Chapter 13 – Relevant Information for Special Decisions

13-1

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

Teaching Notes for Chapter 13

In this chapter, students learn to identify information that is relevant to a specific decision

situation and to apply the information in reaching an appropriate decision. Traditional

textbooks frequently imply that whether a cost is relevant to a special decision depends

on whether the cost exhibits fixed or variable behavior. The conceptual flaw in this

approach hinders student understanding of cost behavior and relevance. If you want your

students to understand the relevance of accounting information, you must dispel the

notion that cost behavior determines relevance. Consider a production supervisor’s

salary that is fixed relative to the number of units of product produced. A traditional

approach would suggest that the salary is not relevant to a special order decision because

it is fixed and therefore will remain unchanged regardless of whether the special order is

accepted or rejected. The message implied by this explanation is that fixed costs are not

relevant. Students are confused later to learn that the same cost (a production

supervisor’s salary) may be relevant in deciding whether to make or buy the product. If

the company buys the product, it avoids the costs of producing it, including the

supervisor’s salary. The salary cost is still fixed, but now it is a relevant cost.

Clearly, a fixed cost can be relevant or not relevant. Likewise, a variable cost can be

relevant or not relevant. Consider the cost of direct labor. Direct labor cost is relevant to

a special order decision because it can be avoided by rejecting the special order. Now

change the decision context. Suppose a company is deciding whether to make red or

green chairs. Either color chairs fired or green) requires the same amount of direct labor.

Here, the labor cost is variable but not relevant. As these examples show, there is no

connection between cost behavior and relevance. A cost is relevant to a special decision

if it satisfies two criteria: (1) it is future-oriented, and (2) it differs between the

alternatives available to the decision-maker. These criteria apply regardless of whether

the cost is fixed or variable.

To avoid the confusion associated with using fixed and variable terminology when

identifying costs relevant to special decisions, Chapter 13 uses terminology from the

activity-based costing (ABC) literature to describe the costs involved. We classify costs

into one of four hierarchical categories: (1) unit-level, (2) batch-level, (3) product-level,

and (4) facility-level costs. These cost categories are logically associated with relevance.

For example, because unit-level costs are incurred each time a unit of product is made,

they are relevant to a special order decision about whether additional units should be

made and sold. However, because the number of units of product made and sold does not

affect product-level and facility-level costs, those costs are not relevant to a special order

decision. The hierarchical classification scheme still requires exercising judgment. For

example, whether a batch-level cost is relevant to a special order decision depends upon

whether the additional units would be produced as part of an existing batch or as a

separate batch. Even so, the hierarchical classification scheme is clearer than the cost

behavior approach. While it may be unfamiliar at first, we encourage you to experiment

with the hierarchical classification.

By this point in the course, most students are ready to begin the first class on Chapter

13 with a problem-based learning exercise. Demonstration Problem 13-1 provides an

entertaining introduction to the topic of special decisions. It does not require knowledge

Chapter 13 – Relevant Information for Special Decisions

13-2

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

of the hierarchical scheme discussed above. While you may find the solution obvious,

repeated use in our classes suggests that students find the answer elusive enough to

stimulate enthusiastic class participation.

Detailed Outline of a Lesson Plan for Chapter 13

I. Use Demonstration Problem 13-1 as a problem-based learning exercise.

Briefly explain how DDI established the $350 price. Only clarify the facts of the

problem. Do not provide instruction regarding the meaning of relevance. This is

a problem-based learning experience. Providing the answer too early removes the

opportunity for students to discover concepts for themselves. Have students work

in their groups to complete the problem requirement.

II. Engage students in a discussion regarding their groups’ decisions. The

problem calls for the group members to select a spokesperson. This is an

effective, non-threatening way to encourage group members to take the exercise

seriously. Knowing that the group’s answer may have to be defended publicly

motivates students to develop a serious response. Allowing the group to select the

spokesperson reduces anxiety. Most groups include at least one person who does

not mind acting as a spokesperson. Consequently, group members are motivated

but not threatened.

A. After allowing time (usually 10 to 15 minutes) for groups to formulate

answers, ask the spokespersons to raise their hands to indicate whether they

would accept or reject the special order for 200 driveways. Begin with a

spokesperson from a group that rejects the offer. Ask the spokesperson to

explain why the group rejected the offer. When you ask an open-ended

question such as this, be prepared for unexpected responses. Remain open-

minded and respectful of all answers. The answer most frequently

encountered in our classes centers on the mistaken belief that the cost of

paving the driveways is greater than the sales price. Students draw this

conclusion because they include the overhead cost in the cost of pouring the

additional 200 driveways. The way different groups measure the overhead

cost can vary. Some groups simply include the $80 per driveway overhead

cost mentioned in the problem. Because the resulting total cost of $300

exceeds the offer price of $250, they reject the offer. Other groups recalculate

the per unit cost based on a revised volume of 1,200 driveways. ($80,000 /

1,200 = $67 per driveway). The total cost is then $287 ($100 materials +

$120 labor + $67 overhead). Again, the cost of $287 is greater than the offer

price of $250, and students reject the offer. At this point, you should not

correct the answer. Doing so would end the discussion. Instead, ask a

spokesperson from a group that decided to accept the order to explain their

reasoning. Here also, you may get a variety of answers. Keep searching until

you find the right one. We have never had a class in which some group did

not recognize that the overhead cost was not relevant because DDI incurs it

regardless of whether the special order is accepted or rejected. (The overhead

Chapter 13 – Relevant Information for Special Decisions

13-3

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

cost does not differ between the alternatives.) When trying to identify the

right answer, look for the right logic rather than the right terms. Remember

this is a problem-based learning exercise. Students have not yet been exposed

(unless they read ahead!) to such terms as relevant, differential, incremental,

or avoidable. Even so, some students are able to tap into the logic. In a

problem-based learning experience, the instructor’s job is to provide names

for concepts the students discover. This teaching strategy is different from the

traditional approach wherein the instructor provides definitions for terms.

B. After emphasizing that the overhead cost is not relevant, try playing devil’s

advocate. Tell the students that you are one of DDI’s regular customers who

just happens to run into Rachel Rodgers, the new builder, at a local Chamber

of Commerce meeting. You discover that Rachel is paying $250 per driveway

while you are paying $350. Engage a spokesperson from a group that decided

to accept the offer, and complain about the excessive charge you are paying

compared to what Ms. Rodgers is paying. Permit other members of the class

to respond to your complaint. This approach provides a natural preface to a

discussion of the qualitative features that decision-makers must consider.

C. Now it is time to define relevance.

III. Introduce the concept of relevance. Explain that the overhead cost in the DDI

problem is not relevant to the special order decision because DDI will incur it

regardless of whether the order is accepted or rejected. In other words, DDI

cannot avoid the overhead cost by rejecting the special order. Explain that to be

relevant a cost must (1) differ between the alternatives, and (2) be future-oriented.

Reinforce the two criteria for relevance with an example that contrasts relevant

costs with a sunk cost. The following illustration has worked well in the

classroom. Ask your students to suppose their friend paid $20,000 to purchase

stock. The market price of the stock immediately dropped to $15,000. The friend

wants to buy a car. The friend does not have the money to buy the car and does

not want to sell the stock because she will lose $5,000 ($20,000 cost − $15,000

current market value). Is the friend exercising good or poor judgment? Give your

students time to ponder the question. If you have time, let a few of them share

their ideas with the class. Conclude with the observation that whether to sell the

stock is their friend’s personal choice, but they should make sure the friend’s

decision is not influenced by the loss in market value of the stock. The $20,000

stock cost is irrelevant. The relevant question to the friend is, “if you had $15,000

today would you buy stock or a car?” If the answer is “buy the car,” then she

should sell the stock and purchase the car.

IV. Distinguish between product costing, cost behavior, and relevance.

Students who understand concepts can distinguish among them. Thus far in the

course, we have introduced three key concepts: (1) product costing, (2) cost

behavior, and (3) relevance. Demonstration Problem 13-2 is designed to

compare and contrast these three concepts. Also, we integrate all three concepts

Chapter 13 – Relevant Information for Special Decisions

13-4

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

in one problem to alert students to the interrelationships among underlying

concepts. They cannot succeed if they merely memorize one chapter at a time

and forget it after the test. They must develop a foundation that enables them to

fuse isolated concepts into an integrated whole. Demonstration Problem 13-2

provides a critical cumulative learning experience. Cover this problem in class

and then assign Exercises 13-1 and 13-2 as homework assignments.

V. Introduce the concept of opportunity cost and explain why opportunity costs

are relevant.

We suggest the following example. Brown Manufacturing Company (BMC) is

currently using a building as a manufacturing facility. Depreciation on the

building is $200,000 per year. The building is in a location that is experiencing

significant growth in retail shopping. A retail company has offered to rent the

manufacturing facility from BMC at a price of $180,000 per year. What cost is

relevant in deciding whether to move the manufacturing facility to a different

location?

Answer: The $180,000 opportunity cost is the relevant cost. It represents the

amount BMC will sacrifice if it chooses to remain in the same location. The

depreciation of $200,000 is a sunk cost that is not relevant.

VI. Introduce the cost classification hierarchy. While this classification scheme

may be unfamiliar at first, once you are familiar with it, you will find it a superior

tool for identifying the costs relevant to a given decision. The four cost categories

are:

A. Unit-level: costs incurred to make or sell one unit of a product or service.

Examples include direct materials and direct labor costs.

B. Batch-level: costs incurred to make or distribute a batch (group) of units of a

product. Examples include setup and inspection costs.

C. Product-level: costs incurred to create, sustain, or sell a product or product

line. Examples include legal costs incurred each time a publishing company

files for a new book copyright and engineering costs incurred each time an

automobile manufacturer adds a new model to its line. The distinguishing

feature here is between new products or more units of existing products.

D. Facility-level: costs incurred to establish and maintain a business facility.

Examples include factory depreciation, maintenance, utilities, and

administrative salaries.

The relationships between different types of special decisions and the above cost

classifications are described below.

A. Special order decisions require identifying the relevant costs of making and

selling additional units of a product and then comparing these costs with the

incremental sales revenue the company will earn if it accepts the special order.

Chapter 13 – Relevant Information for Special Decisions

13-5

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

The quantitative aspect of a special order decision involves three steps. First,

determine the amount of revenue the company will earn by selling the

additional units of product. Next, determine the relevant costs of making the

additional units. Third, compare the incremental revenues to the additional

costs. If the incremental revenues exceed the additional costs, the quantitative

analysis suggests accepting the special order.

What costs must a company consider when deciding whether to sell

additional units of a product at a price below the company’s normal sales

price? If the company makes and sells additional units of a product, total unit-

level costs will differ from what they would be if the company rejected the

special order. Consequently, unit-level costs are relevant for special order

decisions. Batch-level costs may or may not be relevant to special order

decisions. Batch-level costs are not relevant if expanding production of an

existing batch can fill the special order. However, if the company must

produce a separate batch to satisfy the special order, batch-level costs are

relevant because they could be avoided if the special order were rejected.

Since product-level and facility-level costs remain unchanged regardless of

whether a special order is accepted or rejected, they are not avoidable and

therefore are not relevant.

B. Outsourcing decisions require identifying the relevant costs of making a

product internally and then comparing those costs to the cost of outsourcing –

buying the product from an outside supplier. Outsourcing decisions are

frequently called make or buy decisions. Unit-level, batch-level, and product-

level costs are all relevant to outsourcing decisions. In general, these costs are

avoidable if products are outsourced instead of being produced internally.

Some product-level costs, however, may not be relevant to an outsourcing

decision. For example, product sales commissions are incurred regardless of

whether the product is manufactured internally or purchased from a third

party. Because facility-level costs remain unchanged regardless of whether a

product is made internally or outsourced, they are not avoidable and therefore

are not relevant.

C. Segment elimination decisions require identifying the relevant costs of

operating a business segment and comparing these costs to the revenue

generated by the segment. The choice is between closing down or continuing

to operate the business segment. Unit-level, batch-level, product-level, and

facility-level costs are usually all relevant to a segment elimination decision.

Some facility-level costs, however, may not be relevant. For example, certain

corporate-level facility costs may be incurred even if a segment of a company

is eliminated. Such facility-level costs are not avoidable and are therefore not

relevant.

D. Asset replacement decisions require identifying the relevant costs of

operating existing assets and comparing these costs to the costs of operating

new, replacement assets. Quantitative analysis will indicate that a company

should choose the lowest cost option.

VII. Work an example of each type of special decision problem.

Chapter 13 – Relevant Information for Special Decisions

13-6

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

A. Recall that Demonstration Problem 13-1 involved a special order decision.

Exercise 13-6 in the textbook provides a good follow-up problem. You

should be able to assign this exercise without providing any introduction.

You could have the students compare their answers with members of their

group. If you are short of time, you may simply provide the answer or assign

the problem as homework for students to do outside of class.

B. Provide a brief explanation of an outsourcing decision. Explain that unit-

level, batch-level, and some product-level costs are relevant to outsourcing

decisions. Use Exercise 13-13 as an example. This exercise includes

considering opportunity cost. You may choose to work the exercise as a

demonstration problem or let students attempt it on their own as you circulate

through the room. By seeking help from you or their group members most

students are able to complete this problem. While the approach of letting

students discover concepts themselves may be highly effective, it does require

considerable class time. The extent to which you choose to intervene is a

matter of personal style.

C. Provide a brief explanation of a segment elimination decision. Use Exercise

13-14 as a demonstration problem.

D. Provide a brief explanation of an asset replacement decision. Use Exercise

13-18 as a demonstration problem.

Summary Outline of a Lesson Plan for Chapter 13

I. Use Demonstration Problem 13-1 as a problem-based learning exercise.

Have students work in their groups to complete the problem requirement.

II. Engage students in a discussion regarding their groups’ decisions.

III. Introduce the concept of relevance. To be relevant a cost must (1) differ

between the alternatives, and (2) be future-oriented.

IV. Distinguish between product costing, cost behavior, and relevance.

The text has thus far introduced three key concepts: (1) product costing, (2) cost

behavior, and (3) relevance. Demonstration Problem 13-2 is designed to

directly compare and contrast these three concepts. Exercises 13-1 and 13-2 may

be assigned as homework.

V. Introduce the concept of opportunity cost and explain why opportunity costs

are relevant.

VI. Introduce the cost classification hierarchy. The four cost categories are:

A. Unit-level: costs incurred to make or sell one unit of a product or service,

e.g. direct materials and direct labor costs.

B. Batch-level: costs incurred to make or distribute a batch (group) of units of a

product, e.g. setup and inspection costs.

Chapter 13 – Relevant Information for Special Decisions

13-7

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

C. Product-level: costs incurred to create, sustain, or sell a product or product

line, e.g. legal costs incurred each time a publishing company files for a new

manufacturer adds a new model to its line up. The distinguishing feature here

is between new products or more units of existing products.

D. Facility-level: costs incurred to establish and maintain a business facility, e.g.

factory depreciation, maintenance, utilities, and administrative salaries.

Discuss the relationships between different types of special decisions and the

above cost classifications.

VII. Work an example of each type of special decision problem.

A. Use Exercise 13-6A as an example of a special order decision.

B. Use Exercise 13-13 as an example of an outsourcing decision.

C. Use Exercise 13-14as an example of a segment elimination decision.

D. Use Exercise 13-18 as an example of an asset replacement decision.

Quiz Questions for Chapter 13

Use the following information to answer the next three questions.

Harcourt Marketing (HM) has the capacity to produce 10,000 fax machines per year. HM currently

produces and sells 7,000 units per year. The fax machines normally sell for $100 each. Modem Products

has offered to buy 2,000 fax machines from HM for $60 each. Unit–level costs associated with

manufacturing each fax machine are $15 for direct labor and $40 for direct materials. Product-level and

facility-sustaining costs are $50,000 and $65,000, respectively.

1. What is HM’s current profit (net income)?

a. $115,000

b. $120,000

c. $200,000

d. $315,000

2. How much would profit increase (decrease) if HM accepted this special order?

a. $10,000

b. $112,000

c. ($10,000)

d. ($112,000)

3. Should HM accept the special offer?

a. yes, unequivocally

b. no, because it would decrease company profit

c. yes, if qualitative factors are favorable.

d. no, because GAAP requires all costs to be included in the product

Use the following information to answer the next two questions.

Based on the segment income statement below, Gourmet Sorbet is considering eliminating its Mango

Tango line.

Revenue from Mango Tango sales

$500,000

Salaries for Mango Tango workers

(120,000)

Direct material costs for Mango Tango

(300,000)

Sunk costs (equipment depreciation)

(75,000)

Allocated company-wide facility-sustaining costs

(50,000)

Net loss

$ (45,000)

4. The total relevant costs in this decision add up to

a. $400,000.

b. $475,000.

c. $525,000.

d. $420,000

Chapter 13 – Relevant Information for Special Decisions

13-8

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

5. If Mango Tango were eliminated, profitability would

a. increase $25,000.

b. increase $525,000.

c. decrease $80,000.

d. decrease $100,000.

6. To be relevant, information must

a. differ among the alternatives.

b. make a difference in a decision.

c. be future oriented.

d. all of the above.

7. GOGO Golf Carts currently produces its own electric motors. Electco has offered to sell the electric

motors to GOGO at a price of $300 each.

GOGO’s current production information for the motors follows:

Unit-level material and labor $175

Facility-level depreciation of manufacturing equip. $12,000/year

Product-level supervisor’s salary $24,000/year

Annual facility-level utilities . $1,500

GOGO is currently operating profitably producing 2,000 engines a year. GOGO maintains worker

loyalty by offering employees lifetime employment. Which of the following is true?

a. GOGO should buy the engines for cost savings of $113 per unit.

b. GOGO should continue producing the engines.

c. GOGO has relevant costs of greater than $300 a unit and should buy.

d. GOGO will save $126,000 by producing the engines.

8. A cost that is not affected by later decisions is called a(n)

a. replacement cost.

b. historical cost.

c. opportunity cost.

d. sunk cost.

9. A condensed income statement for Tramco follows: (amounts are in thousands of dollars)

Products

F

G

H

Total

Sales (total)

$200

$180

$320

$700

Unit-level Variable Cost (total)

(120)

(160)

(200)

(480)

Contribution Margin

80

20

120

220

Facility-Level Fixed Cost

(25)

(30)

(40)

(95)

Income (Loss)

$ 55

$(10)

$ 80

$125

Tramco’s management is considering whether to discontinue manufacturing product G at the

beginning of the next year. Doing so will have no effect on total fixed costs and no effect on the

sales or variable costs of products F and H. The change in income that would result from

discontinuing product G is

a. $10,000 increase

b. $10,000 decrease

c. $20,000 decrease

d. $30,000 increase

10. Jason Company is considering replacing equipment that originally cost $600,000. New equipment

costs $500,000, and the old equipment can be sold for $400,000. What is the sunk cost in this

situation?

a. $600,000

b. $200,000

c. $400,000

d. $500,000

Chapter 13 – Relevant Information for Special Decisions

13-9

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

11. Tom’s Toolery is operating at 80% of its productive capacity. It is currently purchasing for $20

each a part used in its manufacturing operation. Tom’s estimates it could make the part internally for a total

cost of $24 per unit, consisting of $18 of unit-level production costs and $6 of facility-level costs that are

currently attributed to other products. Tom’s usually purchases 50,000 units of the part each year. These

units could be manufactured using Tom’s excess capacity. What is the differential increase or decrease in

cost derived from making the part rather than purchasing it?

a. $100,000 cost decrease

b. $100,000 cost increase

c. $200,000 cost increase

d. $1,000,000 cost increase

Solutions to Quiz Questions

Question

Answer

1

C

2

A

3

C

4

D

5

C

6

D

7

B

8

D

9

C

10

A

11

A

Demonstration Problems for Chapter 13

Demonstration Problem 13-1 Special Order

Davis Driveways, Inc. (DDI) pours concrete driveways for single family homes. DDI uses a cost-plus

pricing approach. The company’s accountant prepared the following report showing how DDI

established the price per driveway at $350.

Davis Driveways, Inc.

Cost Plus Pricing Policy

Materials $100

Labor 120

Overhead* 80

Total $300

Desired Profit 50

Price $350

*Annual overhead cost for rent on the corporate office and supervisory

salaries is $80,000. Normal volume is 1,000 driveways per year.

Overhead cost per unit is determined as $80,000 / 1,000 units = $80 per

unit. The relevant range is from 800 to 1,500 units.

Chapter 13 – Relevant Information for Special Decisions

13–10

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

A new builder in town, Rachel Rodgers, has acquired a large tract of land upon which

she intends to build 200 single family homes. Ms. Rodgers offers to purchase all 200

driveways from DDI. However, she is willing to pay only $250 per driveway.

Required

Assume your group is a management team responsible for deciding whether to accept or

reject Ms. Rodgers’ offer. Develop a response, support your decision with appropriate

computations, and choose a spokesperson to explain your answer.

Demonstration Problem 13-2 Contrast Relevance, Cost

Behavior, and Cost Type

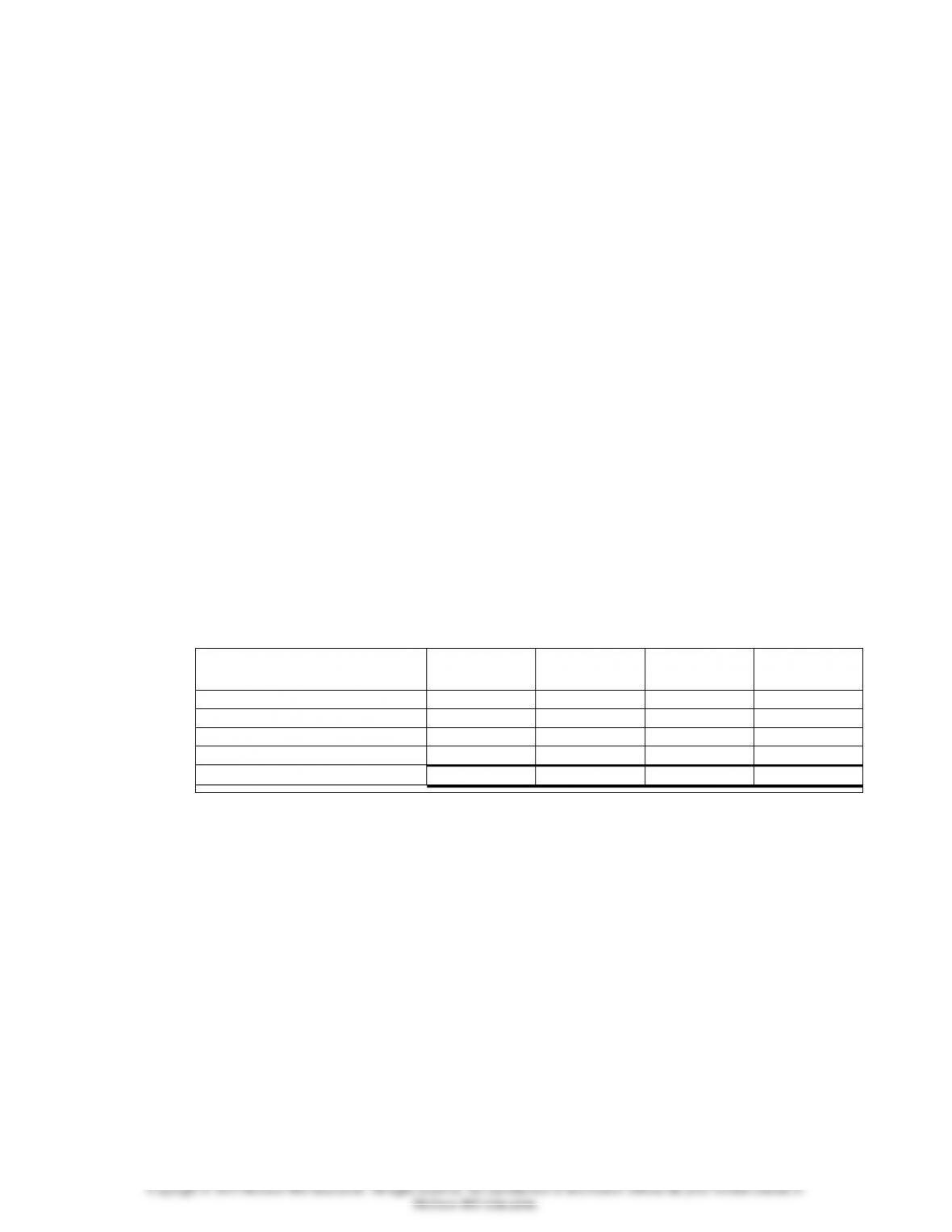

Pass Fast, Inc. is considering two alternative locations in which to conduct its CPA

review course. One alternative is an exclusive hotel; the other is a moderately priced

training facility. The hotel is in a central location easily accessible to potential students.

The training facility is in a less desirable location. Pass Fast has gathered the following

cost data regarding the two locations.

Cost Items

Hotel

Training

Facility

Relevant?

Cost

Behavior

Product

or GS&A

Rental Fee for Classroom

$2,000

$1,500

Twenty Advertising Brochures Distributed to

each Student for Referrals

250

250

Cost of Instruction

5,000

5,000

Books (per student)

100

100

Refreshments (per student)

5

4

Depreciation on Instructional Equipment

400

400

Required

a. In the column titled “Relevant?” indicate whether each cost is relevant (Yes) or not

relevant (No) to deciding which facility to rent for the course.

b. In the column titled “Cost Behavior” indicate whether each cost is fixed, variable, or

mixed relative to the number of students attending the course.

c. In the column titled “Product or GS&A” indicate whether each cost would be

classified as a product cost or a general, selling, and administrative (GS&A) cost.

Demonstration Problem 13-1 Solution

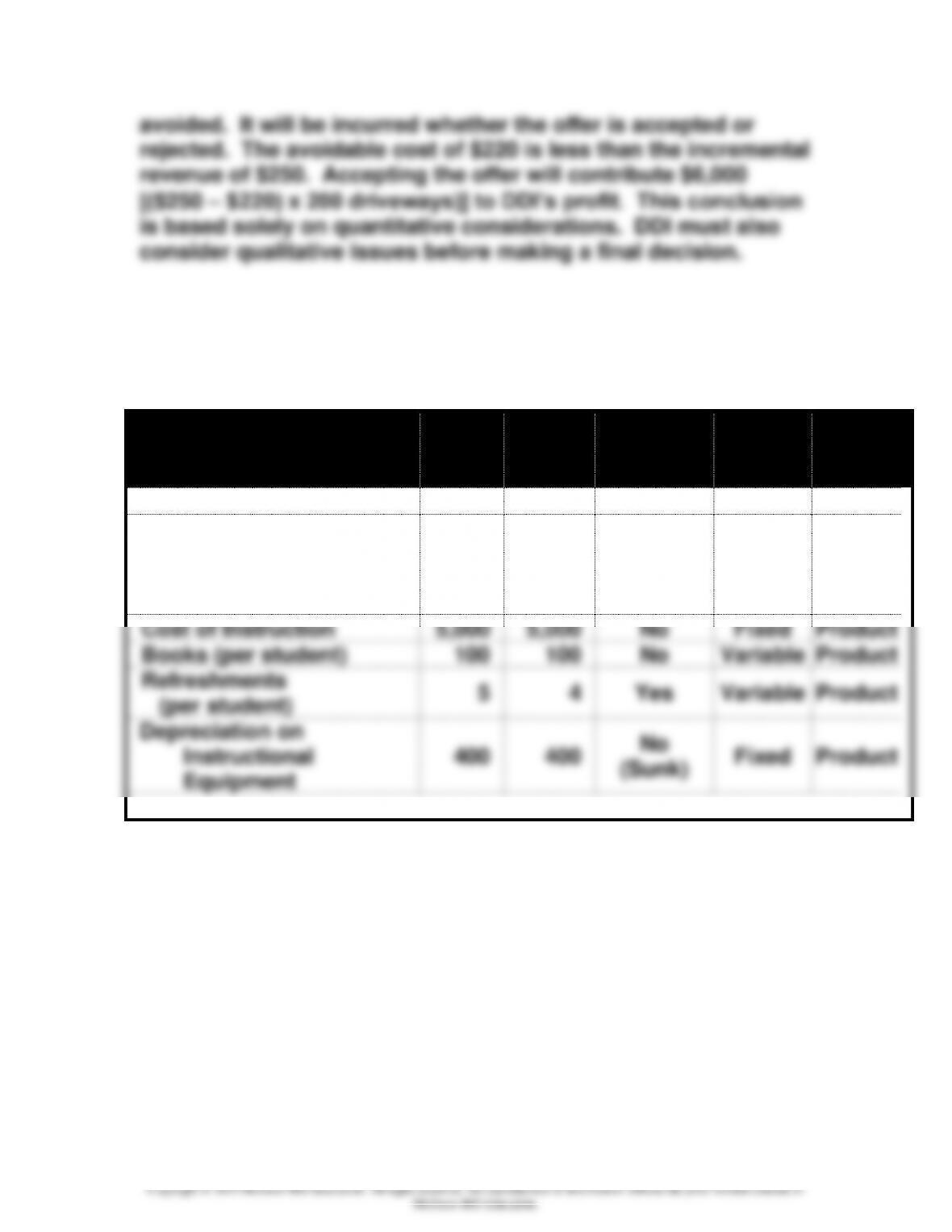

From a quantitative standpoint, DDI should accept the offer. By

not accepting, DDI would avoid the $220 per driveway cost of

Chapter 13 – Relevant Information for Special Decisions

13–11

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

Demonstration Problem 13-2 Solution

Cost Items

Hotel

Training

Facility

Relevant?

Cost

Behavior

Product

or

GS&A

Rental Fee for Classroom

$2,000

$1,500

Yes

Fixed

Product

Twenty Advertising

Brochures Distributed to

each Student for

Referrals

250

250

No

Variable

GS&A

Cost of Instruction

5,000

5,000

No

Fixed

Product

Books (per student)

100

100

No

Variable

Product

Refreshments

(per student)

5

4

Yes

Variable

Product

Depreciation on

Instructional

Equipment

400

400

No

(Sunk)

Fixed

Product

Demonstration Problem 13-1 Work Paper