Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

3-1

EXERCISE 3-12

a. Annual rate = Discount rate x (365 days ÷ Discount term*)

b. Since the annualized discount rate (36.5%) is significantly higher than the cost of borrowing

EXERCISE 3-13

a. The Merchandise Inventory account is analyzed as follows:

Mdse. Inventory

2. Purcashed Inventory $35,000

3. Inventory Sold (21,000)

Book Balance 14,000

4. Less:Actual Count (13,500)

Difference in book and actual inventory $ 500

b. Lost, stolen, or damaged inventory may not have been accounted for. When management

EXERCISE 3-14

a.

Computation of Gross Margin

Sales Revenue

$37,500

Less: Cost of Goods Sold

(20,000)

Gross Margin

$17,500

b.

Computation of Gain on Sale of Land

Selling Price

$40,000

Less: Cost of Land Sold

(25,000)

Gain on Sale of Land

$15,000

3-2

c. Gross Margin is sales less cost of goods sold that is shown on the income statement before

d. Neither gross margin nor gain on sale of land is shown specifically in the Statement of Cash

EXERCISE 3-15

Single-Step Income Statement:

Healthy Eats

Income Statement

For the Year Ended December 31, 2014

Net Sales

$2,000

Expenses

Cost of Goods Sold

$1,200

Advertising Expense

400

Interest Expense

140

Salaries Expense

260

Rent Expense

220

Total Expenses

(2,220)

Loss on Sale of Land

(50)

Net Income (Loss)

$ (270)

Multistep Income Statement:

Healthy Eats

Income Statement

For the Year Ended December 31, 2014

Net Sales

$2,000

Cost of Goods Sold

(1,200)

Gross Margin

800

Operating Expenses

Advertising Expense

$400

Salaries Expense

260

Rentlies Expense

220

Total Operating Expenses

(880)

3-3

Operating Income (Loss)

(80)

Non-Operating Items

Interest Expense

(140)

Loss on Sale of Land

(50)

Net Income (Loss)

$ (270)

3-4

EXERCISE 3-16

a.

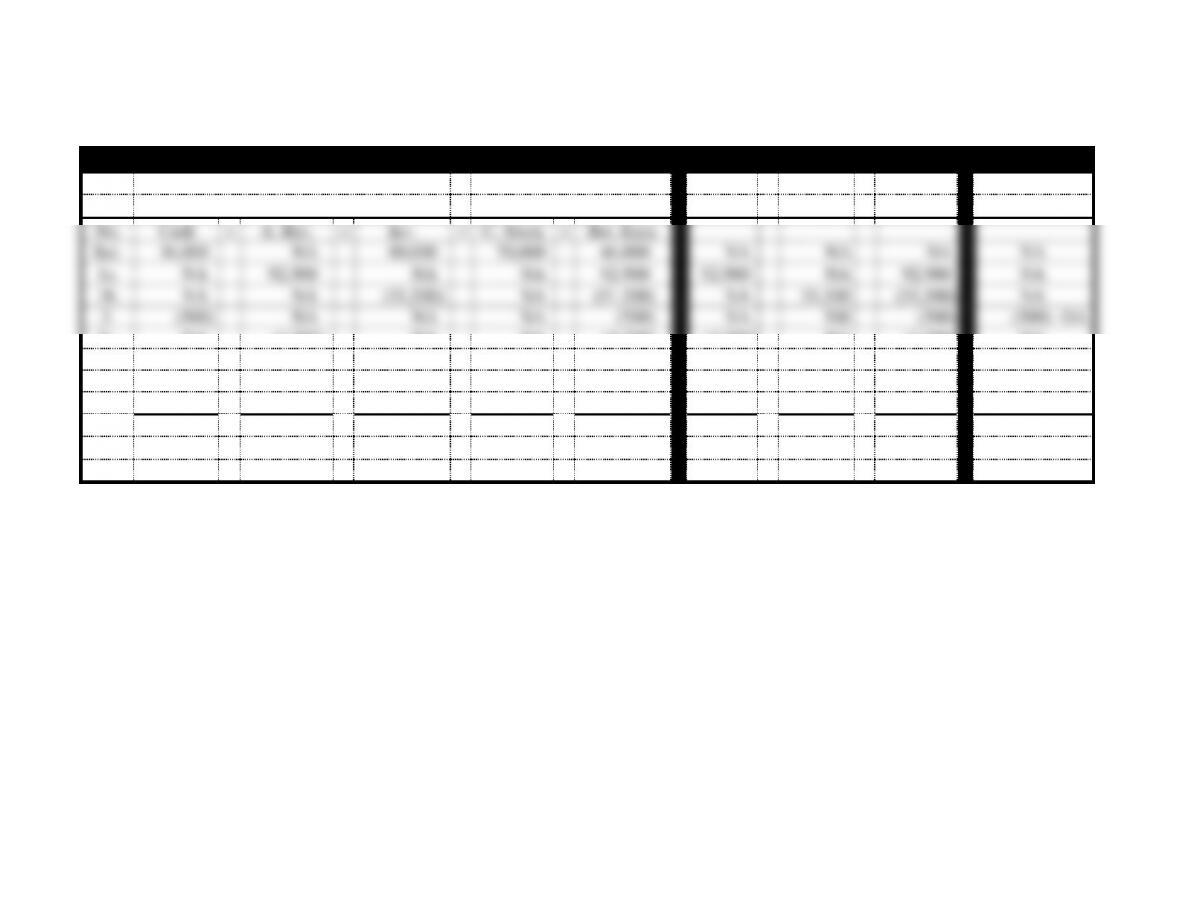

Poole Company Effect of Events on the Financial Statements

Assets

=

Equity

Rev.

−

Exp.

=

Net. Inc.

Cash Flow

No.

Cash

+

A. Rec.

+

Inv.

=

C. Stock

+

Ret. Earn.

Bal.

36,000

NA

80,000

70,000

46,000

NA

NA

NA

NA

1a.

NA

92,900

NA

NA

92,900

92,900

NA

92,900

NA

1b.

NA

NA

(51,500)

NA

(51,500)

NA

51,500

(51,500)

NA

2.

(500)

NA

NA

NA

(500)

NA

500

(500)

(500) OA

3a.

NA

(4,700)

NA

NA

(4,700)

(4,700)

NA

(4,700)

NA

3b.

NA

NA

3,200

NA

3,200

NA

(3,200)

3,200

NA

4.

NA

(1,500)

NA

NA

(1,500)

(1,500)

NA

(1,500)

NA

5.

71,000

(71,000)

NA

NA

NA

NA

NA

NA

71,000 OA

Tot.

106,500

+

15,700

+

31,700

=

70,000

+

83,900

86,700

−

48,800

=

37,900

70,500 NC

3-5

EXERCISE 3-16 (cont.)

b.

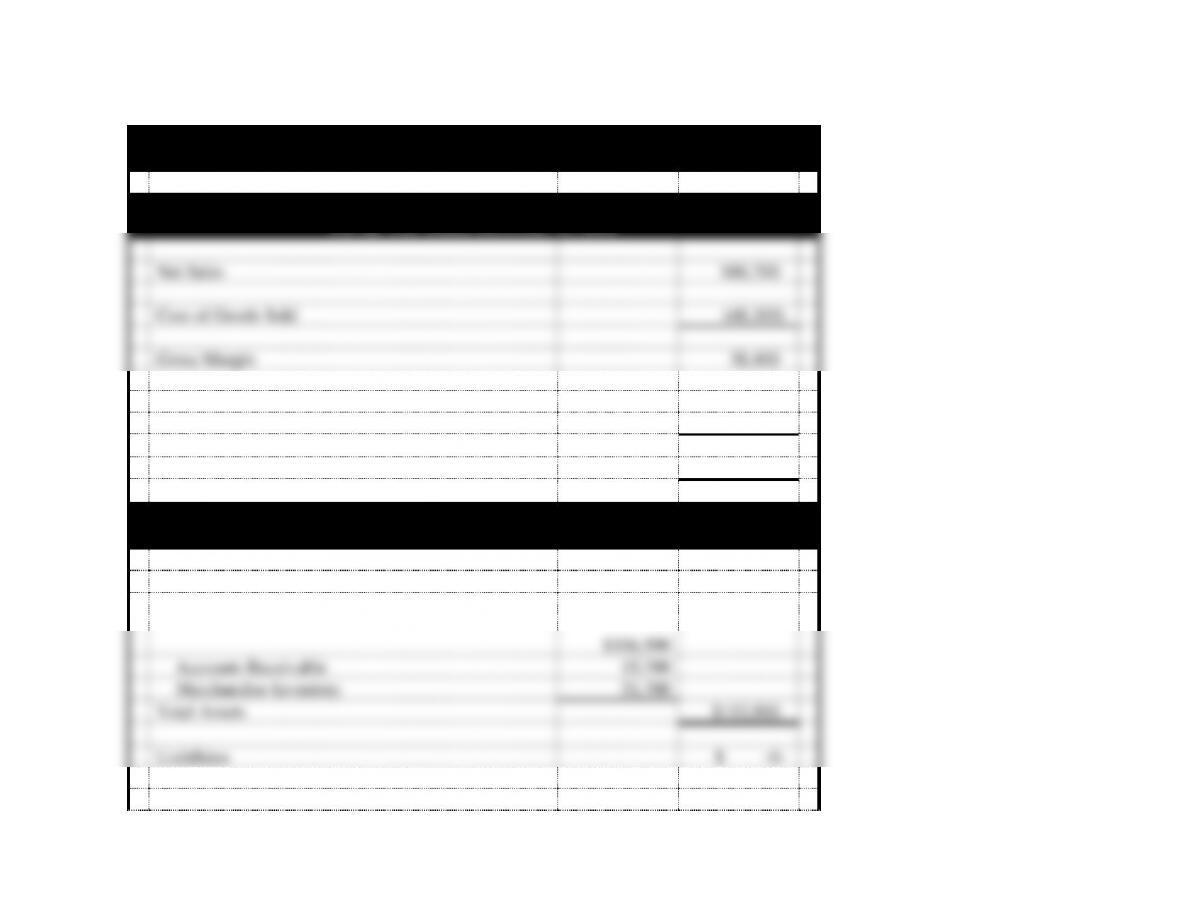

Poole Company

Financial Statements

Income Statement

For the Year Ended December 31, 2014

Net Sales

$86,700

Cost of Goods Sold

(48,300)

Gross Margin

38,400

Operating Expenses

Transportation-out

(500)

Net Income

$37,900

Balance Sheet

As of December 31, 2014

Assets

Cash

$106,500

Accounts Receivable

15,700

Merchandise Inventory

31,700

Total Assets

$153,900

Liabilities

$ -0-

Stockholders’ Equity

3-6

Common Stock

$70,000

Retained Earnings

83,900

Total Stockholders’ Equity

153,900

Total Liabilities and Stockholders’ Equity

$153,900

EXERCISE 3-16 b. (cont.)

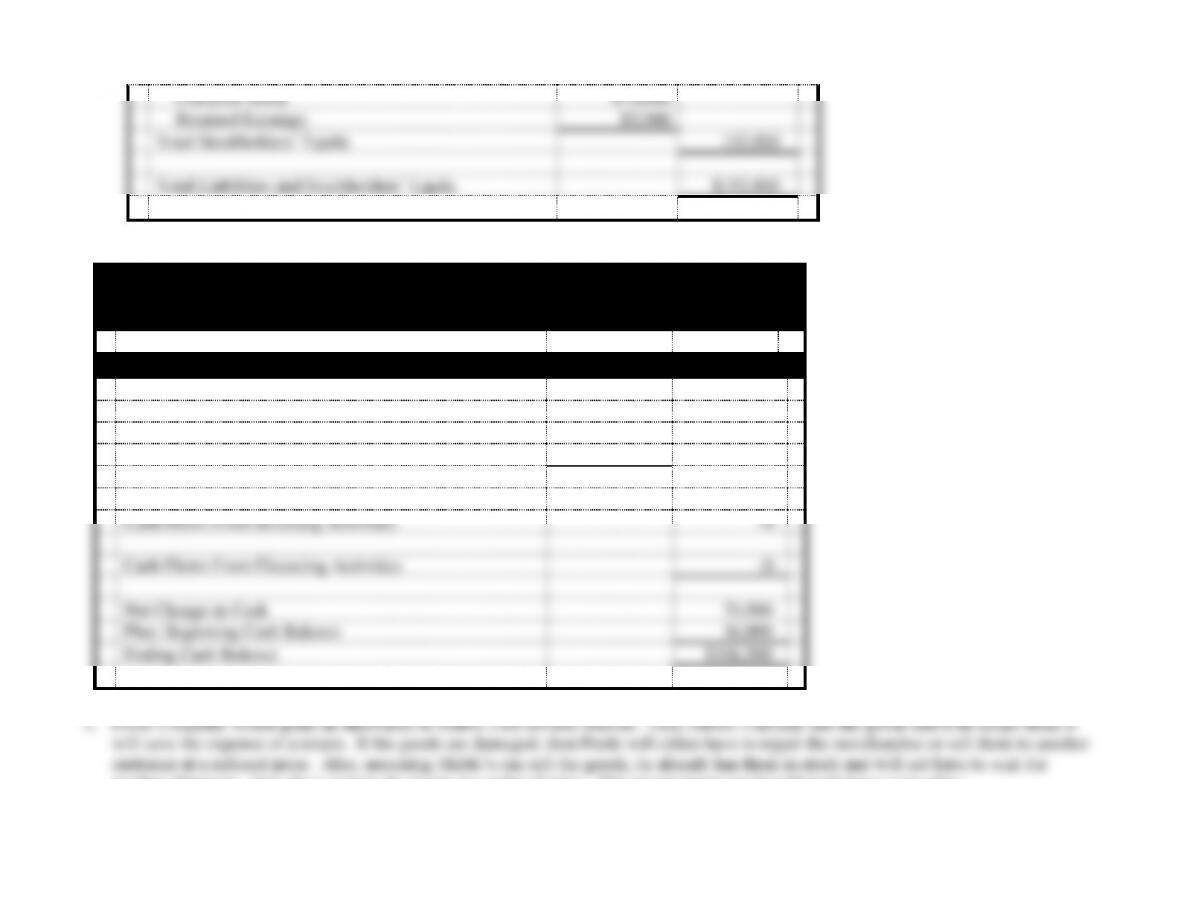

Poole Company

Financial Statements

For the Year Ended December 31, 2014

Statement of Cash Flows

Cash Flows From Operating Activities:

Inflow from Customers

$71,000

Outflow for Expenses

(500)

Net Cash Flow from Operating Activities

$ 70,500

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities

-0-

Net Change in Cash

70,500

Plus: Beginning Cash Balance

36,000

Ending Cash Balance

$106,500

another shipment. Also, he is getting the goods at a reduced price. This arrangement can benefit both buyer and seller

EXERCISE 3-17

3-7

a.

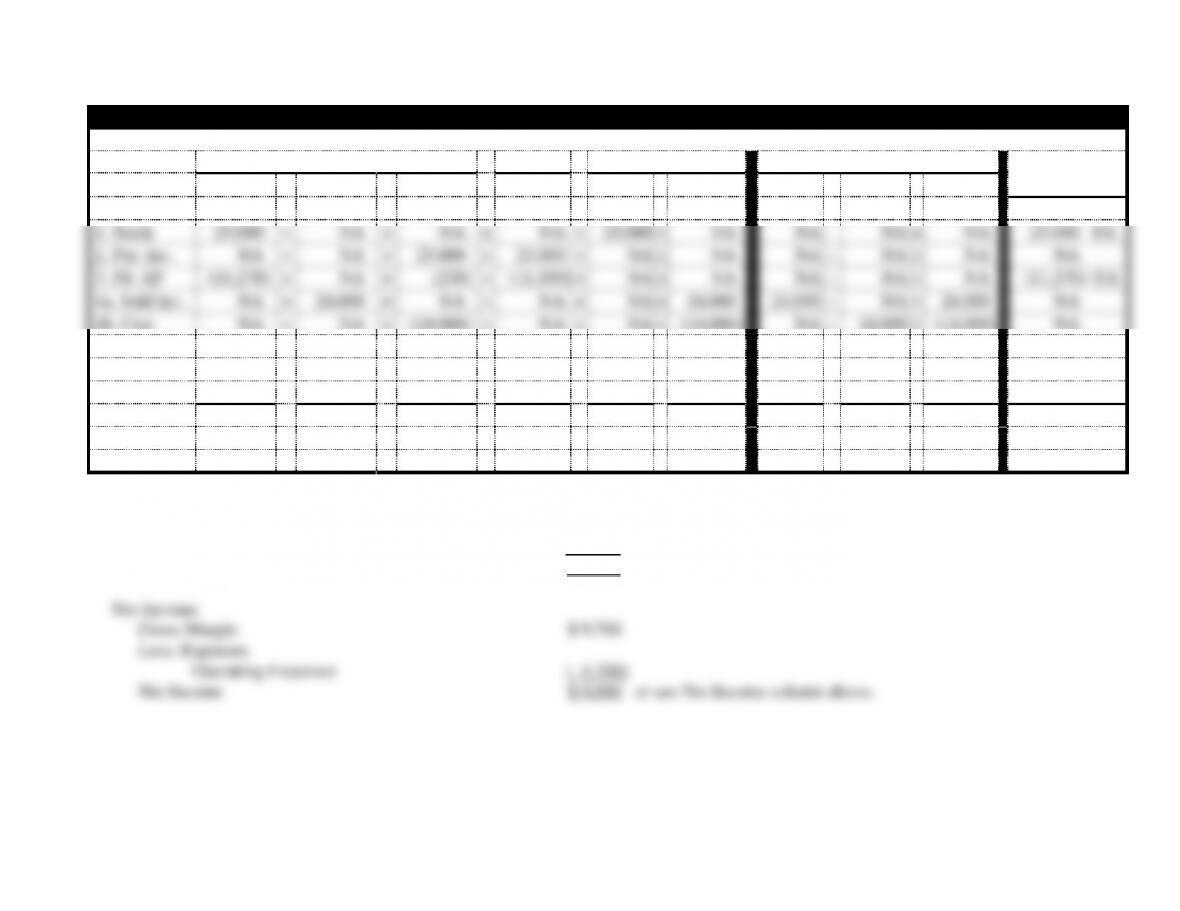

Clayton Computers Horizontal Statements Model for 2014

Assets

=

Liab.

+

Stkholders’ Equity

Income Statement

Statement of

Cash

+

A. Rec.

+

Inv.

=

A. Pay.

+

C. Stk.

+

Ret. Ear.

Rev.

−

Exp.

=

Net Inc.

Cash Flows

1. Stock

25,000

+

NA

+

NA

=

NA

+

25,000

+

NA

NA

−

NA

=

NA

25,000 FA

2. Pur. Inv.

NA

+

NA

+

23,000

=

23,000

+

NA

+

NA

NA

−

NA

=

NA

NA

3. Pd. AP

(11,270)

+

NA

+

(230)

=

(11,500)

+

NA

+

NA

NA

−

NA

=

NA

(11,270) OA

4a. Sold Inv.

NA

+

24,000

+

NA

=

NA

+

NA

+

24,000

24,000

−

NA

=

24,000

NA

4b. Cost

NA

+

NA

+

(14,000)

=

NA

+

NA

+

(14,000)

NA

−

14,000

=

(14,000)

NA

5. Coll. AR

23,760

+

(24,000)

+

NA

=

NA

+

NA

+

(240)

(240)

−

NA

=

(240)

23,760 OA

6. Pd. Exp.

(1,700)

+

NA

+

NA

=

NA

+

NA

+

(1,700)

NA

−

1,700

=

(1,700)

(1,700) OA

7. Pd. AP

(11,500)

+

NA

+

NA

=

(11,500)

+

NA

+

NA

NA

−

NA

=

NA

(11,500) OA

End. Bal.

24,290

+

-0-

+

8,770

=

-0-

+

25,000

+

8,060

23,760

−

15,700

=

8,060

24,290 NC

7

b. Gross Margin:

Net Sales $23,760

Cost of Goods Sold (14,000)

Gross Margin $ 9,760

3-8

EXERCISE 3-17 (cont.)

c. Cash discounts are given to encourage prompt payment by the customers (accounts receivable).

of the invoice is due in 30 days.EXERCISE 3-18

a.

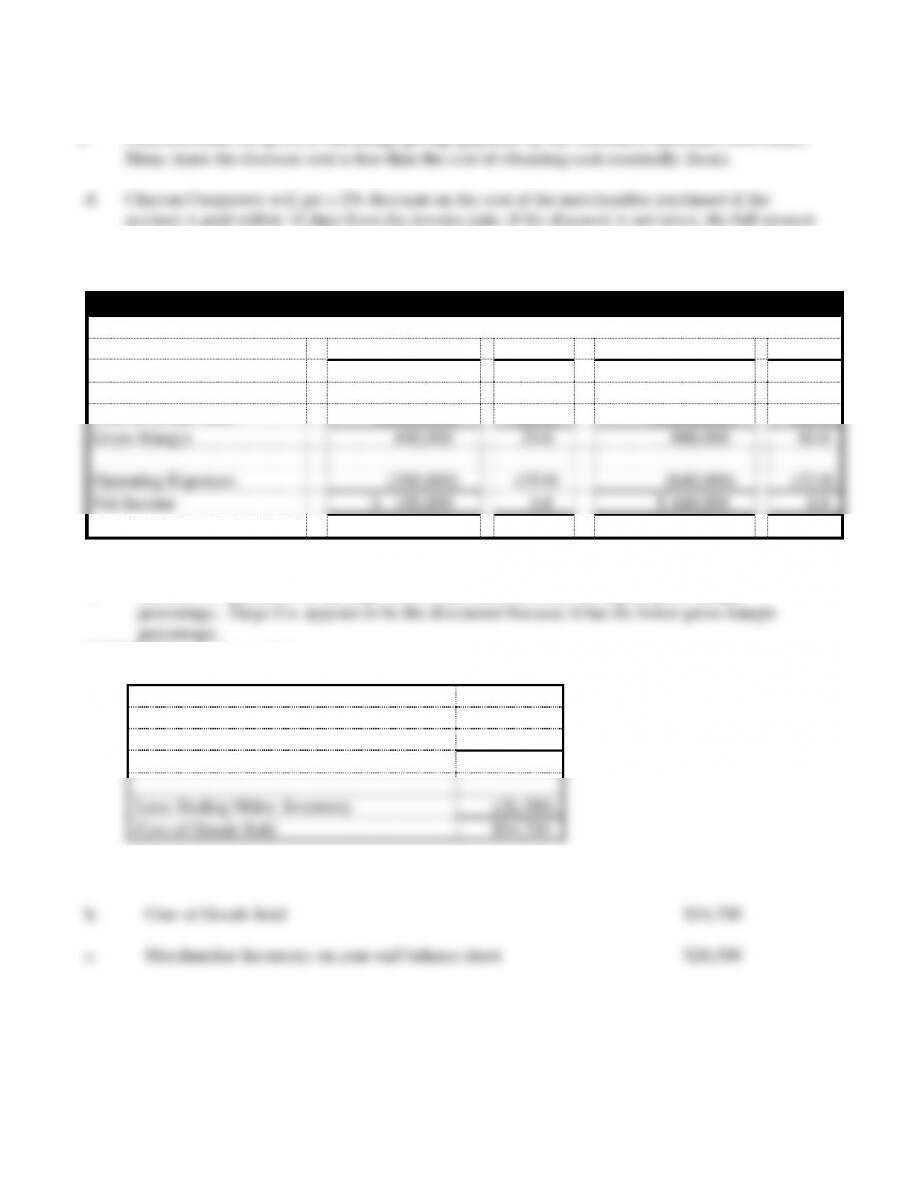

Common Size Income Statements

Fargo

%

Huston

%

Sales

$2,000,000

100.0

$2,000,000

100.0

Cost of Goods Sold

(1,600,000)

(80.0)

(1,200,000)

(60.0)

Gross Margin

400,000

20.0

800,000

40.0

Operating Expenses

(300,000)

(15.0)

(640,000)

(32.0)

Net Income

$ 100,000

5.0

$ 160,000

8.0

b. Huston Co. appears to be the high-end retailer because it has the higher gross margin

EXERCISE 3-19 (Appendix)

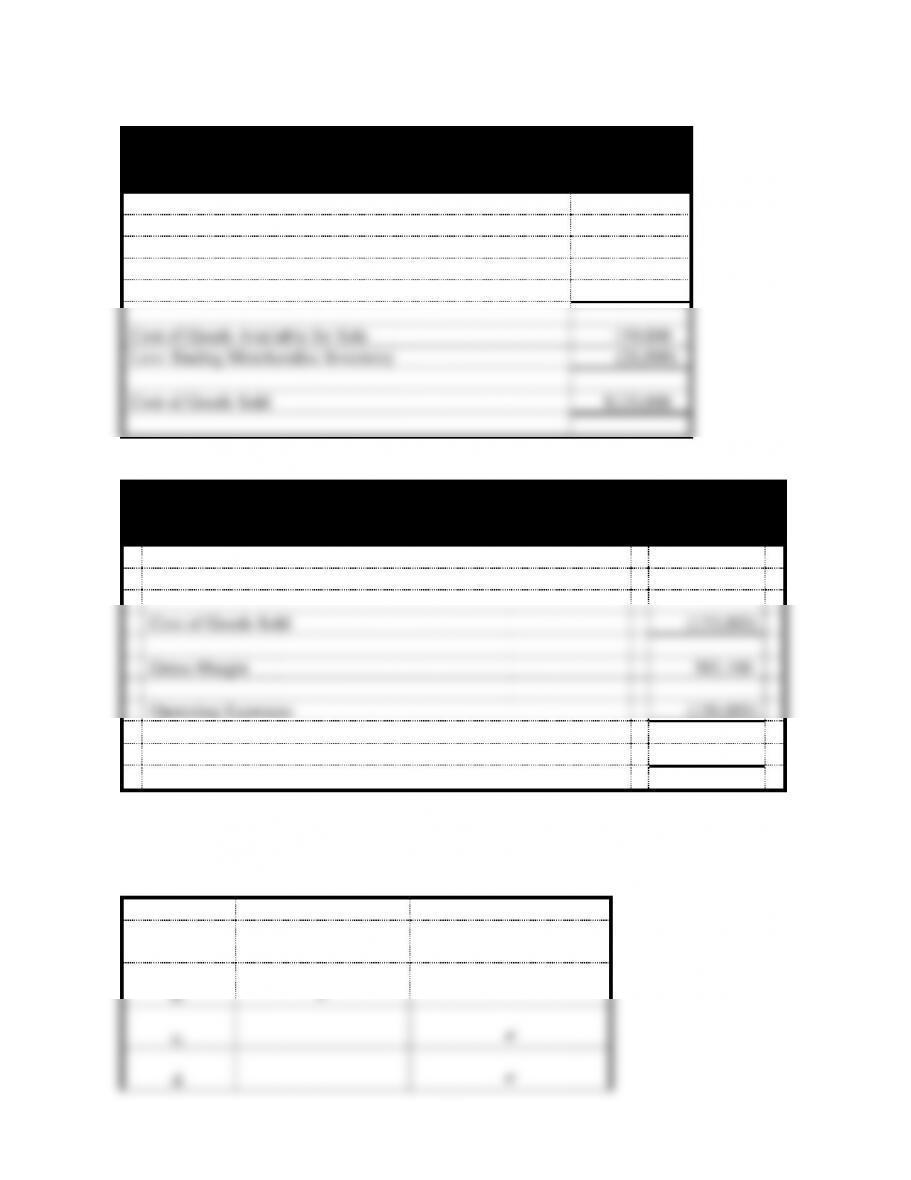

Beginning Mdse. Inventory

$16,000

Plus: Merchandise Purchased

65,000

Total Available for Sale

81,000

Less: Ending Mdse. Inventory

(26,300)

Cost of Goods Sold

$54,700

a. Goods Available for Sale $81,000

3-9

EXERCISE 3-20 (appendix)

a.

Belk Antiques

Schedule of Cost of Goods Sold

For the Year Ended December 31, 2014

Beginning Merchandise Inventory

$ 42,000

Plus: Purchases

128,000

Plus: Transportation-in

1,000

Less: Purchase Returns and Allowances

(12,000)

Cost of Goods Available for Sale

159,000

Less: Ending Merchandise Inventory

(26,000)

Cost of Goods Sold

$133,000

b.

Belk Antiques

Income Statement

For the Year Ended December 31, 2014

Net Sales Revenue*

$516,100

Cost of Goods Sold

(133,000)

Gross Margin

383,100

Operating Expenses

(130,000)

Net Income

$253,100

*Sales, $520,000 − Sales Returns and Allow., $3,900 = Net Sales, $516,100

PROBLEM 3-21

Event

Product Costs

Period Costs

a.

b.

c.

d.

3-10

e.

f.

g.

h.

i.

j.

PROBLEM 3-22

Event

Freight Costs Paid

Period/Product Cost

a.

$500

Product

b.

$-0-

NA

c.

$-0-

NA

d.

$300

Period

3-11

PROBLEM 3-23

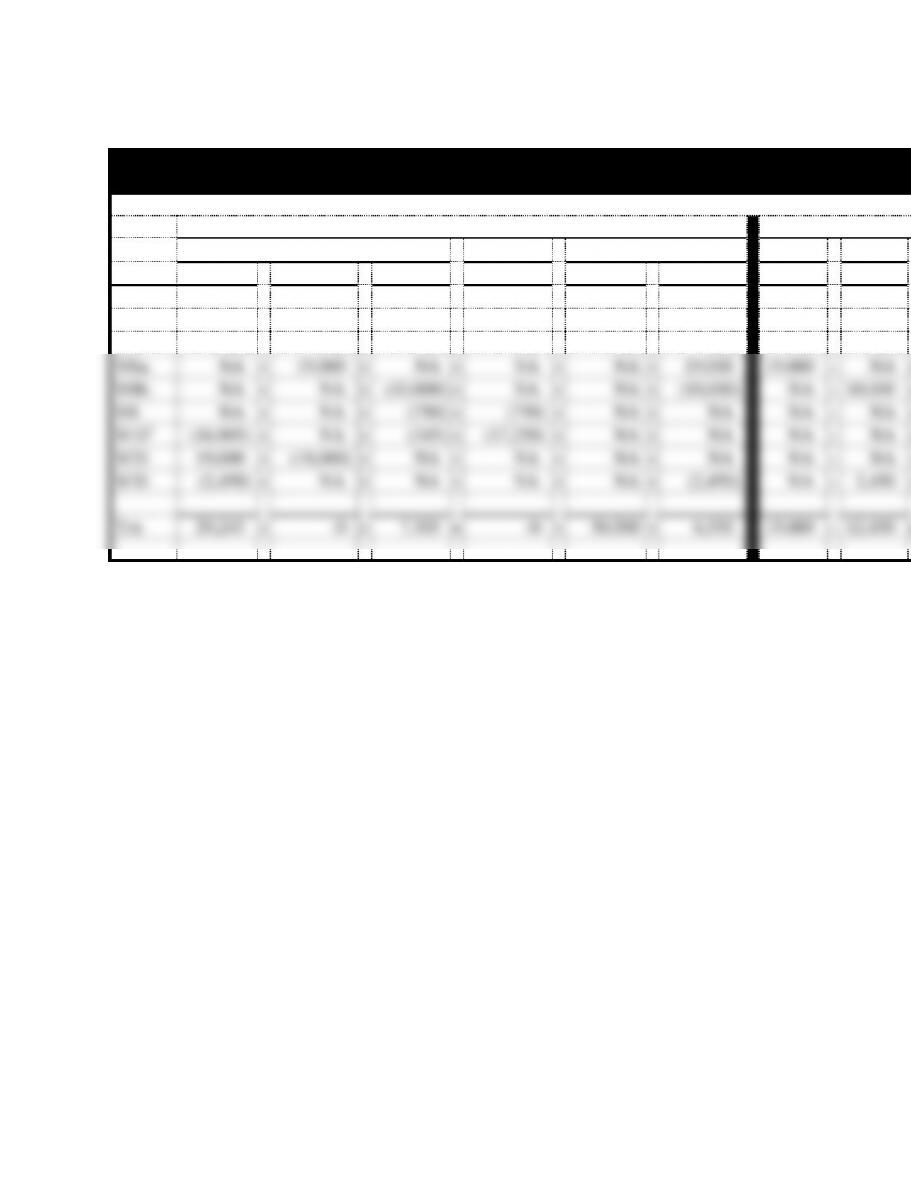

a.

Yang’s Imports

Effect of Transactions on Financial Statements Using Horizontal Statements Model

Balance Sheet

Income Statement

Date

Assets

=

Liab.

+

Stockholders’ Equity

Rev.

−

Exp.

=

Cash

+

Acc. Rec.

+

Inv.

=

Acct. Pay.

+

C. Stk.

+

Ret. Earn.

9/1

30,000

+

NA

+

NA

=

NA

+

30,000

+

NA

NA

−

NA

=

9/1

NA

+

NA

+

18,000

=

18,000

+

NA

+

NA

NA

−

NA

=

9/5

(400)

+

NA

+

400

=

NA

+

NA

+

NA

NA

−

NA

=

9/8a.

NA

+

19,000

+

NA

=

NA

+

NA

+

19,000

19,000

−

NA

=

9/8b.

NA

+

NA

+

(10,000)

=

NA

+

NA

+

(10,000)

NA

−

10,000

=

9/8

NA

+

NA

+

(750)

=

(750)

+

NA

+

NA

NA

−

NA

=

9/101

(16,905)

+

NA

+

(345)

=

(17,250)

+

NA

+

NA

NA

−

NA

=

9/20

19,000

+

(19,000)

+

NA

=

NA

+

NA

+

NA

NA

−

NA

=

9/30

(2,450)

+

NA

+

NA

=

NA

+

NA

+

(2,450)

NA

−

2,450

=

Tot.

29,245

+

-0-

+

7,305

=

-0-

+

30,000

+

6,550

19,000

−

12,450

=

1($18,000 − $750) = $17,250; $17,250 x .98 = $16,905 cash paid for inventory. Discount taken

$17,250 x 2% = $345.