balance is determined by adding the cash revenue, $7,000, to the beginning balance of

$42,873, and subtracting the cash payment of $24,127 ($4,187 for interest and

$19,940 for principal repayment). The ending cash balance is $25,746. These

amounts are reported in the statement of cash flows. Because all earnings are retained

in the business, retained earnings amounts to last year’s ending balance plus the 2014

net income ($1,000 + $2,813 = $3,813).

Year 2016

Assign this year for students to complete in class. The one dollar negative

balance in the note payable account is due to rounding.

VI. Lines of credit. Businesses frequently use lines of credit to meet fluctuating borrowing

needs. One effective way to introduce the topic is by referring to lines of credit available

to consumers. For example, cash advances on credit cards represent a form of credit line

with which many students are familiar. Like consumer lines of credit, commercial lines

offer considerable flexibility by permitting borrowers to obtain and repay funds at will.

They are, therefore, a convenient source of short-term credit. Borrowers pay for this

convenience with relatively high interest rates that fluctuate with market conditions. You

can use Exercise 7-13 as a demonstration problem or a homework assignment.

VII. Demonstration Problem 7-4 illustrates accounting for a bond liability across five

consecutive accounting cycles. It is similar to the text illustration. A company issues

bonds to obtain money to purchase land which it leases to a customer. Because land does

not depreciate, the problem can focus on accounting for bond liabilities without the

distraction of other complexities. The problem requires students to prepare financial

statements.

The bonds are issued at face value and pay interest on December 31 of each year.

The accounting in these circumstances is essentially identical to that for notes

payable. The only difference is using the term bond instead of the term note. This is

a good time to explain that companies issue bonds because they can obtain more

attractive credit terms by issuing bonds to the general public than by issuing notes to

banks. In general, the term notes is used when companies borrow money from banks

or other companies; the term bonds is used when companies borrow money from the

general public.

To save time and focus attention on financial statement effects, we recommend

that you use the work papers for Demonstration Problem 7-4. Walk your students

through the first year statements line by line.

Year 2014

1. Revenue. The problem specifies the 2014 revenue as $7,000.

2. Expense. The amount of interest expense for the year is $6,000 ($50,000 x .12).

Have students fill in the amount of net income. Keep them actively involved.

3. Cash. The December 31, 2014 cash balance is determined as follows: cash

increased by $50,000 from issuing the bonds and decreased by $50,000 with the

land purchase. Cash also increased by $7,000 from receiving rent revenue. Cash

decreased by $6,000 with the December 31 interest payment. The ending cash

balance is $1,000.

4. Land. The cost of the land was $50,000. Have students fill in the amount of total

assets.

5. Bond Payable. The face value of the bond liability ($50,000) is reported on the

year-end balance sheet. Have students compute total liabilities. Since interest is

paid in cash on December 31 there is no accrued interest to report in the financial

statements.

6. Retained Earnings. Since no dividends were paid, the total amount of net

income was retained in the business. Retained earnings would be $1,000. Have

students compute total liabilities and equity.

7. Cash Flow. Since revenue was collected in cash, the operating activities section

of the statement of cash flows reports cash received from customers of $7,000.

The $6,000 outflow for interest expense is also reported in the operating activities

section. Under investing activities there is a $50,000 outflow for the purchase of

land. There’s a $50,000 inflow from the bond issue reported under financing

activities. The net result is a $1,000 increase in cash.

Year 2015

Because the second year differs somewhat from the first, you may want to walk

your students through it as well. The revenue and expenses are identical to those

reported in 2014. Cash again increases by $1,000 ($7,000 cash collected from

revenue less $6,000 paid on December 31 for interest). Therefore, the December 31,

2015 cash balance is $2,000 (the December 31, 2014 $1,000 cash balance plus the

$1,000 2015 increase). Since all income is retained in the business, retained earnings

amounts to the 2014 ending balance plus the 2015 net income ($1,000 + $1,000 =

$2,000). The only cash flows are those for the revenue collected and interest paid.

Years 2016 and 2017

Use these years as an in-class assignment for students to complete.

Year 2018

Students may need some help with this year. Revenue and expenses are the same

as in previous years. However, the land was sold and the bond liability repaid on

December 31, 2018. These events affect the balance sheet and the statement of cash

flows. The land and the bond liability will no longer appear on the balance sheet.

The operating activities section of the statement of cash flows will report the $7,000

inflow from customers and the $6,000 outflow for the payment of interest. The

investing activities section will report a $50,000 inflow from the sale of land. Also,

the financing activities section will report a $50,000 outflow for the repayment of the

bonds. The net change in cash is a $1,000 increase ($7,000 − $6,000 + $50,000 −

$50,000).

VIII. Time considerations and homework assignments. Completing Demonstration

Problems 7-1 and 7-2 should require approximately one hour of class time. Have the

students work along with you as you explain the problems. For example, in

Demonstration Problem 7-2, you can show the computations for the assumption that the

note was issued on April 1, and then have students calculate interest for the other two

issue dates. Exercises 7-1 and 7-2 are good to use as reinforcement for interest expense

recognition. Most students grasp sales tax and warranty obligations quickly. We find ten

to fifteen minutes per subject to be sufficient. Plan to spend less than one hour of class

time covering installment loans and lines of credit. Use Exercise 7-10 to reinforce

accounting for installment loans; Problem 7-33 pertains to lines of credit. Allow an

additional 30 to 45 minutes of class time to cover bond liabilities. Exercise 7-22 may be

used as homework or in-class practice in preparing a classified balance sheet. Because

both current and long-term liabilities are covered in this chapter, the chapter will require

more class time than most other chapters.

Demonstration Problems for Chapter 7

Demonstration Problem 7-1: Accrued Interest Payable

Part A

Canton Company experienced the following accounting events during 2014:

1. Canton Company borrowed $10,000 cash from the National Bank on September 1, 2014.

2. Canton invested the borrowed money in land.

3. Canton leased the land and earned rent revenue of $600 cash.

4. As of December 31, 2014, accrued interest (interest expense) on Canton’s bank loan was

$400.

Required

1. Record the events under an accounting equation.

2. Prepare an income statement, a statement of retained earnings, a balance sheet, and a

statement of cash flows for 2014.

Part B

Canton Company experienced the following accounting events during 2015:

1. Canton earned rent revenue of $1,350 cash in 2015.

2. Canton sold its land for $10,000 cash.

3. Canton accrued interest of $800 on the bank loan.

4. Canton paid cash for the interest due on the bank loan.

5. Canton repaid the $10,000 bank loan (See Event 1 in Part A above) with cash.

Required

1. Record the events under an accounting equation.

2. Prepare an income statement, a statement of retained earnings, a balance sheet, and a

statement of cash flows for 2015.

Demonstration Problem 7-2: Accrued Interest Computations

Johnson Company borrowed $1,000 cash by issuing a one-year note to McCoy Company. McCoy

charged Johnson interest on the note at a 12 percent annual rate. Both companies close their books

on December 31, 2014.

Required

Determine the amount of accrued interest expense Johnson would report and the amount of accrued

interest revenue McCoy would report at December 31, 2014, under each of the three following

independent assumptions of the note issue date. The note was issued (money was borrowed) on

(1) April 1, 2014; (2) June 1, 2014; and (3) October 1, 2014.Demonstration Problem 7-3:

Amortizing a Loan

King Company was started on January 1, 2014, when it issued a $60,000 face value term note to

State Bank. The note had a 10 percent annual interest rate and a three-year term to maturity.

Principal and interest were paid in three $24,127 payments on December 31 of 2014, 2015, and

2016. King Company earned cash revenue of $7,000 per year in 2014 through 2016 and interest

on the bank loan was the company’s only expense.

Required

a. Prepare an amortization schedule that allocates the year-end payments between interest and

principal for the three-year term of the loan.

b. Prepare income statements, balance sheets, and statements of cash flows for 2014, 2015, and

2016.

Demonstration Problem 7-4: Bond Issue

Land Development Company (LDC) was started in 2014 when it issued bonds with a face value

of $50,000. LDC purchased land with the cash proceeds from the bond issue. The land was

adjacent to one of Central Bank’s branches. Central Bank leased the land from LDC for the

construction of a parking lot.

Required

Prepare an income statement, a balance sheet, and a statement of cash flows assuming that:

1. The bonds were issued at face value on January 1, 2014. They had a five-year term and a 12

percent stated rate of interest. Interest was payable in cash annually on December 31 of each

year with the first payment due December 31, 2014.

2. LDC used the $50,000 cash proceeds to purchase the land.

3. Central Bank agreed to pay $7,000 cash per year for five years to lease the land.

4. On December 31, 2018, LDC sold the land for $50,000 cash and paid the principal due on the

bond liability.

SOLUTIONS TO

DEMONSTRATION PROBLEMS

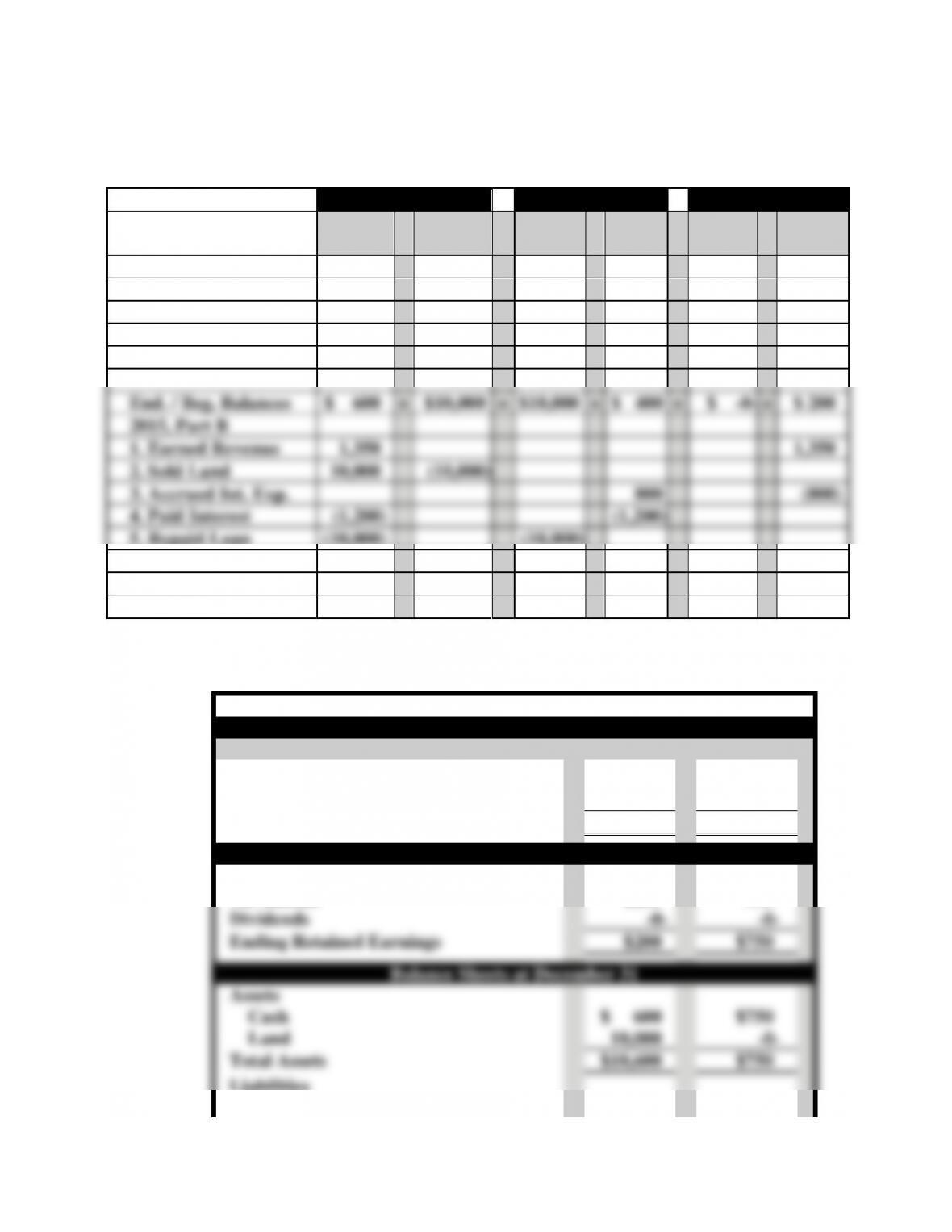

Demonstration Problem 7-1: Solution, Parts A & B,

Accounting Equation

Assets

=

Liab.

+

Equity

2014, Part A

Cash

+

Land

=

Notes

Payable

+

Int.

Pay.

+

Com.

Stock

+

Ret.

Ear.

Beginning Balances

$ -0-

$ -0-

$ -0-

$ -0-

$ -0-

$ -0-

1. Effect of Borrowing

10,000

10,000

2. Purchase of Land

(10,000)

10,000

3. Earned Revenue

600

600

4. Accrued Int. Exp.

400

(400)

−−−−−

−−−−

−−−−

−−−−

−−−−−

−−−−−

End. / Beg. Balances

$ 600

+

$10,000

=

$10,000

+

$ 400

+

$ -0-

+

$ 200

2015, Part B

1. Earned Revenue

1,350

1,350

2. Sold Land

10,000

(10,000)

3. Accrued Int. Exp.

800

(800)

4. Paid Interest

(1,200)

(1,200)

5. Repaid Loan

(10,000)

(10,000)

−−−−−

−−−−

−−−−

−−−−

−−−−−

−−−−−

Ending Balances

$ 750

+

$ -0-

=

$ -0-

+

$ -0-

+

$ -0-

+

$ 750

════

════

════

════

═════

═════

Demonstration Problem 7-1: Solution, Parts A & B,

Financial Statements

Canton Company

Income Statements

For the Years Ended December 31,

2014

2015

Rent Revenue

$600

$1,350

Interest Expense

(400)

(800)

Net Income

$200

$550

Statements of Retained Earnings

Beginning Retained Earnings

-0-

$200

Net Income

$200

550

Dividends

-0-

-0-

Ending Retained Earnings

$200

$750

Balance Sheets at December 31

Assets

Cash

$ 600

$750

Land

10,000

-0-

Total Assets

$10,600

$750

Liabilities

Interest Payable

$ 400

-0-

Note Payable

10,000

-0-

Equity

Retained Earnings

200

$750

Total Liabilities and Equity

$10,600

$750

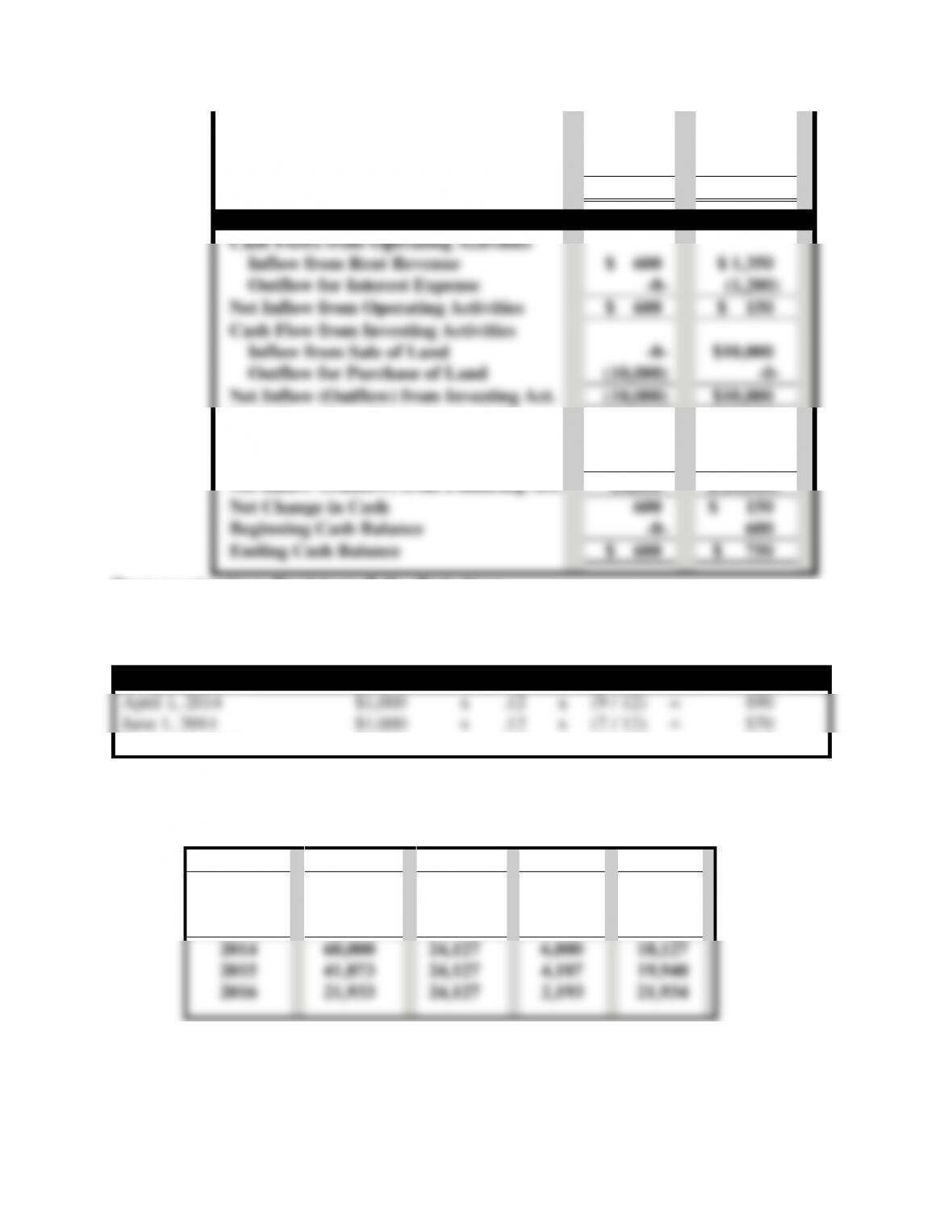

Statements of Cash Flows

Cash Flows from Operating Activities

Inflow from Rent Revenue

$ 600

$ 1,350

Outflow for Interest Expense

-0-

(1,200)

Net Inflow from Operating Activities

$ 600

$ 150

Cash Flow from Investing Activities

Inflow from Sale of Land

-0-

$10,000

Outflow for Purchase of Land

(10,000)

-0-

Net Inflow (Outflow) from Investing Act.

(10,000)

$10,000

Cash Flows from Financing Activities

Inflow from Issue of Note

10,000

-0-

Outflow for Repayment of Note

-0-

$(10,000)

Net Inflow (Outflow) from Financing Act.

10,000

$(10,000)

Net Change in Cash

600

$ 150

Beginning Cash Balance

-0-

600

Ending Cash Balance

$ 600

$ 750

Demonstration Problem 7-2: Solution

Johnson’s 2014 interest expense equals McCoy’s 2014 interest revenue, as follows:

Date Note Issued

Principal

x

Rate

x

Time

=

Accrued Interest

April 1, 2014

$1,000

x

.12

x

(9 / 12)

=

$90

June 1, 2014

$1,000

x

.12

x

(7 / 12)

=

$70

October 1, 2014

$1,000

x

.12

x

(3 / 12)

=

$30

Demonstration Problem 7-3: Solution, part a. Amortization Table

Column 1

Column 2

Column 3

Column 4

Column 5

Accounting

Period

Principal

Balance on

Jan. 1

Cash

Payment

Dec. 31

Applied

to

Interest

Applied

to

Principal

2014

60,000

24,127

6,000

18,127

2015

41,873

24,127

4,187

19,940

2016

21,933

24,127

2,193

21,934

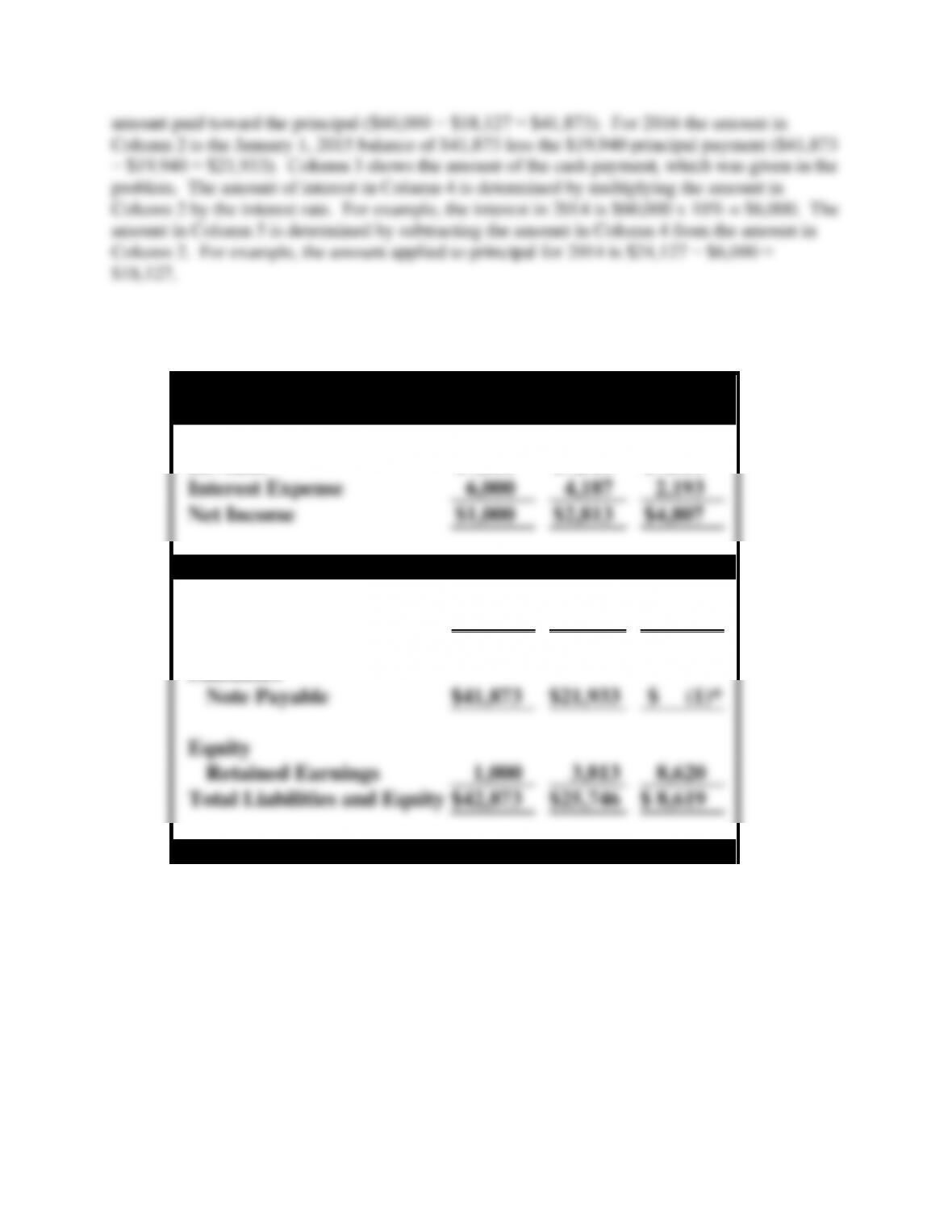

Computations: Column 2 shows the liability amount on January 1. For 2014, this amount was

$60,000. For 2015 the amount in Column 2 is the $60,000 beginning balance less the $18,127

Demonstration Problem 7-3: Solution, part b. Financial Statements

Financial Statements

Income Statements

2014

2015

2016

Revenue

$7,000

$7,000

$7,000

Interest Expense

6,000

4,187

2,193

Net Income

$1,000

$2,813

$4,807

Balance Sheets

Assets

Cash

$42,873

$25,746

$ 8,619

Liabilities

Note Payable

$41,873

$21,933

$ (1)*

Equity

Retained Earnings

1,000

3,813

8,620

Total Liabilities and Equity

$42,873

$25,746

$ 8,619

Statements of Cash Flows