Chapter 15 – Performance Evaluation

15-1

Teaching Notes for Chapter 15

This chapter begins with the fundamental concepts underlying responsibility accounting

and also provides students with a minimal explanation of flexible budgeting and variance

analysis. Students need to know that managers prepare static budgets based on the

planned volume of activity at the beginning of an accounting period. On the other hand,

managers prepare flexible budgets based on the actual volume of activity at the end of the

accounting period. Further, students will need to know the following rules for variance

analysis:

With respect to revenue, managers want the actual amount to be greater than the standard

amount. The description of revenue variances is:

When: Actual Sales > Expected (Standard) Sales, the Variance is Favorable.

When: Actual Sales < Expected (Standard) Sales, the Variance is Unfavorable.

With respect to costs, managers want the actual amount to be less than the standard amount.

The description of cost variances is:

When: Actual Costs > Expected (Standard) Costs, the Variance is Unfavorable.

When: Actual Costs < Expected (Standard) Costs, the Variance is Favorable.

You can use Exercise 15-4 as a demonstration problem on variances and Exercise15-5 as

a homework assignment to provide students the background they need to understand this

concept.

Detailed Outline of a Lesson Plan for Chapter 15

I. Introduce the concept of decentralization and the primary features of

responsibility accounting. The fundamental concepts underlying responsibility

accounting are easy to grasp. Most students can learn these basics through a

reading assignment. Assign the material from the beginning of the chapter

(approximately the first six pages) as an advance reading requirement. We

recognize that many students fail to read ahead. In fact, we teach most of our

classes assuming that students read after instead of before class. For this chapter,

we motivate students to read ahead by advising them that the first class on the

topic begins with a group exercise for which they must have read the assigned

materials. If you believe that your students will not complete the advance reading

assignment, develop a brief lecture to introduce the primary features of

responsibility accounting.

II. Distribute Demonstration Problem 15-1 and have students complete the

requirements as a group. Ask each group to choose a spokesperson. Have two

or three of the groups place their organization charts on the board. Use the charts

to stimulate a general discussion that leads to the development of a reasonable

Chapter 15 – Performance Evaluation

15-2

solution to the requirements. You can assign Exercise 15-1 as a follow up

homework assignment.

III. Work Demonstration Problem 15-2 as an in-class group learning experience.

Distribute the work paper for the problem. Have students individually complete

the missing information and compare their answers with the members of their

group. Call out or display the answers so students can check their work. Based on

time available, use Exercises 15-4 and 15-5 as in-class reinforcement or as

homework assignments.

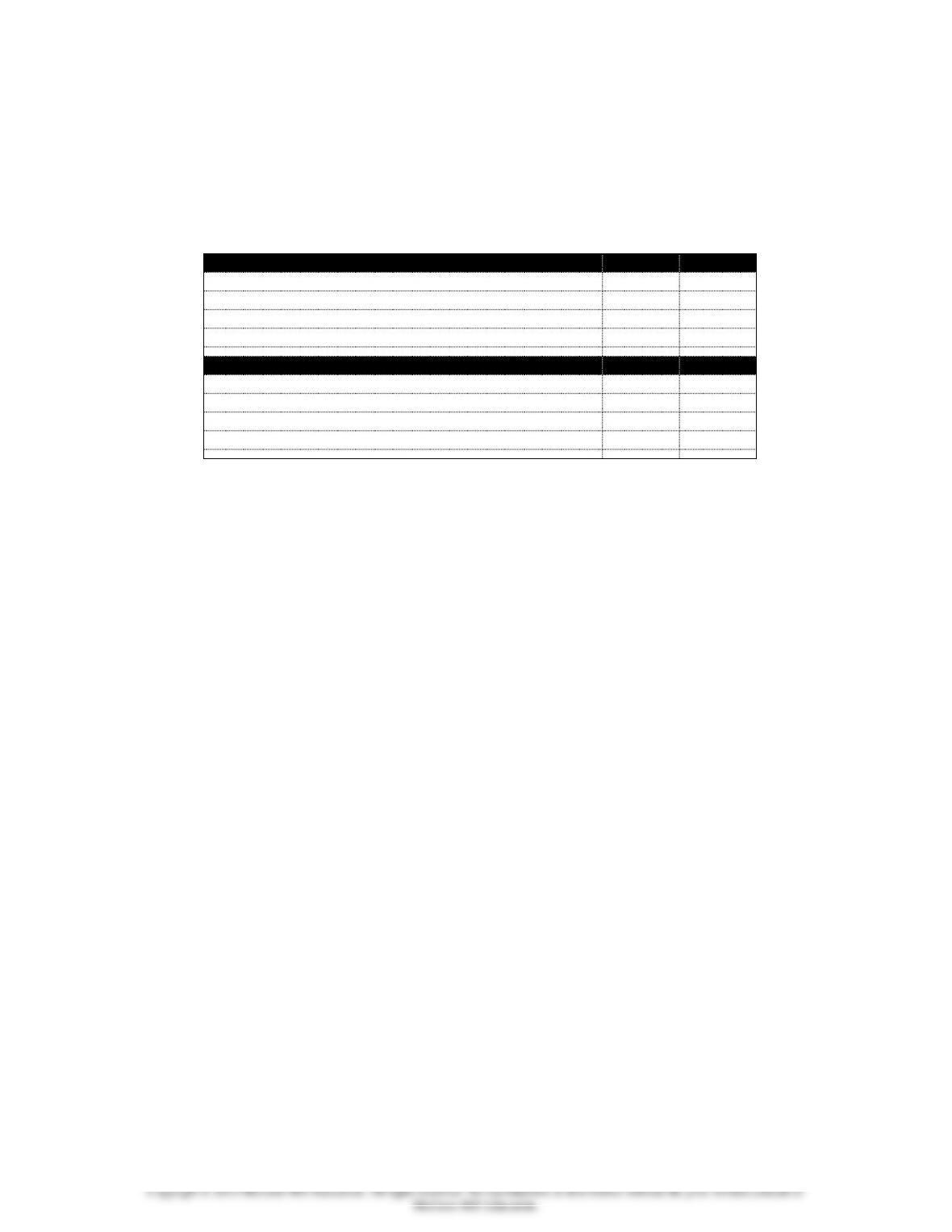

IV. Define the terms static budget and flexible budget and show students how to

calculate sales and variable cost volume variances and flexible budget

variances.

A. A static budget is based on standard prices and costs multiplied by the

expected (standard) volume of activity (planned number of units of product).

The master budget discussed in the previous chapter is a static budget.

B. A flexible budget is based on standard prices and costs multiplied by the

actual volume of activity (actual number of units of product).

C. The actual result is obtained by multiplying actual prices and costs by the

actual volume of activity (actual number of units of product).

D. The volume (activity) variance is the difference between the static budget and

the flexible budget.

E. The flexible budget variance is the difference between the flexible budget and

the actual results.

F. The variances described above can be summarized in a chart as follows:

Static Budget

Flexible Budget

Actual Result

Standard Prices and

Costs

Standard Prices and

Costs

Actual Prices and

Costs

X

X

X

Expected (Standard)

Units

Actual Units

Actual Units

Volume Variance

Flexible Budget Variance

V. Work Demonstration Problem 15-3 to illustrate computing volume and

flexible budget variances. Work this problem in a style that keeps students

actively involved. For example, students should be able to begin work on

requirement a without prior instruction. Distribute the problem and work papers

and let them get started on their own. Circulate around the room, answer

questions, and offer assistance to those having trouble. If many students are

having trouble, interrupt the class and provide general instruction. As the faster

students begin to finish requirement a, have them move forward to requirement

b. Again, provide general instruction based on class needs.

Chapter 15 – Performance Evaluation

15-3

VI. Use any of the exercises from 15-6 through 15-10 as in-class reinforcement or

as homework. You can also assign Problems 15-19 through 15-21 as

homework.

VII. Use Demonstration Problem 15-4 to reinforce the variance analysis concepts.

This problem integrates responsibility accounting concepts with a brief

introduction to flexible budgeting and variance analysis.

VIII. Show students how to compute return on investment with the summary

formula (Operating income ÷ Operating assets). Distribute Demonstration

Problem 15-5 and have students complete requirement a. Circulate around the

room helping students understand how to calculate ROI. Ask them if a higher or

lower ROI suggests better performance. Comparing ROI with interest earned on

a savings account is a good way to give students a feel for what ROI means.

IX. Show the class how the summary ROI formula can be subdivided into two

separate ratios, margin and turnover. Describe the useful information

managers gain by analyzing the separate components. Use requirement b of

Demonstration Problem 15-5 as an in-class exercise to give students practice

computing margin and turnover, and to illustrate how these measures can provide

information to improve managerial performance. Ask your students to explain the

meaning of margin and turnover.

X. Use requirement c of Demonstration Problem 15-5 as a problem-based

learning exercise. Have students complete the requirement before you introduce

the concept of suboptimization. Let them develop solutions in their groups.

Some groups are likely to recommend accepting the investment opportunity

because its ROI exceeds the company’s average ROI. Other groups are likely to

recognize that the additional investment will reduce the Hydride Division’s

average ROI to a point that is below NiCad’s ROI. A class discussion of the

various group findings will reveal that the additional investment will increase the

company’s overall ROI but will harm the performance evaluation of Hydride’s

manager. Now introduce the term suboptimization. This requirement provides a

great segue for introducing the residual income performance measure.

XI. Show how top management can use residual income to overcome the

suboptimization problem inherent in using ROI to evaluate performance.

Use requirement d of Demonstration Problem 15-5 to illustrate how to compute

residual income. Explain the impact of using residual income on the decision of

whether to accept the additional investment.

XII. You can use Exercise 15-16 as an in-class reinforcement exercise to give

students practice computing ROI and RI. Use Problem 15-23 as a homework

assignment covering ROI and RI.

Chapter 15 – Performance Evaluation

15-4

Summary Outline of a Lesson Plan for Chapter 15

I. Introduce the concept of decentralization and the primary features of

responsibility accounting.

II. Distribute Demonstration Problem 15-1 and have students complete the

requirements as a group. Have group spokespersons put organization charts on

the board to stimulate discussion. Assign Exercise 15-1 or Problem 15-18 as

homework.

III. Work Demonstration Problem 15-2 as an in-class group learning experience.

Use Exercises 15-4, 15-5, or 15-6 as in-class reinforcement or as homework

assignments.

IV. Define the terms static budget and flexible budget and show students how to

calculate volume (activity) variances and flexible budget variances.

Static Budget

Flexible Budget

Actual Result

Standard Prices and

Costs

Standard Prices and

Costs

Actual Prices and

Costs

X

X

X

Expected (Standard)

Units

Actual Units

Actual Units

Volume (Activity) Variance

Flexible Budget Variance

V. Work Demonstration Problem 15-3 to illustrate computing volume (activity)

and flexible budget variances. Keep students actively involved, having them

work on each requirement as you circulate around the room.

VI. Use any of the exercises from 15-8 through 15-10 as in-class reinforcement or

as homework. You can also assign Problems 15-19 or 15-21 as homework.

VII. Use Demonstration Problem 15-4 to reinforce the variance analysis concepts.

VIII. Show students how to compute return on investment with the summary

formula (Operating income ÷ Operating assets). Compare ROI with interest

earned on a savings account. Distribute Demonstration Problem 15-5 and have

students complete requirement a, circulating to help as needed.

Chapter 15 – Performance Evaluation

15-5

IX. Show the class how the summary ROI formula can be subdivided into two

separate ratios, margin and turnover. Describe the useful information

provided by analyzing the separate components. Use requirement b of

Demonstration Problem 15-5 as an in-class exercise.

X. Use requirement c of Demonstration Problem 15-5 as a problem-based

learning exercise. Have students work the requirement first and then introduce

the concept of suboptimization.

XI. Show how top management can use residual income to overcome the

suboptimization problem inherent in using ROI to evaluate performance.

Use requirement d of Demonstration Problem 15-5 to illustrate how to compute

residual income. Explain the impact that using residual income has on the

decision.

XII. Use Exercise 15-16 as an in-class reinforcement exercise to give students

practice computing ROI and RI. Use Problem 15-23 as a homework

assignment covering ROI and RI.

Quiz Questions for Chapter 15

1. Which of the following is NOT considered an advantage of decentralization?

a. Decentralization often improves the quality of decision making by delegation of authority.

2. A cost center

a. incurs expenses, earns revenue, and is evaluated using return on investment.

b. needs no managerial control or supervision.

c. should be eliminated to increase profit.

d. incurs expenses and earns no revenue.

3. Which of the following would improve a firm’s return on investment?

a. Raising sales prices and incurring higher expenses.

b. Increasing earnings and investment in assets.

c. Lowering sales prices and increasing asset investment.

d. A decrease in expenses with no effect on revenues or the investment in assets.

4. Which of the following statements is false? An investment center

a. may develop its own long-term investment strategy.

b. is responsible for revenues but not expenses.

c. has many of the characteristics of an independent business.

d. may purchase long-term assets.

Use the following information to answer the next two questions: National’s cost accountant prepared

the following static budget based on expected activity of 2,000 units for the 2014 accounting period:

Sales Revenue $64,000

Chapter 15 – Performance Evaluation

15-6

Variable Costs (34,000)

Contribution Margin 30,000

Fixed Costs (18,000)

Net Income $12,000

5. If National actually produced 1,800 units, the flexible budget would show variable costs of

a. $34,000.

b. $22,666.

c. $30,600.

d. $25,500.

6. If National actually produced 1,900 units, the flexible budget would show fixed costs amounting to

a. $19,800.

b. $18,000.

c. $52,000.

d. none of the above.

Use the following information to answer the next two questions: Cox Manufacturing Company

prepared the following static budget income statement for 2014:

Sales Revenue $125,000

Variable Costs (75,000)

Contribution Margin 50,000

Fixed Cost (30,000)

Net Income $ 20,000

The budget was based on an expected sales volume of 5,000 units. Actual sales volume was 6,000 units.

7. The amount of net income based on a flexible budget of 6,000 units is expected to be

a. $24,000.

b. $26,000.

c. $30,000.

d. $45,000.

8. The sales revenue volume variance is

a. $25,000 favorable.

b. $10,000 unfavorable.

c. $4,000 unfavorable.

d. $6,000 favorable.

9. Marjorie Jewels, a maker of fashionable rings, produced and sold 6,000 rings during the recent

accounting period. The company had expected to sell 5,600 rings. Because of competition, the

company priced the rings at $20 each, $2 lower than the budgeted selling price. Based on this

information, there is

a. a favorable $8,000 sales volume variance.

b. an unfavorable $800 total sales variance.

c. an unfavorable sales price variance.

d. all of the above.

10. Which employees would most likely be held responsible for a volume variance?

a. production workers

b. marketing managers

c. purchasing agents

d. production managers

15-7

11. If the planned or expected level of activity is overstated (unreasonably high), what consequence is

likely?

a. The predetermined overhead rate will be overstated.

b. Products are likely to be underpriced.

c. Products are likely to be overpriced.

d. Per unit variable overhead costs are understated.

12. Last year, Thurco Corporation had revenues of $120,000 and expenses of $70,000. If Thurco had

$500,000 of operating assets last year, what was Thurco’s return on investment?

a. 10%

b. 15%

c. 20%

d. 16.7%

13. Last year, Thurco Corporation had revenues of $120,000 and expenses of $70,000. If Thurco had

$500,000 of operating assets last year, what was Thurco’s margin?

a. 16.6%

b. 22.2%

c. 33.3%

d. 41.7%

14. Last year, Thurco Corporation had revenues of $120,000 and expenses of $70,000. If Thurco had

$500,000 of operating assets last year, what was Thurco’s turnover?

a. .48

b. .24

c. .16

d. .40

15. LINK, Inc. has a margin of 3.5 % and a turnover of 4. What is LINK’s return on investment?

a. 10%

b. 14%

c. 88%

d. 7.5%

16. Maxwell Company established a center to provide its employee training seminars. Maxwell budgeted

costs for a weekend training seminar for managers at $300 per employee. Actual costs were $315 per

employee. The training center would be considered a (an)

a. asset center.

b. profit center.

c. cost center.

d. investment center.

17. Which of the following statements about ROI is true?

a. Using ROI avoids conflicts of interest between a department and the business as a whole.

b. ROI cannot be used to measure performance for investment centers.

c. ROI can be calculated by multiplying margin by turnover.

d. ROI is equal to net income divided by sales.

18. The management strategy that focuses on significant variances is called

a. decentralized management.

b. management by exception.

c. profit management.

d. centralized management.

Chapter 15 – Performance Evaluation

15-8

19. Kennedy Aeronautics desires an 8% ROI on all investment projects. Details of a proposed investment

include the following:

Sales Revenues $30,000

Expenses 27,000

Investment Turnover 1.5

Which of the following statements is accurate?

a. Based on ROI, the company should accept the investment project.

b. The investment project would have a 10% return.

c. The company should reject the investment project.

d. The company’s margin is 14.3%.

20. The management of Dakota Industries obtained the following information about the performance of a

major investment project.

Revenues $200,000

Average Operating Assets 300,000

Net Operating Income 30,000

Desired ROI 10%

The project’s residual income was

a. $30,000.

b. $10,000.

c. $0.

d. 10%.

21. The accounting records pertaining to a Cassidy Products investment project were recently destroyed by

fire. The company accountant was able to recall the following information:

Desired ROI 12%

Net Income $260,000

Residual Income $20,000

Based on this information, how much is the company’s investment in the project?

a. $225,000

b. $2,000,000

c. $1,460,000

d. $1,875,000

Solutions to Quiz Questions

Question

Answer

1

B

2

D

3

D

4

B

5

C

6

B

7

C

8

A

Chapter 15 – Performance Evaluation

15-9

9

C

10

B

11

B

12

A

13

D

14

B

15

B

16

C

17

C

18

B

19

A

20

C

21

B

Demonstration Problems for Chapter 15

Demonstration Problem 15-1

Organization Chart and Responsibility Centers

LiPari Personnel Services Company has two operating divisions. The Clerical Services

division places (finds jobs for) people who have clerical skills; the Computer Services

division places individuals who have computer programming skills. A secretarial labor

pool provides support to both divisions. Each of the two operating divisions has an

Employee Search department that locates individuals seeking jobs and a Client Services

department that identifies and serves companies seeking employees. LiPari has a chief

executive officer (CEO) and a vice-president of operations. The vice-president of

operations reports to the CEO and the managers of the two operating divisions report to

the vice-president. LiPari also employs an administrative manager. The manager of the

secretarial labor pool and an advertising manager report to the administrative manager,

who reports to the CEO.

Required

a. Develop an organization chart that shows reasonable lines of authority for the

primary responsibility centers of the LiPari Personnel Services Company.

b. Classify the responsibility centers shown on your organization chart as cost centers,

profit centers, or investment centers.

c. Would you expect the CEO to know if the advertising manager is paying too much

for radio advertising? Explain. Include a discussion of the decentralization concept.

Demonstration Problem 15-2 Character of Variances

Required

Chapter 15 – Performance Evaluation

15–10

Compute variances for the items shown in the following list and indicate whether each

variance is favorable (F) or unfavorable (UF).

Item

Budget

Actual

Variance

F or UF

Selling and Administrative Expenses

$ 29,000

$ 27,000

Sales Revenue

$310,000

$325,000

Materials Price

$2.00 per lb.

$2.10 per lb.

Cost of Goods Sold

$125,000

$100,000

Materials Purchases

$250,000

$265,000

Materials Usage

6,000 lbs.

5,800 lbs.

Sales Price

$550 each

$500 each

Labor Rate

$8.10 per hour

$7.95 per hour

Production Volume

950 units

900 units

Labor Usage

$96,000

$97,000

Research and Development Expense

$22,000

$25,000

Demonstration Problem 15-3 Sales Volume (Activity) and

Flexible Budget Variances

The following data apply to chairs made by the Western Chair Company.

Price and Variable Costs Per Unit:

Standard

Actual

Sales Price

$62.00

$60.00

Direct Materials Cost

16.00

16.34

Direct Labor Cost

12.00

10.92

Overhead Cost

14.00

14.20

General, Selling, and Administrative (G,S,&A) Cost

8.00

7.00

Expected Fixed Costs:

Manufacturing

$120,400

$114,000

General, Selling, and Administrative

67,000

69,000

Western planned to make and sell 43,000 chairs. It actually produced and sold 44,000

chairs.

Required

a. Prepare a pro forma income statement based on the static budget.

b. Prepare a pro forma income statement based on a flexible budget and compute the

volume (activity) variances. Indicate whether the variances are favorable or

unfavorable and speculate as to what management position would be held responsible

for each variance.

c. Prepare an income statement that shows the actual results, and compute the flexible

budget variances. Indicate whether the variances are favorable or unfavorable and

Chapter 15 – Performance Evaluation

15–11

speculate as to what management position would be held responsible for each

variance.

Demonstration Problem 15-4 Variances and Responsibility

Sweeney Company’s 2014 responsibility accounting report includes the following:

Per Unit Variable Costs:

Standard

Actual

Materials Cost

$22.00

$21.80

Customer Delivery Cost

1.90

1.95

Inspection Cost

1.20

1.16

Sales Commissions

4.00

4.20

Fixed Costs:

Manufacturing

$720,000

$708,000

Advertising

107,000

120,000

Financial Statement Software Costs

15,600

18,000

Product Liability Cost

45,400

17,900

Actual volume of production and sales was 90,000 units.

Required

a. Determine the amount of the variances for the above costs and indicate whether each

variance is favorable or unfavorable.

b. Speculate as to the management position that would be held responsible for (able to

explain) each variance.

Demonstration Problem 15-5 ROI and Residual Income

The Hydride Division of Murdoch Corporation is an investment center. It has $4,000,000

of operating assets. During 2014, the Hydride Division earned operating income of

$720,000 on $12,000,000 of sales. Murdoch’s companywide return on investment (ROI)

is approximately 14%.

Required

a. Compute the ROI for the Hydride Division.

b. Calculate the two ratios into which ROI can be subdivided, margin and turnover, for

the Hydride Division. What useful information can management gain by analyzing

these two performance measures?

c. Assume Murdoch uses ROI to rank managerial performance. The Hydride Division

has the highest ROI in the company. Hydride’s nearest internal competitor is the

NiCad Division, which has an average ROI of 17%. Murdoch needs to invest excess

capital. The manager of the Hydride Division has the opportunity to expand existing

capacity by investing an additional $4,000,000 in machinery. The expected ROI for

the machinery investment is 15%. Should Hydride’s manager accept or reject the

investment opportunity? Why?