Chapter 04 – Internal Controls, Accounting for Cash, and Ethics

4-1

General Comments for Chapter 4

Internal Controls, Accounting

for Cash, and Ethics

This chapter explains internal controls, which are the policies and procedures used to

provide reasonable assurance that the objectives of an enterprise will be accomplished. While the

mechanics of internal control systems vary from company to company, the chapter presents cash

as an important business asset and special procedures that should be employed to control the re-

ceipts and payments of cash.

One of the most common control policies is to use checking accounts for all payments

except petty cash disbursements. Students learn that a bank reconciliation should be prepared

each month to explain differences between the bank statement and a company’s internal account-

ing records. A common reconciliation format determines the true cash balance based on both

bank and book records. Items that typically appear on a bank reconciliation include the follow-

ing: the bank balance, deposits in transit, outstanding checks, the book balance, interest revenue

collected by the bank, receivables collected by the bank, bank service charges, and non-sufficient

funds (NSF) checks. Agreement of the two true cash balances (Bank versus Book) provides evi-

dence that accounting for cash transactions has been accurate.

The chapter also discusses the importance of ethics in the accounting profession. The

American Institute of Public Accountants requires all of its members to comply with the Code of

Professional Conduct. Situations where opportunity, pressure, and rationalization exist can lead

employees to conduct unethical acts, which, in cases like Enron, have destroyed the organization.

Finally, the chapter discussed the auditor’s role in financial reporting, including the materiality

concept and the types of audit opinions that may be issued.

Consider beginning the chapter with a discussion of internal controls and a question

about a practice familiar to your students. For example, ask why a movie theater uses one person

to sell tickets and another to collect them as patrons enter the theater. Couldn’t the theater save

money by using one employee to both sell and collect the tickets? Such a question leads into

discussing separation of duties. Similarly, you may ask why a department store requires two

clerks to sign a receipt for returned merchandise, or why some convenience stores post a sign by

the cash register offering each customer a cash reward if the cashier fails to give the customer a

receipt. After a brief introduction most students can grasp the internal control concepts by

reading the chapter material. As a lead-in to preparing a bank reconciliation, you may wish to

explain why companies need good internal controls for cash and provide examples of appropriate

controls. This will then lead to the fraud triangle, why the control of cash is so important, and the

accountant’s role in society requires trust, credibility, and ethics.

Chapter 04 – Internal Controls, Accounting for Cash, and Ethics

4-2

Detailed Outline of a Lesson Plan for Chapter 4

I. Begin the discussion of internal controls with a brief introduction about the nature

and purpose of internal controls. Students should be able to learn the details about

internal control concepts through their reading assignment. Mention that a business needs

good internal controls to protect its cash.

II. Use Demonstration Problem 4-1 to show students how to prepare a bank

reconciliation. Many students have checking accounts and, therefore, some familiarity

with reconciling items. You can stimulate interest by having students help create the

form for the bank reconciliation. Write captions for the unadjusted bank and book

balances on the chalkboard. Point out that neither of these amounts represents the true

amount of cash the company owns. Then ask what could cause differences between the

unadjusted bank balance and the true cash balance. Use student input to develop a form

for determining the true balance from the starting point of the unadjusted bank balance.

Use the same approach to develop a form for computing the true balance when starting

with the unadjusted book balance. Use these forms to work out the solution to

Demonstration Problem 4-3. Alternatively, use the forms provided in this manual.

III. Use Demonstration Problem 4-2 to reinforce bank reconciliation procedures. This

problem requires determining the amount of the unadjusted book balance in the cash

account. It provides sufficient information for students to determine the true cash balance

starting from the unadjusted bank balance. Students must realize that the true cash

balance is the same whether it is determined from the perspective of the unadjusted bank

or the unadjusted book balance. Once students understand this point, they can determine

the unadjusted book balance by working backwards from the true cash balance.

IV. Time considerations and homework assignments. Allot approximately one hour of

class time to cover internal controls and bank reconciliations. Problems 4-21 and 4-22

will provide useful follow-up for Demonstration Problems 4-1 and 4-2. We also

recommend Exercise 4-15 as an introductory problem when discussing the fraud triangle,

with a follow-up homework assignment of Problem 4-24. Exercises 4-13, 4-14, and 4-17

provide good scenarios for discussing the AICPA Professional Code of Conduct and

auditor responsibilities, with follow-up homework assignments of Problem 4-25 and

ATC 4-5.

Chapter 04 – Internal Controls, Accounting for Cash, and Ethics

4-3

Demonstration Problems for Chapter 4

Demonstration Problem 4-1: Bank Reconciliation

The bank statement for Greenbrier Furniture Stores showed a balance of $63,289 as of

November 30. The unadjusted balance in the general ledger cash account at November 30 was

$59,345. An examination of the bank statement disclosed the following information.

1. Outstanding checks totaled $24,598.

2. The bank had issued a $157 credit memo for interest deposited into Greenbrier’s account.

3. The bank had deducted $469 for two non-sufficient funds (NSF) checks.

4. The bank statement enclosures included a debit memo for $36 the bank had deducted from

Greenbrier’s account to pay for new checks.

5. Deposits in transit were $19,060.

6. The bank had mistakenly deducted from Greenbrier’s account a $1,246 check drawn on the

Greenbay Company.

Required

a. Reconcile the balance shown on the bank statement and the unadjusted balance of the

company’s cash account to the true cash balance.

b. What is the amount of cash that should be reported on Greenbrier’s balance sheet as of

November 30?

Demonstration Problem 4-2: Bank Reconciliation

The bank statement for Broom Company showed a $200 bank balance at the end of the month.

A comparison of Broom Company’s bank statement and accounting records disclosed a $40

deposit in transit and $55 of outstanding checks at month-end. The bank statement enclosures

included a $5 NSF check and a credit memo for $10 of interest.

Required

a. Determine the unadjusted book balance in the cash account.

b. What is the book balance in Broom’s cash account after the adjusting entries have been

made?

Chapter 04 – Internal Controls, Accounting for Cash, and Ethics

4-4

SOLUTIONS TO

DEMONSTRATION PROBLEMS

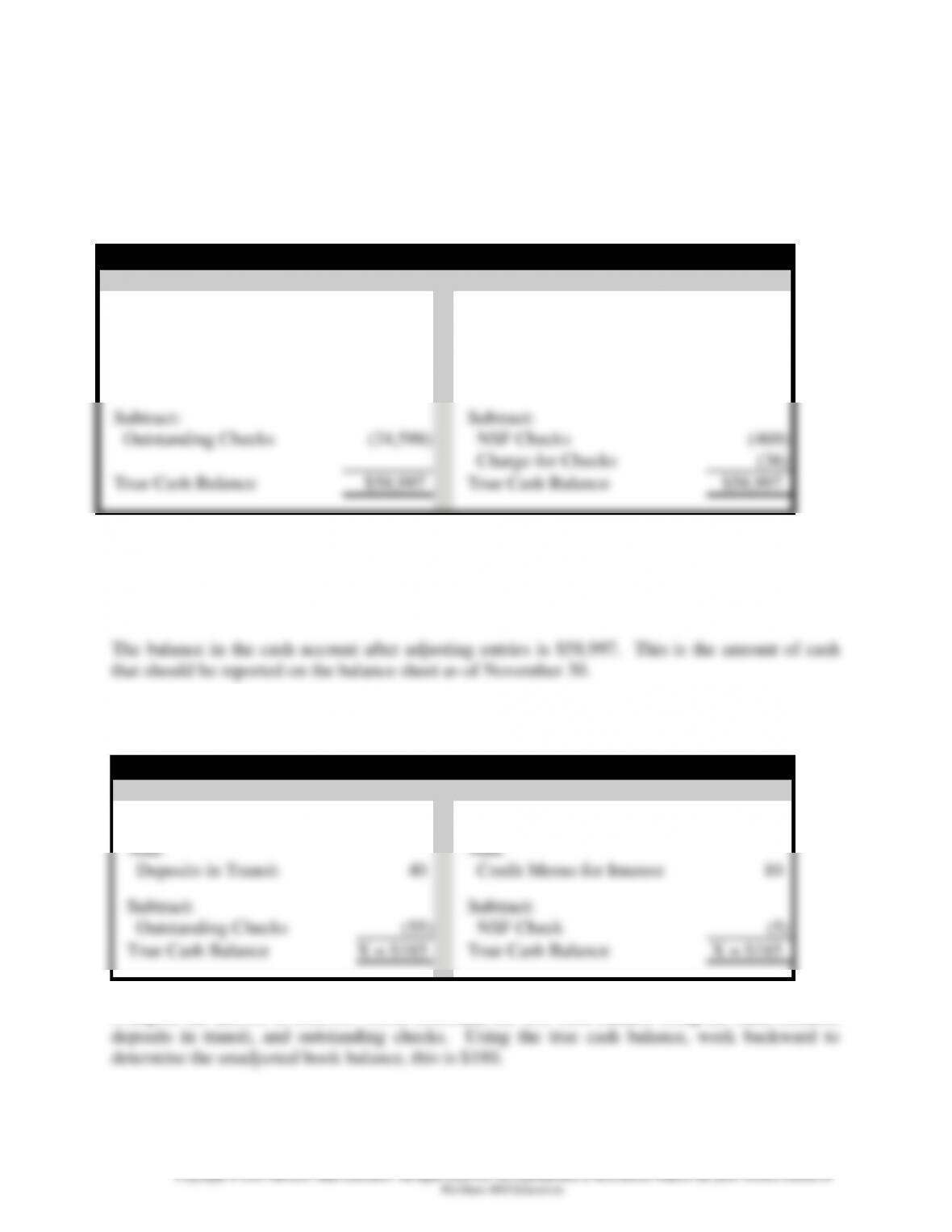

Demonstration Problem 4-1: Solution, part a. Bank Reconciliation

Bank Reconciliation

Unadjusted Bank Balance

$63,289

Unadjusted Book Balance

$59,345

Add:

Add:

Deposits in Transit

19,060

Credit Memo for Interest

157

Bank Error, Greenbay Check

1,246

Subtract:

Subtract:

Outstanding Checks

(24,598)

NSF Checks

(469)

Charge for Checks

(36)

True Cash Balance

$58,997

True Cash Balance

$58,997

Demonstration Problem 4-1: Solution, part b.

Determine Cash Balance

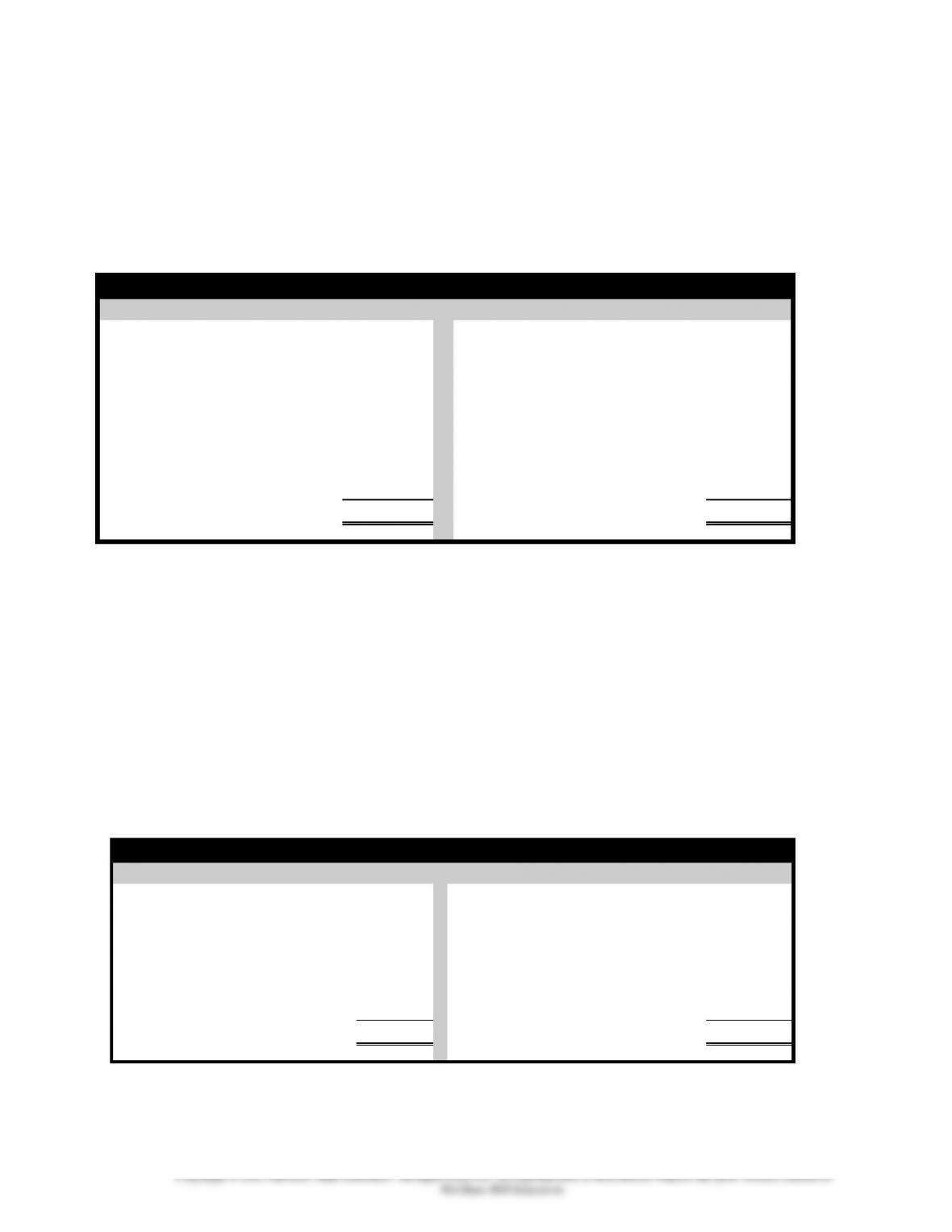

Demonstration Problem 4-2: Solution, part a. Bank Reconciliation

Bank Reconciliation

Unadjusted Bank Balance

$200

Unadjusted Book Balance

Y = $180

Add:

Add:

Deposits in Transit

40

Credit Memo for Interest

10

Subtract:

Subtract:

Outstanding Checks

(55)

NSF Check

(5)

True Cash Balance

X = $185

True Cash Balance

X = $185

Compute the answer as follows: First, determine the true cash balance using the bank balance,

Chapter 04 – Internal Controls, Accounting for Cash, and Ethics

4-5

Demonstration Problem 4-2: Solution, part b.

Determine Cash Balance

The balance in the cash account, after the adjusting entries have been posted to the ledger

Chapter 04 – Internal Controls, Accounting for Cash, and Ethics

4-6

WORK PAPERS FOR

DEMONSTRATION PROBLEMS

Demonstration Problem 4-1: Work Paper, part a. Bank Reconciliation

Bank Reconciliation

Unadjusted Bank Balance

Unadjusted Book Balance

Add:

Add:

Subtract:

Subtract:

True Cash Balance

$58,997

True Cash Balance

$58,997

Demonstration Problem 4-1: Work Paper, part b.

Indicate Amount of Cash to be Reported on Balance Sheet

Demonstration Problem 4-2: Work Paper, part a. Bank Reconciliation

Bank Reconciliation

Unadjusted Bank Balance

$200

Unadjusted Book Balance

Y =

Add:

Add:

Subtract:

Subtract:

True Cash Balance

X =

True Cash Balance

X =

Chapter 04 – Internal Controls, Accounting for Cash, and Ethics

4-7

Demonstration Problem 4-2: Work Paper, part b.

Indicate Book Balance of the Cash Account

Chapter 04 – Internal Controls, Accounting for Cash, and Ethics

4-8

Quiz Questions for Chapter 4

1. Mary Wilson is an accounting clerk for a large department store. Her husband owns an office supply

business. Mary paid her husband’s business for supplies the department store never received. Which of

the following practices would allow Mary to perpetrate this scam?

a. Keeping prenumbered checks under lock and key.

b. Allowing a single person to approve disbursements, sign checks, and reconcile the checking

account.

c. Requiring one employee to approve supporting documents and a different employee to sign

checks.

d. Marking supporting documents “paid” when checks are signed.

2. RST’s bank statement included an NSF check that one of its customers had written to pay its account

receivable. How would recording the NSF check affect RST’s accounting equation?

a. Increase assets / decrease liabilities.

b. Have no effect on total assets, liabilities, or equity.

c. Decrease assets / increase liabilities.

d. Increase liabilities / decrease equity.

3. X Company’s unadjusted cash balance at the end of October was $14,350. Other relevant information

is: deposits in transit, $2,300; a credit memo in the bank statement for interest earned, $500; a check for

$50 incorrectly recorded as $55 by the company’s accountant; a debit memo in the bank statement for

an $8 bank service charge; and outstanding checks, $2,100. The true cash balance on October 31 was

a. $14,850.

b. $14,550.

c. $14,537.

d. $14,847.

4. EFG Company’s bank statement reported an unadjusted bank account balance of $20,900 at the end of

February. Analyzing the February bank statement disclosed the following:

Credit memo for funds the bank had collected on a note receivable, $800

Deposits in transit, $1,420

Debit memo for service charge, $6.50

Outstanding checks, $750

NSF check, $310

The true cash balance at the end of February was

a. $21,260.00.

b. $22,053.50.

c. $21,570.00.

d. $22,370.00.

5. Which of the following is true?

a. Internal controls are unnecessary when key employees are bonded.

b. Experienced accounting clerks need not use prenumbered documents.

c. The practice of separating duties prevents an employee from both approving a refund and

disbursing the cash.

d. Administrative controls would limit access to physical assets but not to accounting records.

6. A company can protect itself from dishonest employees by obtaining

a. a signature card.

b. a certified check.

c. an outstanding check.

d. a fidelity bond.

7. There are three elements typically present when fraud occurs. These are

Chapter 04 – Internal Controls, Accounting for Cash, and Ethics

4-9

a. Opportunity, internal controls and pressure.

b. Opportunity, pressure and rationalization.

c. Pressure, rationalization and expenses.

d. Rationalization, opportunity and independence.

8. All of the following are true about the primary roles of an independent auditor (CPA) except:

a. The auditor maintains professional confidentiality of client records.

b. The auditor assumes both legal and professional responsibilities to the public as well as to the company

paying the auditor.

c. The auditor presents conclusions in audit reports that include an opinion about whether statements are

prepared in conformity with GAAP.

d. The auditor determines if financial statements are completely accurate.

Chapter 04 – Internal Controls, Accounting for Cash, and Ethics

4-10

Solutions to Quiz Questions

Question

Answer

1

B

2

B

3

D

4

C

5

C

6

D

7

B

8

D

Chapter 04 – Internal Controls, Accounting for Cash, and Ethics

4-11

Summary Outline of a Lesson Plan for Chapter 4

I. Begin with a brief introduction about the nature and purpose of internal controls.

Offer a few familiar internal control examples.

II. Use Demonstration Problem 4-1 to show students how to prepare a bank

reconciliation.

III. Use Demonstration Problem 4-2 to reinforce bank reconciliation procedures.

IV. Time considerations and homework assignments. Allot approximately one hour of

class time to cover internal controls and bank reconciliations. Problems 4-21 and 4-22

will provide useful follow-up for Demonstration Problems 4-1 and 4-2. We also

recommend Exercise 4-15 as an introductory problem when discussing the fraud triangle,

with a follow-up homework assignment of Problem 4-24. Exercises 4-13, 4-14, and 4-17

provide good scenarios for discussing the AICPA Professional Code of Conduct and

auditor responsibilities, with follow-up homework assignments of Problem 4-25 and

ATC 4-5.