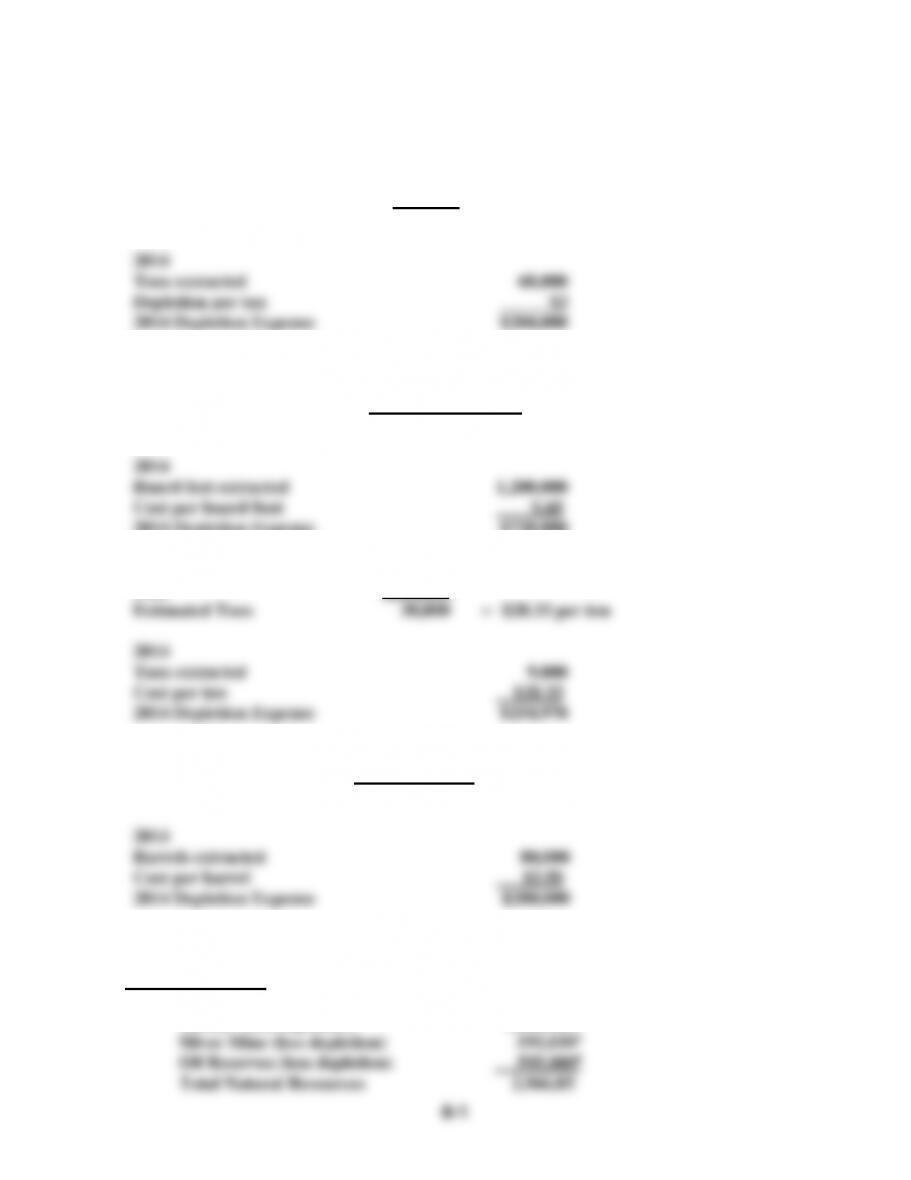

PROBLEM 6-30

a.

Computations:

Coal Mine – Depletion

Cost

$900,000

=

$3.00 per ton

Estimated Tons

300,000

2014

Tons extracted

68,000

Depletion per ton

$3

2014 Depletion Expense $204,000

Timber – Depletion

Cost

$2,000,000 – 200,000

=

$.60 per board foot

Estimated Board Feet

3,000,000

2014

Board feet extracted 1,200,000

Cost per board foot $.60

2014 Depletion Expense $720,000

Silver Mine – Depletion

Cost

$850,000

=

$28.33 per ton

Estimated Tons

30,000

2014

Tons extracted 9,000

Cost per ton $28.33

2014 Depletion Expense $254,970

Oil Reserves – Depletion

Cost

$875,000

=

$3.50 per barrel

Estimated Barrels

270,000 – 20,000

2014

Barrels extracted 80,000

Cost per barrel $3.50

2014 Depletion Expense $280,000

PROBLEM 6-30 (cont.)

b. Natural Resources

Coal Mine (less depletion) $ 696,0001

Timber (less depletion) 1,080,0002

6-2

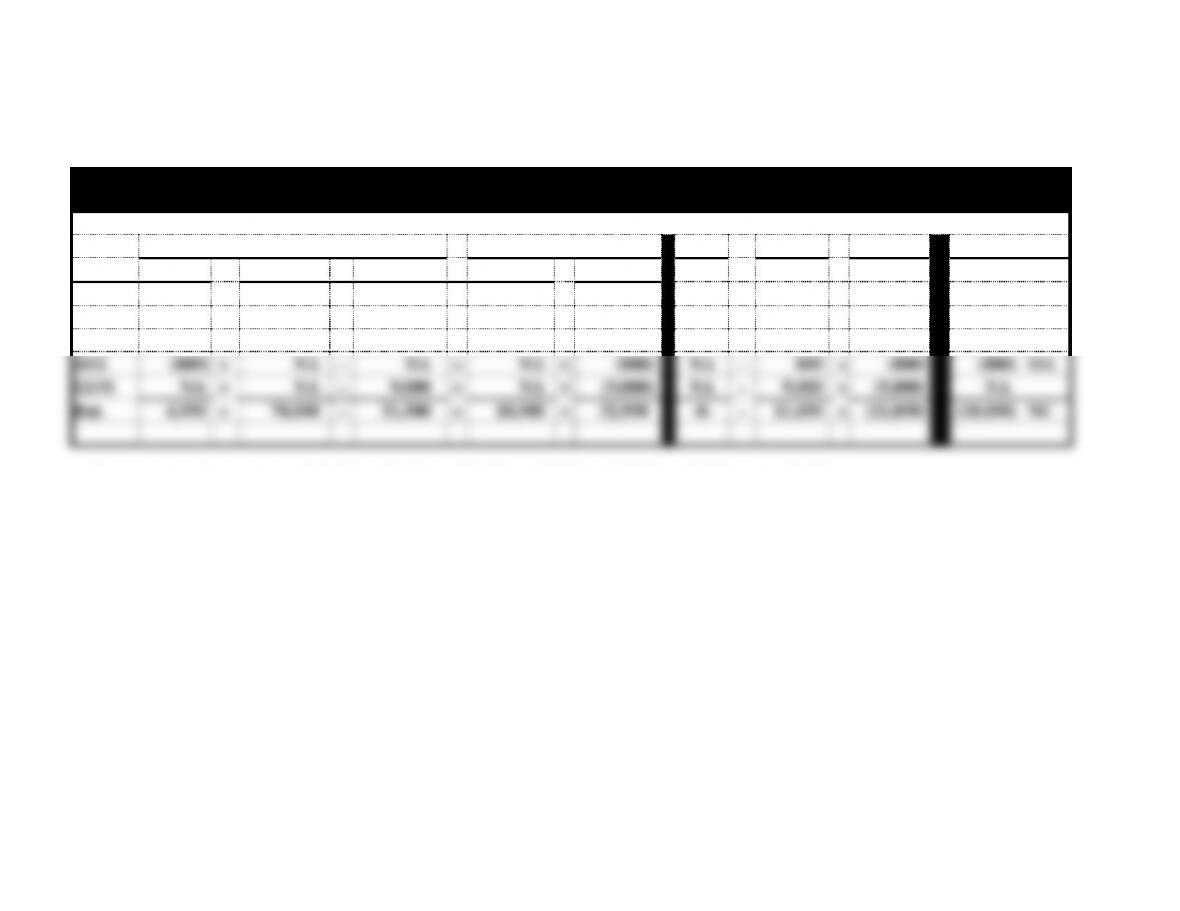

PROBLEM 6-31

Bird Manufacturing

Statements Model

Assets

=

Stockholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Date

Cash

+

Mach.

−

Acc Dep.

=

C. Stock

+

Ret. Ear.

Bal.

15,000

+

62,000

−

22,500

=

10,500

+

44,000

NA

−

NA

=

NA

NA

1/2

(8,000)

+

8,000

−

NA

=

NA

+

NA

NA

−

NA

=

NA

(8,000) IA

8/1

(1,250)

+

NA

−

NA

=

NA

+

(1,250)

NA

−

1,250

=

(1,250)

(1,250) OA

10/2

(800)

+

NA

−

NA

=

NA

+

(800)

NA

−

800

=

(800)

(800) OA

12/31

NA

+

NA

−

9,000

=

NA

+

(9,000)

NA

−

9,000

=

(9,000)

NA

Bal.

4,950

+

70,000

−

31,500

=

10,500

+

32,950

-0-

−

11,050

=

(11,050)

(10,050) NC

*Depreciation Calculation: ($62,000 + $8,000) − $22,500 = $47,500; ($47,500 − $2,500) 5 = $9,000

6-3

PROBLEM 6-32

Acquisition Price $1,500,000

Franchise 120,000 (1,380,000)

Goodwill Acquired $ 120,000

PROBLEM 6-33

The permanent impairment of $100,000 ($200,000 x ½) will be written off in the year the impairment is determined. Total

assets will be decreased and, net income will decrease, but the Statement of Cash Flows will not be affected.PROBLEM 6-34

a. Depreciation expense as a percentage of sales:

b. Property plant, and equipment (depreciable assets) as a percentage of total assets:

c. Net income was not provided in this problem (intentionally), so the return on assets ratio cannot be used to assess which

6-4

d. These companies are not in the same industry, so there are limitations when trying to compare how efficiently they used their

uses it only for some.

6-5

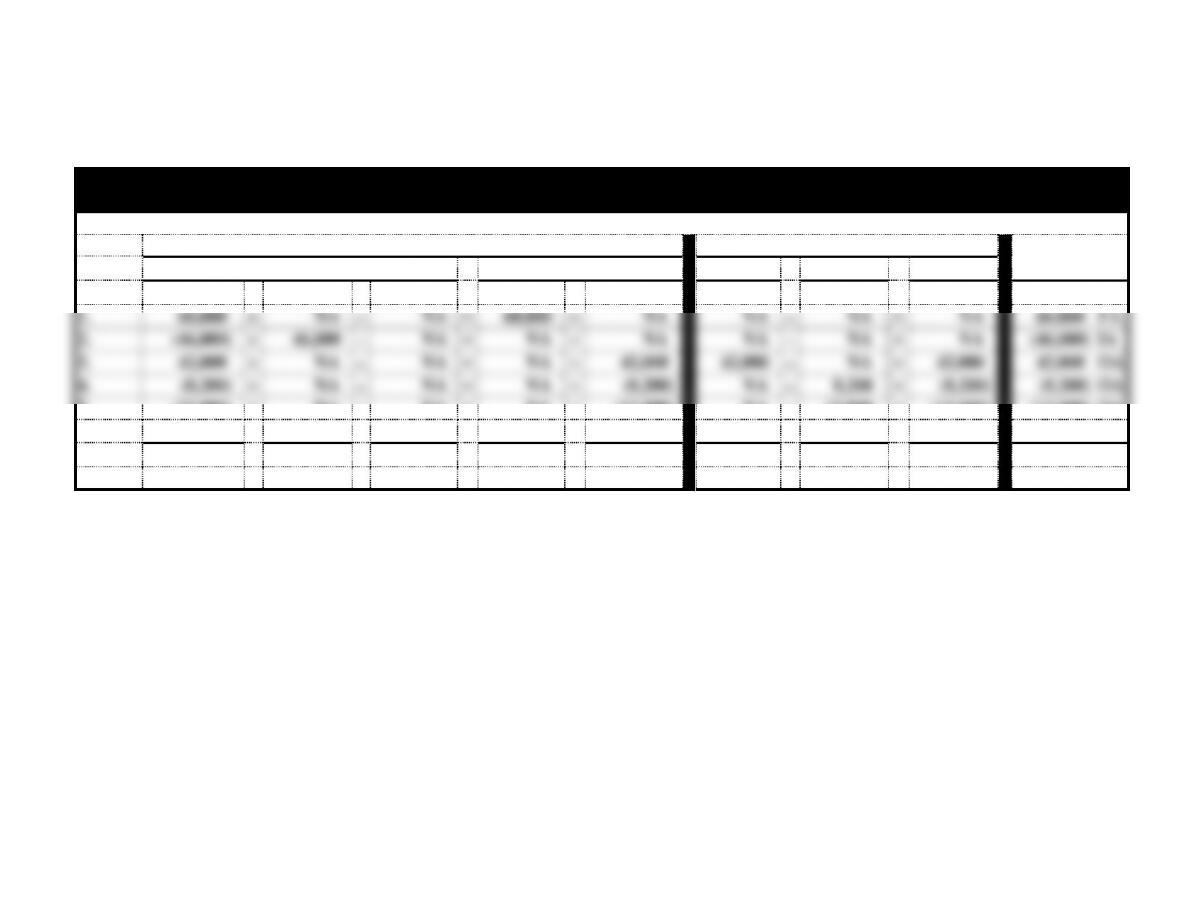

ATC 6-2 (cont.)

Note: It is useful to prepare a horizontal statements model before preparing the financial statements.

Horizontal Statement Model

Using Straight-line Depreciation

Balance Sheet

Income Statement

Statement of

Assets

=

Stockholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

Event

Cash

+

Equip.

−

A. Dep.

=

C. Stock

+

Ret. Ear.

−

=

1.

60,000

+

NA

−

NA

=

60,000

+

NA

NA

−

NA

=

NA

60,000 FA

2.

(46,000)

+

46,000

−

NA

=

NA

+

NA

NA

−

NA

=

NA

(46,000) IA

3.

42,000

+

NA

−

NA

=

NA

+

42,000

42,000

−

NA

=

42,000

42,000 OA

4.

(8,200)

+

NA

−

NA

=

NA

+

(8,200)

NA

−

8,200

=

(8,200)

(8,200) OA

5.

(12,000)

+

NA

−

NA

=

NA

+

(12,000)

NA

−

12,000

=

(12,000)

(12,000) OA

6.

NA

+

NA

−

10,000

=

NA

+

(10,000)

NA

−

10,000

=

(10,000)

NA

Bal.

35,800

+

46,000

−

10,000

=

60,000

+

11,800

42,000

−

30,200

=

11,800

38,800 NC

6-6

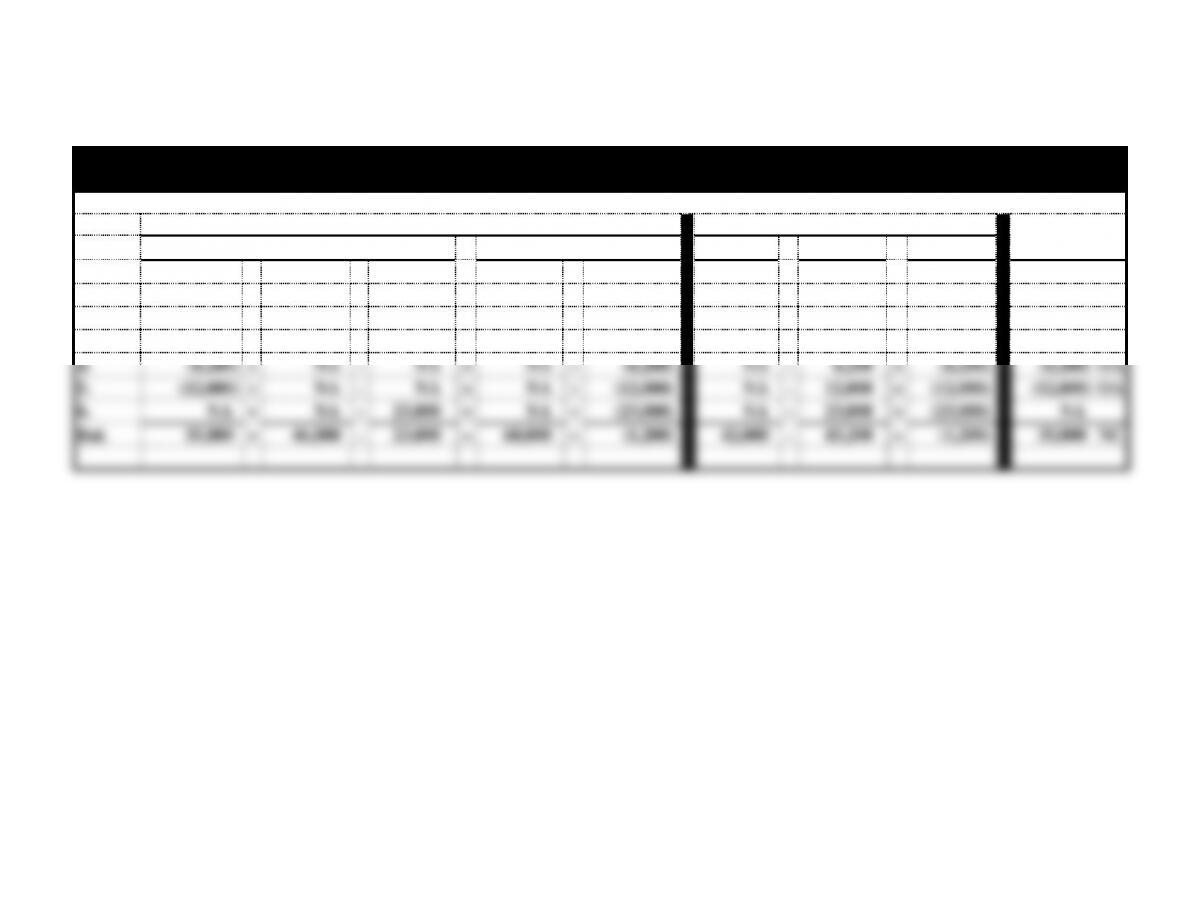

ATC 6-2 (cont.)

Horizontal Statement Model

Using Double-Declining Balance Depreciation

Balance Sheet

Income Statement

Statement of

Assets

=

Stockholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

Event

Cash

+

Equip.

−

A. Dep.

=

C. Stock

+

Ret. Ear.

−

=

1.

60,000

+

NA

−

NA

=

60,000

+

NA

NA

−

NA

=

NA

60,000 FA

2.

(46,000)

+

46,000

−

NA

=

NA

+

NA

NA

−

NA

=

NA

(46,000) IA

3.

42,000

+

NA

−

NA

=

NA

+

42,000

42,000

−

NA

=

42,000

42,000 OA

4.

(8,200)

+

NA

−

NA

=

NA

+

(8,200)

NA

−

8,200

=

(8,200)

(8,200) OA

5.

(12,000)

+

NA

−

NA

=

NA

+

(12,000)

NA

−

12,000

=

(12,000)

(12,000) OA

6.

NA

+

NA

−

23,000

=

NA

+

(23,000)

NA

−

23,000

=

(23,000)

NA

Bal.

35,800

+

46,000

−

23,000

=

60,000

+

(1,200)

42,000

−

43,200

=

(1,200)

35,800 NC

6-7

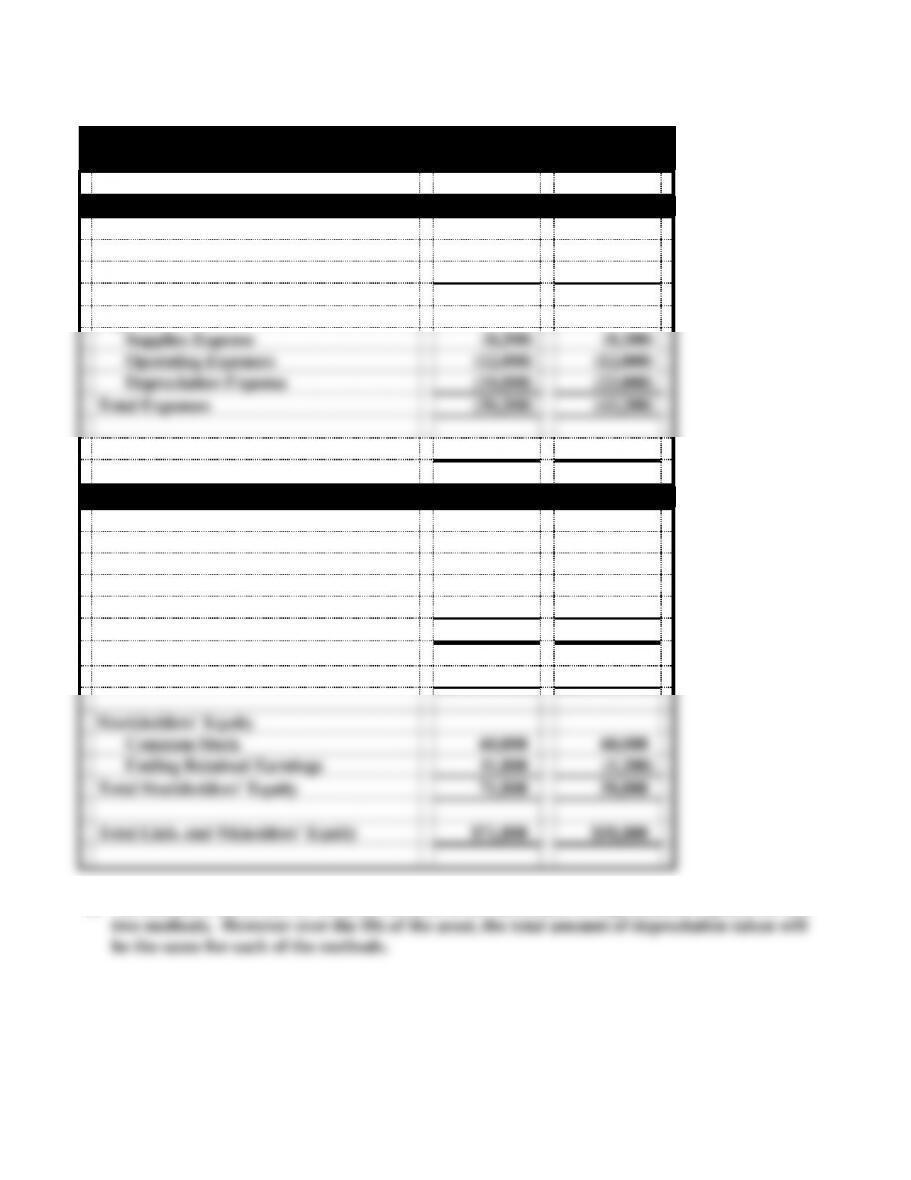

ATC 6-2 (cont.)

a.

Sweet’s Bakery

Financial Statements

Income Statements

SL

DDB

Sales Revenue

$42,000

$42,000

Expenses

Supplies Expense

(8,200)

(8,200)

Operating Expenses

(12,000)

(12,000)

Depreciation Expense

(10,000)

(23,000)

Total Expenses

(30,200)

(43,200)

Net Income

$11,800

$ (1,200)

Balance Sheets

Assets

Cash

$35,800

$35,800

Equipment

46,000

46,000

Less: Accumulated Depr.

(10,000)

(23,000)

Total Assets

$71,800

$58,800

Liabilities

$ -0–

$ -0–

Stockholders’ Equity

Common Stock

60,000

60,000

Ending Retained Earnings

11,800

(1,200)

Total Stockholders’ Equity

71,800

58,800

Total Liab. and Stkholders’ Equity

$71,800

$58,800

b. Net income is different for the year because of the difference in depreciation expense for the

6-8

ATC 6-3

The data for Microsoft is from its June 30, 2012 Form 10-K and the data for Intel are from its

December 29, 2012 Form 10-K. Dollars amounts are in millions.

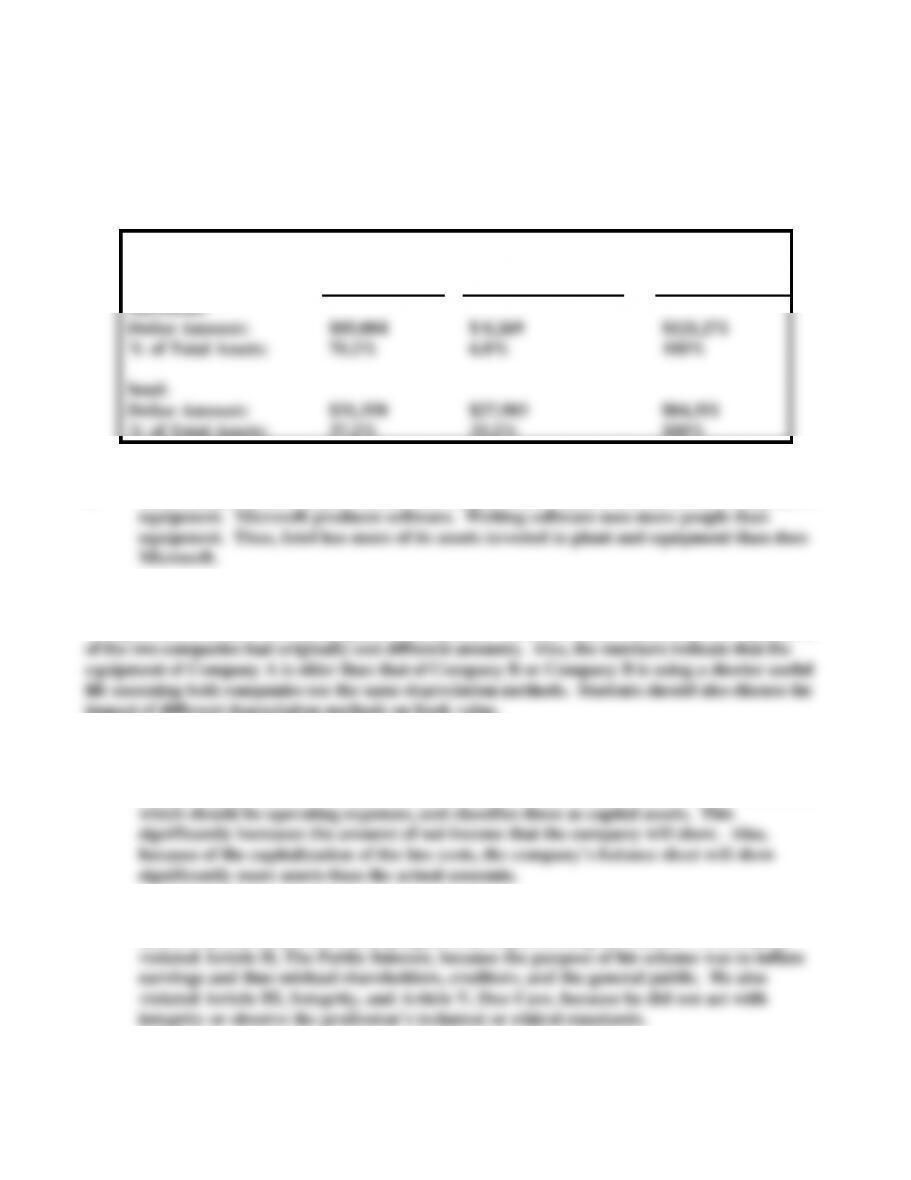

a.

Current

Assets

Property, Plant

and Equipment

Total

Assets

Microsoft:

Dollar Amount:

$85,084

$ 8,269

$121,271

% of Total Assets:

70.2%

6.8%

100%

Intel:

Dollar Amount:

$31,358

$27,983

$84,351

% of Total Assets:

37.2%

33.2%

100%

b. Intel manufactures computer hardware (chips). This requires the use of lots of expensive

ATC 6-4

This problem is used to test thinking and writing skills. Students should realize that the equipment

impact of different depreciation methods on book value.

ATC 6-5

a. As stated in the problem, operating expenses reduce the amount of net income the

company presents on the income statement. Mr. Blowhard’s scheme takes the line costs,

b. Mr. Blowhard’s accountant violated Article I, Responsibilities. He did not exercise

sensitive professional and moral judgment by implementing the scheme. He certainly

c. The three elements of the fraud triangle are opportunity, pressure and rationalization.

Mr. Blowhard’s problem was that he wanted to sell the company and retire wealthy, and

6-9