Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 07 - Accounting for Liabilities

7-1

Operating Activities

Inflow from Customers

$ 7,000

$ 7,000

$ 7,000

Outflow for Interest

(6,000)

(4,187)

(2,193)

Investing Activities

-0-

-0-

-0-

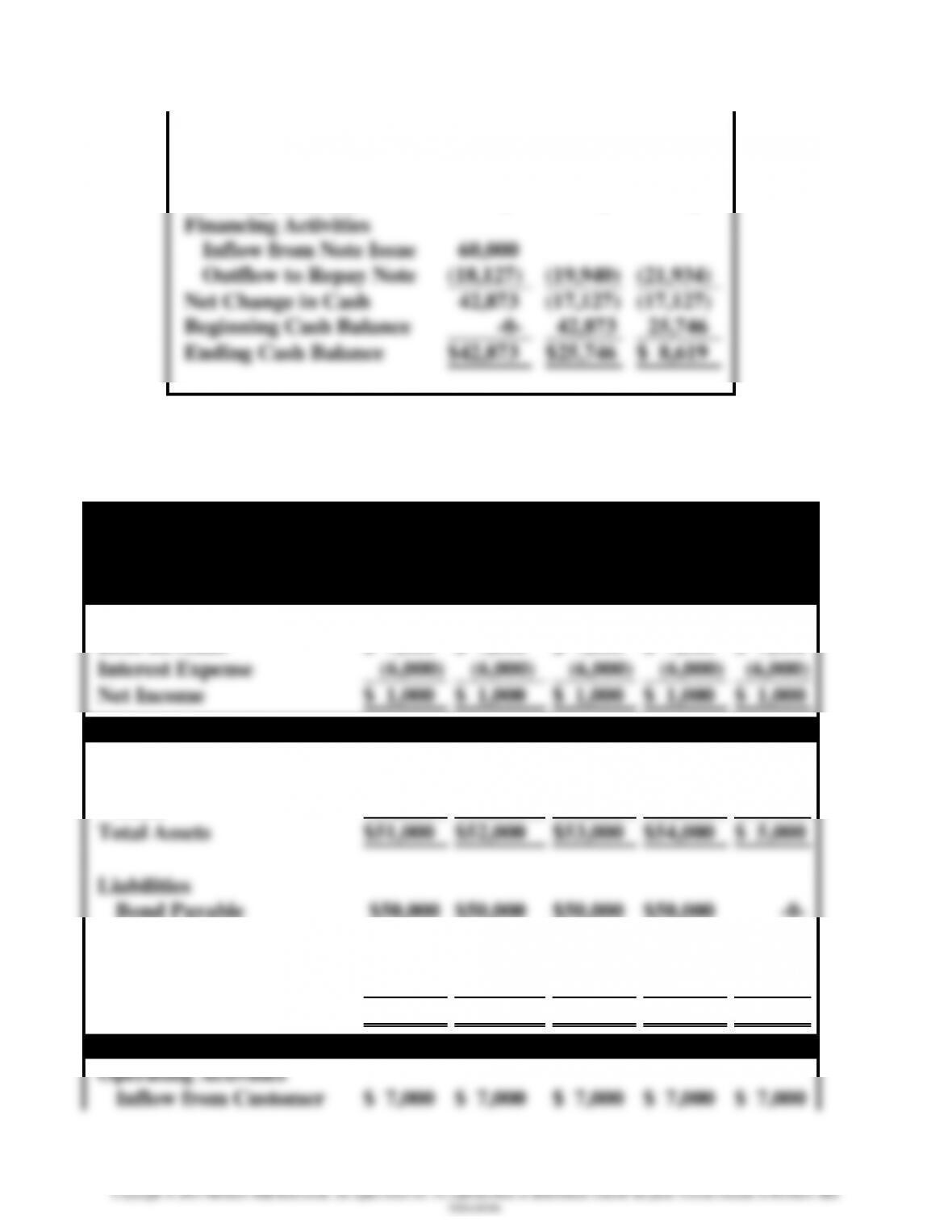

Financing Activities

Inflow from Note Issue

60,000

Outflow to Repay Note

(18,127)

(19,940)

(21,934)

Net Change in Cash

42,873

(17,127)

(17,127)

Beginning Cash Balance

-0-

42,873

25,746

Ending Cash Balance

$42,873

$25,746

$ 8,619

*The one dollar negative balance in the note payable account is due to rounding.

Demonstration Problem 7-4: Solution

Financial Statements

Land Development Company

Bonds Issued at Face Value with Interest Payable Annually

Income Statements

2014

2015

2016

2017

2018

Rent Revenue

$ 7,000

$ 7,000

$ 7,000

$ 7,000

$ 7,000

Interest Expense

(6,000)

(6,000)

(6,000)

(6,000)

(6,000)

Net Income

$ 1,000

$ 1,000

$ 1,000

$ 1,000

$ 1,000

Balance Sheets

Assets

Cash

$ 1,000

$ 2,000

$ 3,000

$ 4,000

$ 5,000

Land

50,000

50,000

50,000

50,000

-0-

Total Assets

$51,000

$52,000

$53,000

$54,000

$ 5,000

Liabilities

Bond Payable

$50,000

$50,000

$50,000

$50,000

-0-

Equity

Retained Earnings

1,000

2,000

3,000

4,000

5,000

Total Liabilities and Equity

$51,000

$52,000

$53,000

$54,000

$ 5,000

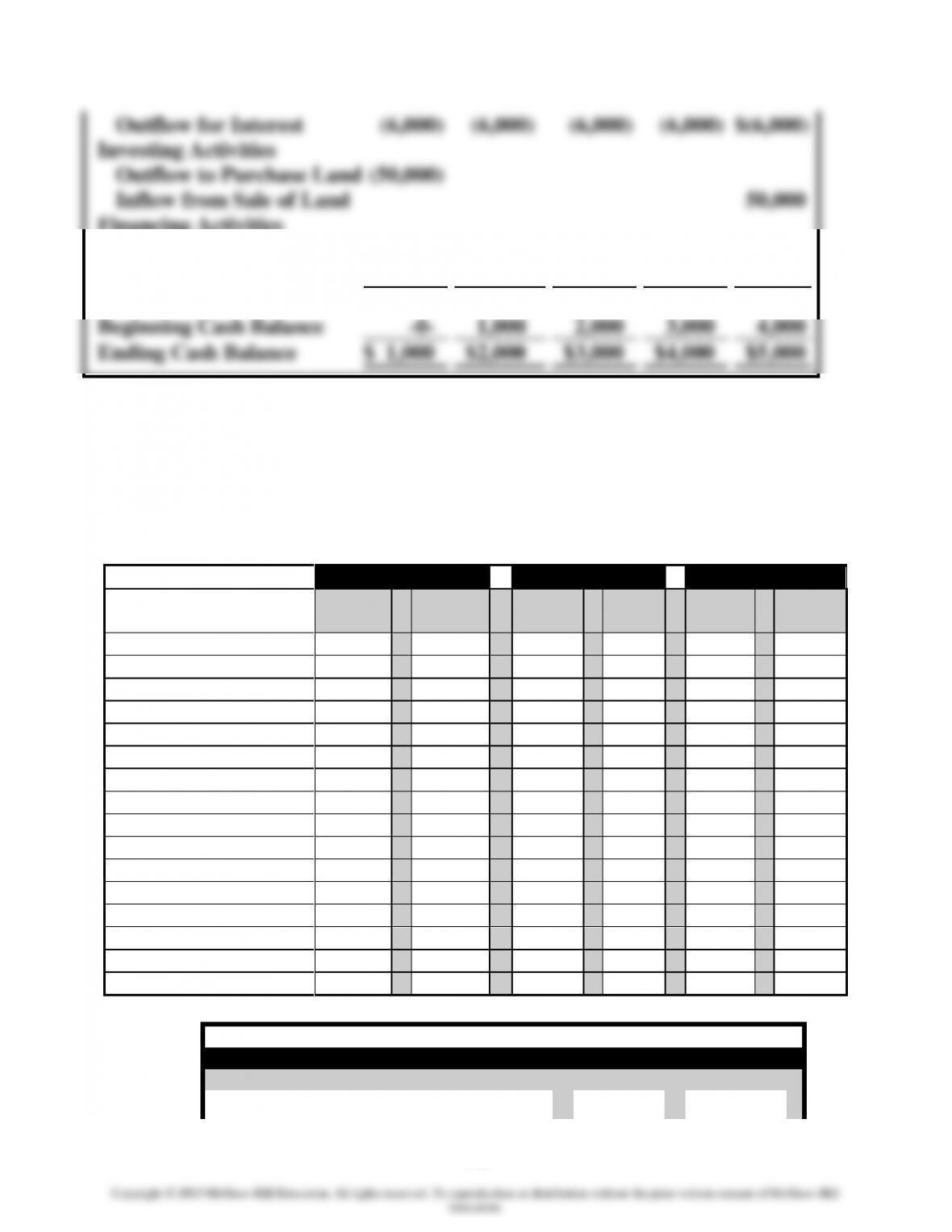

Statements of Cash Flows

Operating Activities

Inflow from Customer

$ 7,000

$ 7,000

$ 7,000

$ 7,000

$ 7,000

Chapter 07 - Accounting for Liabilities

7-2

Outflow for Interest

(6,000)

(6,000)

(6,000)

(6,000)

$(6,000)

Investing Activities

Outflow to Purchase Land

(50,000)

Inflow from Sale of Land

50,000

Financing Activities

Inflow from Bond Issue

50,000

Outflow to Repay Bond

(50,000)

Net Change in Cash

1,000

1,000

1,000

1,000

1,000

Beginning Cash Balance

-0-

1,000

2,000

3,000

4,000

Ending Cash Balance

$ 1,000

$2,000

$3,000

$4,000

$5,000

WORK PAPERS FOR

DEMONSTRATION PROBLEMS

Demonstration Problem 7-1: Work Paper, Parts A & B,

Accounting Equation

Assets

=

Liab.

+

Equity

2014 Part A

Cash

+

Land

=

Notes

Payable

+

Int.

Pay.

+

Com.

Stock

+

Ret.

Ear.

Beginning Balances

$ -0-

$ -0-

$ -0-

$ -0-

$ -0-

$ -0-

1. Effect of Borrowing

2. Purch. of Land

3. Earned Revenue

4. Accrued Int. Exp.

End. / Beg. Balances

$ 600

+

$10,000

=

$10,000

+

$ 400

+

$ -0-

+

$ 200

2015 Part B

1. Earned Revenue

2. Sold Land

3. Accrued Int. Exp.

4. Paid Interest

5. Repaid Loan

−−−−−

−−−−

−−−−

−−−−

−−−−−

−−−−−

Ending Balances

$ 750

+

$ -0-

=

$ -0-

+

$ -0-

+

$ -0-

+

$ 750

═══

════

════

════

═════

═════

Demonstration Problem 7-1: Work Paper, Parts A & B, Financial Statements

Canton Company

Income Statements

For the Years Ended December 31,

2014

2015

Rent Revenue

Chapter 07 - Accounting for Liabilities

7-3

Interest Expense

Net Income

Statements of Retained Earnings

Beginning Retained Earnings

Net Income

Dividends

Ending Retained Earnings

$200

$750

Balance Sheets at December 31

Assets

Cash

Land

Total Assets

$10,600

$750

Liabilities

Interest Payable

Note Payable

Equity

Retained Earnings

Total Liabilities and Equity

$10,600

$750

Statements of Cash Flows

Cash Flows from Operating Activities

Inflow from Rent Revenue

Outflow for Interest Expense

Net Inflow from Operating Activities

Cash Flow from Investing Activities

Inflow from Sale of Land

Outflow for Purchase of Land

Net Inflow (Outflow) from Investing Act.

Cash Flows from Financing Activities

Inflow from Issue of Note

Outflow for Repayment of Note

Net Inflow (Outflow) from Financing Act.

Net Change in Cash

Beginning Cash Balance

Ending Cash Balance

$ 600

$ 750

Demonstration Problem 7-2: Work Paper

Johnson’s 2014 interest expense equals McCoy’s 2014 interest revenue, as follows:

Date Note Issued

Principal

x

Rate

x

Time

=

Accrued Interest

April 1, 2014

x

x

=

June 1, 2014

x

x

=

Chapter 07 - Accounting for Liabilities

7-4

October 1, 2014

x

x

=

Demonstration Problem 7-3: Work Paper, part a. Amortization Table

Column 1

Column 2

Column 3

Column 4

Column 5

Accounting

Period

Principal

Balance on

Jan. 1

Cash

Payment

Dec. 31

Applied

to

Interest

Applied

to

Principal

2014

60,000

24,127

2015

2016

Demonstration Problem 7-3: Work Paper, part b. Financial Statements

Financial Statements

Income Statements

2014

2015

2016

Revenue

$7,000

$7,000

$7,000

Interest Expense

Net Income

Balance Sheets

Assets

Cash

$42,873

$25,746

$ 8,619

Liabilities

Note Payable

(1)*

Equity

Retained Earnings

Total Liabilities and Equity

Statements of Cash Flows

Operating Activities

Inflow from Customers

Outflow for Interest

Chapter 07 - Accounting for Liabilities

7-5

Investing Activities

Financing Activities

Inflow from Note Issue

Outflow to Repay Note

Net Change in Cash

42,873

(17,127)

(17,127)

Beginning Cash Balance

Ending Cash Balance

*The one dollar negative balance in the note payable account is due to rounding.

Chapter 07 - Accounting for Liabilities

7-6

Demonstration Problem 7-4: Work Paper

Financial Statements

Land Development Company

Bonds Issued at Face Value with Interest Payable Annually

Income Statements

2014

2015

2016

2017

2018

Rent Revenue

$ 7,000

$ 7,000

$ 7,000

$ 7,000

$ 7,000

Interest Expense

Net Income

Balance Sheets

Assets

Cash

Land

Total Assets

Liabilities

Bond Payable

Equity

Retained Earnings

Total Liabilities and Equity

Statements of Cash Flows

Operating Activities

Inflow from Customer

Outflow for Interest

Investing Activities

Outflow to Purchase Land

Inflow from Sale of Land

Financing Activities

Inflow from Bond Issue

Outflow to Repay Bond

Net Change in Cash

1,000

1,000

1,000

1,000

1,000

Beginning Cash Balance

Ending Cash Balance

Quiz Questions for Chapter 7

7-7

Education.

1. On January 1, 2014, Ink, Inc. borrowed $100,000 cash from Fidelity Bank on a note that had a 6 percent

annual interest rate and a five-year term. The loan is to be repaid in annual payments of $23,741.69 on

January 1 each year. The amount of the January 1, 2015, payment applied to interest and to principal would

be

a. $6,000 / $94,000.

b. $17,741.69 / $94,000.

c. $4,935.50 / $82,258.31.

d. $6,000 / $17,741.69.

2. Indigo Company can borrow up to $50,000 on its bank line of credit. The company agrees to pay interest

monthly at 2 percent above prime. Funds are borrowed or repaid on the first day of each month.

Month

Amounts Borrowed or (Repaid)

Prime Rate

Jan.

$15,000

6 percent

Feb.

$ (5,000)

5 percent

March

$30,000

4 percent

The amount of interest to be accrued on March 31 is

a. $225.00.

b. $100.00.

c. $133.33.

d. $200.00.

Use the following information to answer the next two questions. Yeats Company issued a $5,000 face value note

to the State Bank on December 1, 2014. The note had a 12 percent annual rate of interest and a one-year term.

3. The adjusting entry to record accrued interest on December 31, 2014, would

a. decrease liabilities by $50.

b. decrease equity by $50.

c. increase net income by $50.

d. none of the above.

4. The amount of cash paid for interest in 2015 is:

a. $550.

b. $50.

c. $600.

d. none of the above.

Use the following information to answer the next two questions. On May 1, 2014, Arrow Company borrowed

$10,000 from the State Bank at 9 percent annual interest. The note issued by Arrow had a one-year term. Arrow

reported cash revenue of $3,400 and $800 in 2014 and 2015, respectively.

5. Arrow’s net income for 2014 and 2015 would be

a. $2,500 / $100.

b. $2,800 / $500.

c. $2,400 / $800.

d. $2,500 / $800.

6. The cash flow from operating activities Arrow would report on the 2014 and 2015 statements of cash flows

would be

a. $2,800 / $500.

b. $2,500 / $800.

c. $2,800 / $(100).

Chapter 07 - Accounting for Liabilities

7-8

d. $3,400 / $(100).

7. Which of the following illustrates the recognition of sales tax collected at the point of sale?

Balance Sheet

Income Statement

Statement of

Assets

=

Liab.

+

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

a.

+

+

n/a

n/a

n/a

n/a

n/a

b.

+

+

n/a

+

n/a

+

n/a

c.

−

−

n/a

n/a

+

−

− OA

d.

+

+

n/a

n/a

n/a

n/a

+ OA

8. Issuance of a note payable with a six month term to maturity is what type of transaction?

a. Asset source.

b. Asset use.

c. Claims exchange.

d. Claims decrease.

9. A contingent liability that is remote is

a. shown in the balance sheet and disclosed in the footnotes.

b. not shown in the balance sheet but is disclosed in the footnotes.

c. shown in the balance sheet but not in the footnotes.

d. not shown in the balance sheet and is not disclosed in the footnotes.

10. Select the true statement.

a. If the likelihood of a contingent liability is probable and the amount can be estimated, it must be shown

in the balance sheet.

b. If the likelihood of a contingent liability is reasonably possible it does not have to be shown in the

balance sheet but must be disclosed in the footnotes.

c. If the likelihood of a contingent liability is remote it does not have to be shown in the balance sheet nor

disclosed in the footnotes.

d. All of the above are true.

Solutions to Quiz Questions

Question

Answer

1

D

2

D

3

B

4

C

5

B

6

D

7

D

8

A

9

D

10

D

Chapter 07 - Accounting for Liabilities

Summary Outline of a Lesson Plan for Chapter 7

I. Use Demonstration Problem 7-1 to introduce accrued interest payable. In this

problem, the amount of interest has already been calculated to allow you to concentrate

on how interest expense affects the financial statements.

II. Hand out Demonstration Problem 7-2. Use this problem to show students how to

compute accrued interest.

III. Use an exercise in the text to demonstrate sales taxes. Exercise 7-3 serves as a good

demonstration problem. Exercise 7-4 works well as a reinforcement exercise for

homework.

IV. Use exercises in the text to demonstrate contingent liabilities and product

warranties. Exercise 7-5 provides a good basis for a discussion about contingent

liabilities. Exercises 7-6 and 7-7 provide comprehensive problems dealing with

warranties. They serve as excellent demonstration problems for a brief lecture on how to

report warranty obligations.

V. Demonstration Problem 7-3 illustrates accounting for a term loan repaid with equal

annual payments of principal and interest.

VI. Lines of credit. You can use Exercise 7-13 as a demonstration problem or a homework

assignment related to lines of credit.

VII. Demonstration Problem 7-4 illustrates accounting for a bond liability across five

consecutive accounting cycles. The text covers bonds issued at face amount; it does not

cover bond discounts or premiums.

VIII. Time considerations and homework assignments. Current liabilities (Demonstration

Problems 7-1 and 7-2) should take at least an hour of class time. Exercises 7-1 and 7-2

are good to use as reinforcement for interest expense recognition. Spend approximately

15 minutes each on sales tax and warranty obligations. Plan to spend less than one hour

of class time covering installment loans and lines of credit. Demonstration Problem 7-3

provides an example of an installment loan, and you may wish to use Exercises 7-10 and

7-11 to reinforce accounting for installment loans. Problem 7-33 pertains to lines of

credit. Allow an additional 30 to 45 minutes of class time to cover bond liabilities.

Exercise 7-22 may be used as homework or in-class practice in preparing a classified

balance sheet.