Chapter 16 Planning for Capital Investments

16-1

Answers to Questions

1. A capital investment is an investment in a long-term operational asset. Stocks and

bonds are not operational assets but rather intangible legal agreements of

ownership in another company or loans to another company. They are bought and

sold in organized free markets, such as the New York Stock Exchange where there

revenues, or cost savings, generated by the asset.

2. This concept applies for the following reasons: 1) the smaller present amount can

be invested to earn interest that increases its future worth, 2) there is risk associated

3. Yes, both statements mean that a dollar today has more value because it can be

invested to earn interest, it has less risk associated with its receipt, and there is less

risk of its decrease in buying power due to inflation. In the first statement, you

4. When a company invests in capital assets, it is giving

up present dollars in exchange for future dollars. Since present dollars have more value,

the company must be compensated for the exchange. This compensation is called the

you received a 10% return ($500/$5,000).

5. In order to obtain assets (capital) to make investments, businesses must pay owners

dividends and lenders interest. The return paid to investors and creditors is the

cost of capital establishes the minimum acceptable rate of return on investments.

6. To determine the amount to invest today solve the following equation:

Investment x (0.10) + Investment = $500,000

Investment x (0.10 + 1) = $500,000

Chapter 16 Planning for Capital Investments

16-2

7. Many times converting future values into their present value equivalents requires a

considerable amount of mathematical manipulation, particularly if the future values

future values into present values.

8. An annuity is a series of equal cash flows paid over equal time intervals at a

9. Some programs offer an efficient means of converting future values into present

value equivalents. The conversion power of the present value function available

10. The mathematical formula based on the present value of an annuity table factor

would be written as:

Annual payment x PV of an annuity factor @ 14% for 5 years = PV

11. The bank’s investment balance is declining each year. A part of the original

investment is recovered with each payment made by Ms. Espinosa. Since the

interest Ms. Espinosa pays is based on the investment balance, the amount of

12. The higher net present value does not necessarily imply the better investment

opportunity. Other factors such as the amount of the initial outlay and the

Chapter 16 Planning for Capital Investments

16-3

13. Projects that produce zero or positive net present values satisfy the desired rate of

14. The net present value method does not provide a measure of the rate of return. It

simply indicates whether or not a project meets the desired rate of return criterion.

15. The investment with the highest internal rate of return is not always the best

investment even when risk is relatively equal. Firms have a limited supply of capital

16. Pursuing the highest rate of return does not guarantee the maximum profit for

companies. As long as an investment results in a return greater than the company’s

cost of capital, the investment will contribute additional profit to the company. If

17. The desired rate of return represents the level of return that management seeks to

attain on all investments. The internal rate of return is the actual return from a

18. Inflow items include incremental revenue, operating cost savings, salvage values,

19. The strategy is not sound because it does not take into account the limitations of the

20. The payback method can be used when cash flows are unequal. A cumulative

technique or an averaging technique can be employed.

21. The primary advantages of the unadjusted rate of return are simplicity and ease of

16-4

22. Capital investments involve major commitments of resources that are recovered

over extended future periods via increases in revenue or decreases in expenses.

23. A postaudit consists of using the same analytical techniques used for evaluating a

capital investment proposal in evaluating its success. A postaudit is conducted at

Exercise 16-1

Item

Type of Cash Flow

a. Initial investment

Outflow

b. Salvage value

Inflow

c. Recovery of working capital

Inflow

d. Incremental expenses

Outflow

e. Working capital commitments

Outflow

f. Cost savings

Inflow

g. Incremental revenue

Inflow

Exercise 16-2

a.

Present value

Present value

=

Future value

x

Table Factor*

Present value

=

$80,000

x

0.943396

Present value

=

$75,472

b.

Investment + (0.06 x Investment) = $80,000

Exercise 16-3

Chapter 16 Planning for Capital Investments

16-5

a.

Present value

Present value

=

Future value

x

Table Factor*

Present value

=

$600,000

x

0.680583

Present value

=

$408,350

*Table 1, n = 5, r = 8%

Ms. Long should not accept her employer’s offer of $360,000 because this amount is less

Exercise 16-4

a.

Present Value

Present Value

=

Future Value

x

Table Factor

=

Present Value

Present value

=

$20,000

x

0.925926(1)

=

$18,518.52

Present value

=

$20,000

x

0.857339(2)

=

17,146.78

Present value

=

$20,000

x

0.793832(3)

=

15,876.64

Total present value

$51,541.94

(1)Table 1, n = 1, r = 8%

b.

Present Value

Present Value

=

Future Value

x

Table Factor

=

Present Value

Present value

=

$20,000

x

2.577097(1)

=

$51,541.94

c. The present values are the same because the present value factor of Table 2 is

simply the sum of the three values from Table 1.

Exercise 16-5

a.

Chapter 16 Planning for Capital Investments

16-6

Present Value

Present Value

=

Future Value

x

Table Factor

=

Present Value

Present value

=

$28,000

x

3.387211*

=

$ 94,841.91

Present value

=

$42,000

x

0.762895**

=

32,041.59

Total present value

=

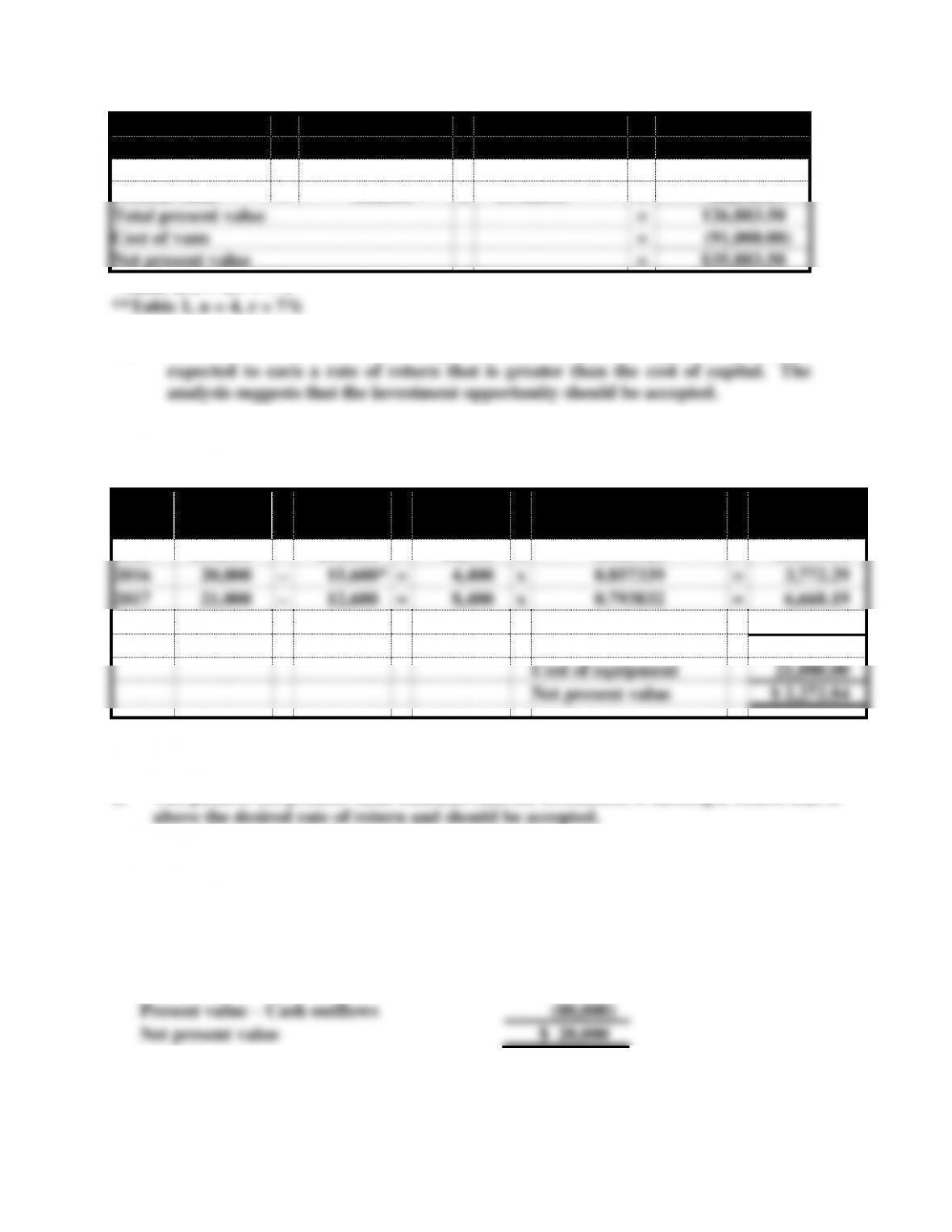

126,883.50

Cost of vans

=

(91,000.00)

Net present value

=

$35,883.50

*Table 2, n = 4, r = 7%

b. Since the net present value is positive, the investment opportunity can be

Exercise 16-6

a.

Year

Cash

Inflow

−

Cash

Outflow

=

Net Cash

Flows

x

Present Value

Table Factor

=

Present

Value

2015

$16,000

−

$10,000

=

$6,000

x

0.925926

=

$5,555.56

2016

20,000

−

15,600*

=

4,400

x

0.857339

=

3,772.29

2017

21,000

−

12,600

=

8,400

x

0.793832

=

6,668.19

2018

22,500**

−

12,600

=

9,900

x

0.735030

=

7,276.80

Present value

23,272.84

Cost of equipment

21,000.00

Net present value

$ 2,272.84

* $12,000 + $3,600

** $21,000 + $1,500

b. The positive net present value indicates that the investment is earning a return that is

Exercise 16-7

a.

Alternative 1

Present value – Cash inflows

$100,000

Present value – Cash outflows

(80,000)

Net present value

$ 20,000

Alternative 2

Present value – Cash inflows

$240,000

Chapter 16 Planning for Capital Investments

16-7

Present value – Cash outflows

(210,000)

Net present value

$ 30,000

Exercise 16-7 (continued)

b.

Present value

index

Present value of cash

inflows

$100,000

for

=

————————

=

————

=

1.25

Alternative 1

Present value of cash

outflows

$80,000

Present value

index

Present value of cash

inflows

$240,000

for

=

————————

=

————–

=

1.14

Alternative 2

Present value of cash

outflows

$210,000

Exercise 16-8

Revenues

$ 400,000

Operating expenses

(210,000)

Depreciation expense

(90,000)

($360,000 – $0) 4

Income before taxes

100,000

Tax expense

(30,000)

($100,000 x 0.30)

Net income

70,000

Add back depreciation

90,000

Net cash flows

$ 160,000

(For years 2 to 4)

Because the cash expenditure for equipment will be $360,000, the first year’s operations

Chapter 16 Planning for Capital Investments

16-8

Exercise 16-9

a.

Present value table factor x $1,280,000 = $7,865,045.76

Looking at table 2, at row 10, we find the factor 6.144567 under the rate of return column

marked 10%. Accordingly, 10% represents the internal rate of return.

Exercise 16-10

a. Determination of the annuity table values can be accomplished by dividing the

cost of the investment by the annuity:

First investment: $9,840.48 ÷ $2,400 = 4.1002. Locating this value in Table 2

b. Since the second investment has a higher internal rate of return it should be

accepted.

(1) The life of the investments. The second investment has a three-year useful life.

below the return generated by the first investment.

Exercise 16-10 (continued)

(2) The size of the investment. If the company has $9,840.48 (i.e., amount of the first

investment opportunity) of funds available to invest and only invests $6,442.74

Chapter 16 Planning for Capital Investments

16-9

(3) Confidence in the accuracy of projected cash flows. Uncertainty is just another

Exercise 16-11

Mr. Lyte does have a point. The company should evaluate the results of capital budget

decisions through the practice of conducting postaudits. A postaudit should be

conducted at the end of each capital investment project. The postaudit should repeat

the analytical technique that was used to justify the original investment. For example,

Exercise 16-12

a.

Cash cost of investment Annual cash inflow = Payback period

Alternative 1

$9,000,000 $3,000,000 = 3 years

Alternative 2

b. The payback method does not consider the life of the investment. In this case,

Exercise 16-13

a.

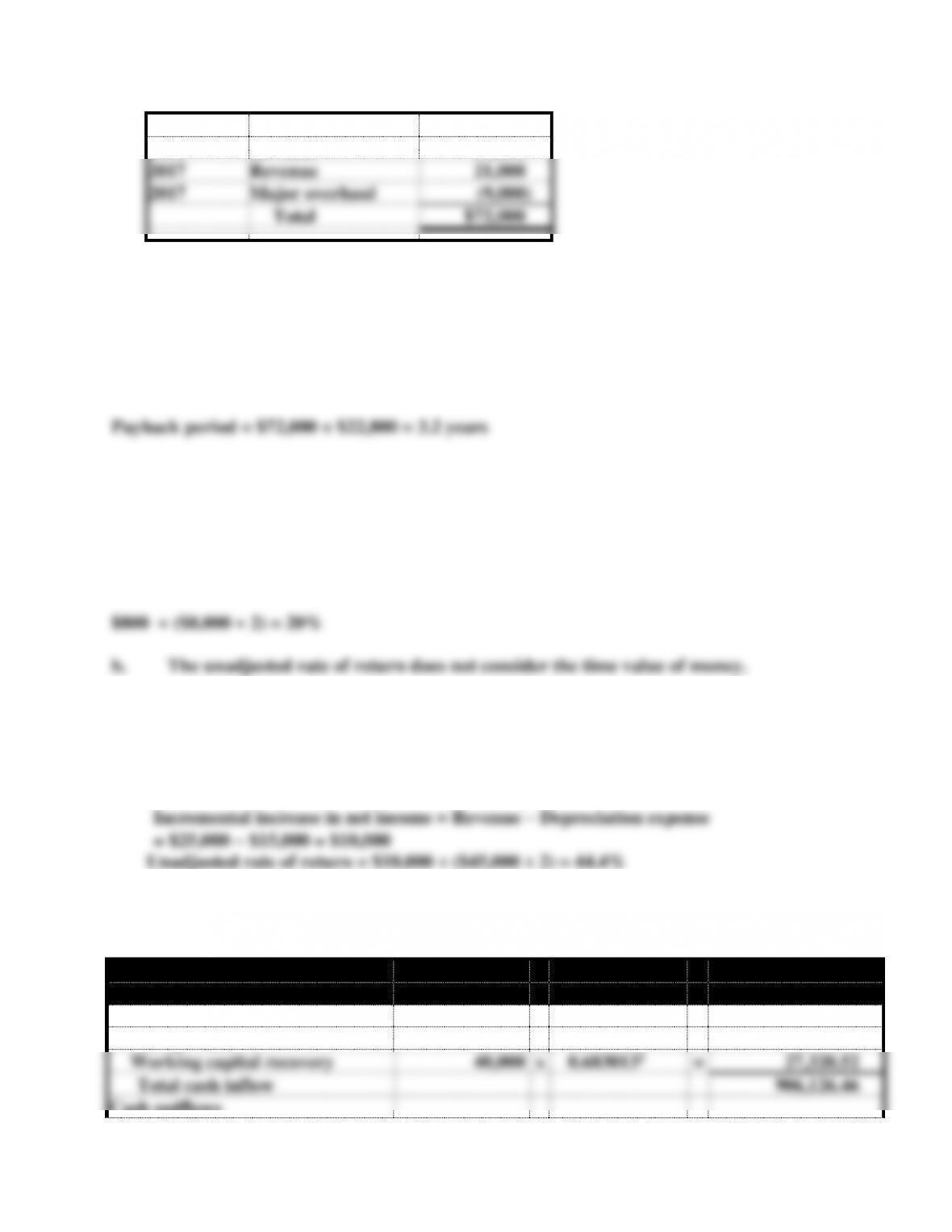

Year

Nature of Item

Cash Flows

Chapter 16 Planning for Capital Investments

16-10

2015

Revenue

$30,000

2016

Revenue

30,000

2017

Revenue

21,000

2017

Major overhaul

(9,000)

Total

$72,000

The payback occurs at the end of 3 years.

b. Average cash inflow is computed as follows:

($30,000 + $30,000 + $21,000 − $9,000 + $18,000 + $14,400 + $9,600) ÷ 5 = $22,800

average per year

Exercise 16-14

a.

Incremental increase in net income Average cost of original investment

Exercise 16-15

a. $45,000 ÷ $25,000 = 1.8 years

b. Depreciation expense = $45,000 ÷ 3 = $15,000 per year

Problem 16-16

a.

Alternative 1

Cash Inflows

Table Value

Present Value

Annual cash inflows

$260,000

x

3.1698651

=

$824,164.90

Salvage value

80,000

x

0.6830132

=

54,641.04

Working capital recovery

40,000

x

0.6830132

=

27,320.52

Total cash inflow

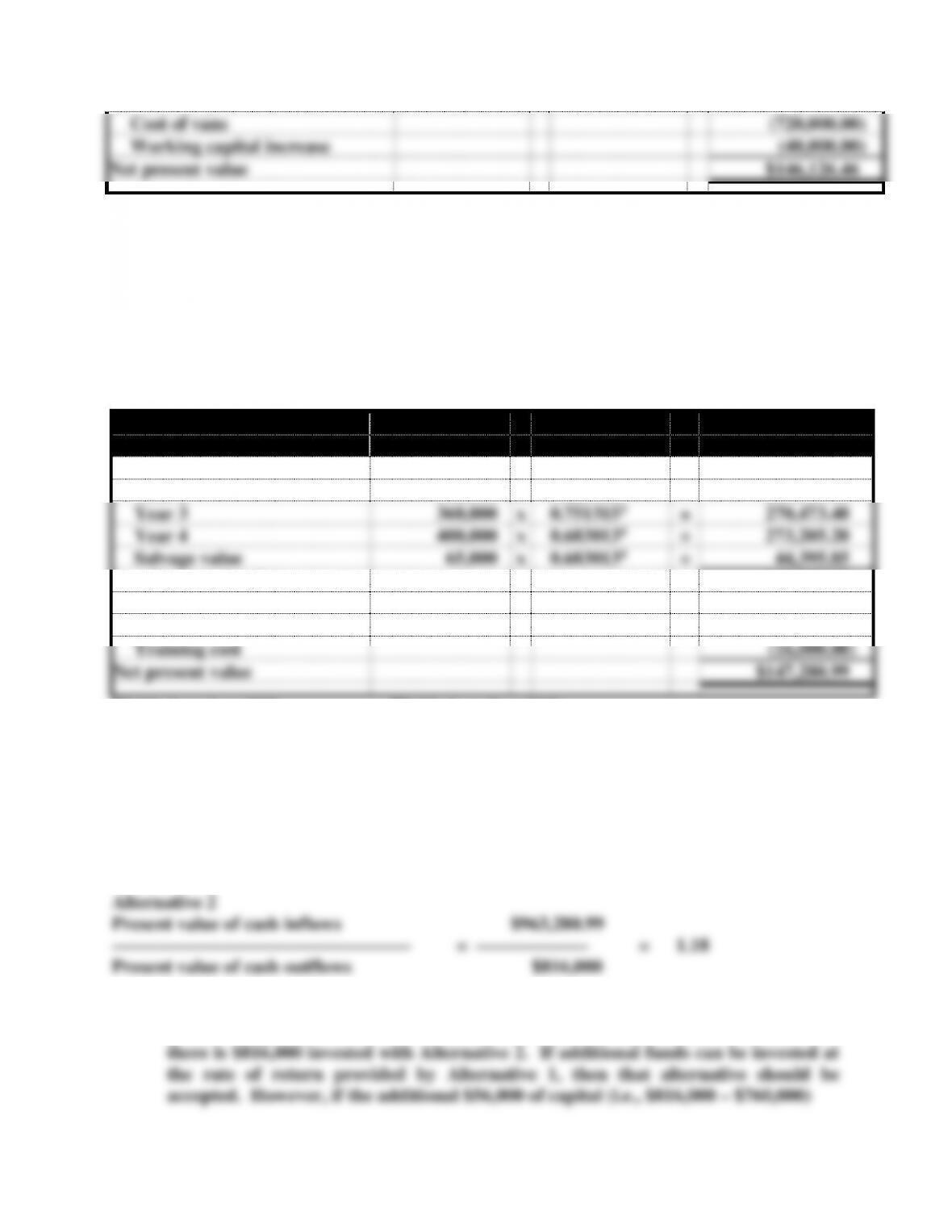

906,126.46

Cash outflows

Chapter 16 Planning for Capital Investments

16-11

Cost of vans

(720,000.00)

Working capital increase

(40,000.00)

Net present value

$146,126.46

1Table 2, n= 4, r = 10%

2Table 1, n= 4, r = 10%

Problem 16-16 (continued)

Alternative 2

Cash Inflows

Table Value

Present Value

Year 1

$140,000

x

0.9090911

=

$127,272.74

Year 2

300,000

x

0.8264462

=

247,933.80

Year 3

360,000

x

0.7513153

=

270,473.40

Year 4

400,000

x

0.6830134

=

273,205.20

Salvage value

65,000

x

0.6830134

=

44,395.85

Total cash inflow

963,280.99

Cash outflows

Cost of trucks

(800,000.00)

Training cost

(16,000.00)

Net present value

$147,280.99

1Table 1, n=1, r=10% 3Table 1, n=3, r=16%

2Table 1, n=2, r=10% 4Table 1, n=4, r=16%

b.

Alternative 1:

Present value of cash inflows

$906,126.46

––––––––––––––––––––––––––––––––

=

––––––––––––––

=

1.19

Present value of cash outflows

$760,000

Alternative 2

Present value of cash inflows

$963,280.99

––––––––––––––––––––––––––––––––

=

––––––––––––

=

1.18

Present value of cash outflows

$816,000

c. Alternative 1 will provide the higher rate of return, but alternative 2 results in a

greater net present value. With Alternative 1 there is only $760,000 invested while