ATC 14-1

a.

Budgeted

Financial Statements

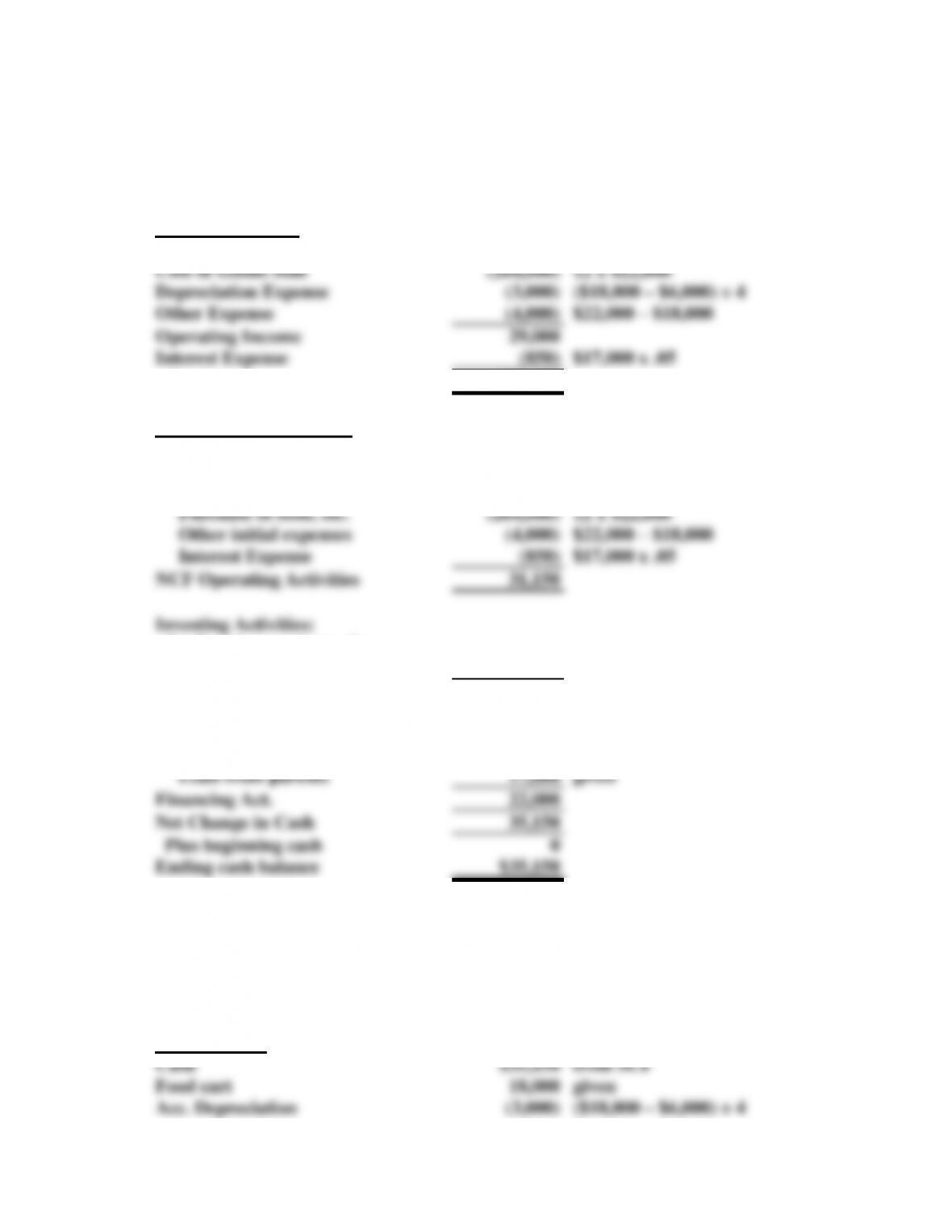

Income Statement

Amounts

Computations

Sales Revenue

$300,000

12 x $25,000

Cost of Goods Sold

(264,000)

12 x $22,000

Depreciation Expense

(3,000)

($18,000 – $6,000) ÷ 4

Other Expense

(4,000)

$22,000 – $18,000

Operating Income

29,000

Interest Expense

(850)

$17,000 x .05

Net Income

$28,150

Statement of Cash Flows

Operating Activities:

Inflows from sales

$300,000

12 x $25,000

Outflows for:

Purchase of food, etc.

(264,000)

12 x $22,000

Other initial expenses

(4,000)

$22,000 – $18,000

Interest Expense

(850)

$17,000 x .05

NCF Operating Activities

31,150

Investing Activities:

Outflow for purchase of

cart

(18,000)

given

Financing Activities”

Inflows from:

Contribution by owners

5,000

given

Loan from parents

17,000

given

Financing Act.

22,000

Net Change in Cash

35,150

Plus beginning cash

0

Ending cash balance

$35,150

ATC 14-1 (continued)

Budgeted

Financial Statements

continued

Balance Sheet

Amounts

Computations

Cash

$35,150

from SCF

Food cart

18,000

given

Acc. Depreciation

(3,000)

($18,000 – $6,000) ÷ 4

Total Assets

$50,150

Note Payable

$17,000

given

Contributed Capital

5,000

given

Retained Earn.

28,150

from Inc. Statement

Total Liab. & Equity

$50,150

b. The budget financial statements above assume sales for each month of the year will be

approximately equal to sales for September and October. Most likely, sales will be

pay their living expenses.

ATC 14-2

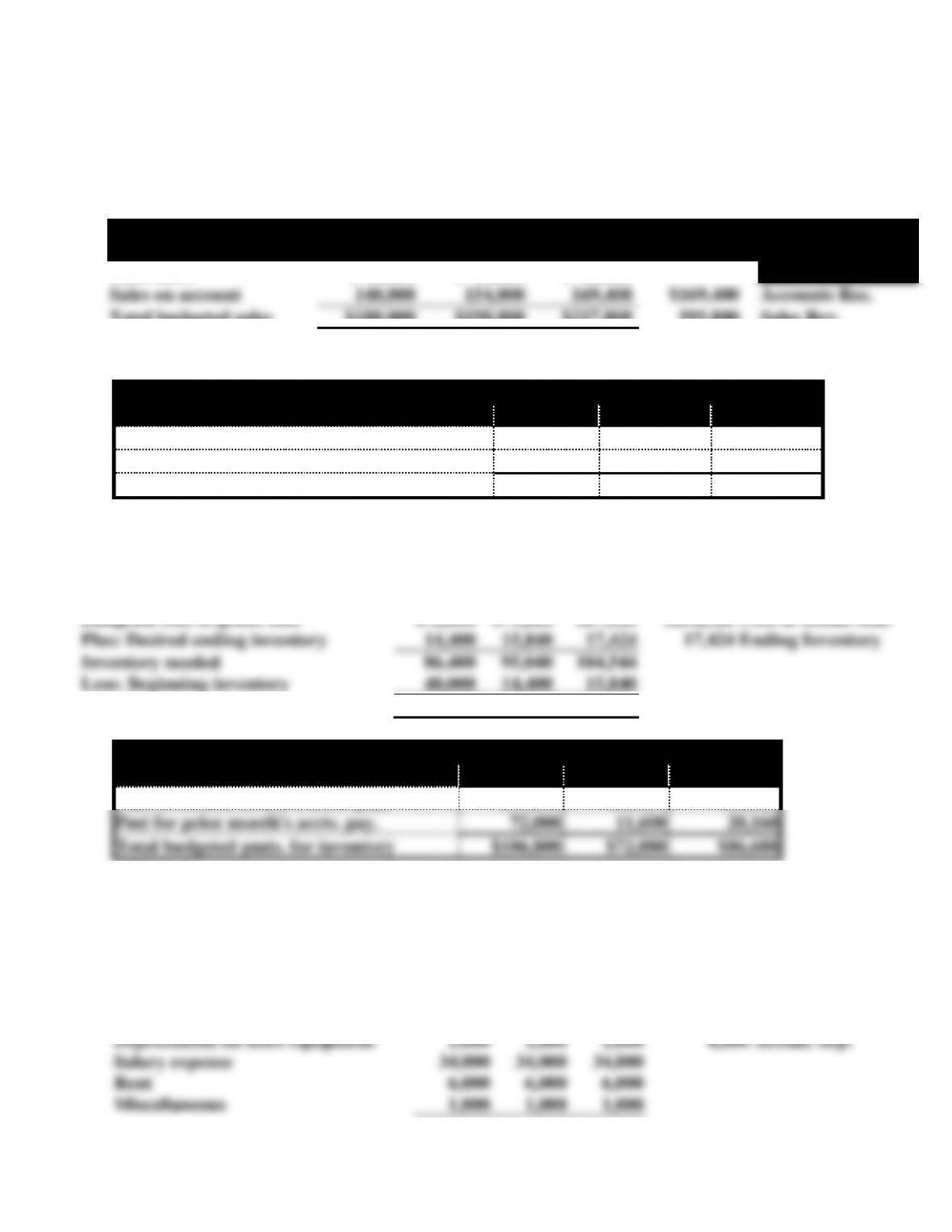

a. Group Tasks

Task 1

Pro Forma

October

November

December

Data

Cash sales

$ 40,000

$ 44,000

$ 48,400

Sales on account

140,000

154,000

169,400

$169,400

Accounts Rec.

Total budgeted sales

$180,000

$198,000

$217,800

595,800

Sales Rev.

Schedule of Cash Receipts

October

November

December

Cash sales

$ 40,000

$ 44,000

$ 48,400

Collections from accounts receivable

60,000

140,000

154,000

Total cash collections

$100,000

$184,000

$202,400

Task 2

Pro Forma

Oct.

Nov.

Dec.

Data

Budgeted cost of goods sold

$72,000

$79,200

$87,120

$238,320

Cost of Goods Sold

Plus: Desired ending inventory

14,400

15,840

17,424

17,424

Ending Inventory

Inventory needed

86,400

95,040

104,544

Less: Beginning inventory

40,000

14,400

15,840

Required purchases (on account)

$46,400

$80,640

$88,704

22,176

Accounts Payable

Schedule of Cash Payments Budget for Inventory Purchases

October

November

December

Pmt of current month’s accts. pay.

$34,800

$60,480

$66,528

Pmt for prior month’s accts. pay.

72,000

11,600

20,160

Total budgeted pmts. for inventory

$106,800

$72,080

$86,688

ATC 14-2

Task 3

Pro Forma

Oct.

Nov.

Dec.

Data

Sales commissions

$ 7,200

$ 7,920

$ 8,712

$ 8,712

Commissions pay.

Supplies expense

1,800

1,980

2,178

Utilities

2,200

2,200

2,200

2,200

Utility payable

Depreciation on store equipment

1,600

1,600

1,600

4,800

Accum. dep.

Salary expense

34,000

34,000

34,000

Rent

6,000

6,000

6,000

Miscellaneous

1,000

1,000

1,000

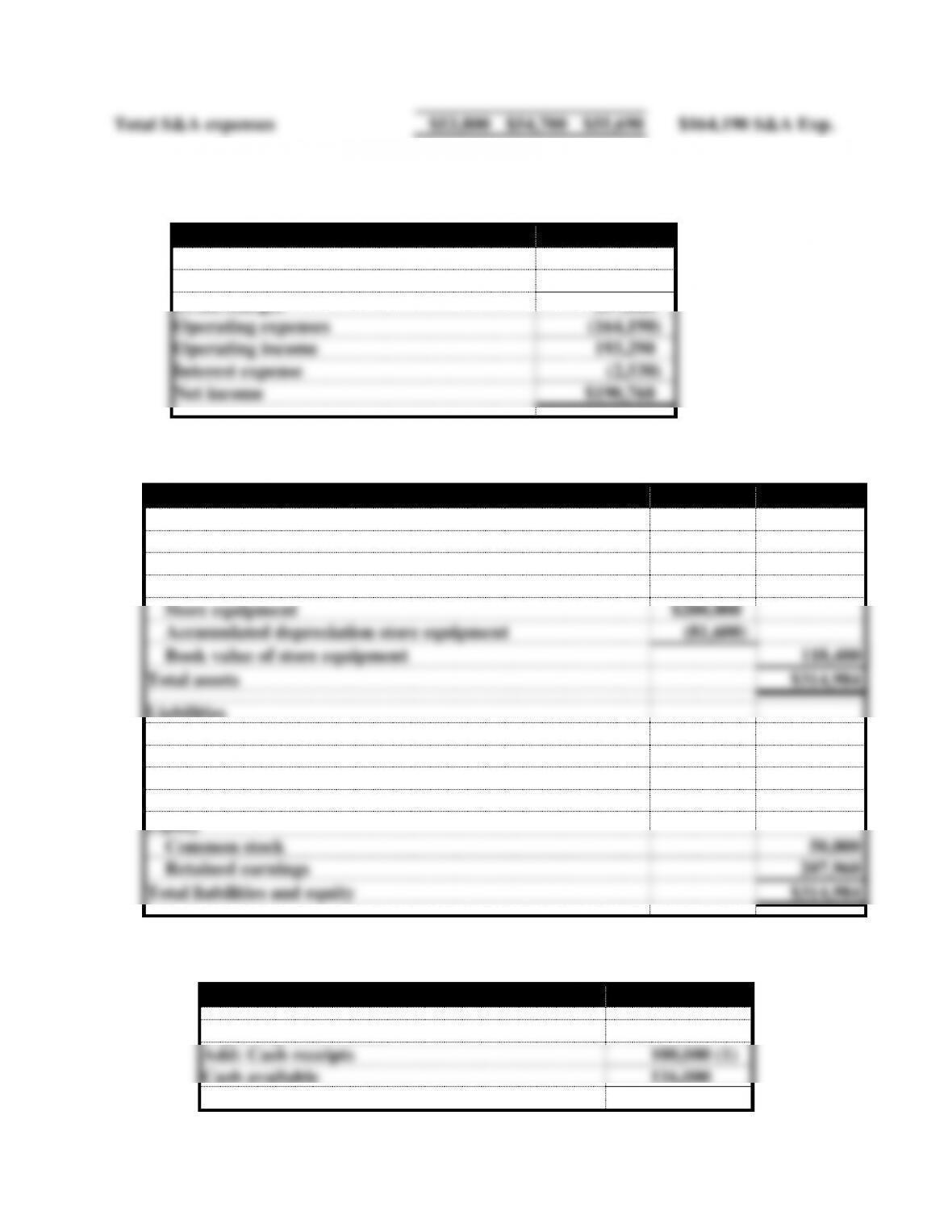

b. Financial Statements

Income Statement

Sales revenue

$595,800

Cost of goods sold

(238,320)

Gross margin

357,480

Operating expenses

(164,190)

Operating income

193,290

Interest expense

(2,530)

Net income

$190,760

ATC 14-2 (continued)

Balance Sheet

Assets

Cash

$ 9,760

Accounts receivable

169,400

Inventory

17,424

Store equipment

$200,000

Accumulated depreciation store equipment

(81,600)

Book value of store equipment

118,400

Total assets

$314,984

Liabilities

Accounts payable

$ 22,176

Utilities payable

2,200

Sales commissions payable

8,712

Line of credit

23,936

Equity

Common stock

50,000

Retained earnings

207,960

Total liabilities and equity

$314,984

c. Havel will need to borrow money in October.

Cash Budget for October

Beginning cash balance

$ 16,000

Add: Cash receipts

100,000 (1)

Cash available

116,000

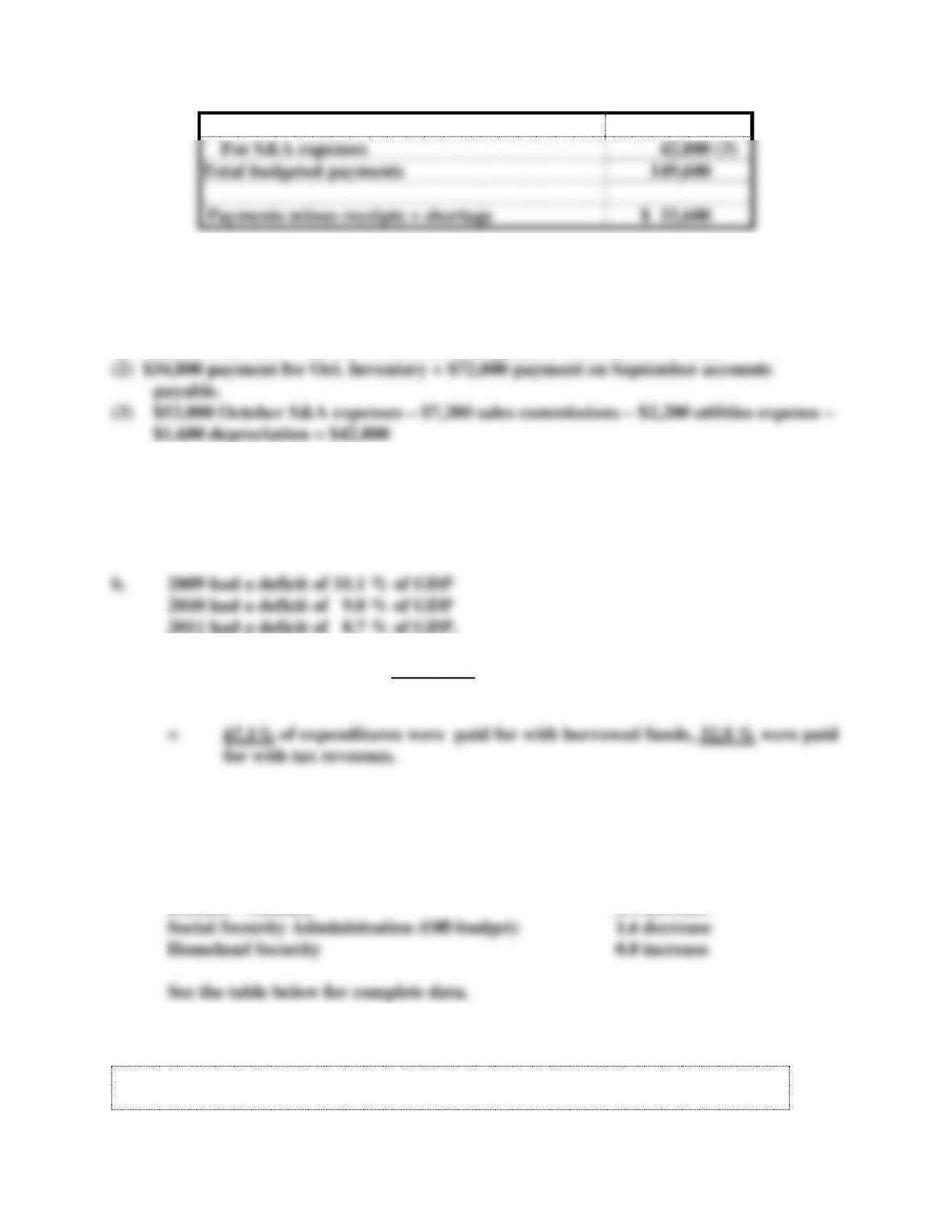

Less: Payments

Total S&A expenses

$53,800

$54,700

$55,690

$164,190

S&A Exp.

For inventory purchases

106,800 (2)

For S&A expenses

42,800 (3)

Total budgeted payments

149,600

Payments minus receipts = shortage

$ 33,600

ATC 14-2 (continued)

(1) $40,000 cash sales + $60,000 collection on September accounts receivable.

ATC 14-3

a. There was a budgeted surplus in 6 years of in the 53 years from 1960 to 2011: 1960,

1969, 1998, 1999, 2000, 2001. Thus, a deficit was reported in 47 years.

c. For 2009: Deficit $1,412,688

Receipts $2,104,989

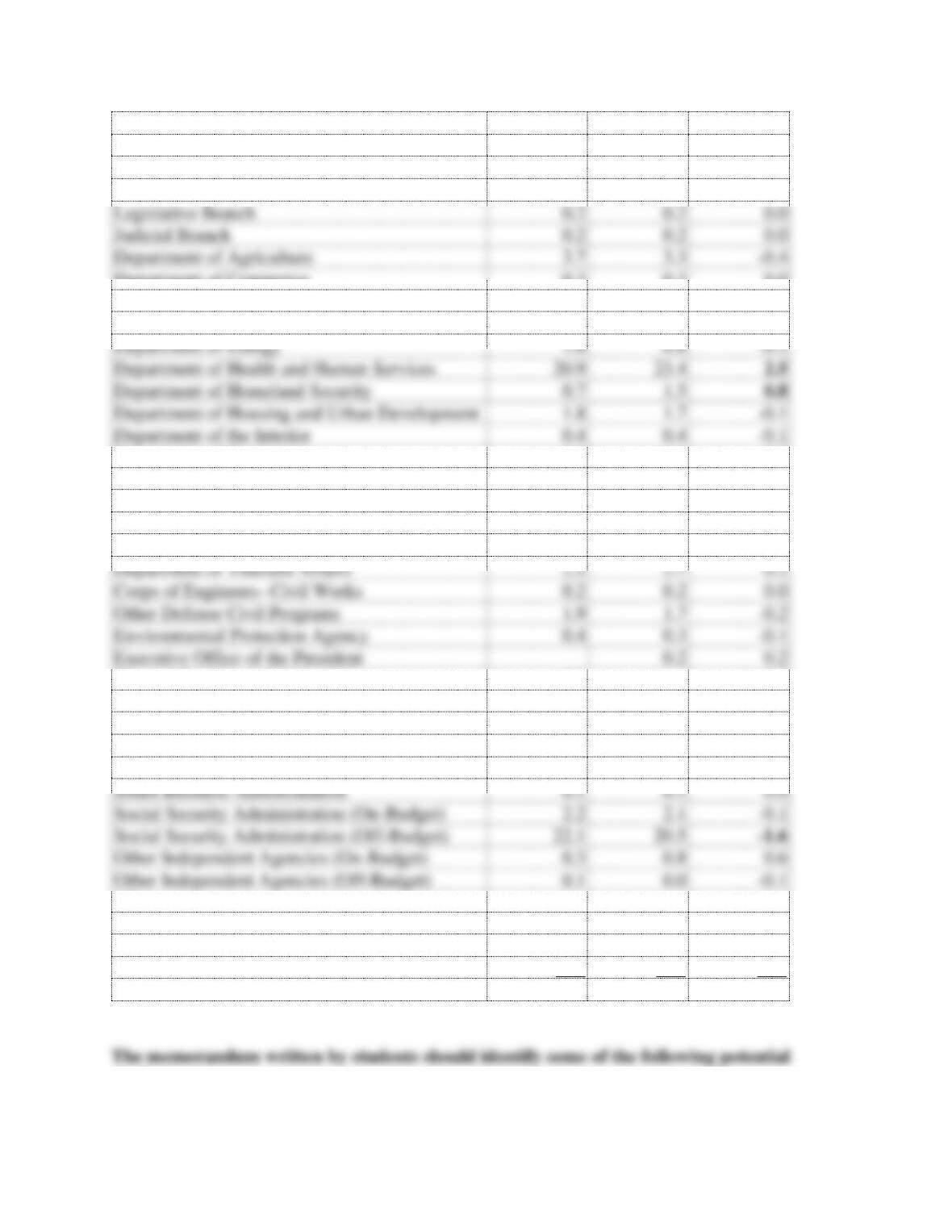

d. The departments whose budgets changed the most from the Clinton years to the

Bush years were:

Treasury 4.6 decrease

Health and Human Services 2.5 increase

Defense—Military 2.4 increase

ATC 14-3 continued

Comparison of Average Budget Percentages by Department for 1994 – 2001 (Clinton

Years) to 2002 – 2009 (Bush Years)

Average

Average

for

for

Clinton

Bush

Years

Years

Difference

Legislative Branch

0.2

0.2

0.0

Judicial Branch

0.2

0.2

0.0

Department of Agriculture

3.7

3.3

-0.4

Department of Commerce

0.3

0.3

0.0

Department of Defense—Military Programs

16.2

18.6

2.4

Department of Education

1.9

2.5

0.6

Department of Energy

1.0

0.8

-0.2

Department of Health and Human Services

20.9

23.4

2.5

Department of Homeland Security

0.7

1.5

0.8

Department of Housing and Urban Development

1.8

1.7

-0.1

Department of the Interior

0.4

0.4

-0.1

Department of Justice

0.8

1.0

0.2

Department of Labor

2.1

2.5

0.4

Department of State

0.4

0.5

0.1

Department of Transportation

2.3

2.4

0.0

Department of the Treasury

22.4

17.8

-4.6

Department of Veterans Affairs

2.5

2.7

0.2

Corps of Engineers—Civil Works

0.2

0.2

0.0

Other Defense Civil Programs

1.9

1.7

-0.2

Environmental Protection Agency

0.4

0.3

-0.1

Executive Office of the President

0.2

0.2

General Services Administration

0.1

-0.1

International Assistance Programs

0.6

0.5

-0.1

National Aeronautics and Space Administration

0.9

0.6

-0.2

National Science Foundation

0.2

0.2

0.0

Office of Personnel Management

2.7

2.4

-0.4

Small Business Administration

0.1

0.1

0.0

Social Security Administration (On-Budget)

2.2

2.1

-0.1

Social Security Administration (Off-Budget)

22.1

20.5

-1.6

Other Independent Agencies (On-Budget)

0.3

0.8

0.6

Other Independent Agencies (Off-Budget)

0.1

0.0

-0.1

Allowances

Undistributed Offsetting Receipts

-9.4

-9.2

0.1

(On-budget)

-6.2

-5.0

1.2

(Off-budget)

-3.2

-4.2

-1.0

Total outlays

100.0

100.0

0.0

ATC 14-4

challenges.

competition to be held in a given year.

• Many of the USOC’s revenues are not correlated with activities that cause it to

incur expenses, as is the case with business enterprises. Thus, just because revenues

are down it does not mean that expenses will also decline.

• Any grants from government sources may be affected by politics.

• Games may be disrupted by international events over which the USOC has no

control or event the ability to predict. These events can reduce revenue

unexpectedly.

ATC 14-5

a. Mr. Cleaver’s behavior could be construed to be in violation of the objectivity

standards. The failure to disclose the lack of need for computers to the Board of

Education would violate (1) the standard to communicate information fairly and

objectively and (2) the standard to disclose fully all relevant information that could

b. As its name implies, participative budgeting encourages participation by

subordinates as well as upper level managers in the budget process. Information