Chapter 06 – Accounting for Long-Term Operational Assets

6-1

General Comments for Chapter 6

Accounting for Long-Term Operational Assets

This chapter explains how acquiring, using, and disposing of long-term operational assets

affect financial statements. Because these activities span several accounting periods, we

recommend using a multicycle teaching model to illustrate accounting for them. Use a model

that presents financial statements vertically and accounting cycles horizontally. Students will see

how depreciation accumulates on the balance sheet and how cash flows occur in different periods

from expense recognition. You can visually portray the connections between asset usage and

revenue generation. The multicycle model is a powerful classroom learning tool.

The chapter covers basket purchases, alternative depreciation computations, revising

estimates and capital versus revenue expenditures, as well as depreciation, depletion, and

amortization. Considerable effort has been devoted to thinning the material into a manageable

set of concepts that all students will find useful. For example, the text omits the sum-of-the-

years’ digits method and partial period depreciation as well as depreciation for tax purposes.

Detailed Outline of a Lesson Plan for Chapter 6

I. Demonstration Problem 6-1 is based on a business that purchases an automobile

and then leases it to a customer. The problem illustrates three different depreciation

methods across four years.

A. Begin the problem by briefly discussing how to determine asset cost. The general

rule is that the cost of an asset includes any expenditure reasonably necessary to

obtain the asset and get it ready to use. With respect to Demonstration Problem 6-1

the automobile cost is $20,000 ($19,000 list − $1,000 cash discount + $2,000 interior

upgrade). The asset has a four-year useful life and a $4,000 salvage value.

B. Scenario 1. Explain that recognizing depreciation expense means allocating to

expense a portion of the cost of an operational asset. Next, have students calculate

depreciation expense for each of the four years using the straight-line method.

Briefly explain how depreciation is calculated using the straight-line method. When

most of the students have had ample time to work out the annual depreciation

expense, put the answer on the board so they can check their work. The annual

straight-line depreciation expense is $4,000 per year [($20,000 − $4,000) ÷ 4].

After they have determined the straight-line depreciation expense, have students

prepare financial statements for the first accounting cycle. You can save time by

using the work papers included in this manual. Computations for Scenario 1

(straight-line depreciation) are shown below:

Year 2014

1. Revenue. The problem specifies the 2014 revenue, $7,200.

6-3

C. Scenario 2. Before proceeding to Scenario 2 you will need to show your students

how to compute double-declining-balance depreciation. The computations are shown

below for your convenience:

Year

(Cost

─

Accumulated

Depreciation)

x

(2 x Straight-

Line Rate)

=

Depreciation

Expense

2014

(20,000

─

$ -0-)

x

.5

=

$10,000

2015

(20,000

─

10,000)

x

.5

=

5,000

2016

(20,000

─

15,000)

x

.5

=

1,000*

2017

(20,000

─

16,000)

x

.5

=

0*

*The 2016 formula yields $2,500. However, only $1,000 can be charged

because the asset cannot be depreciated below its salvage value.

Similarly, the amount of depreciation recognized in 2017 is zero because

the asset has been fully depreciated.

After you have shown students how to compute depreciation expense, have them

complete the financial statements. Again, using the work papers will save class time.

We suggest you help the students get started by working through the 2014 statements

step by step. The logic for determining the amounts on the statements is described

above in the explanation for Scenario 1. Although amounts for some items differ, the

logic is the same.

Once the students have completed the financial statements, it is a good idea to

have them compare Scenario 2 statements with Scenario 1 statements. Point out that

the end result is the same under either method. The difference lies in the timing

rather than the total amount of expense recognized. Point out that the scenarios

involve different amounts of revenue recognition and cash flow each year (although

the same amounts for the term of the lease as a whole).

D. Scenario 3. Before proceeding to Scenario 3 you will need to show your students

how to compute units-of-production depreciation. The computations are shown

below for your convenience:

Begin by determining the depreciation cost per mile:

(Cost − Salvage Value) ÷ Number of Miles = Depreciation Cost Per Mile

($20,000 − $4,000) ÷ 100,000 = $0.16 per mile

Determine the annual depreciation expense by multiplying the number of miles

driven during the year by the depreciation cost per mile.

Year

Miles Driven

x

Cost Per Mile

=

Depreciation Expense

2014

30,000

x

0.16

=

$4,800

2015

10,000

x

0.16

=

1,600

2016

40,000

x

0.16

=

6,400

2017

25,000

x

0.16

=

3,200*

Chapter 06 – Accounting for Long-Term Operational Assets

6-4

*The 2017 formula yields $4,000. However, only $3,200 can

be charged because the asset cannot be depreciated below its

salvage value.

After you have shown students how to compute depreciation expense, have them

complete the financial statements. Again, help them get started by working through

the 2014 statements step by step. The logic for determining the amounts on the

statements is described above in the explanation for Scenario 1. Although amounts

for some items differ, the logic is the same. Students are likely to need less help for

this scenario than they needed before.

Once the students have completed the financial statements, it is a good idea to

have them compare the financial statements generated under all three scenarios.

Emphasize that the end result is the same regardless of depreciation method. The

difference lies in the timing rather than the total amount of expense recognized.

II. Demonstration Problem 6-2 introduces accounting for capital expenditures and

maintenance costs incurred after the acquisition date. The objectives are twofold: to

illustrate how maintenance costs affect the financial statements differently than capital

expenditures; and to show how capital expenditures made to improve the quality of an

asset differ from those made to extend the useful life of the asset. The statements model

is suited to these instructional objectives. Draw or display a statements model. Then

show students how maintenance costs and capital expenditures affect financial statements

differently.

III. Introduce accounting for natural resources. Highlight the similarities between units-

of-production depreciation and depletion. Use Exercise 6-18 as a demonstration

problem.

IV. Introduce accounting for intangible assets. Highlight the similarities between straight-

line depreciation and amortization computations. Use Exercise 6-19 as a demonstration

problem.

V. Time considerations and homework assignments. Plan to spend approximately one

hour of class time on the different depreciation methods. Allow an additional hour to

cover related subjects such as basket purchases and accounting for capital expenditures,

depletion, and amortization of intangibles. Problem 6-28 is a multicycle problem that

will allow students to see how depreciation affects financial statements over an asset’s

life cycle. Problem 6-23 requires applying different depreciation methods to the same

asset. Students will see that the amount of expense recognized in any single accounting

period is affected by the type of depreciation method chosen. Exercise 6-17 involves

capital expenditures. Problem 6-30 covers depletion. Problems 6-32 and 6-33 address

intangible assets.

Chapter 06 – Accounting for Long-Term Operational Assets

6-5

Demonstration Problems for Chapter 6

Demonstration Problem 6-1: Alternative Depreciation Methods

The following events pertain to Sanders Rental Company (SRC).

1. SRC was started when it issued common stock for $21,000 cash.

2. On January 1, 2014, SRC paid cash to purchase an automobile. The car dealer gave SRC a

$1,000 cash discount off the $19,000 list price. However, SRC paid an additional $2,000 to

equip the car with a more luxurious interior so it would have greater appeal to its clientele.

Sanders Rental Company expected the car to have a four-year useful life and a $4,000

salvage value. SRC expected to lease the car for 100,000 miles before disposing of it.

3. SRC leased the car to a customer who drove it 30,000 / 10,000 / 40,000 / 25,000 miles

during 2014, 2015, 2016, and 2017, respectively. SRC sold the car on January 1, 2018, for

$4,300 cash.

4. Assume SRC recognized depreciation expense using one of three separate scenarios. The

revenue stream and amounts of cash flows assumed for each scenario are shown below:

Revenue Stream

Scenario

2014

2015

2016

2017

1

$ 7,200

$7,200

$7,200

$7,200

2

$13,200

$8,200

$4,200

$3,200

3

$ 8,000

$4,800

$9,600

$6,400

Use the following depreciation method for each of the scenarios.

Scenario

Depreciation Method

1

Straight-Line

2

Double-Declining-Balance

3

Units-of-Production

Required

Prepare income statements, balance sheets, and statements of cash flows for 2014 through 2017

for each of the three scenarios.

Chapter 06 – Accounting for Long-Term Operational Assets

6-6

Education.

Demonstration Problem 6-2: Capital vs. Revenue Expenditures

The following statements model depicts the financial condition of Boston Mechanical Company

just prior to an expenditure of $1,000 cash.

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

Cash

+

Equip.

+

Accum.

Dep.

=

Ret. Ear.

1,000

+

5,000

−

(2,000)

=

-0-

+

4,000

-0-

–

-0-

=

-0-

-0-

Required

Show the effects of the expenditure on the statements model under the following three separate

scenarios.

1. The $1,000 was paid for routine maintenance cost.

2. The $1,000 was paid to improve the quality of the equipment.

3. The $1,000 was paid to extend the useful life of the equipment.

SOLUTIONS TO

DEMONSTRATION PROBLEM

Demonstration Problem 6-1: Solution, Scenario 1

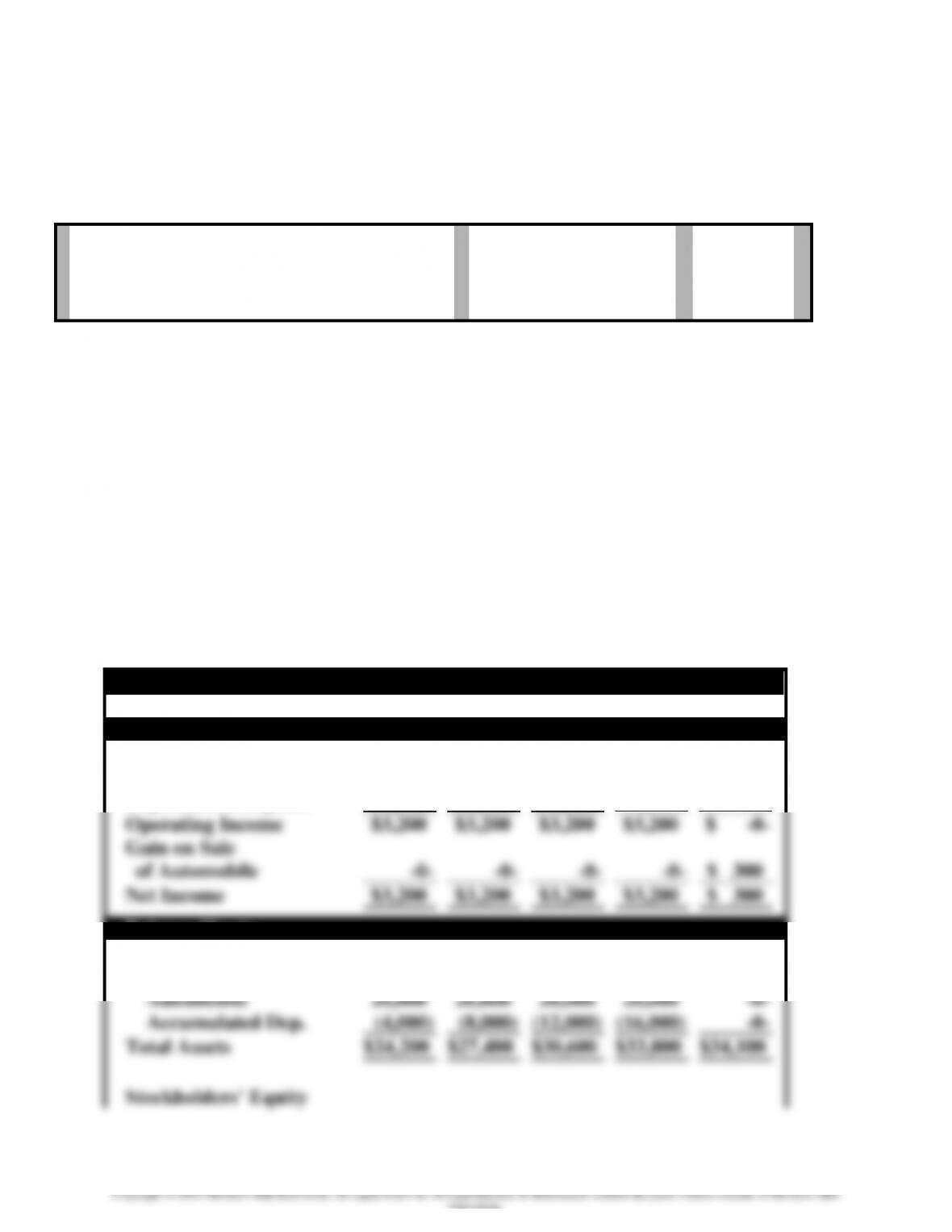

Straight-Line Depreciation

Income Statements

2014

2015

2016

2017

2018

Rent Revenue

$7,200

$7,200

$7,200

$7,200

$ -0-

Depreciation Expense

4,000

4,000

4,000

4,000

-0-

Operating Income

$3,200

$3,200

$3,200

$3,200

$ -0-

Gain on Sale

of Automobile

-0-

-0-

-0-

-0-

$ 300

Net Income

$3,200

$3,200

$3,200

$3,200

$ 300

Balance Sheets

Assets

Cash

$ 8,200

$15,400

$22,600

$29,800

$34,100

Automobile

20,000

20,000

20,000

20,000

-0-

Accumulated Dep.

(4,000)

(8,000)

(12,000)

(16,000)

-0-

Total Assets

$24,200

$27,400

$30,600

$33,800

$34,100

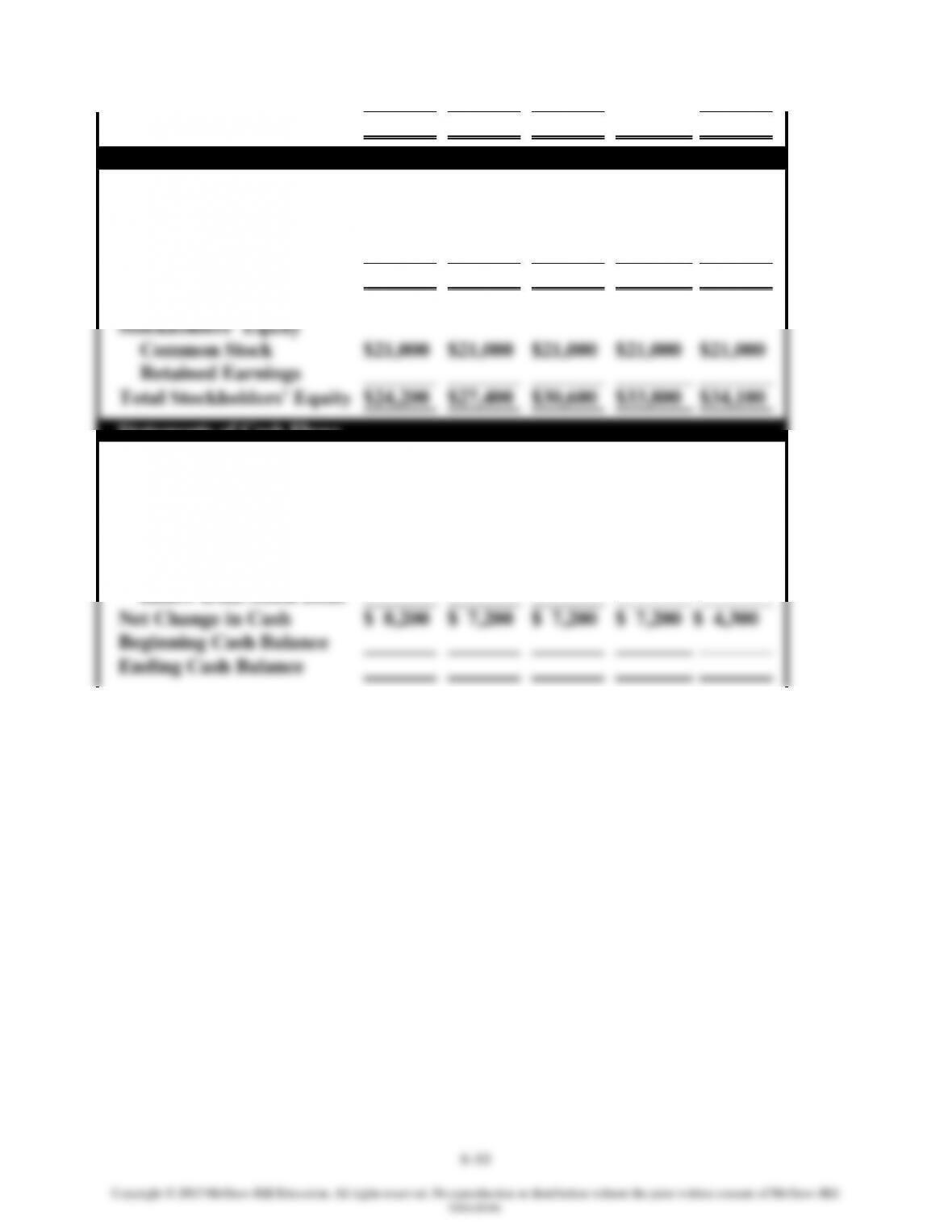

Stockholders’ Equity

Chapter 06 – Accounting for Long-Term Operational Assets

6-7

Education.

Common Stock

$21,000

$21,000

$21,000

$21,000

$21,000

Retained Earnings

3,200

6,400

9,600

12,800

13,100

Total Stockholders’ Equity

$24,200

$27,400

$30,600

$33,800

$34,100

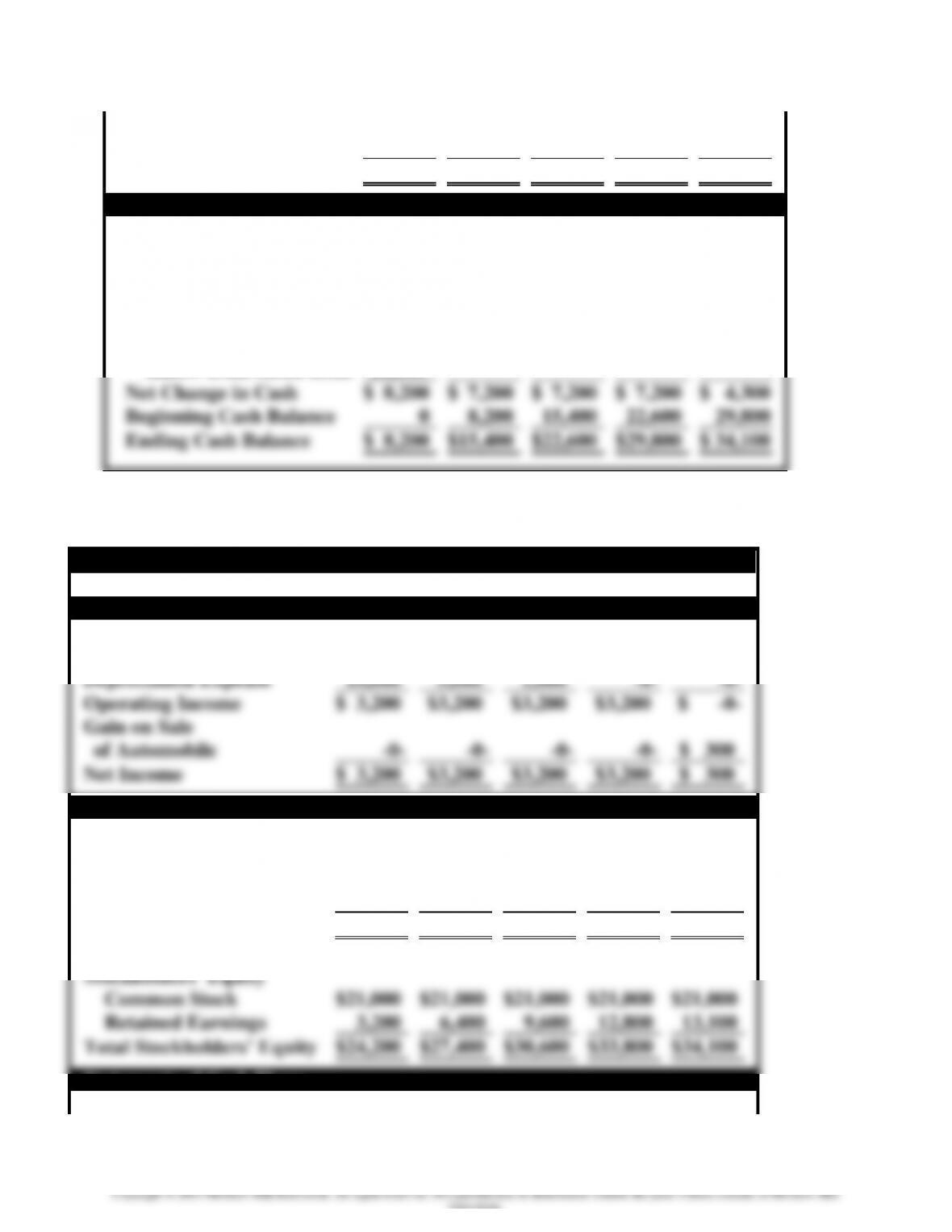

Statements of Cash Flows

Operating Activities

Inflow from Customer

$ 7,200

$ 7,200

$ 7,200

$ 7,200

$ -0-

Investing Activities

Outflow for Automobile

(20,000)

Inflow from Sale of Auto

4,300

Financing Activities

Inflow from Stock Issue

21,000

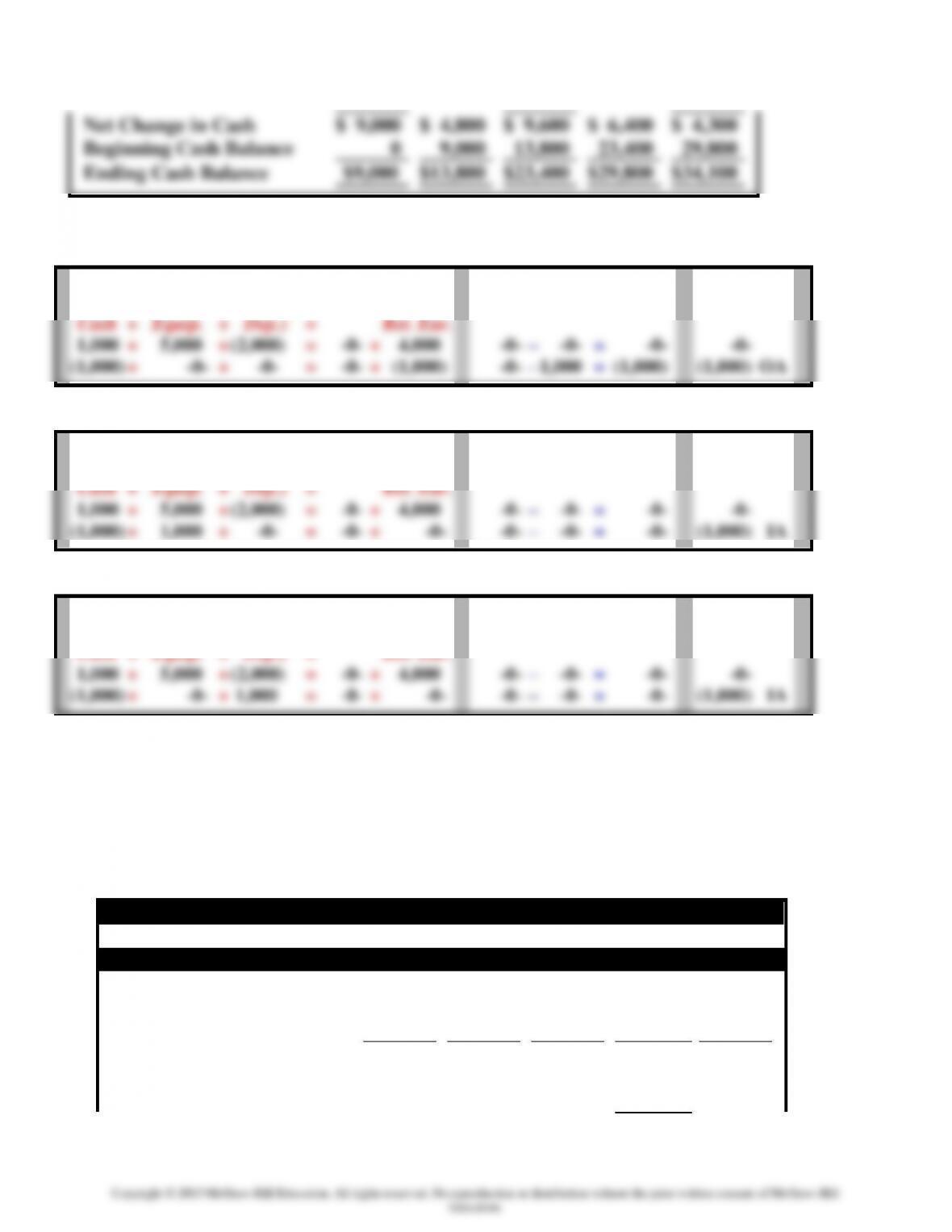

Net Change in Cash

$ 8,200

$ 7,200

$ 7,200

$ 7,200

$ 4,300

Beginning Cash Balance

0

8,200

15,400

22,600

29,800

Ending Cash Balance

$ 8,200

$15,400

$22,600

$29,800

$ 34,100

Demonstration Problem 6-1: Solution, Scenario 2

Double-Declining-Balance Depreciation

Income Statements

2014

2015

2016

2017

2018

Rent Revenue

$13,200

$8,200

$4,200

$3,200

$ -0-

Depreciation Expense

10,000

5,000

1,000

-0-

-0-

Operating Income

$ 3,200

$3,200

$3,200

$3,200

$ -0-

Gain on Sale

of Automobile

-0-

-0-

-0-

-0-

$ 300

Net Income

$ 3,200

$3,200

$3,200

$3,200

$ 300

Balance Sheets

Assets

Cash

$14,200

$22,400

$26,600

$29,800

$34,100

Automobile

20,000

20,000

20,000

20,000

-0-

Accumulated Dep.

(10,000)

(15,000)

(16,000)

(16,000)

-0-

Total Assets

$24,200

$27,400

$30,600

$33,800

$34,100

Stockholders’ Equity

Common Stock

$21,000

$21,000

$21,000

$21,000

$21,000

Retained Earnings

3,200

6,400

9,600

12,800

13,100

Total Stockholders’ Equity

$24,200

$27,400

$30,600

$33,800

$34,100

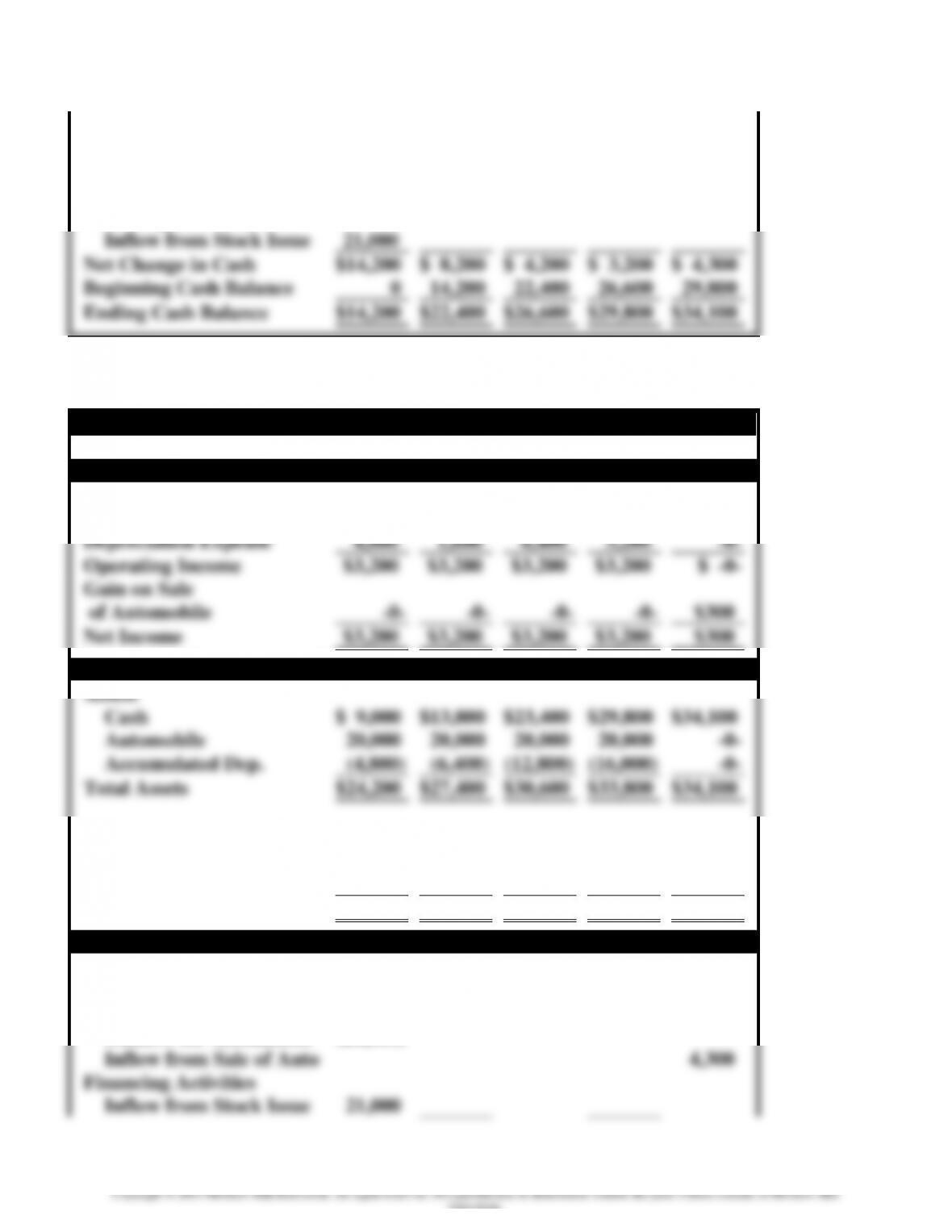

Statements of Cash Flows

Operating Activities

Chapter 06 – Accounting for Long-Term Operational Assets

6-8

Education.

Inflow from Customer

$13,200

$8,200

$4,200

$3,200

$ -0-

Investing Activities

Outflow for Automobile

(20,000)

Inflow from Sale of Auto

4,300

Financing Activities

Inflow from Stock Issue

21,000

Net Change in Cash

$14,200

$ 8,200

$ 4,200

$ 3,200

$ 4,300

Beginning Cash Balance

0

14,200

22,400

26,600

29,800

Ending Cash Balance

$14,200

$22,400

$26,600

$29,800

$34,100

Demonstration Problem 6-1: Solution, Scenario 3

Units-of-Production Depreciation

Income Statements

2014

2015

2016

2017

2018

Rent Revenue

$8,000

$4,800

$9,600

$6,400

$ -0-

Depreciation Expense

4,800

1,600

6,400

3,200

-0-

Operating Income

$3,200

$3,200

$3,200

$3,200

$ -0-

Gain on Sale

of Automobile

-0-

-0-

-0-

-0-

$300

Net Income

$3,200

$3,200

$3,200

$3,200

$300

Balance Sheets

Assets

Cash

$ 9,000

$13,800

$23,400

$29,800

$34,100

Automobile

20,000

20,000

20,000

20,000

-0-

Accumulated Dep.

(4,800)

(6,400)

(12,800)

(16,000)

-0-

Total Assets

$24,200

$27,400

$30,600

$33,800

$34,100

Stockholders’ Equity

Common Stock

$21,000

$21,000

$21,000

$21,000

$21,000

Retained Earnings

3,200

6,400

9,600

12,800

13,100

Total Stockholders’ Equity

$24,200

$27,400

$30,600

$33,800

$34,100

Statements of Cash Flows

Operating Activities

Inflow from Customer

$ 8,000

$ 4,800

$ 9,600

$ 6,400

$ -0-

Investing Activities

Outflow for Automobile

(20,000)

Inflow from Sale of Auto

4,300

Financing Activities

Inflow from Stock Issue

21,000

Chapter 06 – Accounting for Long-Term Operational Assets

6-9

Net Change in Cash

$ 9,000

$ 4,800

$ 9,600

$ 6,400

$ 4,300

Beginning Cash Balance

0

9,000

13,800

23,400

29,800

Ending Cash Balance

$9,000

$13,800

$23,400

$29,800

$34,100

Demonstration Problem 6-2: Solution

1. Paid $1,000 cash for routine maintenance cost.

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

Cash

+

Equip.

+

(Accum.

Dep.)

=

Ret. Ear.

1,000

+

5,000

+

(2,000)

=

-0-

+

4,000

-0-

–

-0-

=

-0-

-0-

(1,000)

+

-0-

+

-0-

=

-0-

+

(1,000)

-0-

–

1,000

=

(1,000)

(1,000) OA

2. Paid $1,000 cash to improve the quality of the equipment.

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

Cash

+

Equip.

+

(Accum.

Dep.)

=

Ret. Ear.

1,000

+

5,000

+

(2,000)

=

-0-

+

4,000

-0-

–

-0-

=

-0-

-0-

(1,000)

+

1,000

+

-0-

=

-0-

+

-0-

-0-

–

-0-

=

-0-

(1,000) IA

3. Paid $1,000 cash to extend the useful life of the equipment.

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

Cash

+

Equip.

+

(Accum.

Dep.)

=

Ret. Ear.

1,000

+

5,000

+

(2,000)

=

-0-

+

4,000

-0-

–

-0-

=

-0-

-0-

(1,000)

+

-0-

+

1,000

=

-0-

+

-0-

-0-

–

-0-

=

-0-

(1,000) IA

WORK PAPERS FOR

DEMONSTRATION PROBLEMS

Demonstration Problem 6-1: Work Paper, Scenario 1

Straight-Line Depreciation

Income Statements

2014

2015

2016

2017

2018

Rent Revenue

$7,200

$7,200

$7,200

$7,200

$ -0-

Depreciation Expense

Operating Income

Gain on Sale

of Automobile

Chapter 06 – Accounting for Long-Term Operational Assets

Net Income

$ 300

Balance Sheets

Assets

Cash

Automobile

Accumulated Dep.

Total Assets

Stockholders’ Equity

Common Stock

$21,000

$21,000

$21,000

$21,000

$21,000

Retained Earnings

Total Stockholders’ Equity

$24,200

$27,400

$30,600

$33,800

$34,100

Statements of Cash Flows

Operating Activities

Inflow from Customer

Investing Activities

Outflow for Automobile

Inflow from Sale of Auto

Financing Activities

Inflow from Stock Issue

Net Change in Cash

$ 8,200

$ 7,200

$ 7,200

$ 7,200

$ 4,300

Beginning Cash Balance

Ending Cash Balance