9-9

Demonstration Problem 9-1 Solution

b. continued

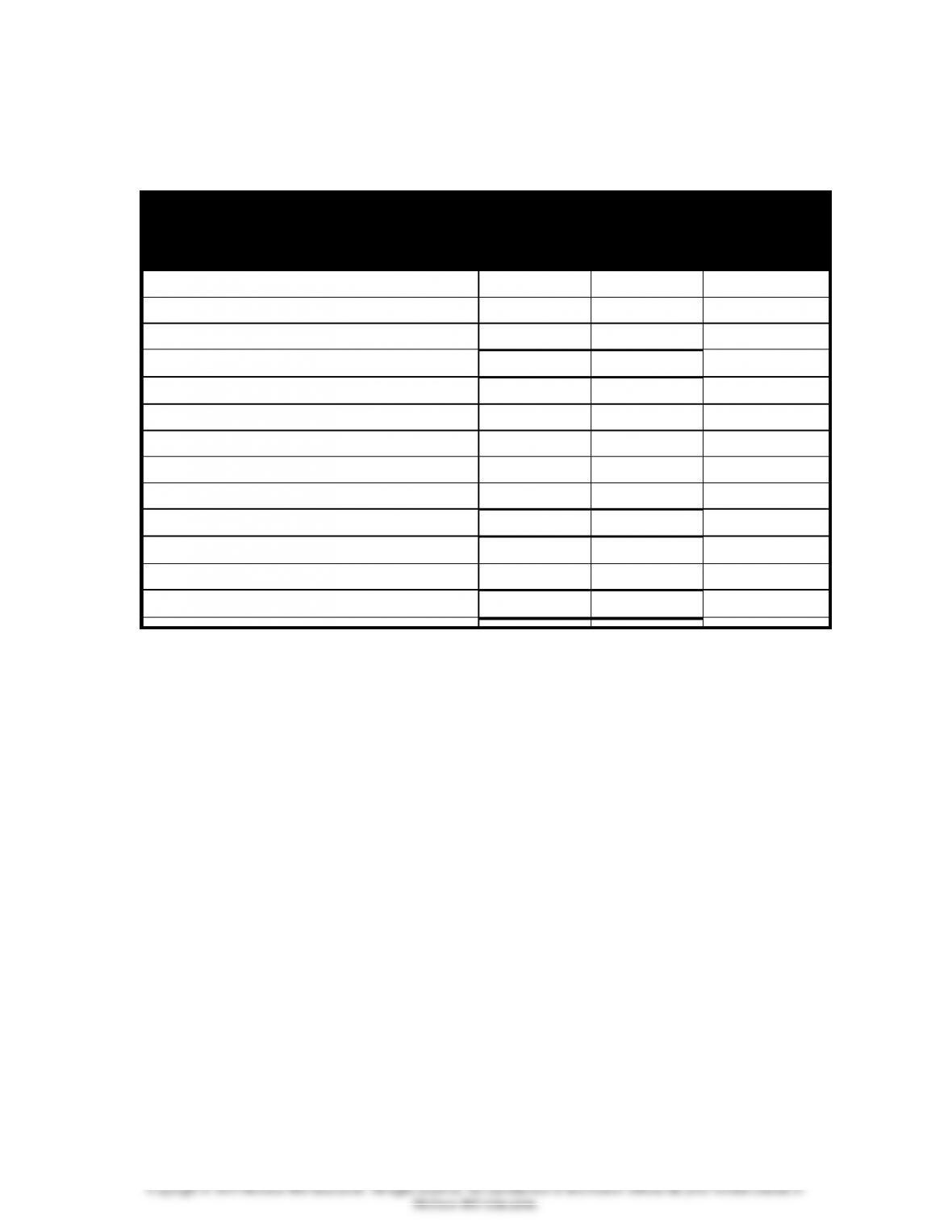

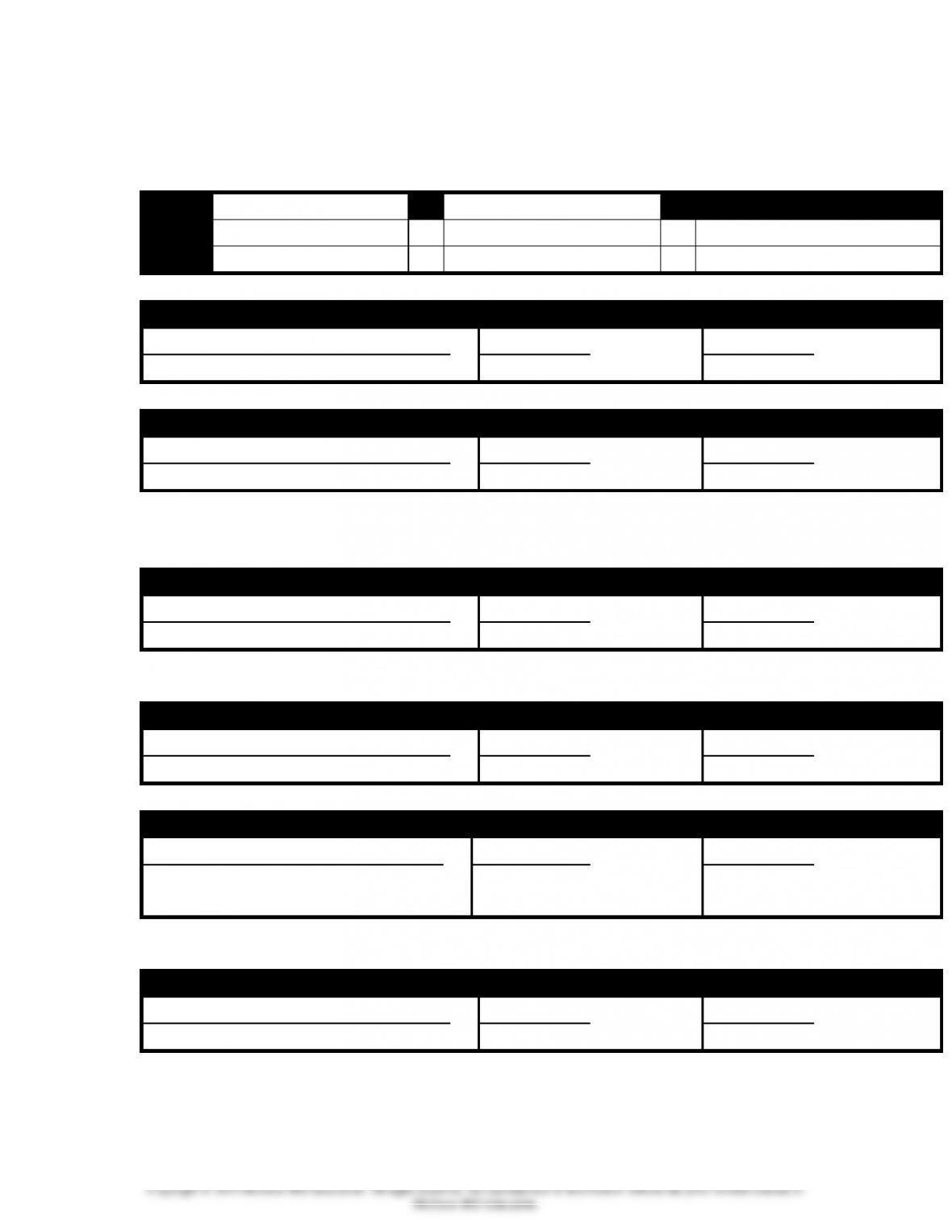

Rosson Company

Vertical Analysis of Balance Sheets

2015

2014

Amount

% of Total

Amount

% of

Total

Assets

Cash

$ 7,500

1.92%

$ 12,500

3.42%

Marketable Securities

1,000

0.26

1,500

0.41

Accounts Receivable

50,000

12.79

47,500

12.98

Inventories

150,000

38.36

145,000

39.62

Prepaid Expenses

5,000

1.28

2,500

0.68

Total Current Assets

213,500

54.60*

209,000

57.10*

Plant and Equipment (net)

147,000

37.60

157,000

42.90

Intangibles

30,500

7.80

0

0.00

Total Assets

$391,000

100.00

$366,000

100.00

Liabilities

Accounts Payable

$ 58,000

14.83

$ 79,500

21.72

Other Accrued Liabilities

25,000

6.39

22,500

6.15

Total Current Liabilities

83,000

21.23*

102,000

27.87

Bonds Payable

90,000

23.02

100,000

27.32

Total Liabilities

173,000

44.25

202,000

55.19

Stockholders’ Equity

Common Stock ($5 par)

130,000

33.25

130,000

35.52

Paid-in Cap. in Excess of Par

20,000

5.12

20,000

5.46

Retained Earnings

68,000

17.39

14,000

3.83

Total Stockholders’ Equity

218,000

55.75*

164,000

44.81

Total Liabilities and

Stk.Equity

$391,000

100.00

$366,000

100.00

*Percentages don’t add up exactly because of rounding.

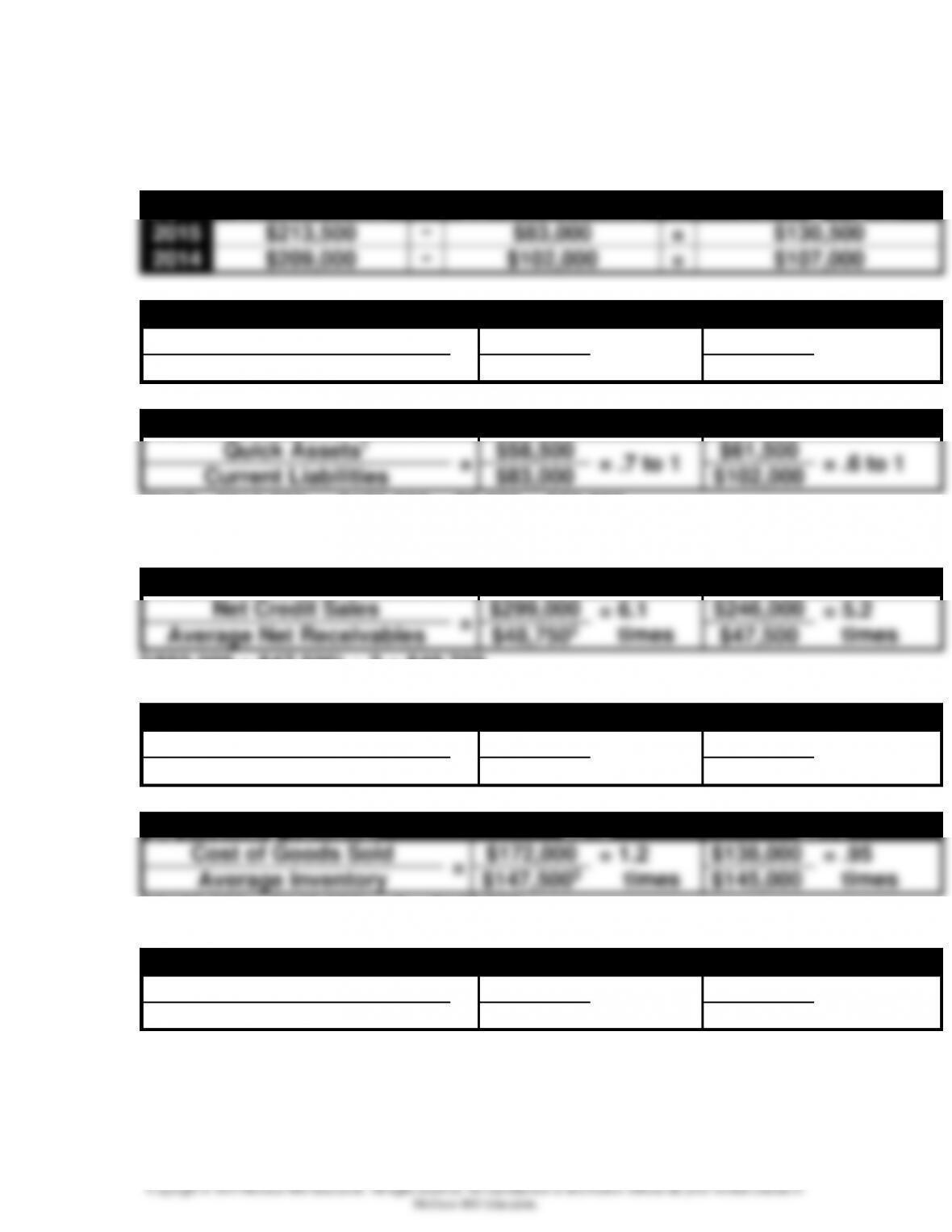

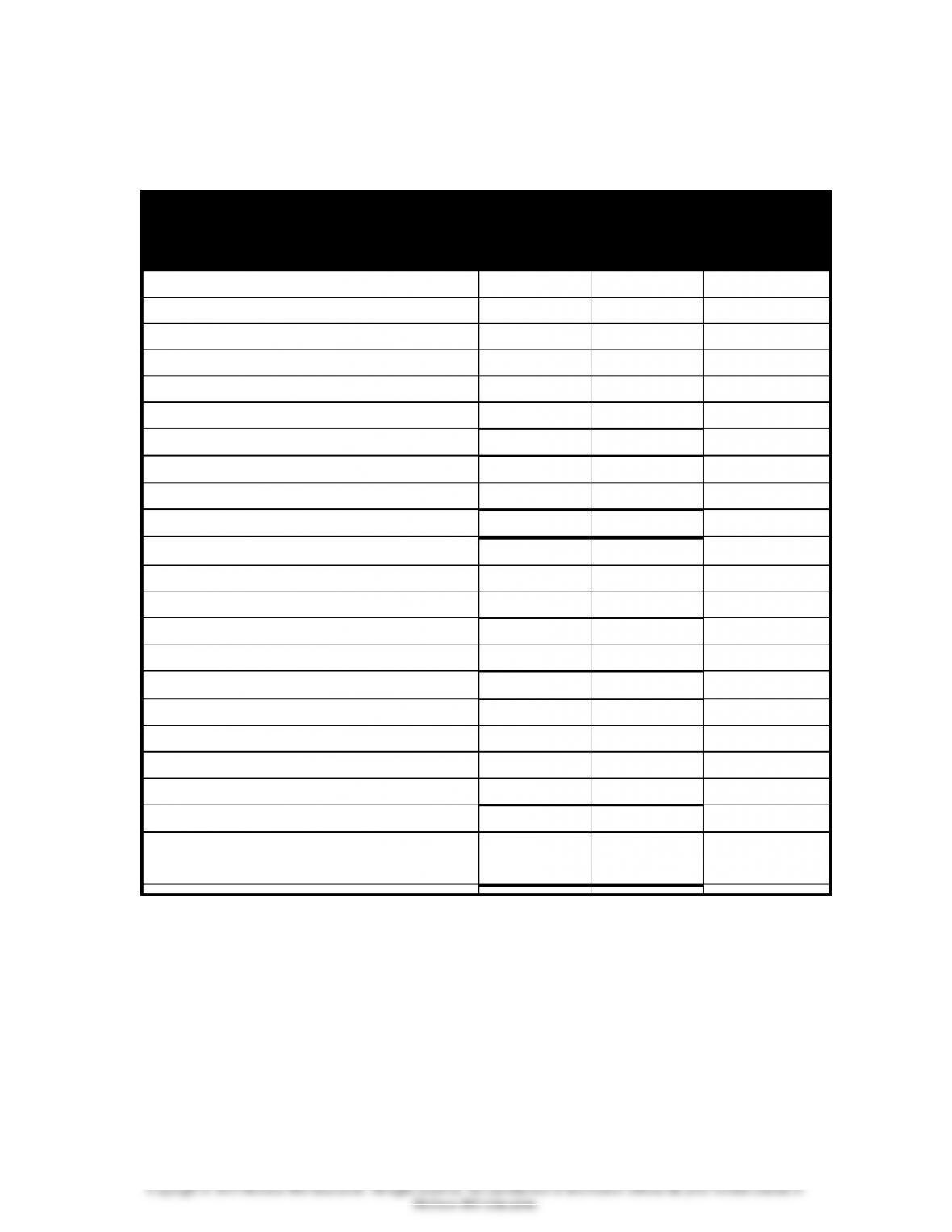

9-10

Demonstration Problem 9-1 Solution

c. Liquidity Ratios

(1)

Current Assets

–

Current Liabilities

=

Working Capital

2015

$213,500

–

$83,000

=

$130,500

2014

$209,000

–

$102,000

=

$107,000

(2) Current Ratio

2015

2014

Current Assets

=

$213,500

= 2.6 to 1

$209,000

= 2.05 to 1

Current Liabilities

$83,000

$102,000

(3) Quick (Acid-test) Ratio

2015

2014

Quick Assets1

=

$58,500

= .7 to 1

$61,500

= .6 to 1

Current Liabilities

$83,000

$102,000

12015: $213,500 – $150,000 – $5,000 = $58,500

2014: $209,000 – $145,000 – $2,500 = $61,500

(4) Accts. Receivable Turnover

2015

2014

Net Credit Sales

=

$299,000

= 6.1

times

$246,000

= 5.2

times

Average Net Receivables

$48,7502

$47,500

2($50,000 + $47,500) ÷ 2 = $48,750

(5)Avg. Days to Collect Receivables

2015

2014

Days in Year

=

365

= 59.8

days

365

= 70.2

days

Accts. Receivable Turnover

6.1 times

5.2 times

(6) Inventory Turnover

2015

2014

Cost of Goods Sold

=

$172,000

= 1.2

times

$138,000

= .95

times

Average Inventory

$147,5003

$145,000

3($150,000 + $145,000) ÷ 2 = $147,500

(7) Avg. Days to Sell Inventory

2015

2014

Days in Year

=

365

= 304.2

days

365

= 384 days

Inventory Turnover

1.2 times

.95 times

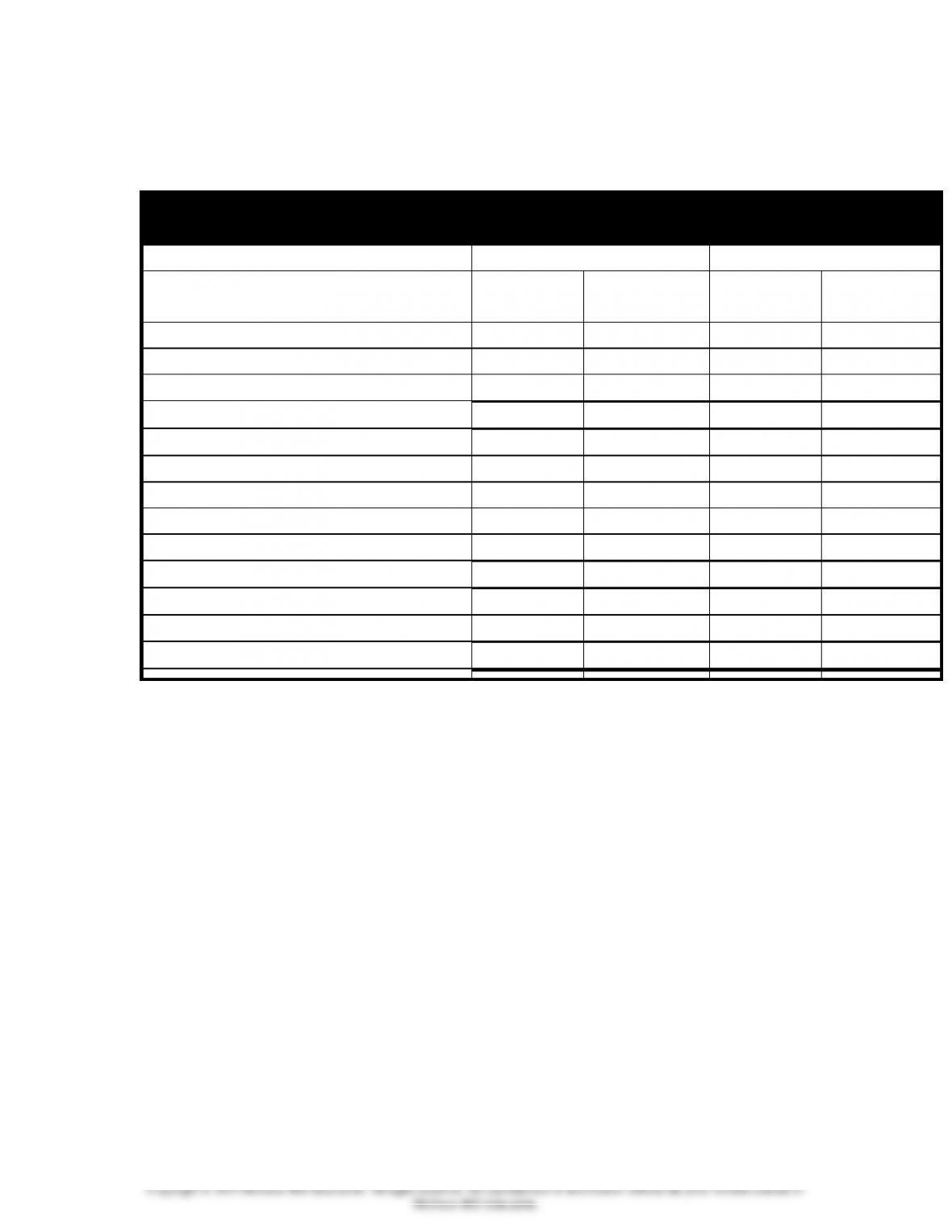

9-11

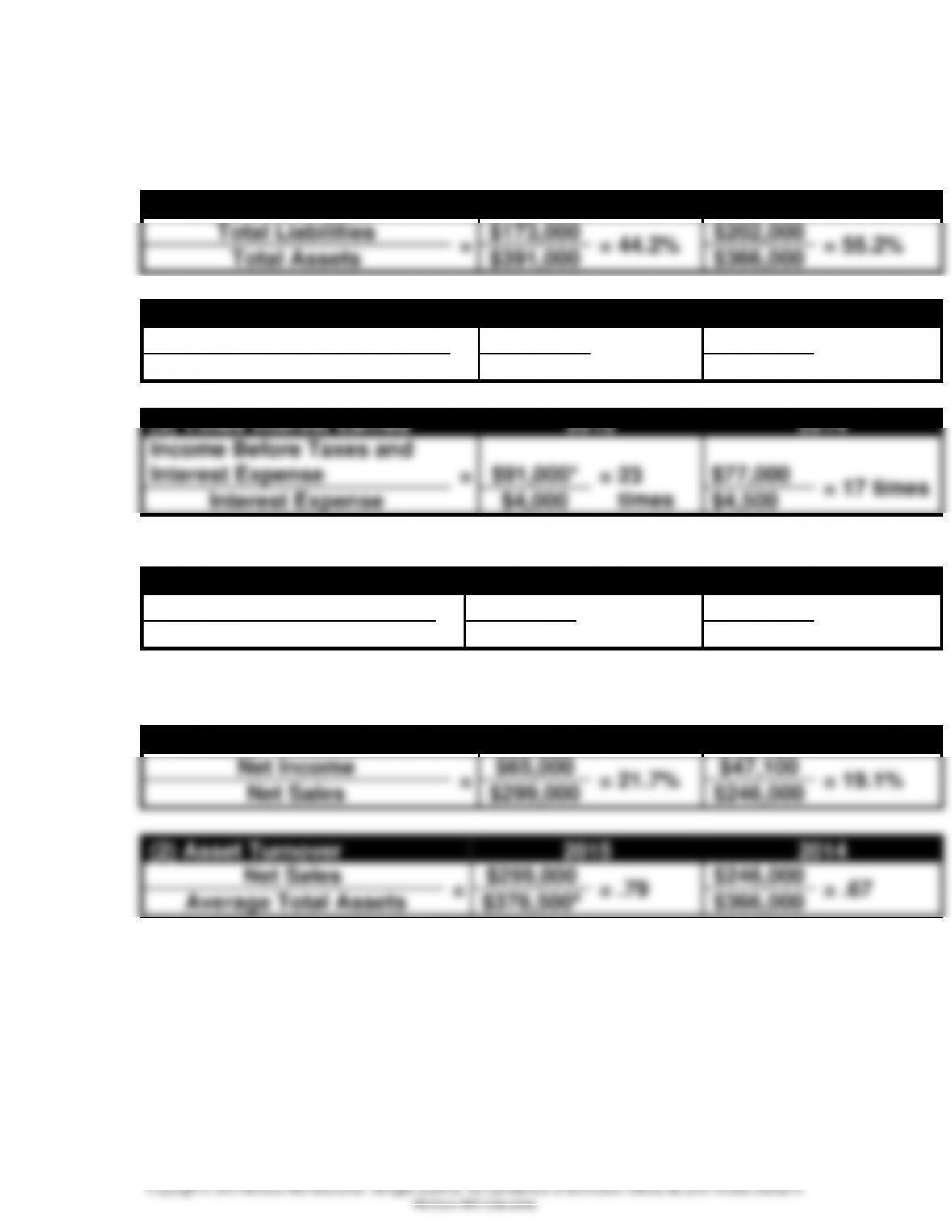

Demonstration Problem 9-1 Solution

d. Solvency Ratios

(1) Debt to Assets

2015

2014

Total Liabilities

=

$173,000

= 44.2%

$202,000

= 55.2%

Total Assets

$391,000

$366,000

(2) Debt to Equity Ratio

2015

2014

Total Liabilities

=

$173,000

= 79.4%

$202,000

= 123.2%

Total Stockholders’ Equity

$218,000

$164,000

(3) Times Interest Earned

2015

2014

Income Before Taxes and

Interest Expense

=

$91,000*

= 23

times

$77,000

= 17 times

Interest Expense

$4,000

$4,500

*Before extraordinary gain

(4) Plant Assets to LT Liab.

2015

2014

Net Plant Assets

=

$147,000

= 1.63 to 1

$157,000

= 1.57 to 1

Long-term Liabilities

$90,000

$100,000

e. Profitability Ratios

(1) Net Margin

2015

2014

Net Income

=

$65,000

= 21.7%

$47,100

= 19.1%

Net Sales

$299,000

$246,000

(2) Asset Turnover

2015

2014

Net Sales

=

$299,000

= .79

$246,000

= .67

Average Total Assets

$378,5004

$366,000

4($391,000 + $366,000) ÷ 2 = $378,500

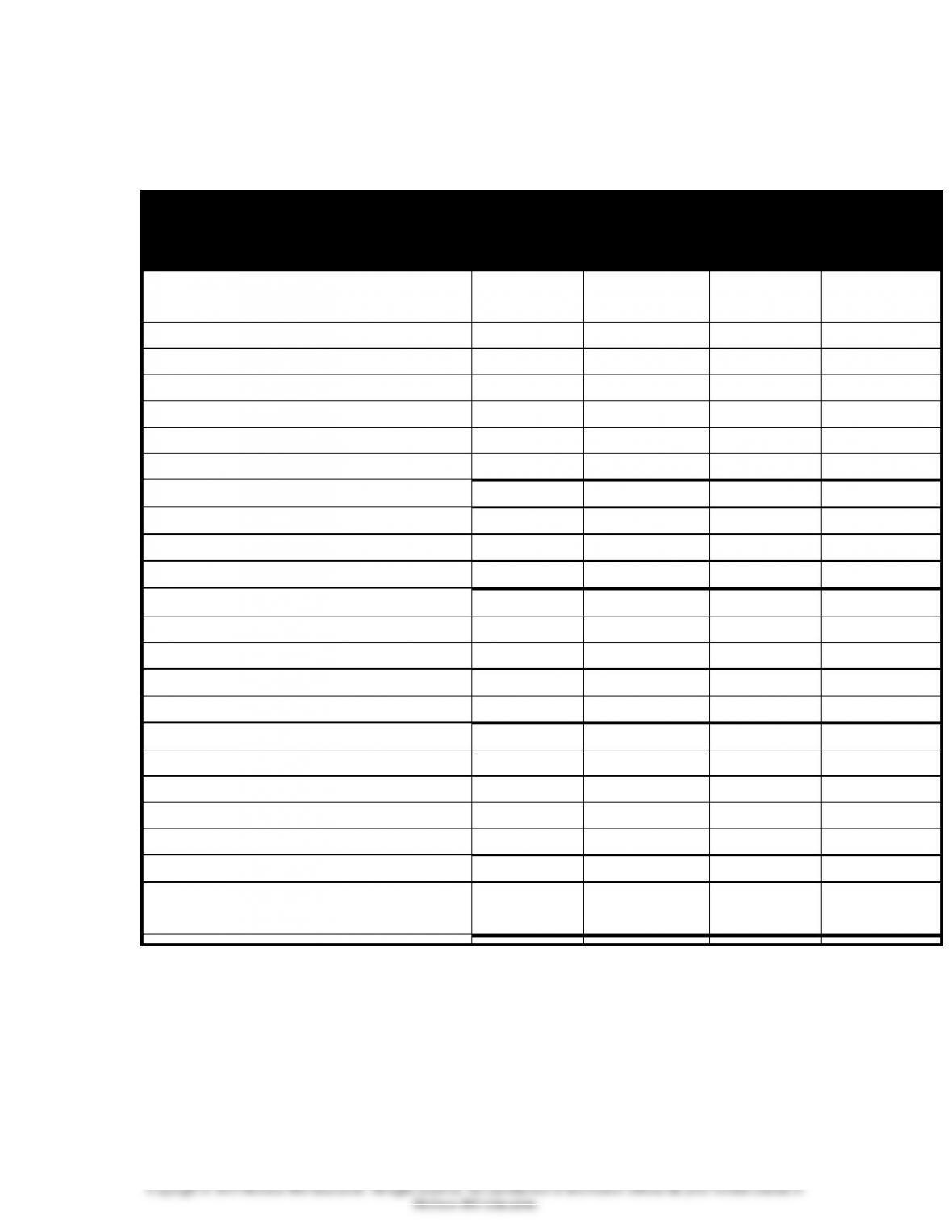

9-12

Demonstration Problem 9-1 Solution

e. Profitability Ratios, continued

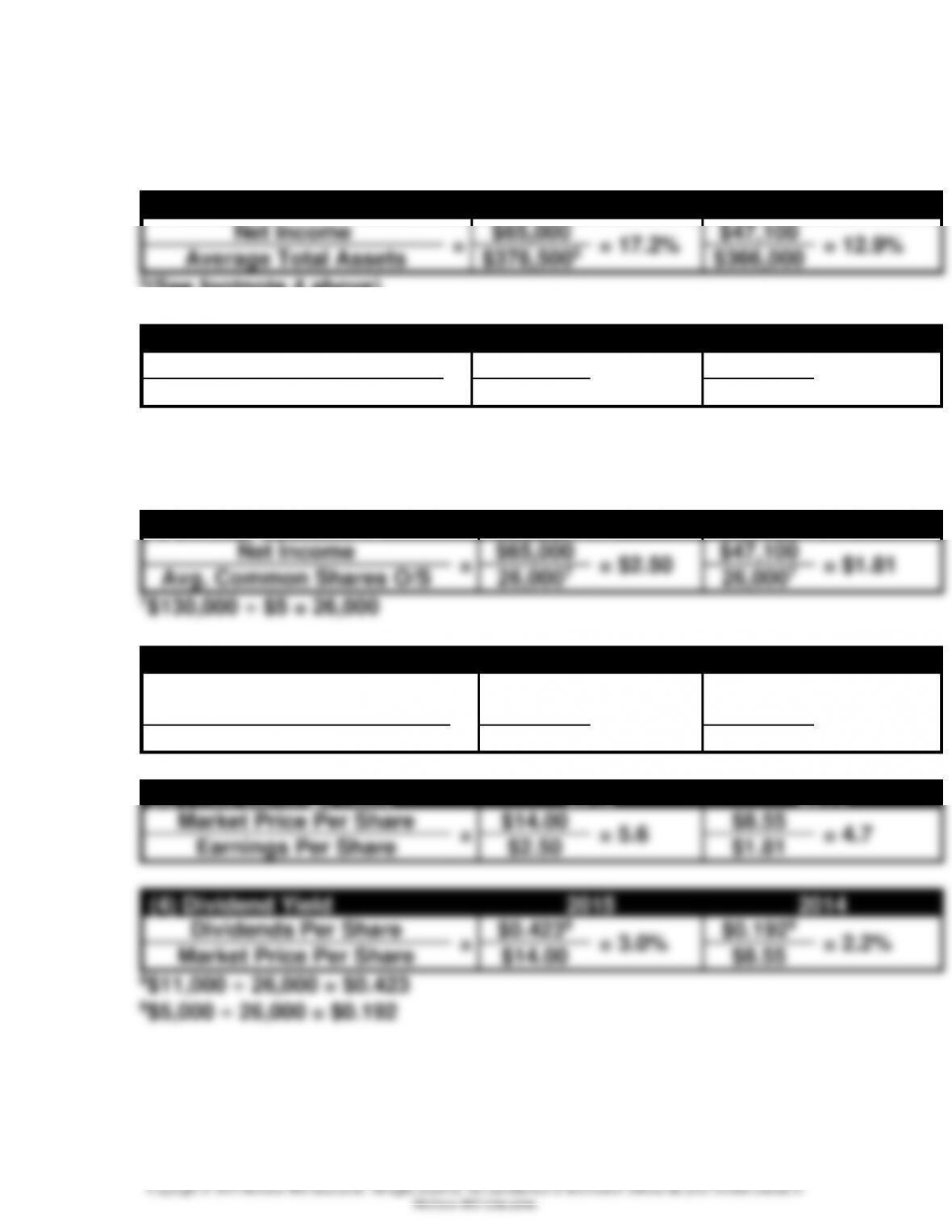

(3) Return on Investment

2015

2014

Net Income

=

$65,000

= 17.2%

$47,100

= 12.9%

Average Total Assets

$378,5005

$366,000

(4) Return on Equity

2015

2014

Net Income

=

$65,000

= 34.0%

$47,100

= 28.7%

Avg. Stockholders’ Equity

$191,0006

$164,000

6($218,000 + $164,000) ÷ 2 = $191,000

f. Stock Market Ratios

(1) Earnings Per Share

2015

2014

Net Income

=

$65,000

= $2.50

$47,100

= $1.81

Avg. Common Shares O/S

26,0007

26,0007

(2) Book Value Per Share

2015

2014

Stockholders’ Equity –

Preferred Rights

=

$218,000

= $8.38

$164,000

= $6.31

Avg. Common Shares O/S

26,000

26,000

(3) Price-earnings Ratio

2015

2014

Market Price Per Share

=

$14.00

= 5.6

$8.55

= 4.7

Earnings Per Share

$2.50

$1.81

(4) Dividend Yield

2015

2014

Dividends Per Share

=

$0.4238

= 3.0%

$0.1929

= 2.2%

Market Price Per Share

$14.00

$8.55

8$11,000 ÷ 26,000 = $0.423

9$5,000 ÷ 26,000 = $0.192

9-13

Demonstration Problem 9-1 Work Papers

a.

Rosson Company

Horizontal Analysis of Income Statements

2015

2014

% Change

Revenues:

Net Sales

$299,000

$246,000

Other Revenues

8,000

9,000

Total Revenues

307,000

255,000

Expenses:

Cost of Goods Sold

172,000

138,000

S,G&A Expenses

44,000

40,000

Interest Expense

4,000

4,500

Income Tax Expense

31,000

25,400

Total Expenses

251,000

207,900

Income Before X/O Items

56,000

47,100

Extraordinary Gain (net of tax)

9,000

0

Net Income

$ 65,000

$ 47,100

9-14

Demonstration Problem 9-1 Work Papers

a. continued

Rosson Company

Horizontal Analysis of Balance Sheets

2015

2014

% Change

Assets

Cash

$ 7,500

$ 12,500

Marketable Securities

1,000

1,500

Accounts Receivable

50,000

47,500

Inventories

150,000

145,000

Prepaid Expenses

5,000

2,500

Total Current Assets

213,500

209,000

Plant and Equipment (net)

147,000

157,000

Intangibles

30,500

0

Total Assets

$391,000

$366,000

Liabilities

Accounts Payable

$ 58,000

$ 79,500

Other Accrued Liabilities

25,000

22,500

Total Current Liabilities

83,000

102,000

Bonds Payable

90,000

100,000

Total Liabilities

173,000

202,000

Stockholders’ Equity

Common Stock ($5 par)

130,000

130,000

Paid-in Cap. in Excess of Par

20,000

20,000

Retained Earnings

68,000

14,000

Total Stockholders’ Equity

218,000

164,000

Total Liabilities and Stk.

Equity

$391,000

$366,000

9-15

Demonstration Problem 9-1 Work Papers

b.

Rosson Company

Vertical Analysis of Income Statements

2015

2014

Amount

% of Total

Amount

% of

Total

Revenues:

Net Sales

$299,000

$246,000

Other Revenues

8,000

9,000

Total Revenues

307,000

255,000

Expenses:

Cost of Goods Sold

172,000

138,000

S,G&A Expenses

44,000

40,000

Interest Expense

4,000

4,500

Income Tax Expense

31,000

25,400

Total Expenses

251,000

*

207,900

*

Income Before X/O Items

56,000

47,100

Extraordinary Gain (net of tax)

9,000

0

Net Income

$ 65,000

$ 47,100

*Percentages don’t add up exactly because of rounding.

9-16

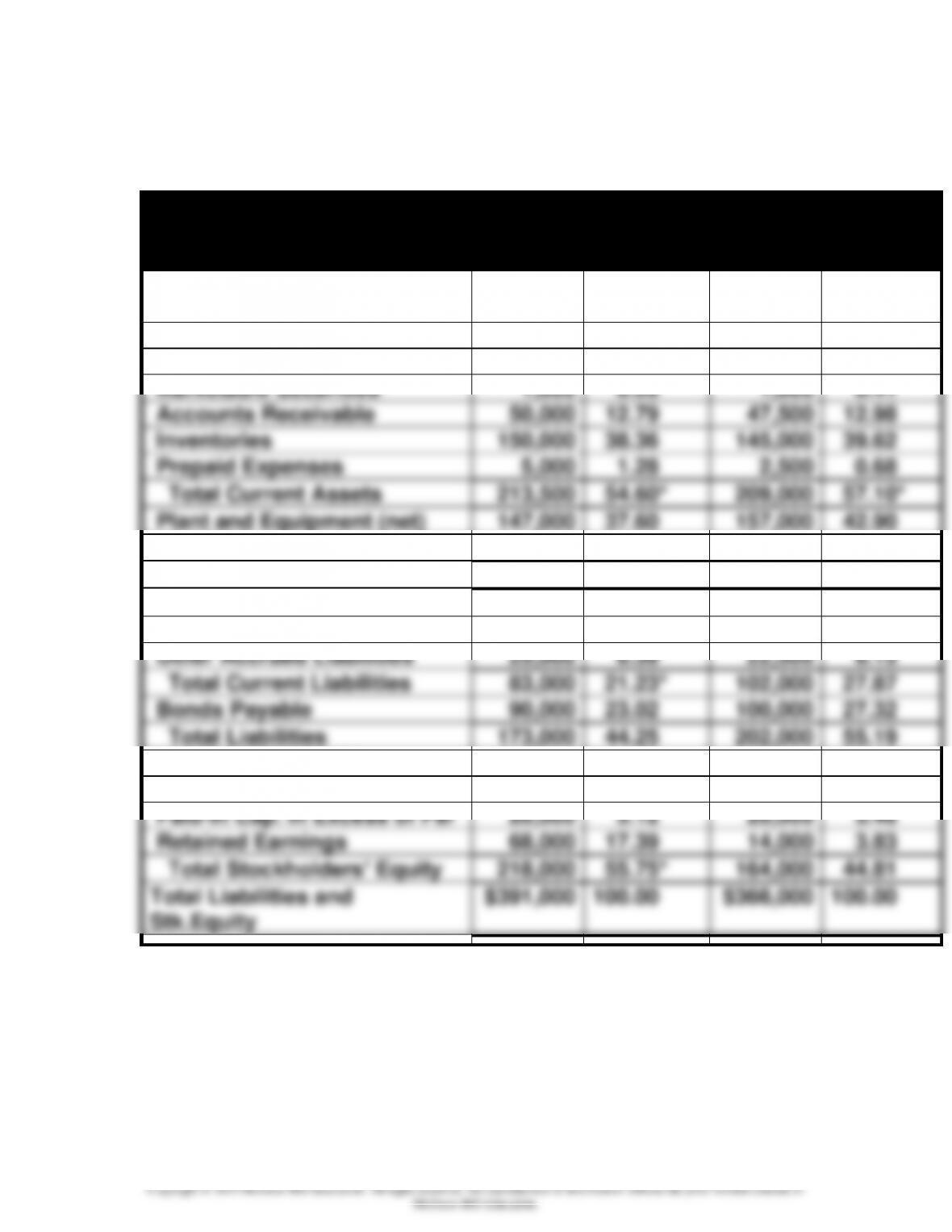

Demonstration Problem 9-1 Work Papers

b. continued

Rosson Company

Vertical Analysis of Balance Sheets

2015

2014

Amount

% of Total

Amount

% of

Total

Assets

Cash

$ 7,500

$ 12,500

Marketable Securities

1,000

1,500

Accounts Receivable

50,000

47,500

Inventories

150,000

145,000

Prepaid Expenses

5,000

2,500

Total Current Assets

213,500

*

209,000

*

Plant and Equipment (net)

147,000

157,000

Intangibles

30,500

0

Total Assets

$391,000

$366,000

Liabilities

Accounts Payable

$ 58,000

$ 79,500

Other Accrued Liabilities

25,000

22,500

Total Current Liabilities

83,000

*

102,000

Bonds Payable

90,000

100,000

Total Liabilities

173,000

202,000

Stockholders’ Equity

Common Stock ($5 par)

130,000

130,000

Paid-in Cap. in Excess of Par

20,000

20,000

Retained Earnings

68,000

14,000

Total Stockholders’ Equity

218,000

*

164,000

Total Liabilities and

Stk.Equity

$391,000

$366,000

*Percentages don’t add up exactly because of rounding.

9-17

Demonstration Problem 9-1 Work Papers

c. Liquidity Ratios

(1)

–

=

Working Capital

2015

–

=

$130,500

2014

–

=

$107,000

(2) Current Ratio

2015

2014

=

= ___to 1

= ___ to 1

(3) Quick (Acid-test) Ratio

2015

2014

1

=

= ___to 1

= ___ to 1

12015:

2014:

(4) Accts. Receivable Turnover

2015

2014

=

= ___

times

= ___

times

2

2

(5)Avg. Days to Collect Receivables

2015

2014

=

= ____

days

= ____

days

(6) Inventory Turnover

2015

2014

=

= ____

times

= ____

times

3

3

(7) Avg. Days to Sell Inventory

2015

2014

=

= ____

days

= ___ days

9-18

Demonstration Problem 9-1 Work Papers

d. Solvency Ratios

(1) Debt to Assets

2015

2014

=

= %

= %

(2) Debt to Equity Ratio

2015

2014

=

= 79.4%

= 123.2%

(3) Times Interest Earned

2015

2014

=

*

= ____

times

= ____

times

*Before extraordinary gain

(4) Plant Assets to LT Liab.

2015

2014

=

= ___ to 1

= ___ to 1

e. Profitability Ratios

(1) Net Margin

2015

2014

=

= %

= %

(2) Asset Turnover

2015

2014

=

=

=

4

4

9-19

Demonstration Problem 9-1 Work Papers

e. Profitability Ratios, continued

(3) Return on Investment

2015

2014

=

= ____%

= ____%

5

5(See footnote 4 above)

(4) Return on Equity

2015

2014

=

= ____%

= _____%

6

6

f. Stock Market Ratios

(1) Earnings Per Share

2015

2014

=

= $

= $

7

7

7

(2) Book Value Per Share

2015

2014

=

= $

= $

(3) Price-earnings Ratio

2015

2014

=

=

=

(4) Dividend Yield

2015

2014

=

8

= %

9

= %

8

9