6-1

PROBLEM 6-25

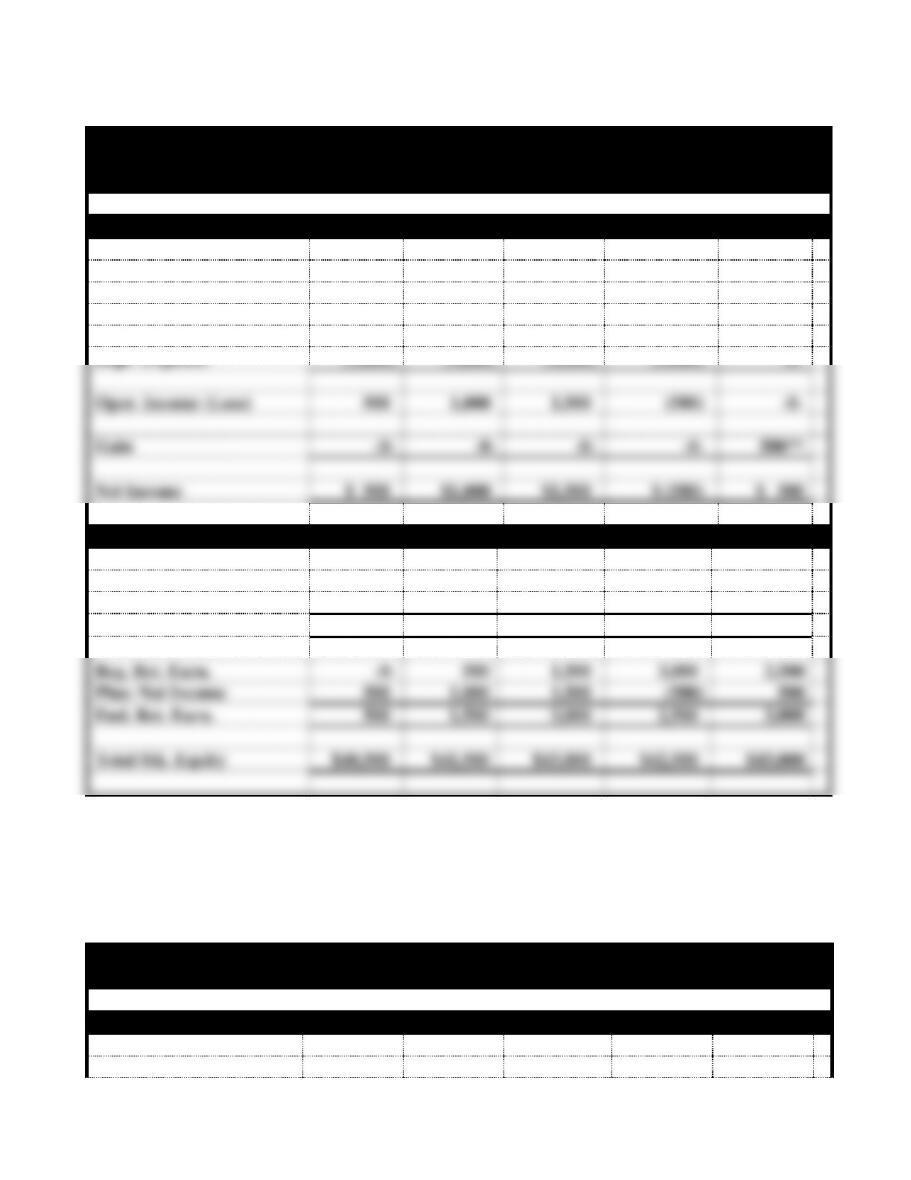

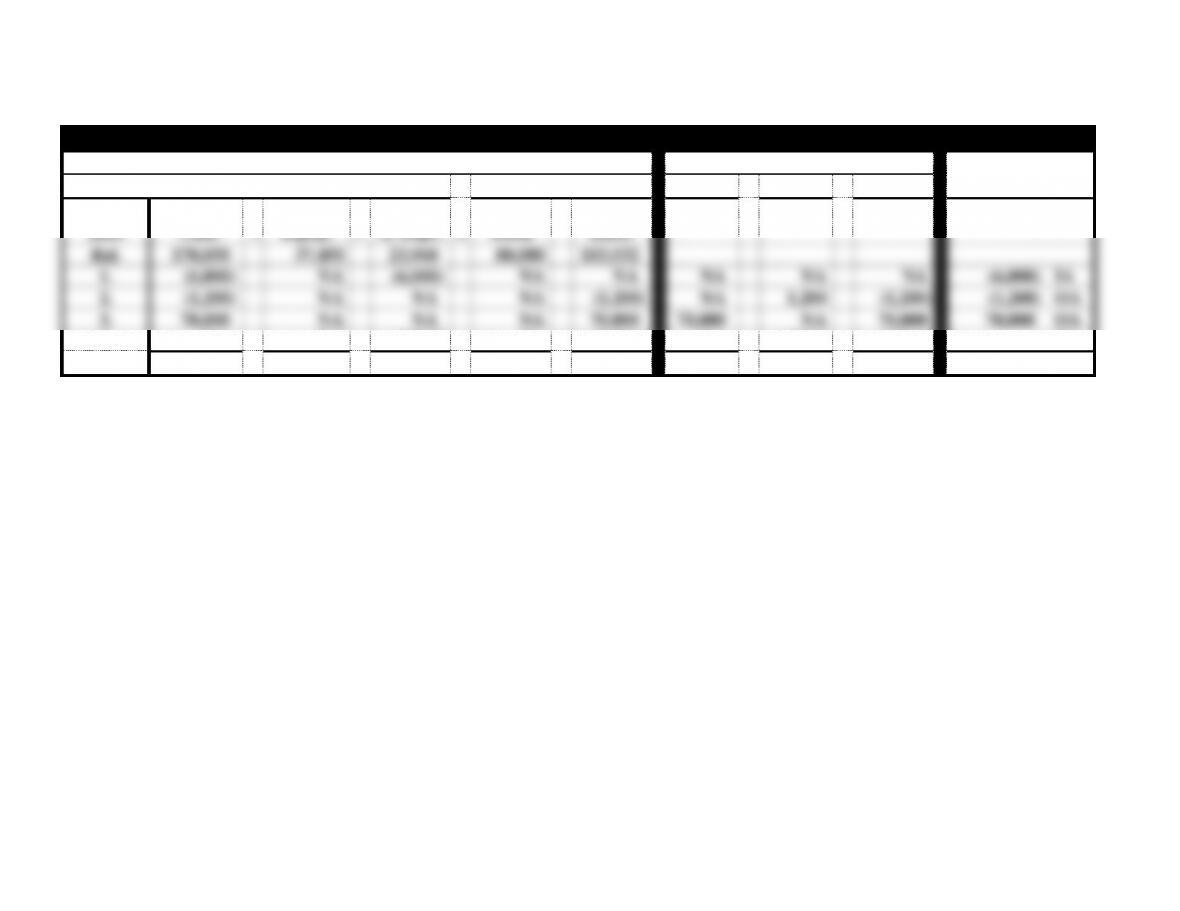

Zhao Company

Financial Statements

For the Year Ended December 31

Income Statements

2014

2015

2016

2017

2018

Revenue

$9,500

$10,000

$10,500

$8,500

$ -0–

Depr. Expense*

(9,000)

(9,000)

(9,000)

(9,000)

-0-

Oper. Income (Loss)

500

1,000

1,500

(500)

-0-

Gain

-0-

-0-

-0-

-0-

500**

Net Income

$ 500

$1,000

$1,500

$ (500)

$ 500

Statements of Changes in Stockholders’ Equity

Beg. Com. Stock

$ -0-

$40,000

$40,000

$40,000

$40,000

Plus: Stk. Issued

40,000

-0-

-0-

-0-

-0-

End. Com. Stock

40,000

40,000

40,000

40,000

40,000

Beg. Ret. Earn.

-0-

500

1,500

3,000

2,500

Plus: Net Income

500

1,000

1,500

(500)

500

End. Ret. Earn.

500

1,500

3,000

2,500

3,000

Total Stk. Equity

$40,500

$41,500

$43,000

$42,500

$43,000

*Depreciation: $40,000 − $4,000 (salvage value) = $36,000;

$36,000 4 = $9,000 per year

**Sale of Equipment: Sales price $4,500 less book value $4,000=$500 gain

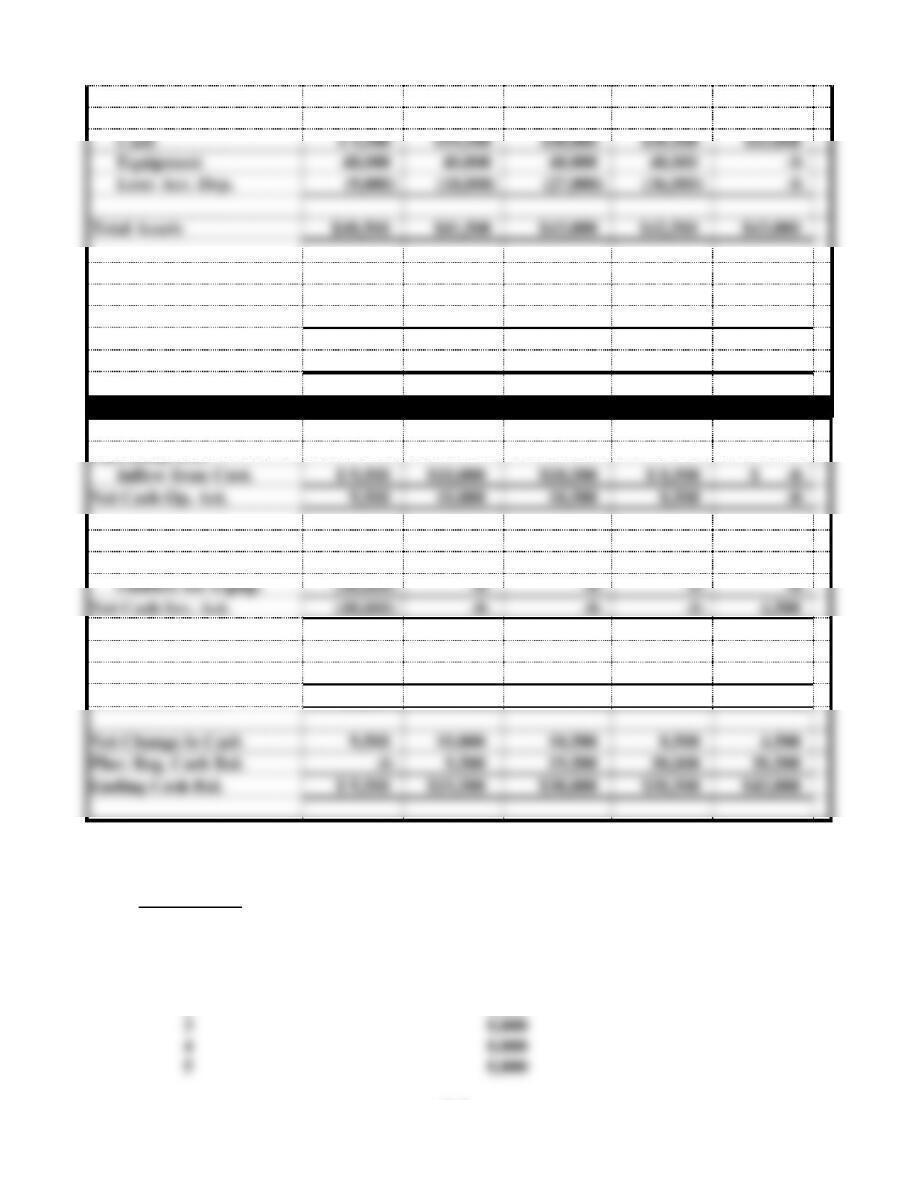

PROBLEM 6-25 (cont.)

Zhao Company

Financial Statements

Balance Sheets as of December 31

2014

2015

2016

2017

2018

6-2

Assets

Cash

$ 9,500

$19,500

$30,000

$38,500

$43,000

Equipment

40,000

40,000

40,000

40,000

-0-

Less: Acc. Dep.

(9,000)

(18,000)

(27,000)

(36,000)

-0-

Total Assets

$40,500

$41,500

$43,000

$42,500

$43,000

Stockholders’ Equity

Common Stock

$40,000

$40,000

$40,000

$40,000

$40,000

Retained Earnings

500

1,500

3,000

2,500

3,000

Total Stk. Equity

$40,500

$41,500

$43,000

$42,500

$43,000

Statements of Cash Flows for the Year Ended December 31

Operating Act.:

Inflow from Cust.

$ 9,500

$10,000

$10,500

$ 8,500

$ -0-

Net Cash Op. Act.

9,500

10,000

10,500

8,500

-0-

Investing Act.:

Inflow from Sale

-0-

-0-

-0-

-0-

4,500

Outflow for Equip.

(40,000)

-0-

-0-

-0-

-0-

Net Cash Inv. Act.

(40,000)

-0-

-0-

-0-

4,500

Financing Act.

Inflow from Stock

40,000

-0-

-0-

-0-

-0-

Net Cash Fin. Act.

40,000

-0-

-0-

-0-

-0-

Net Change in Cash

9,500

10,000

10,500

8,500

4,500

Plus: Beg. Cash Bal.

-0-

9,500

19,500

30,000

38,500

Ending Cash Bal.

$ 9,500

$19,500

$30,000

$38,500

$43,000

PROBLEM 6-26

a. Straight-Line

(Cost − Salvage Value) Useful Life = Annual Depreciation

Year 1 ($42,000 − 2,000) 5 = $8,000 per year

2 8,000

6-3

b. Double-Declining Balance

Accum. Depreciation Annual

(Cost − at Beginning of Period) x (2 x SL Rate) = Depreciation

c. The amount of depreciation expense does not affect cash flow because depreciation is a

d. Straight-Line

Book value $42,000 − $24,000* = $18,000

PROBLEM 6-26 d. (cont.)

Double-Declining-Balance

Book Value $42,000 − $32,928* = $9,072

PROBLEM 6-27

Units-of-Production

Total Estimated

(Cost − Salvage Value) Units of Production = Cost per Unit

6-4

a. $28,500 − $2,500

200,000 = $.13 per mile

6-5

PROBLEM 6-27 (cont.)

b. NC = Net Change in Cash

Renner Corporation

Horizontal Statements Model

Balance Sheet

Income Statement

Statement of

Assets

=

Stockholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

Event

Cash

+

Book Value of Van

=

C. Stock

+

Ret. Ear.

Bal.

50,000

+

=

50,000

+

NA

NA

−

NA

=

NA

NA

Van

(28,500)

+

28,500

=

NA

+

NA

NA

−

NA

=

NA

(28,500) IA

Rev.

26,000

+

=

NA

+

26,000

26,000

−

NA

=

26,000

26,000 OA

Depr.

NA

+

(7,800)

=

NA

+

(7,800)

NA

−

7,800

=

(7,800)

NA

Bal.

47,500

+

20,700

=

50,000

+

18,200

26,000

−

7,800

=

18,200

(2,500) NC

Gain on Sale $ 950

6-6

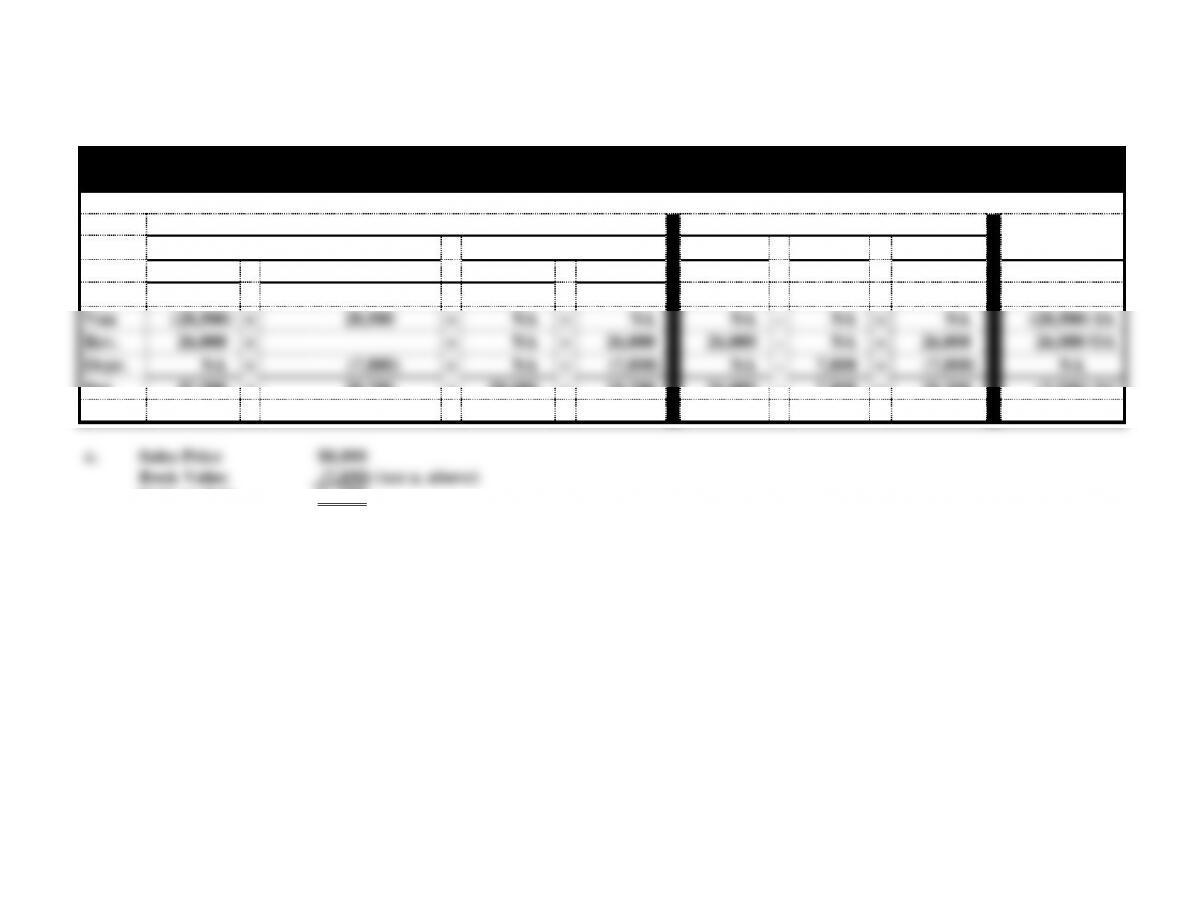

PROBLEM 6-28

a.

Engineering Solutions Inc. Horizontal Statements Model – 2014

Balance Sheet

Income Statement

Statemt. of

Assets

=

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

Event

2014

Cash

+

Equip.

−

A. Depr.

=

Com.

Stock

+

Ret.

Earn.

1.

80,000

NA

NA

80,000

NA

NA

NA

NA

80,000 FA

2.

(35,000)

35,000

NA

NA

NA

NA

NA

NA

(35,000) IA

3.

(2,450)

2,450

NA

NA

NA

NA

NA

NA

(2,450) IA

4.

65,000

NA

NA

NA

65,000

65,000

NA

65,000

65,000 OA

5.

(1,500)

NA

NA

NA

(1,500)

NA

1,500

(1,500)

(1,500) OA

6.

NA

NA

14,9801

NA

(14,980)

NA

14,980

(14,980)

NA

Bal.

106,050

+

37,450

−

14,980

=

80,000

+

48,520

65,000

16,480

48,520

106,050 NC

1($37,450) x (2 x .20) = $14,980

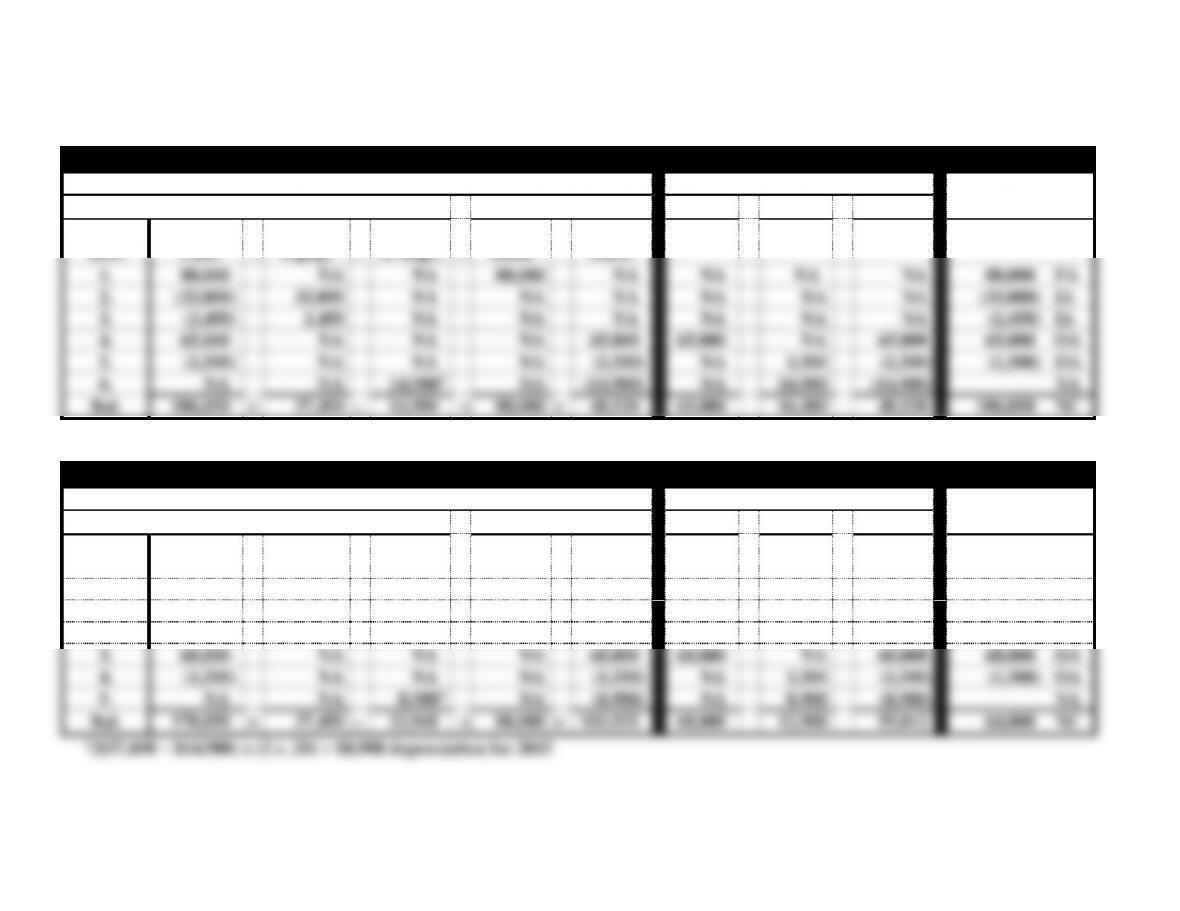

Engineering Solutions Inc. Horizontal Statements Model – 2015

Balance Sheet

Income Statement

Statemt. of

Assets

=

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

Event

2015

Cash

+

Equip.

−

A. Depr.

=

Com.

Stock

+

Ret.

Earn.

Bal.

106,050

37,450

14,980

80,000

48,520

1.

(1,000)

NA

NA

NA

(1,000)

NA

1,000

(1,000)

(1,000) OA

2.

(1,500)

NA

NA

NA

(1,500)

NA

1,500

(1,500)

(1,500) OA

3.

68,000

NA

NA

NA

68,000

68,000

NA

68,000

68,000 OA

4.

(1,500)

NA

NA

NA

(1,500)

NA

1,500

(1,500)

(1,500) OA

5.

NA

NA

8,9882

NA

(8,988)

NA

8,988

(8,988)

NA

Bal.

170,050

+

37,450

−

23,968

=

80,000

+

103,532

68,000

12,988

55,012

64,000 NC

2($37,450 − $14,980) x (2 x .20) = $8,988 depreciation for 2015

6-7

PROBLEM 6-28 (cont.)

Engineering Solutions Inc. Horizontal Statements Model – 2016

Balance Sheet

Income Statement

Statemt. of

Assets

=

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

Event

2014

Cash

+

Equip.

−

A. Depr.

=

Com.

Stock

+

Ret.

Earn.

Bal.

170,050

37,450

23,968

80,000

103,532

1.

(6,000)

NA

(6,000)

NA

NA

NA

NA

NA

(6,000) IA

2.

(1,200)

NA

NA

NA

(1,200)

NA

1,200

(1,200)

(1,200) OA

3.

70,000

NA

NA

NA

70,000

70,000

NA

70,000

70,000 OA

4.

NA

NA

9,7413

NA

(9,741)

NA

9,741

(9,741)

NA

Bal.

232,850

+

37,450

−

27,709

=

80,000

+

162,591

70,000

10,941

59,059

62,800 NC

3[$37,450 − ($23,968 − $6,000)] x (2 x .25) = $9,741 depreciation for 2016

6-8

PROBLEM 6-28 (cont.)

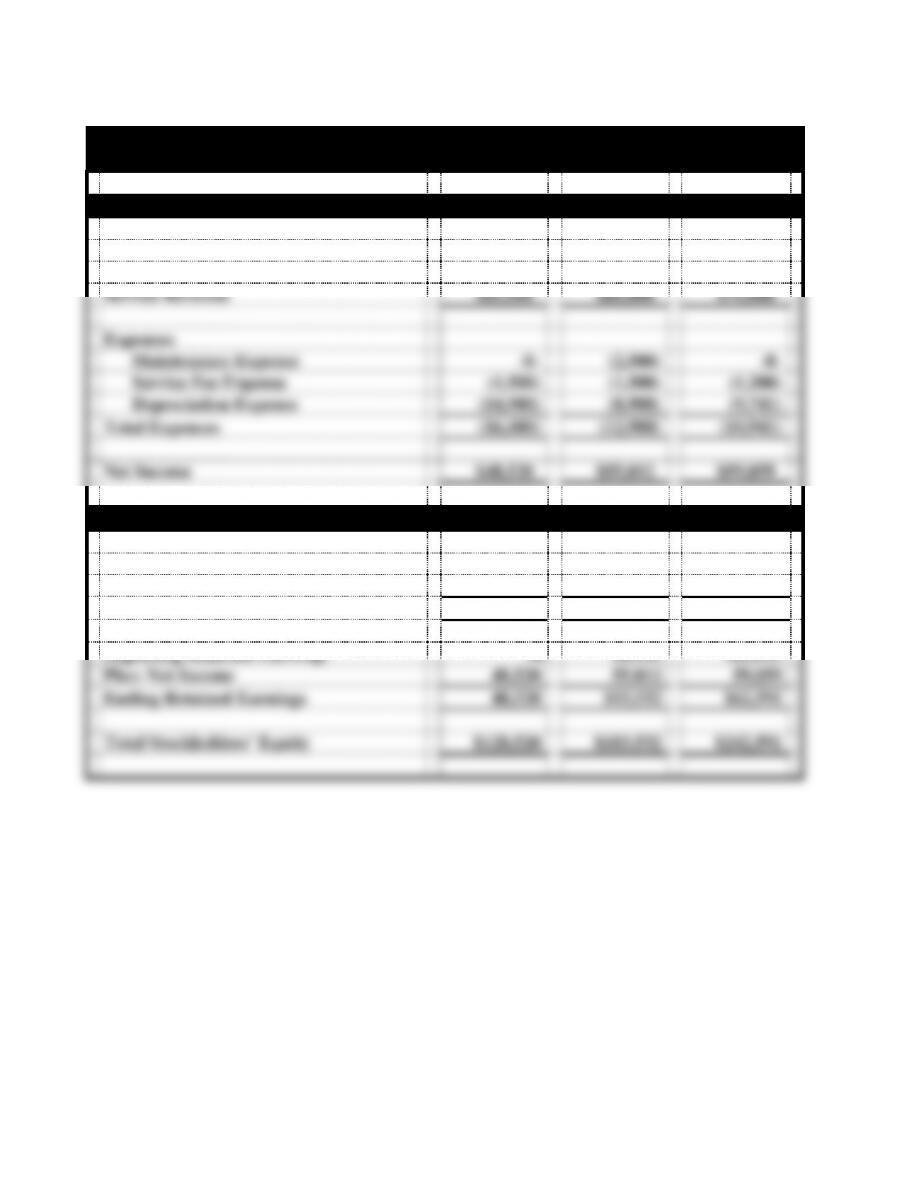

b.

Engineering Solutions, Inc.

Financial Statements For the Year Ended December 31

Income Statements

2014

2015

2016

Service Revenue

$65,000

$68,000

$70,000

Expenses

Maintenance Expense

-0-

(2,500)

-0-

Service Fee Expense

(1,500)

(1,500)

(1,200)

Depreciation Expense

(14,980)

(8,988)

(9,741)

Total Expenses

(16,480)

(12,988)

(10,941)

Net Income

$48,520

$55,012

$59,059

Statements of Changes in Stockholders’ Equity

Beginning Common Stock

$ -0-

$80,000

$ 80,000

Plus: Stock Issued

80,000

-0-

-0-

Ending Common Stock

80,000

80,000

80,000

Beginning Retained Earnings

-0-

48,520

103,532

Plus: Net Income

48,520

55,012

59,059

Ending Retained Earnings

48,520

103,532

162,591

Total Stockholders’ Equity

$128,520

$183,532

$242,591

6-9

PROBLEM 6-28 b.(cont.)

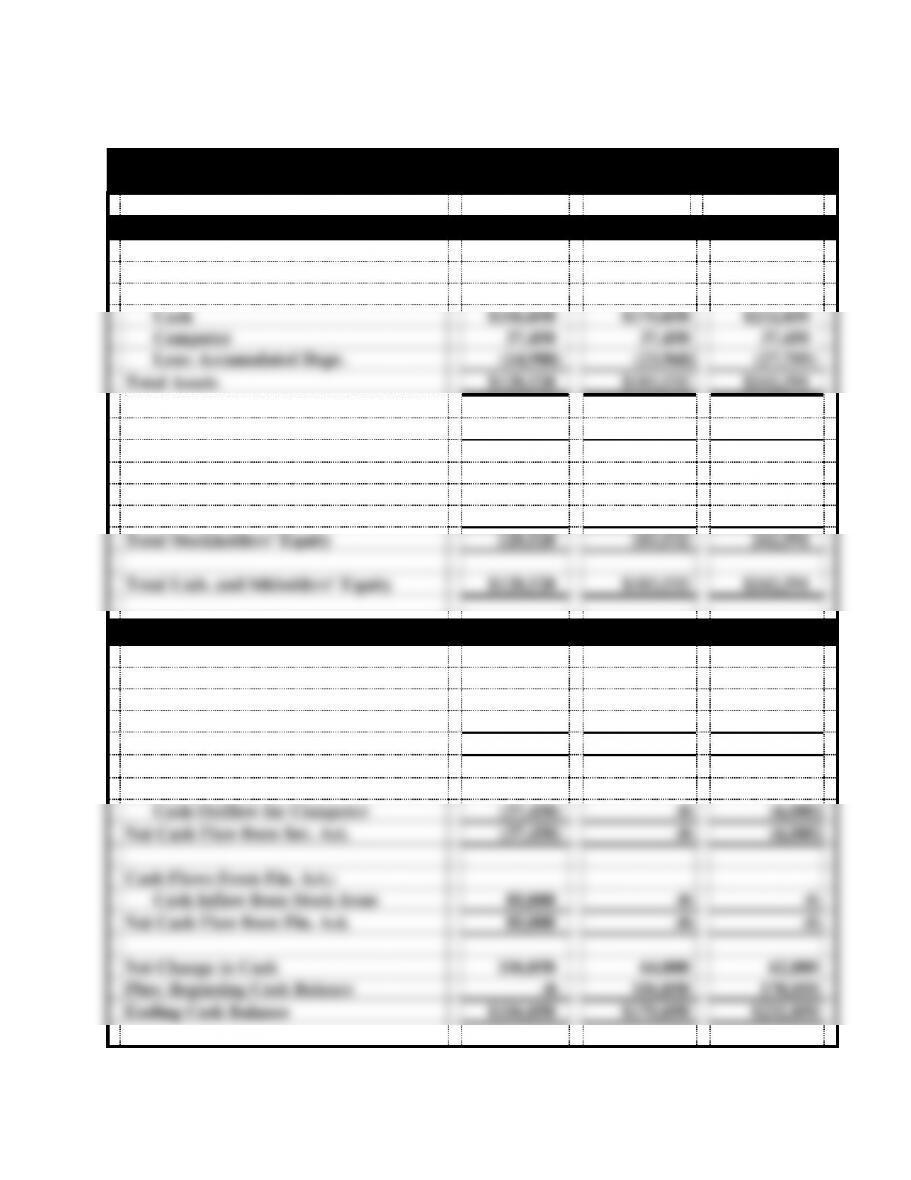

Engineering Solutions Inc.

Financial Statements

Balance Sheets

2014

2015

2016

Assets

Cash

$106,050

$170,050

$232,850

Computer

37,450

37,450

37,450

Less: Accumulated Depr.

(14,980)

(23,968)

(27,709)

Total Assets

$128,520

$183,532

$242,591

Liabilities

$ -0-

$ -0-

$ – 0-

Stockholders’ Equity

Common Stock

80,000

80,000

80,000

Retained Earnings

48,520

103,532

162,591

Total Stockholders’ Equity

128,520

183,532

242,591

Total Liab. and Stkholders’ Equity

$128,520

$183,532

$242,591

Statements of Cash Flows

Cash Flows From Oper. Act.:

Inflow from Revenue

$65,000

$68,000

$ 70,000

Outflow for Expenses

(1,500)

(4,000)

(1,200)

Net Cash Flow from Oper. Act.

63,500

64,000

68,800

Cash Flows From Inv. Act.:

Cash Outflow for Computer

(37,450)

-0-

(6,000)

Net Cash Flow from Inv. Act.

(37,450)

-0-

(6,000)

Cash Flows From Fin. Act.:

Cash Inflow from Stock Issue

80,000

-0-

-0-

Net Cash Flow from Fin. Act.

80,000

-0-

-0-

Net Change in Cash

106,050

64,000

62,800

Plus: Beginning Cash Balance

-0-

106,050

170,050

Ending Cash Balance

$106,050

$170,050

$232,850

6-10

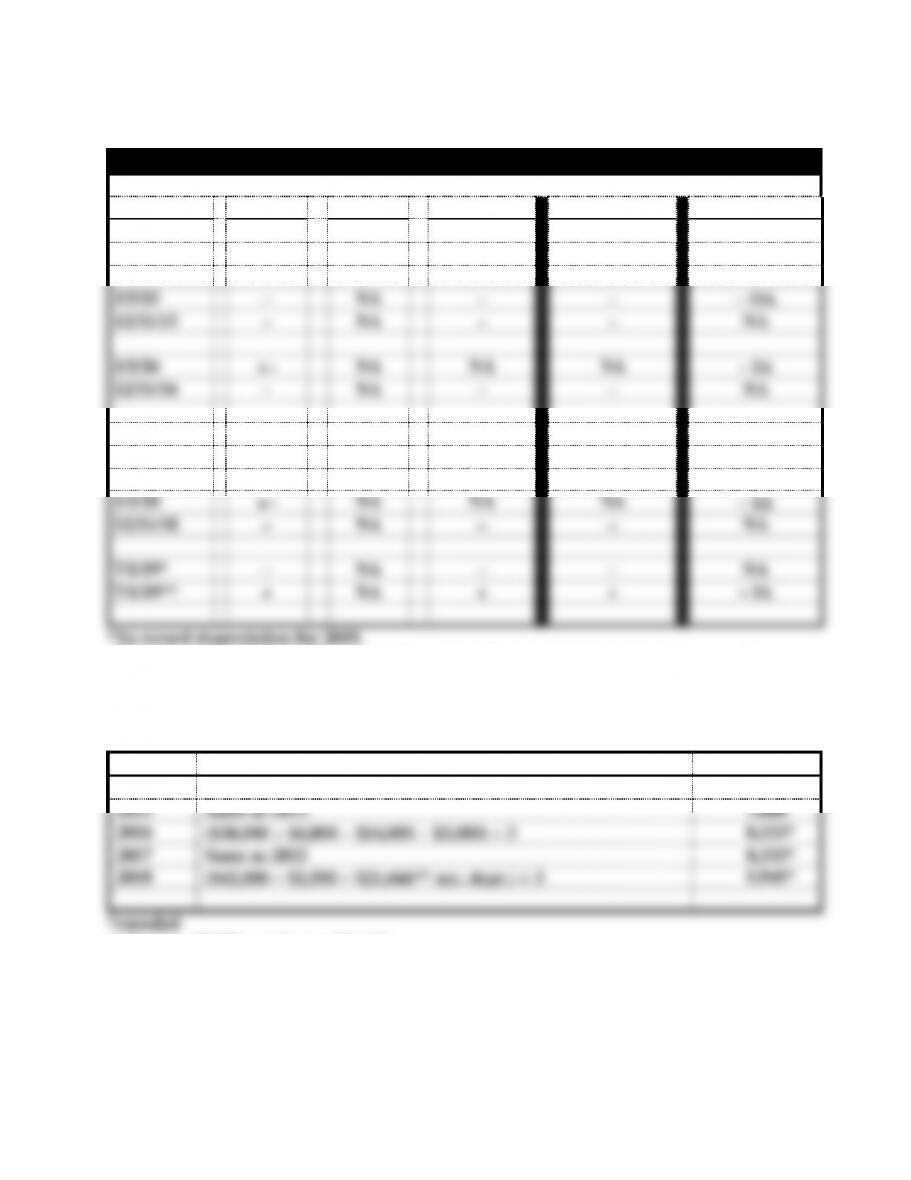

PROBLEM 6-29

a.

Horizontal Statements Model

Date

Assets

=

Liab.

+

Equity

Net Income

Cash Flows

1/1/14

+−

NA

NA

NA

− IA

12/31/14

−

NA

−

−

NA

5/5/15

−

NA

−

−

− OA

12/31/15

−

NA

−

−

NA

1/1/16

+−

NA

NA

NA

− IA

12/31/16

−

NA

−

−

NA

3/1/17

−

NA

−

−

− OA

12/31/17

−

NA

−

−

NA

1/1/18

+−

NA

NA

NA

− IA

12/31/18

−

NA

−

−

NA

7/1/19*

−

NA

−

−

NA

7/1/19**

+

NA

+

+

+ IA

*To record depreciation for 2019.

**To record sale of asset. The plus in the assets column represents the net increase in

assets resulting from the sale of the equipment. Cash increases by a greater amount than

the decrease in the book value of the equipment.

b.

Year

Computation

Depr. Exp.

2014

($38,000 − $3,000) 5

$7,000

2015

Same as 2013

7,000

2016

($38,000 + $4,000 − $14,000 − $3,000) 3

8,333*

2017

Same as 2015

8,333*

2018

($42,000 − $2,500 − $21,666** acc. depr.) 3

5,945*

**30,666 − $9,000 overhaul = $21,666

6-11

PROBLEM 6-29 (cont.)

c.

Computation of Book Value

Year

Cost

−

Acc. Depr.

=

Book Value

2014

$38,000

−

$7,000

=

$31,000

2015

38,000

−

14,000

=

24,000

2016

42,000

−

22,333

=

19,667

2017

42,000

−

30,666

=

11,334

2018

42,000

−

27,611*

=

14,389

*$30,666 − $9,000 overhaul + $5,945 depreciation expense.

d. Computation of Depreciation Expense for 2019:

$5,945 x 6/12 = $2,973

Book Value at Date of Sale: