Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 15 Performance Evaluation

15-1

Answers to questions

1. People, not budgets, control costs. Ms. Kelly needs to use the budget system to build

maintain the desired control.

2. A responsibility center is the point in an organization where the control over

revenue or expense items is located.

3. The three types of responsibility centers are:

(1) cost centers,

Cost centers exist where a business segment incurs costs but does not generate

4. A static budget is based on the expected or planned volume of activity. An example

of a static budget would be the master budget prepared for planning purposes.

Flexible budgets differ from static budgets in that they show the estimated amount

they have control and would be reasonable measures of performance.

5. Mr. Smith is assessing his performance based on a comparison between a static

budget and actual results. Since a static budget is based on the planned level of

6. Sales variances are favorable when actual sales are greater than planned sales and

are unfavorable when actual sales are less than planned sales. Cost variances are

Chapter 15 Performance Evaluation

15-2

7. Many circumstances at the production level could affect Joan’s sales. Low quality

control in the production process could lead to lower quality goods that are difficult

variances can substantiate who is responsible for poor sales performance.

8. To determine volume variances a static budget based on planned volume is

compared to a flexible budget based on actual volume. When actual volume is

greater, variable costs are planned to be greater under the flexible budget. Variable

concern.

9. Sales revenues could increase because of either an increase in sales volume or an

increase in the sales price. The increase in sales volume could have resulted from

the actions of the marketing manager or could have resulted from circumstances or

10. The amount of fixed costs will remain the same under planned or actual volume.

Based on this cost behavior when actual volume is greater than planned, there will

11. Flexible budget variances are determined by taking the difference between flexible

budget amounts (based on standard per unit costs and actual volume) and actual

Chapter 15 Performance Evaluation

15-3

12. To determine if the marketing department’s variances are favorable or unfavorable

overall, the combination of variances requires analysis. The magnitude of the price

variance versus the magnitude of the volume variance would have to be compared. If the

13. Variance reports show variances from standard or expected amounts. Managers

14. It is possible for a manager with a lower return on investment (ROI) to be

outperforming a manager with a higher ROI. Many factors such as work stoppage,

15. The factors that affect the computation of return on investment are: (1) Margin;

Net income/Sales and (2) Turnover; Sales/Investment.

16. The return on investment can be increased by:

(1) increasing sales,

17. A manager is rewarded for an investment that returns an amount in excess of the

company’s desired rate of return under the residual income method. Accordingly,

18. The manager with the highest residual income is not always the best performer.

Managers with larger investments will naturally have higher residual incomes.

Exercise 15-1

Chapter 15 Performance Evaluation

15-4

a. Individual stores of Besant Toys Corporation are profit centers because their

responsibility is mainly to sell products provided by the headquarters for the

b. A balanced scorecard includes both financial and nonfinancial measures. While

return on sales is a good measure for the performance evaluation of individual

light on this particular aspect of store performance.

Employee turnover measures whether store staff members are happy and willing to

continue working for the company. If turnover is high, the store cannot provide

good customer service because employees do not plan to stay with the store for the

performances.

Exercise 15-2

Price/Cost

per Unit

a.

Master

Budget

2,000 Units

b.

Flexible

Budget

2,200 Units

Sales

$10.00

$20,000

$22,000

Variable manufacturing

$6.00

(12,000)

(13,200)

Contribution margin

8,000

8,800

Fixed manufacturing

(3,000)

(3,000)

Fixed selling and admin.

(1,000)

(1,000)

Net income

$ 4,000

$ 4,800

Exercise 15-3

Flexible

Budget

40,000 Hours

Flexible

Budget

45,000 Hours

Flexible

Budget

50,000 Hours

Sales ($160/hr)

$6,400,000

$7,200,000

$8,000,000

Variable costs ($60/hr)

(2,400,000)

(2,700,000)

(3,000,000)

Contribution margin

4,000,000

4,500,000

5,000,000

Chapter 15 Performance Evaluation

15-5

Fixed costs

1,800,000

1,800,000

1,800,000

Net income

$2,200,000

$2,700,000

$3,200,000

Exercise 15-4

Item to Classify

Standard

Actual

Type of

Variance

Sales volume

40,000 units

42,000 units

Favorable

Sales price

$3.60 per unit

$3.63 per unit

Favorable

Materials cost

$2.90 per pound

$3.00 per pound

Unfavorable

Materials usage

91,000 pounds

90,000 pounds

Favorable

Labor cost

$10.00 per hour

$9.60 per hour

Favorable

Labor usage

61,000 hours

61,800 hours

Unfavorable

Fixed cost spending

$400,000

$390,000

Favorable

Fixed cost per unit (volume)

$3.20 per unit

$3.16 per unit

Favorable

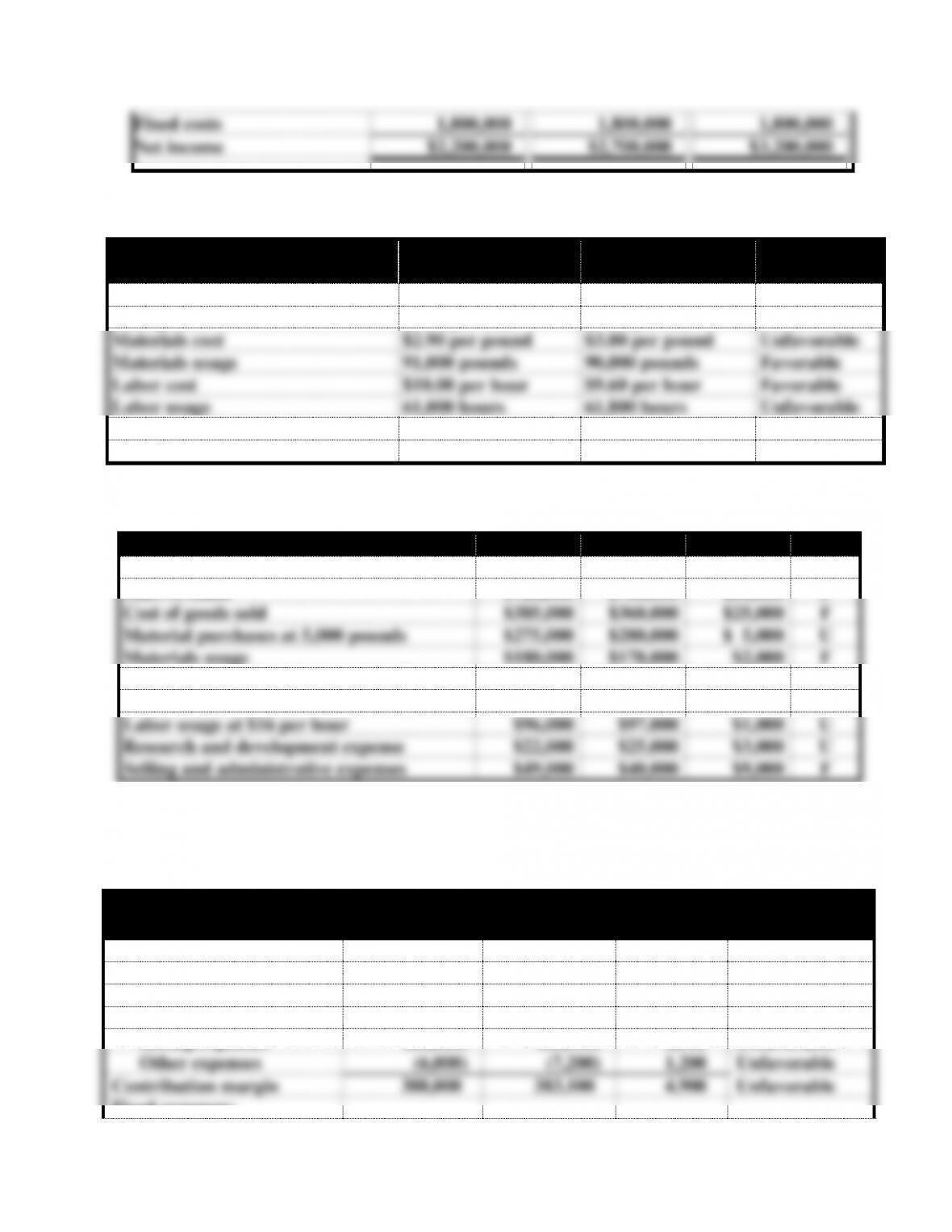

Exercise 15-5

Item

Budget

Actual

Variance

F or U

Sales price

$800

$780

$20

U

Sales revenue

$720,000

$780,000

$60,000

F

Cost of goods sold

$385,000

$360,000

$25,000

F

Material purchases at 5,000 pounds

$275,000

$280,000

$ 5,000

U

Materials usage

$180,000

$178,000

$2,000

F

Production volume

950 units

900 units

50 units

U

Wages at 4,000 hours

$60,000

$58,700

$1,300

F

Labor usage at $16 per hour

$96,000

$97,000

$1,000

U

Research and development expense

$22,000

$25,000

$3,000

U

Selling and administrative expenses

$49,000

$40,000

$9,000

F

Exercise 15-6

a. & b.

Titov Company

Internal Income Statement for 2014

Budget

Actual

Variance

Sales

$800,000

$793,600

$6,400

Unfavorable

Variable expenses:

Product costs

(326,000)

(320,800)

5,200

Favorable

Selling expenses

(80,000)

(82,500)

2,500

Unfavorable

Other expenses

(6,000)

(7,200)

1,200

Unfavorable

Contribution margin

388,000

383,100

4,900

Unfavorable

Fixed expenses:

Chapter 15 Performance Evaluation

15-6

Product costs

(21,000)

(20,780)

220

Favorable

Selling expenses

(40,000)

(39,610)

390

Favorable

Other expenses

(3,200)

(3,350)

150

Unfavorable

Operating income

323,800

319,360

4,440

Unfavorable

Interest expense

(1,300)

(1,200)

100

Favorable

Operating Income

$322,500

$318,160

$4,340

Unfavorable

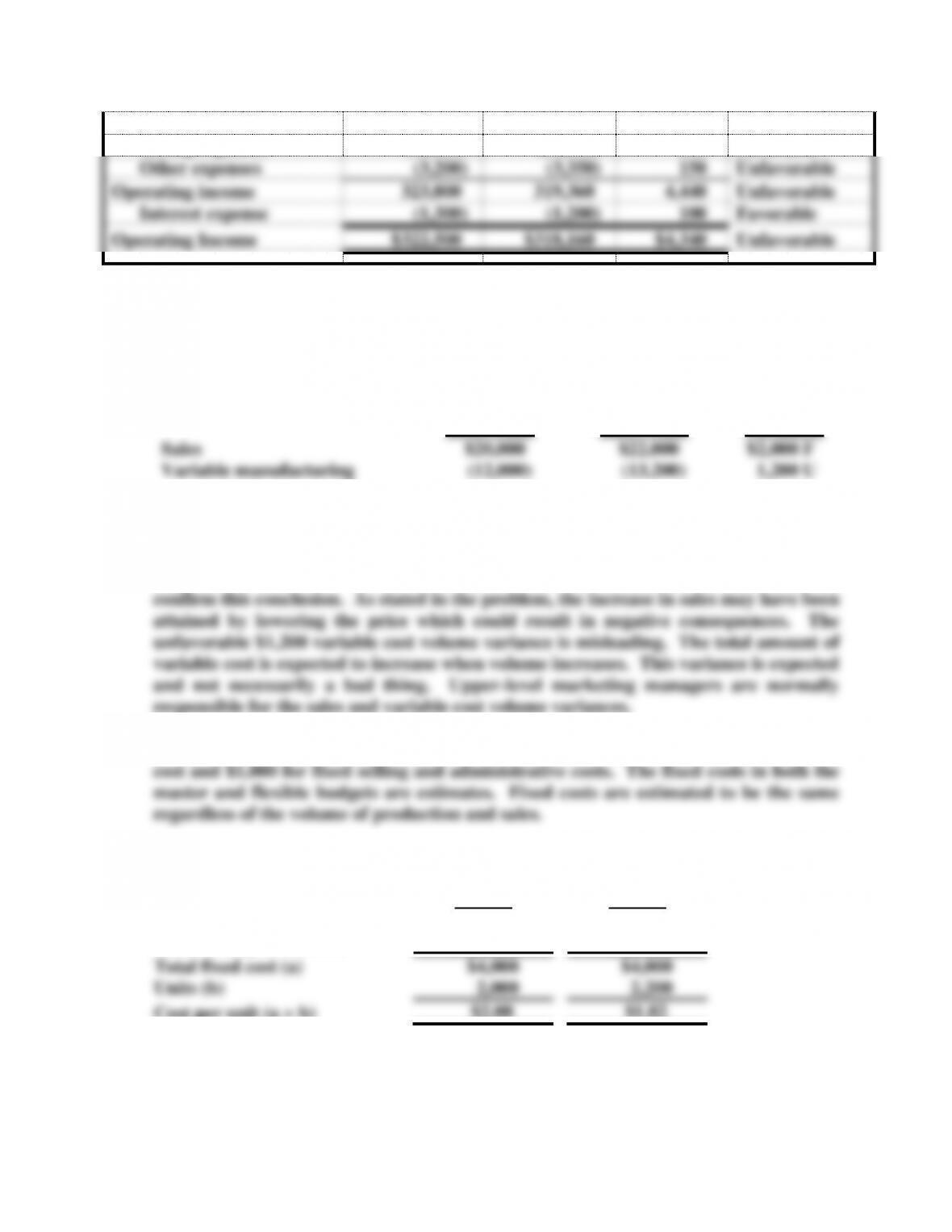

Exercise 15-7

a. & b.

Master

Budget

2,000 Units

Flexible

Budget

2,200 Units

a. & b.

Volume

Variances

Sales

$20,000

$22,000

$2,000 F

Variable manufacturing

(12,000)

(13,200)

1,200 U

c. Since the sales price and cost per unit are the same for both the master and flexible

budgets, the cause of the variances is attributable solely to the fact that the sales

volume was 200 units more than planned. The favorable $2,000 sales volume variance

suggests that it is beneficial to increase sales. However, more information is needed to

d. The amount of fixed cost appearing in the flexible budget is $3,000 for manufacturing

e.

Master

Budget

Flexible

Budget

Fixed manufacturing

$3,000

$3,000

Fixed selling and admin.

1,000

1,000

Total fixed cost (a)

$4,000

$4,000

Units (b)

2,000

2,200

Cost per unit (a b)

$2.00

$1.82

Exercise 15-7 (continued)

Chapter 15 Performance Evaluation

15-7

The increase in sales volume acts to reduce the fixed cost per unit, thereby increasing

profitability. The effect on net income will be magnified as a result of operating

Exercise 15-8

Flexible

Budget

2,200 Units

Actual

Price/Cost at

2,200 Units

a. & b.

Flexible

Budget

Variances

Sales

$22,000

$21,5601

$440 U

Variable manufacturing

(13,200)

(12,650)2

550 F

Contribution margin

8,800

8,910

110 F

Fixed manufacturing

(3,000)

(2,500)

500 F

Fixed selling and admin.

(1,000)

(1,025)

25 U

Net income

$ 4,800

$ 5,385

$585 F

1Actual sales: $9.80 x 2,200 units = $21,560

c. The fixed cost flexible budget variances are frequently called spending variances.

Exercise 15-8 (continued)

d. The unfavorable flexible budget sales variance results from the fact that products

were actually sold at a price below what was planned. To properly interpret this

result, you must also consider the sales volume variance. As previously shown in

Exercise 15-2A, the sales volume variance was $2,000 favorable. A rational

explanation for the two variances is that management sought to increase sales volume

Exercise 15-9

Chapter 15 Performance Evaluation

15-8

b. The marketing department could lack the leadership necessary to motivate the sales

staff to accomplish otherwise attainable objectives.

company’s ability to lower its sales price.

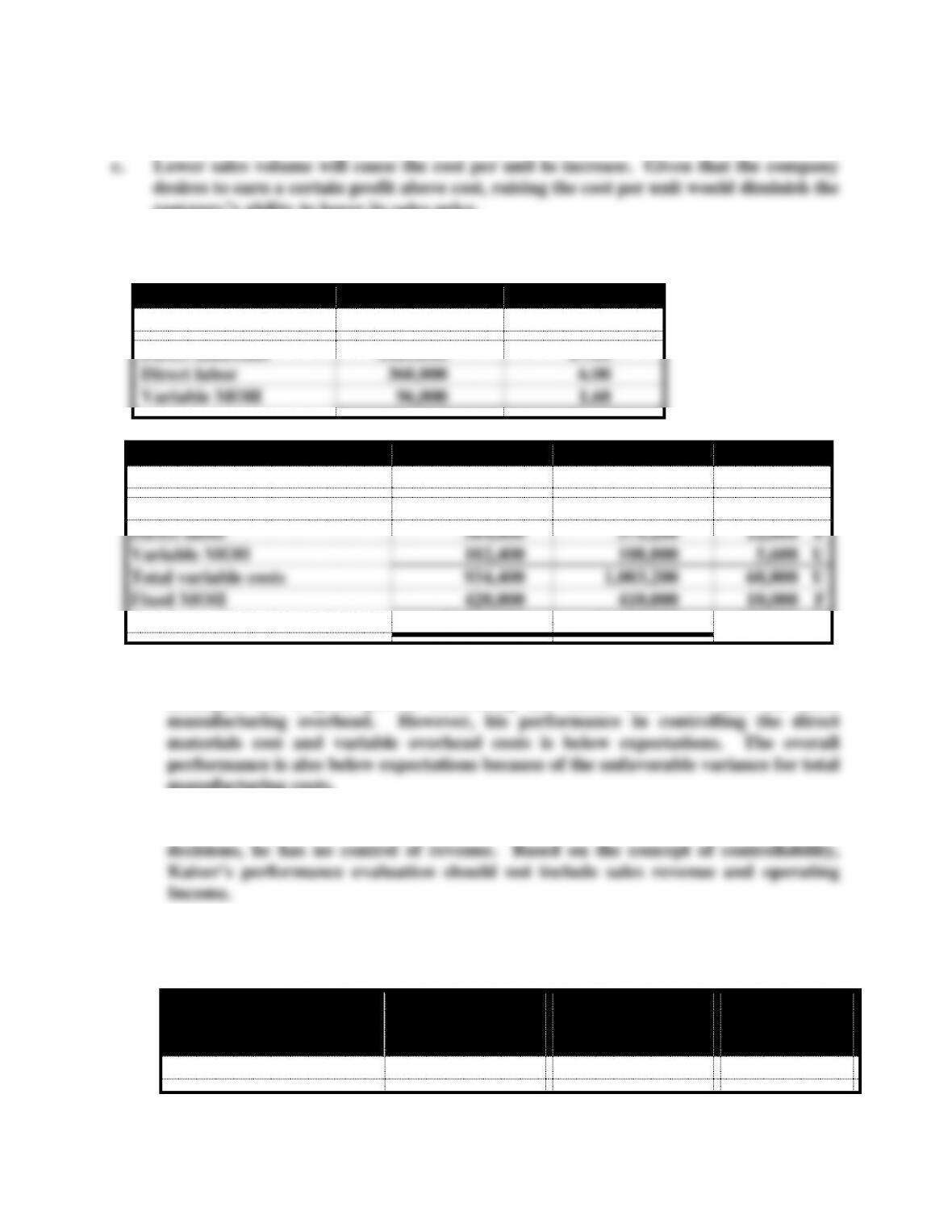

Exercise 15-10

a. & b.

Static Budget

Per Unit Cost

Production in units

60,000 Kits

Direct materials

$420,000

$7.00

Direct labor

360,000

6.00

Variable MOH

96,000

1.60

Flexible Budget

Actual Results

Variances

Production in units

64,000 Kits

64,000 Kits

Direct materials

$448,000

$524,000

$76,000 U

Direct labor

384,000

371,200

12,800 F

Variable MOH

102,400

108,000

5,600 U

Total variable costs

934,400

1,003,200

68,800 U

Fixed MOH

420,000

410,000

10,000 F

Total manufacturing costs

$1,354,400

$1,413,200

$58,800 U

According to the analysis of flexible budget variances, Albert Kaiser, the production

manager, did a good job in controlling the direct labor cost and the fixed

manufacturing costs.

c. Because Mr. Kaiser does not have the authority to make pricing and marketing

Exercise 15-11

a.

Master

Budget

30,000 Hours

Flexible

Budget

31,500 Hours

Volume

Variance

Sales ($100 per hour)

$3,000,000

$3,150,000

$150,000 F

Chapter 15 Performance Evaluation

15-9

b.

Flexible

Budget

31,500 Hours

Actual

Revenue at

31,500 Hours

Flexible

Budget

Variance

Sales

$3,150,000

$2,992,5001

$157,500 U

1Actual Sales: $95 x 31,500 hours = $2,992,500

c. Reducing the sales price was unprofitable. The favorable volume variance is less than

Exercise 15-12

Operating income ÷ Operating assets = ROI

Exercise 15-13

Operating income ÷ Operating assets = ROI

Operating income ÷ $480,000 = 10%

Operating income = Operating assets x ROI

a. If expenses are reduced by $30,000, they would become $222,000. Accordingly, the

operating Income will become $78,000 ($300,000 – $222,000).

Exercise 15-13 (continued)

b. If both sales and expenses cannot be changed, the operating Income would remain

Operating income ÷ Operating assets = ROI

The operating assets must be decreased from $480,000 to $295,385 to achieve

Exercise 15-14

Chapter 15 Performance Evaluation

15-10

Exercise 15-15

a. Division A: Residual income = $26,000 – (16% x $125,000) = $6,000

b. Division A had residual income of $6,000 and Division B had no residual income.

Exercise 15-16

ROI

Operating profit margin x Turnover

0.08 x 2.2 = 0.176 or 17.60%

Investment in operating assets

Turnover = Sales/Operating assets = 2.2

$484,000/X = 2.2

X = $220,000

Operating income

Operating profit margin = Operating income/Sales

0.08 = X/$484,000

X = $38,720

Residual income

$38,720 – [10% x $220,000] = $16,720

Exercise 15-17

Current residual income:

($10,000,000 x 12%) – ($10,000,000 x 8%) = $400,000

New residual income if the investment opportunity is adopted:

Division will be better off taking the opportunity.

Problem 15-18

a. The characteristics that differentiate a cost center, a profit center, and an

investment center from each other are tied to or depend on the concept of