a.

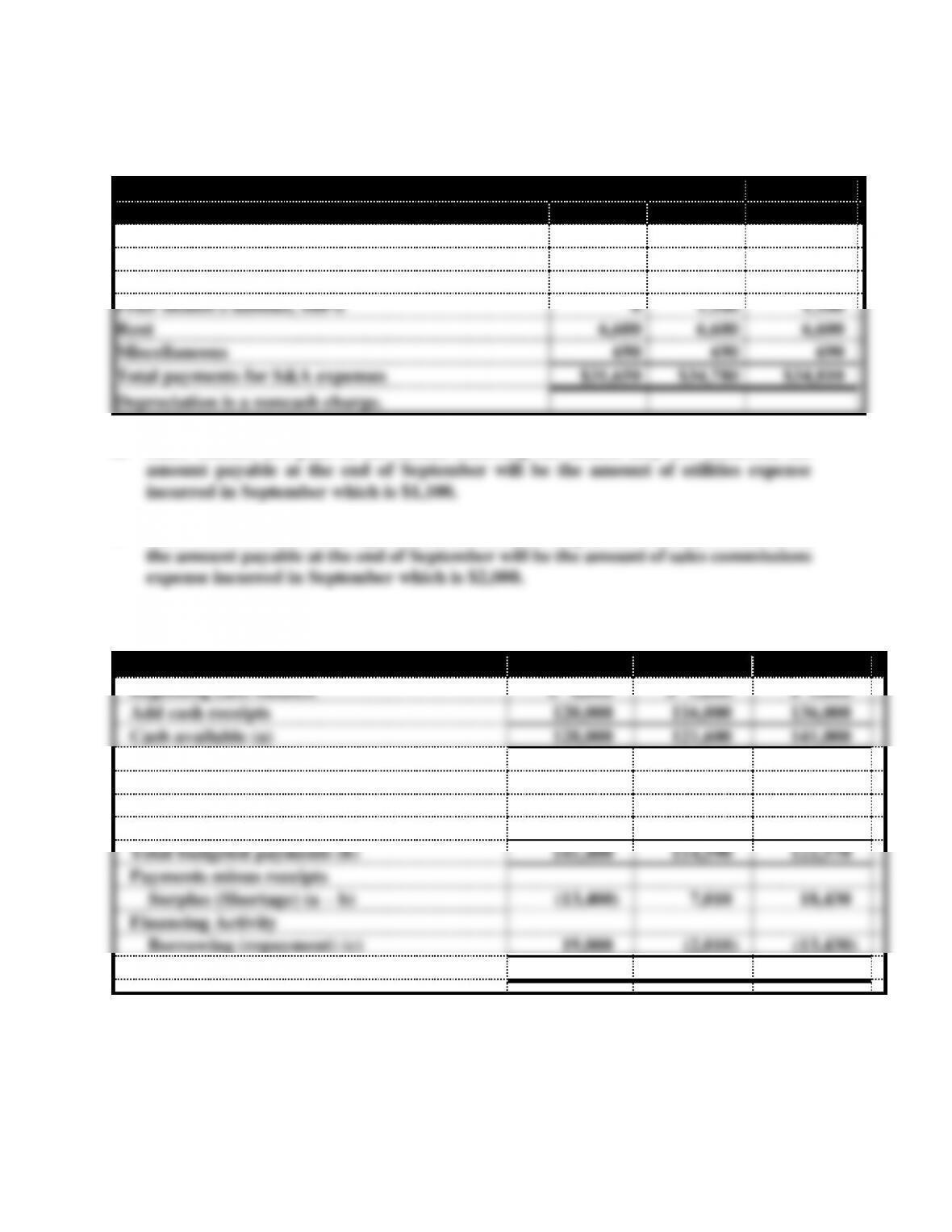

Schedule of Cash Payments for S&A Expenses

July

August

September

Salary expense

$24,000

$24,000

$24,000

Prior month’s sales commissions, 100%

0

2,000

2,000

Supplies expense

360

390

420

Prior month’s utilities, 100%

0

1,100

1,100

Rent

6,600

6,600

6,600

Miscellaneous

690

690

690

Total payments for S&A expenses

$31,650

$34,780

$34,810

Depreciation is a noncash charge.

b. Since utilities are paid in the month following the month they are incurred, the

c. Since sales commissions are paid in the month following the month they are incurred,

Problem 14-20

Cash Budget

January

February

March

Beginning cash balance

$ 8,000

$ 5,600

$ 5,000

Add cash receipts

120,000

116,000

136,000

Cash available (a)

128,000

121,600

141,000

Less cash payments

For inventory purchases

110,000

82,000

95,000

For S&A expenses

31,000

32,000

27,000

Interest exp at 1% per month

4001

5902

5703

Total budgeted payments (b)

141,400

114,590

122,570

Payments minus receipts

Surplus (Shortage) (a – b)

(13,400)

7,010

18,430

Financing Activity

Borrowing (repayment) (c)

19,000

(2,010)

(13,430)

Ending cash balance (a – b + c)

$ 5,600

$ 5,000

$ 5,000

1($40,000) x 1% = $400

2($40,000 + $19,000) x 1% = $590

3($40,000 + $19,000 – $2,010) x 1% = $570 (rounded).

Problem 14-21

This is a typical problem for what-if analysis. Students can use a computerized

spreadsheet to try different possible scenarios.

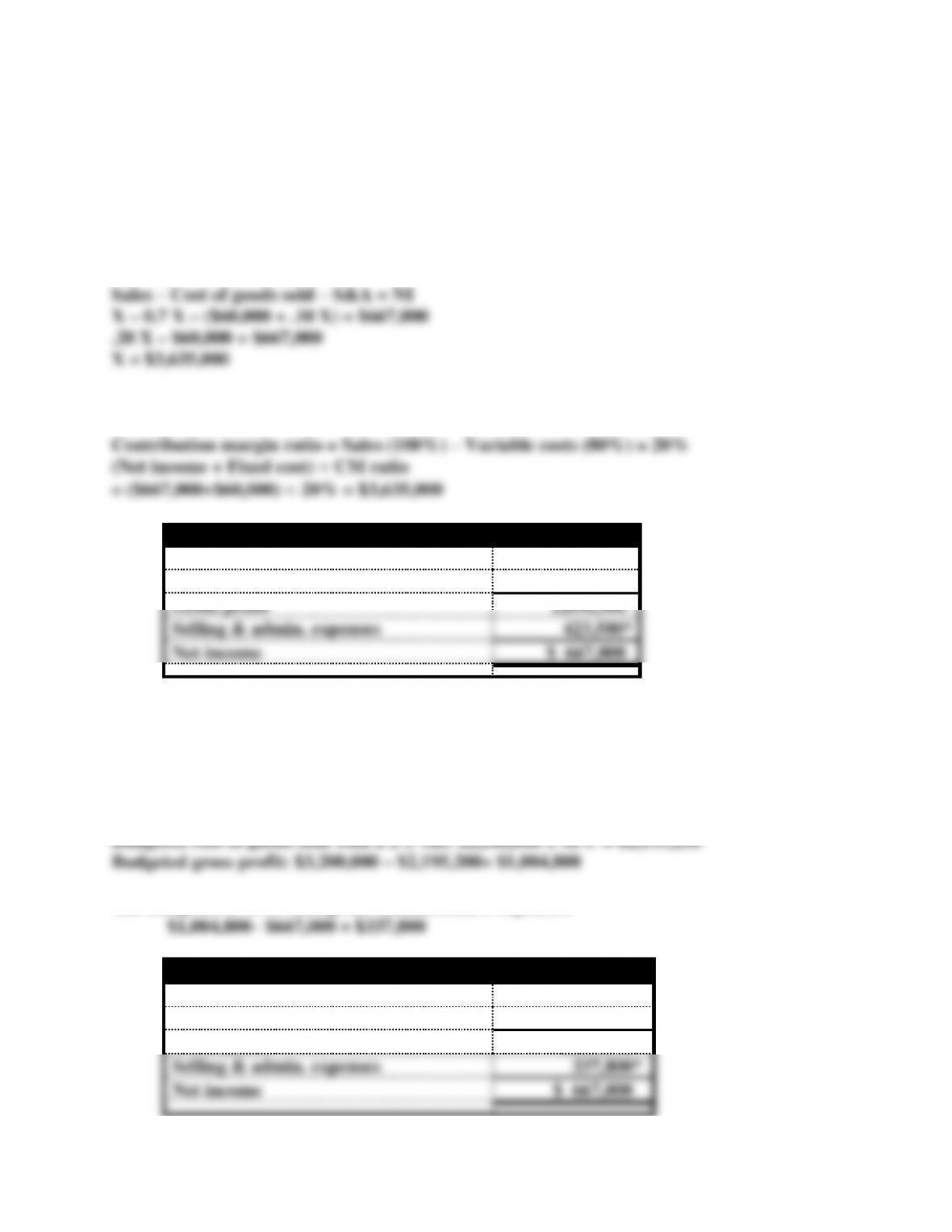

a.

The budgeted net income for the next year: $580,000×115%= $667,000

Assume x = Desired sales

Alternatively, you can use the contribution margin ratio to determine sales.

Pro Forma Income Statement

Sales revenue

$3,635,000

Cost of goods sold

2,544,500

Gross profit

1,090,500

Selling & admin. expenses

423,500*

Net income

$ 667,000

*($3,635,000 x 10% + $60,000) = $423,500

% increase required: ($3,635,000 – $3,200,000) ÷ $3,200,000 = 13.59% (rounded)

Problem 14-21 (continued)

b.

The budgeted level of selling and administrative expenses:

Pro Forma Income Statement

Sales revenue

$3,200,000

Cost of goods sold

2,195,200

Gross profit

1,004,800

Selling & admin. expenses

337,800*

Net income

$ 667,000

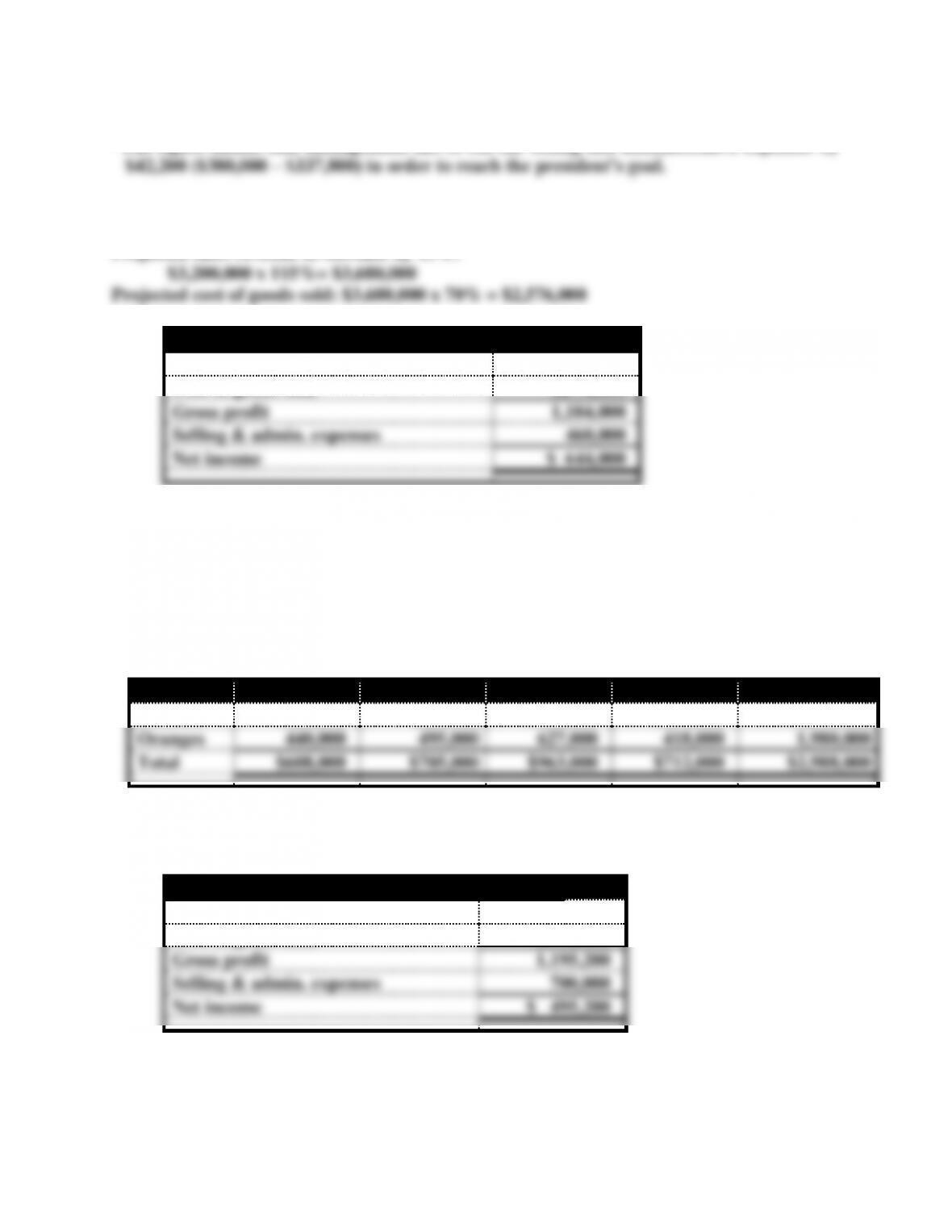

*The figure means that management has to cut the selling and administrative expenses by

c.

Projected sales revenue to increase by 15%:

Pro Forma Income Statement

Sales revenue

$3,680,000

Cost of goods sold

2,576,000

Gross profit

1,104,000

Selling & admin. expenses

460,000

Net income

$ 644,000

Since the projected net income under the given scenario will be only $644,000, which is short

of the original $667,000, the company cannot reach its goal.

Problem 14-22

a.

1st Quarter

2nd Quarter

3rd Quarter

4th Quarter

Total

Peaches

$168,000

$210,000

$336,000

$294,000

$1,008,000

Oranges

440,000

495,000

627,000

418,000

1,980,000

Total

$608,000

$705,000

$963,000

$712,000

$2,988,000

b. Budgeted cost of goods sold: $2,988,000 x 60% = $1,792,800

Budgeted Annual Income Statement

Sales revenue

$2,988,000

Cost of goods sold

1,792,800

Gross profit

1,195,200

Selling & admin. expenses

700,000

Net income

$ 495,200

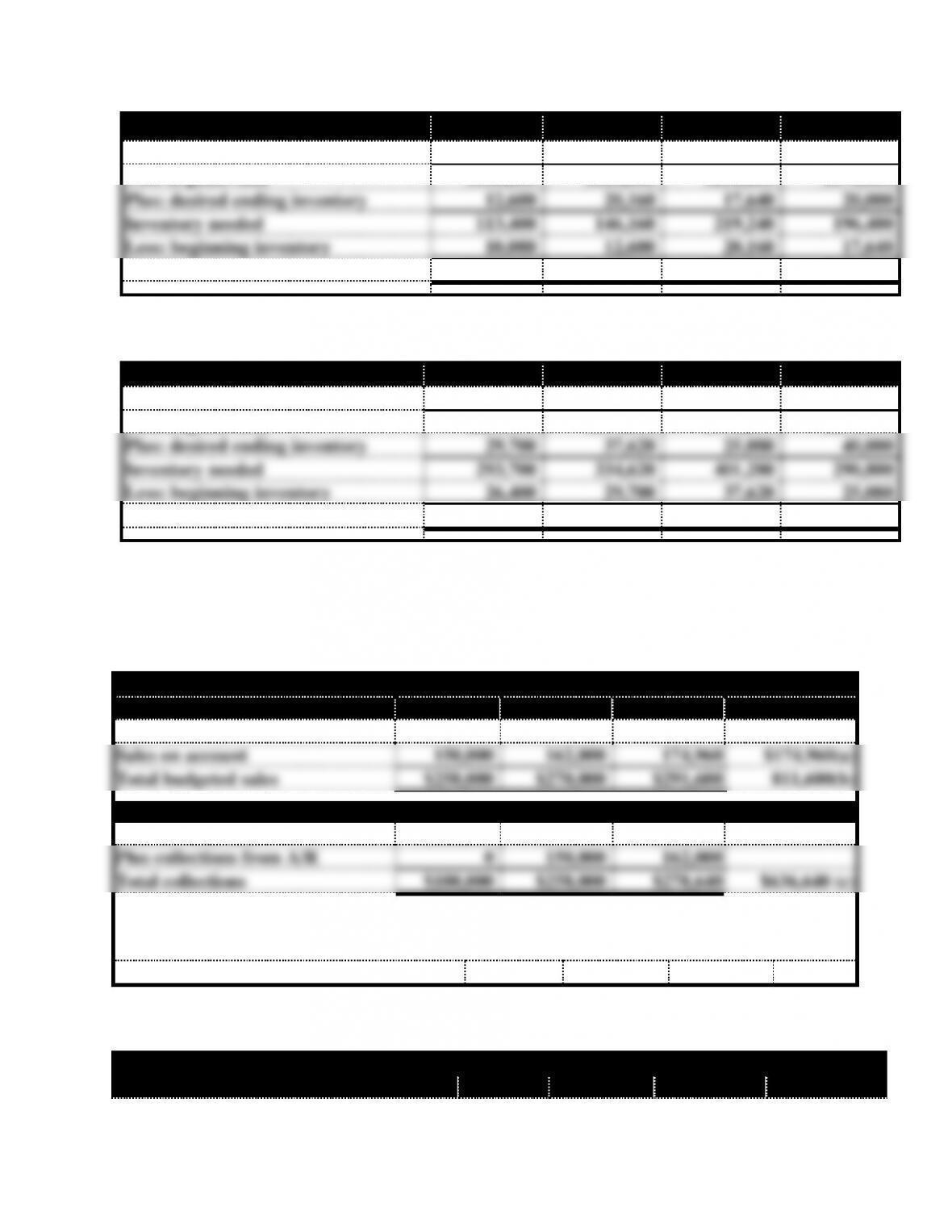

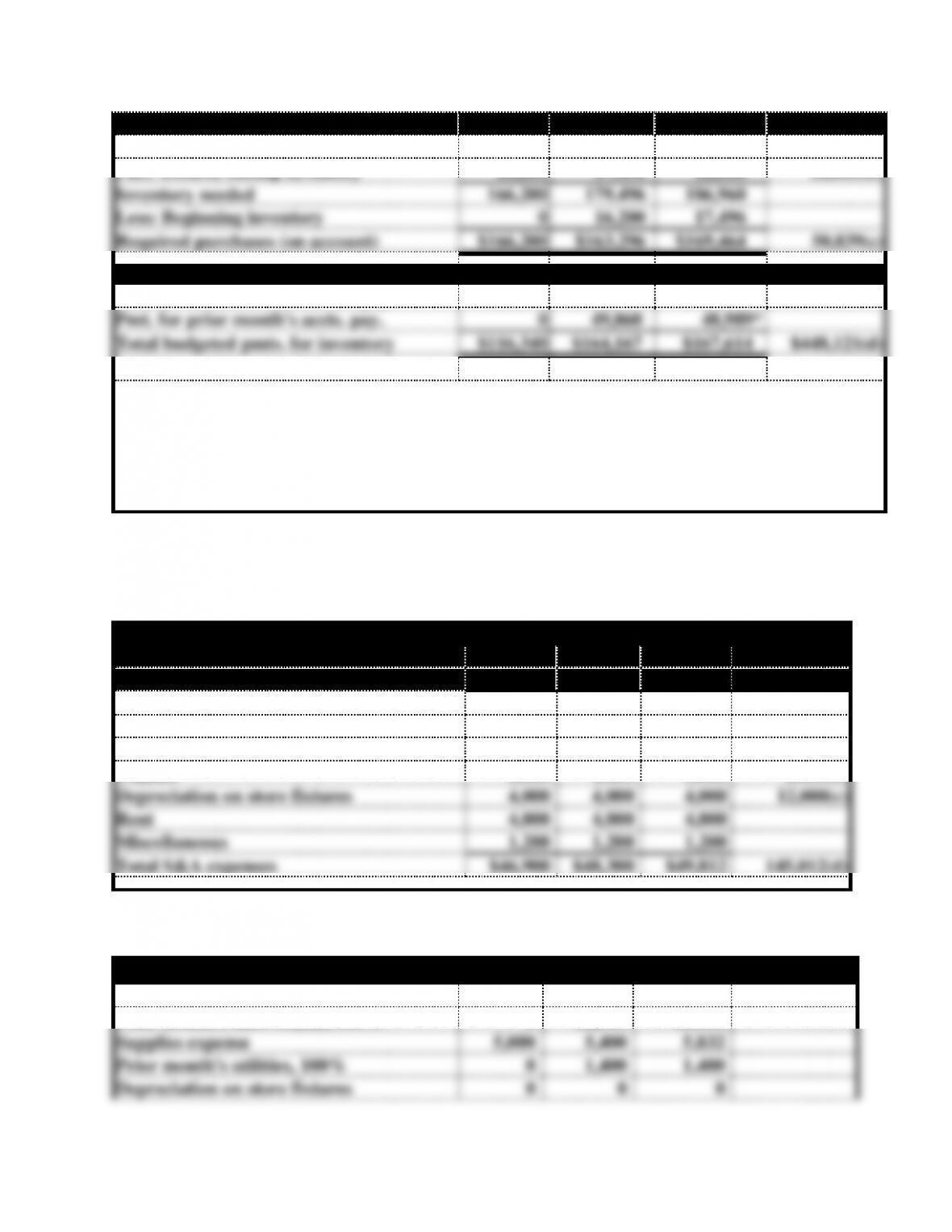

c. Inventory purchases budget for peaches

1st Quarter

2nd Quarter

3rd Quarter

4th Quarter

Sales

$168,000

$210,000

$336,000

$294,000

Cost of goods sold

$100,800

$126,000

$201,600

$176,400

Plus: desired ending inventory

12,600

20,160

17,640

20,000

Inventory needed

113,400

146,160

219,240

196,400

Less: beginning inventory

10,080

12,600

20,160

17,640

Required purchases

$103,320

$133,560

$199,080

$178,760

Inventory purchases budget for oranges

1st Quarter

2nd Quarter

3rd Quarter

4th Quarter

Sales

$440,000

$495,000

$627,000

$418,000

Cost of goods sold

$264,000

$297,000

$376,200

$250,800

Plus: desired ending inventory

29,700

37,620

25,080

40,000

Inventory needed

293,700

334,620

401,280

290,800

Less: beginning inventory

26,400

29,700

37,620

25,080

Required purchases

$267,300

$304,920

$363,660

$265,720

Problem 14-23

(Note: All computations are rounded to the nearest whole dollar.)

a. & b.

Sales Budget

Pro Forma

Oct.

Nov.

Dec.

Data

Cash sales

$100,000

$108,000

$116,640

Sales on account

150,000

162,000

174,960

$174,960(a)

Total budgeted sales

$250,000

$270,000

$291,600

811,600(b)

Schedule of Cash Receipts

Oct.

Nov.

Dec.

Current cash sales

$100,000

$108,000

$116,640

Plus collections from A/R

0

150,000

162,000

Total collections

$100,000

$258,000

$278,640

$636,640 (c)

(a) Ending accounts receivable balance appearing on balance sheet.

(b) Sales revenue appearing on income statement (sum of monthly amounts).

(c) Cash receipts from customers on statement of cash flows (sum of monthly amounts).

c. and d.

Inventory Purchases Budget

Pro Forma

Oct.

Nov.

Dec.

Data

Budgeted cost of goods sold

$150,000

$162,000

$174,960

$486,960(a)

Plus: Desired ending inventory

16,200

17,496

12,000

12,000(b)

Inventory needed

166,200

179,496

186,960

Less: Beginning inventory

0

16,200

17,496

Required purchases (on account)

$166,200

$163,296

$169,464

50,839(c)

Schedule of Cash Payments Budget for Inventory Purchases

Pmt. of current month’s accts. pay.

$116,340

$114,307*

$118,625*

Pmt. for prior month’s accts. pay.

0

49,860

48,989*

Total budgeted pmts. for inventory

$116,340

$164,167

$167,614

$448,121(d)

(a) Cost of goods sold appearing on pro forma income statement (sum of monthly amounts).

(b) Ending inventory balance appearing on pro forma balance sheet.

(c) Ending accounts payable balance appearing on pro forma balance sheet ($169,464 –

$118,625).

(d) Cash payments for inventory purchases (sum of monthly amounts).

*Rounded

Problem 14-23 (continued)

e. and f.

Selling and Administrative Expense Budget

Pro Forma

Oct.

Nov.

Dec.

Data

Salary expense

$18,000

$18,000

$18,000

Sales commissions, 5% of sales

12,500

13,500

14,580

$14,580(a)

Supplies expense, 2% of sales

5,000

5,400

5,832

Utilities

1,400

1,400

1,400

1,400(b)

Depreciation on store fixtures

4,000

4,000

4,000

12,000(c)

Rent

4,800

4,800

4,800

Miscellaneous

1,200

1,200

1,200

Total S&A expenses

$46,900

$48,300

$49,812

145,012(d)

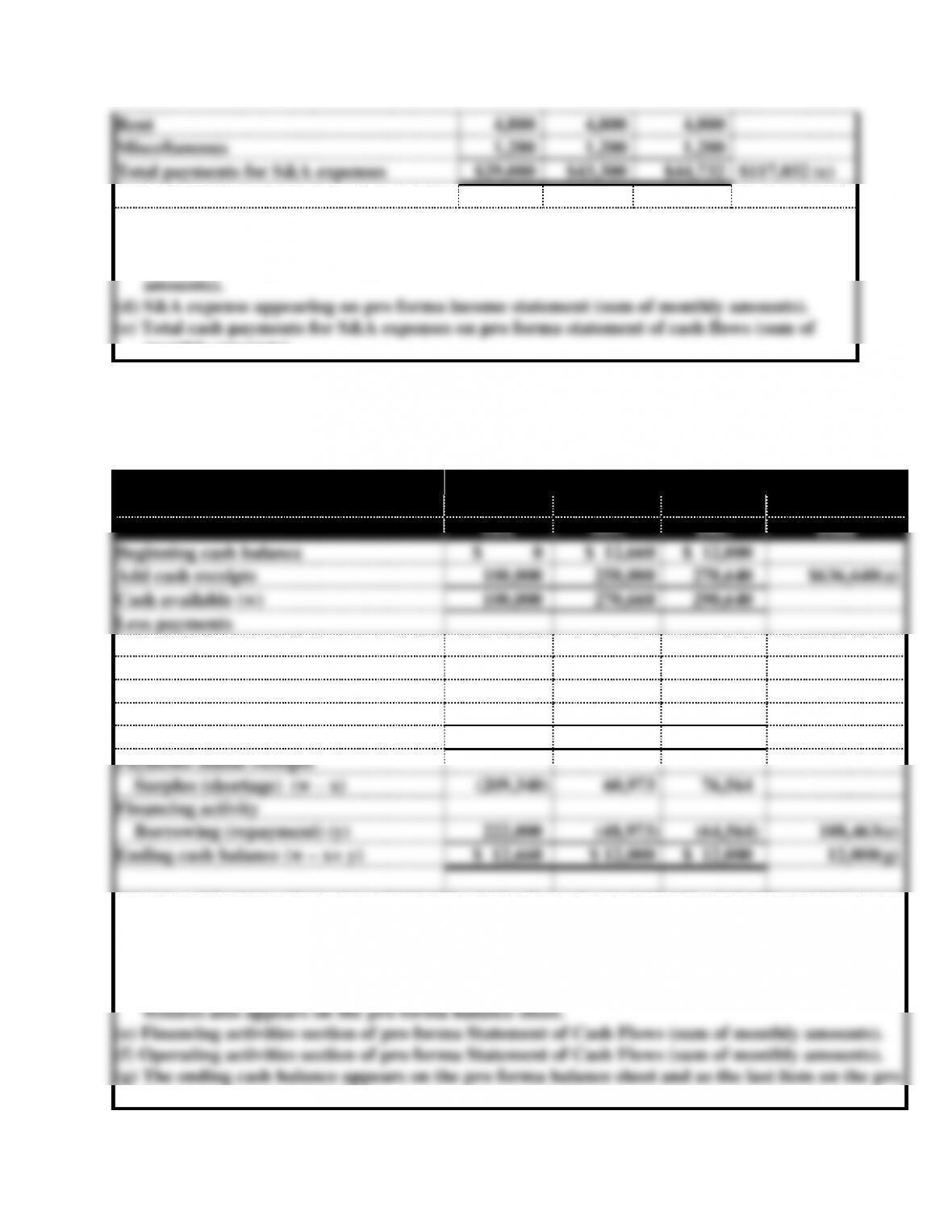

Schedule of Cash Payments for S&A Expenses

Salary expense

$18,000

$18,000

$18,000

Prior month’s sales comm., 100%

0

12,500

13,500

Supplies expense

5,000

5,400

5,832

Prior month’s utilities, 100%

0

1,400

1,400

Depreciation on store fixtures

0

0

0

Rent

4,800

4,800

4,800

Miscellaneous

1,200

1,200

1,200

Total payments for S&A expenses

$29,000

$43,300

$44,732

$117,032 (e)

Depreciation is a noncash charge.

(a) Ending sales commissions payable account balance shown on pro forma balance sheet.

(b) Ending utilities payable account balance shown on pro forma balance sheet.

(c) Accumulated depreciation appears on the pro forma balance sheet (sum of monthly

amounts).

(d) S&A expense appearing on pro forma income statement (sum of monthly amounts).

(e) Total cash payments for S&A expenses on pro forma statement of cash flows (sum of

monthly amounts).

Problem 14-23 (continued)

g.

Cash Budget

Pro Forma

Oct.

Nov.

Dec.

Data

Beginning cash balance

$ 0

$ 12,660

$ 12,000

Add cash receipts

100,000

258,000

278,640

$636,640(a)

Cash available (w)

100,000

270,660

290,640

Less payments

For inventory purchases

116,340

164,167

167,614

$448,121(b)

For S&A expenses

29,000

43,300

44,732

117,032(c)

Purchase of store fixtures

164,000

0

0

164,000(d)

Interest expense*

0

2,220

1,730*

3,950 (f)

Total budgeted payments (x)

309,340

209,687

214,076

Payments minus receipts

Surplus (shortage) (w – x)

(209,340)

60,973

76,564

Financing activity

Borrowing (repayment) (y)

222,000

(48,973)

(64,564)

108,463(e)

Ending cash balance (w – x+ y)

$ 12,660

$ 12,000

$ 12,000

12,000(g)

*October ($0 x 0.01); November ( $222,000 x 0.01); December [( $222,000 – $48,973) x 0.01]

(a) Operating activities section of pro forma Statement of Cash Flows (sum of monthly amounts).

(b) Operating activities section of pro forma Statement of Cash Flows (sum of monthly amounts).

(c) Operating activities section of pro forma Statement of Cash Flows (sum of monthly amounts).

(d) Investing activities section of pro forma Statement of Cash Flows. The investment in store

fixtures also appears on the pro forma balance sheet.

(e) Financing activities section of pro forma Statement of Cash Flows (sum of monthly amounts).

(f) Operating activities section of pro forma Statement of Cash Flows (sum of monthly amounts).

(g) The ending cash balance appears on the pro forma balance sheet and as the last item on the pro

forma statement of cash flows.

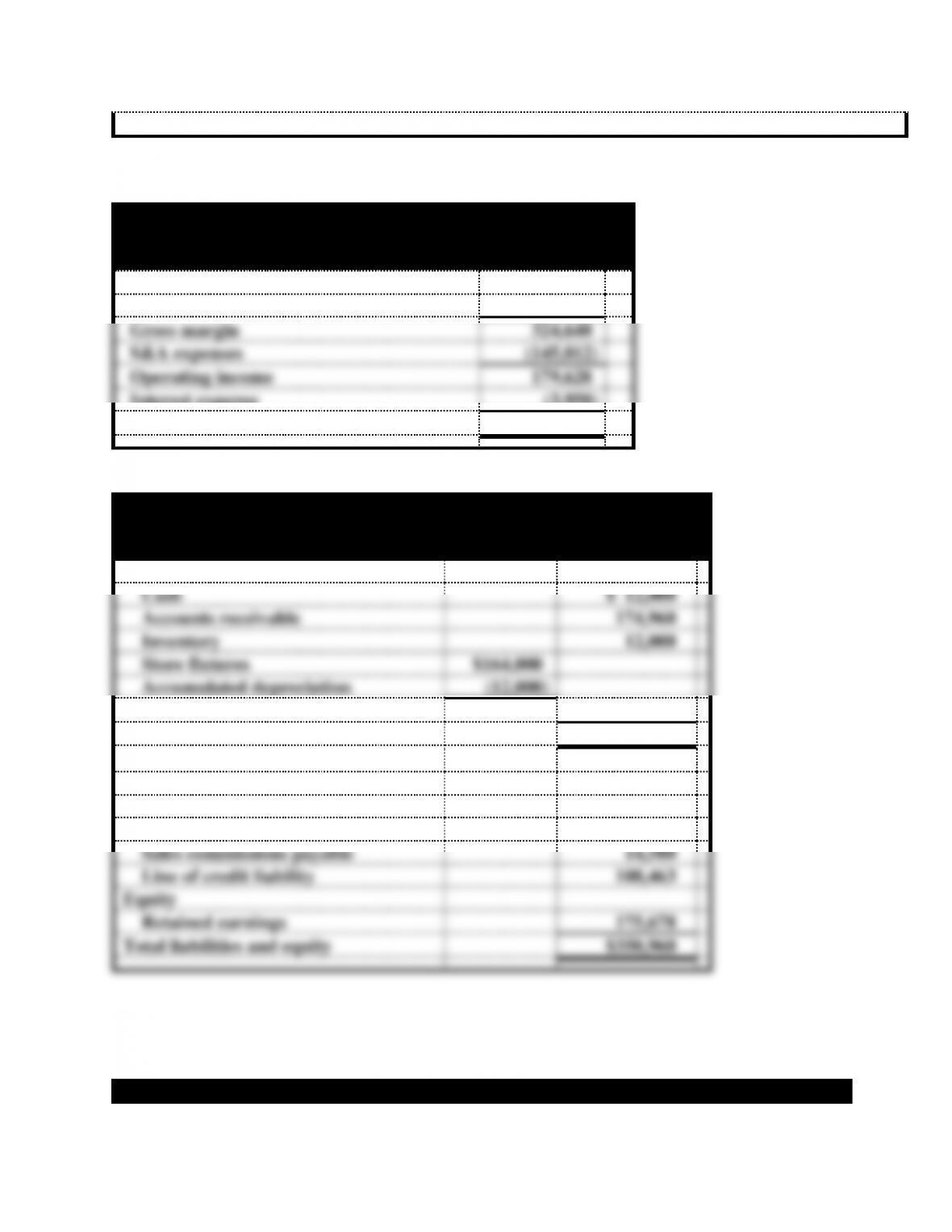

Problem 14-23 (continued)

h.

Haas Company

Pro Forma Income Statement

For the Quarter Ended December 31, 2015

Sales revenue

$811,600

Cost of goods sold

(486,960)

Gross margin

324,640

S&A expenses

(145,012)

Operating income

179,628

Interest expense

(3,950)

Net income

$175,678

i.

Haas Company

Pro Forma Balance Sheet

December 31, 2015

Assets

Cash

$ 12,000

Accounts receivable

174,960

Inventory

12,000

Store fixtures

$164,000

Accumulated depreciation

(12,000)

Book value of fixtures

152,000

Total assets

$350,960

Liabilities

Accounts payable

$ 50,839

Utilities payable

1,400

Sales commissions payable

14,580

Line of credit liability

108,463

Equity

Retained earnings

175,678

Total liabilities and equity

$350,960

Problem 14-23 (continued)

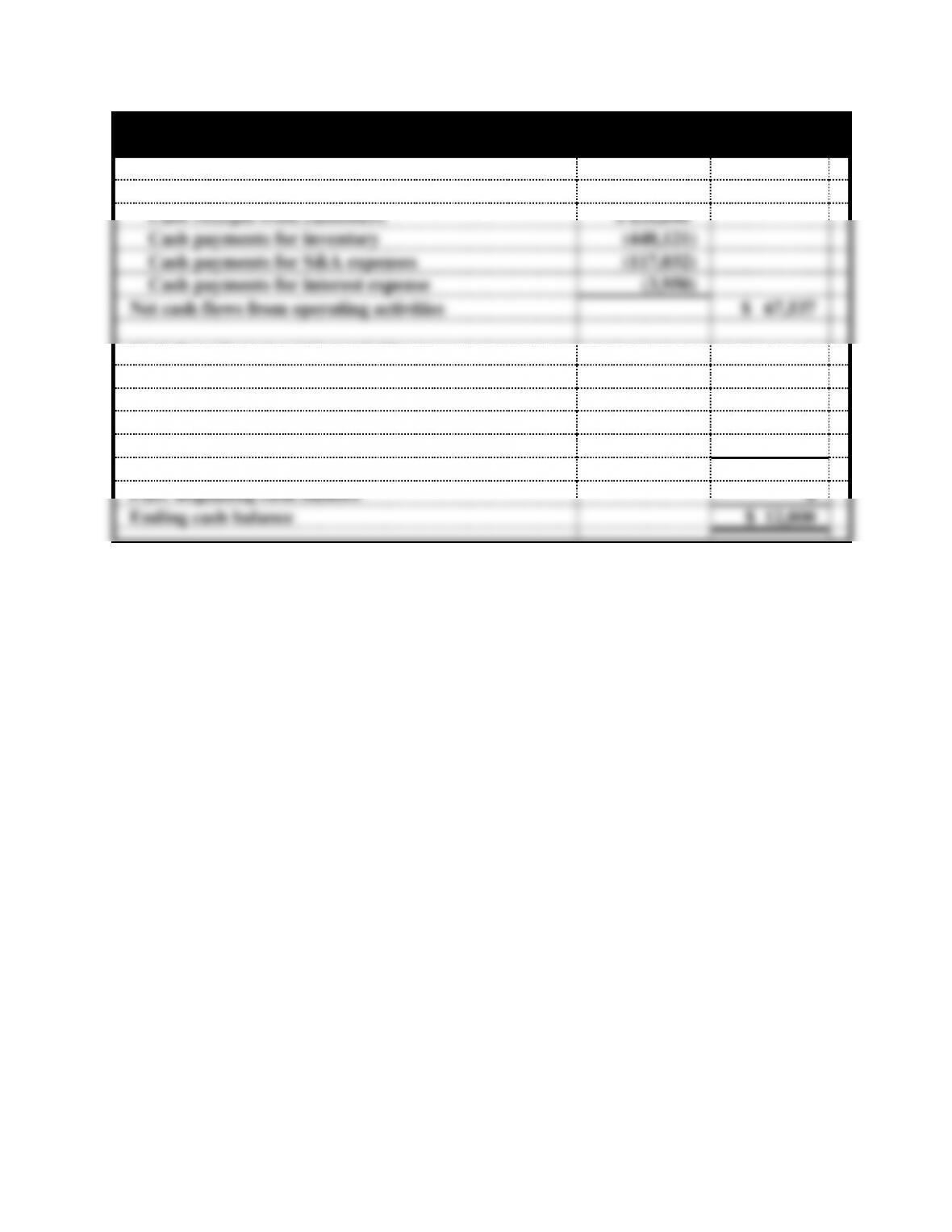

j.

Haas Company

Pro Forma Statement of Cash Flows

For the Quarter Ended December 31, 2015

Cash flows from operating activities

Cash receipts from customers

$ 636,640

Cash payments for inventory

(448,121)

Cash payments for S&A expenses

(117,032)

Cash payments for interest expense

(3,950)

Net cash flows from operating activities

$ 67,537

Cash flows from investing activities

Cash payment for store fixtures

(164,000)

Cash flow from financing activities

Net Inflow from line of credit

108,463

Net increase in cash

12,000

Plus: Beginning cash balance

0

Ending cash balance

$ 12,000