Chapter 11 – Cost Behavior, Operating Leverage, and Profitability Analysis

11-1

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

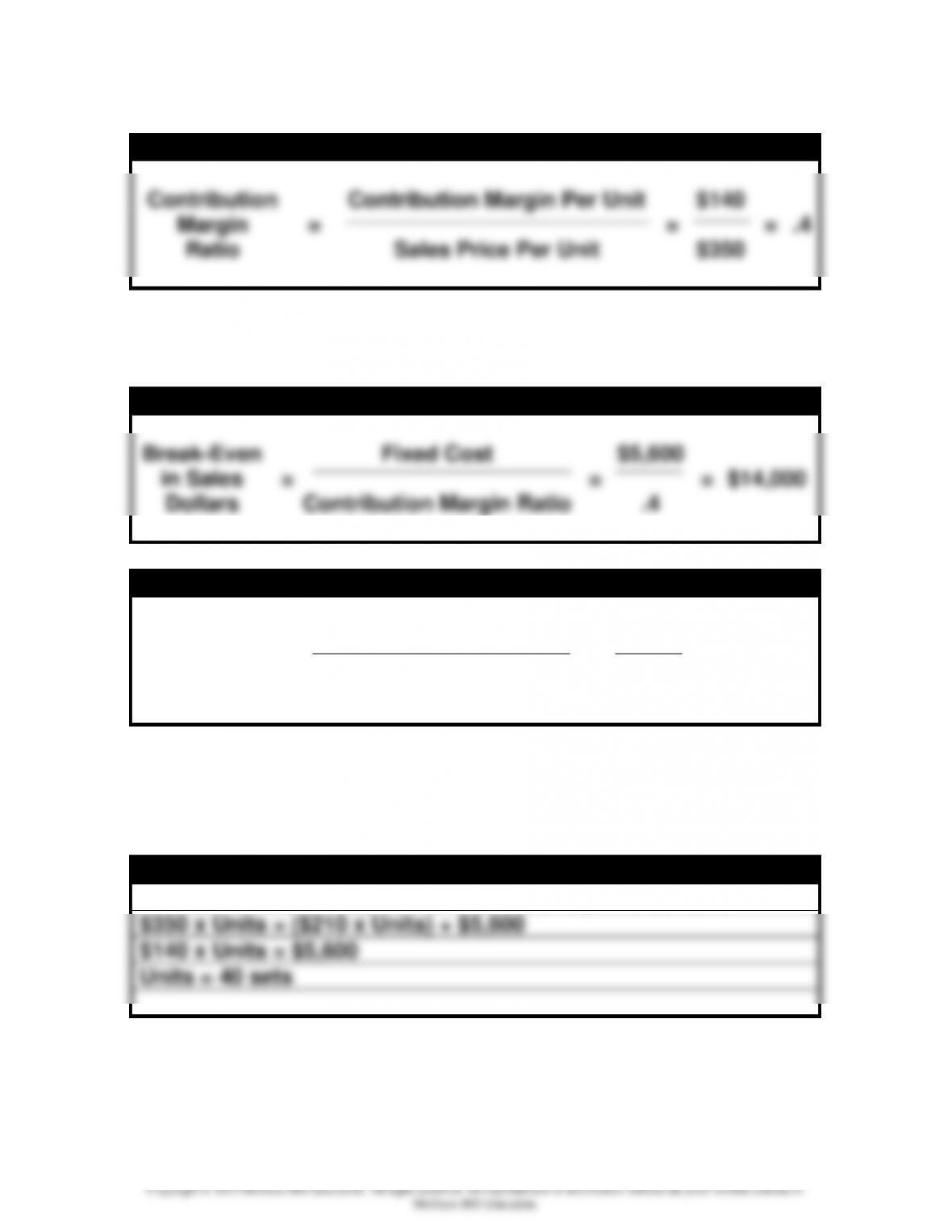

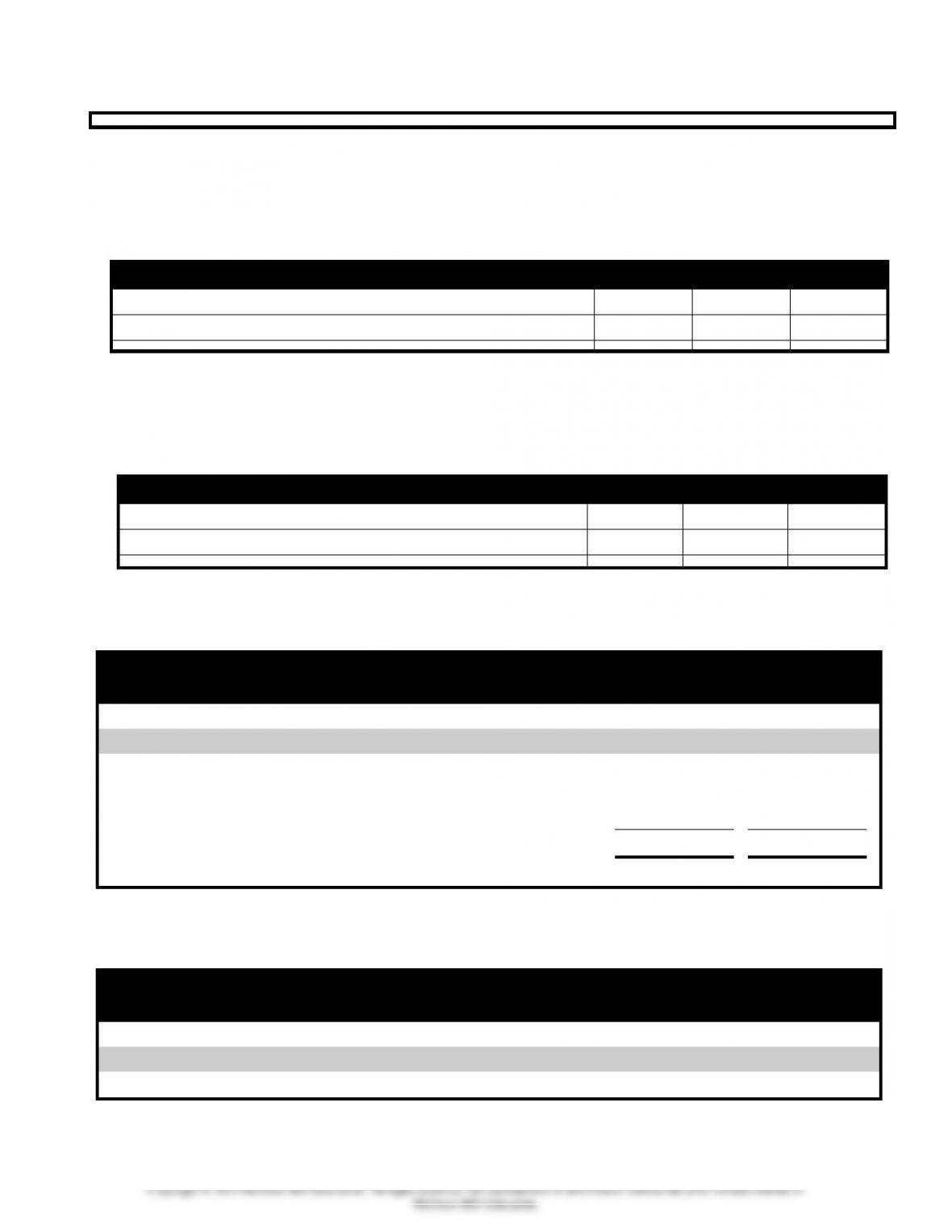

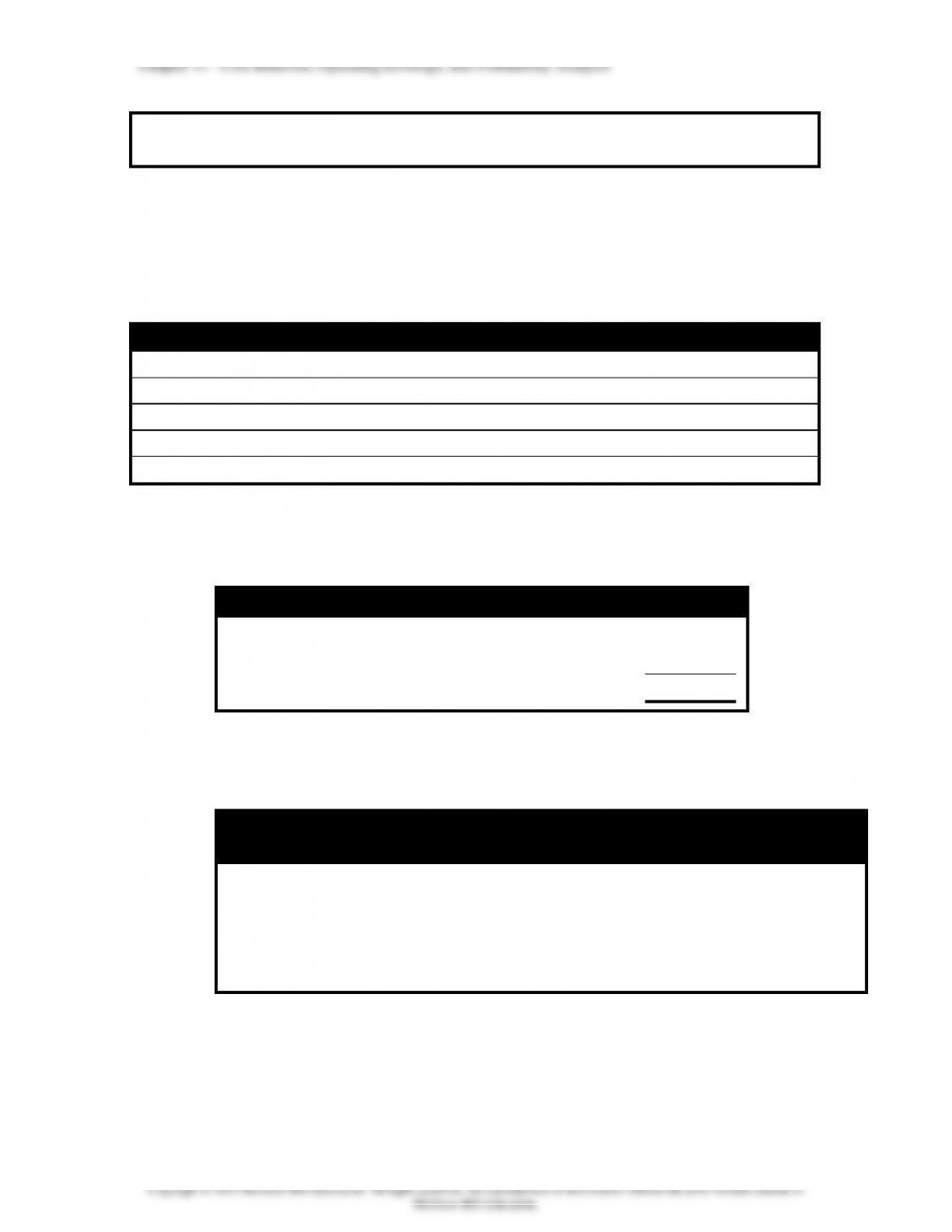

Contribution Margin Ratio

Contribution

Contribution Margin Per Unit

$140

Margin

=

=

=

.4

Ratio

Sales Price Per Unit

$350

(b) Using the contribution margin ratio, calculate the break–

even point in sales dollars and units.

Break-Even Point in Sales Dollars

Break-Even

Fixed Cost

$5,600

in Sales

=

=

=

$14,000

Dollars

Contribution Margin Ratio

.4

Break-Even Point in Number of Units

Break-Even

Total Sales

$14,000

in Units

=

=

=

40 Units

Sales Price Per Unit

$350

Demonstration Problem 11-4 Solution continued

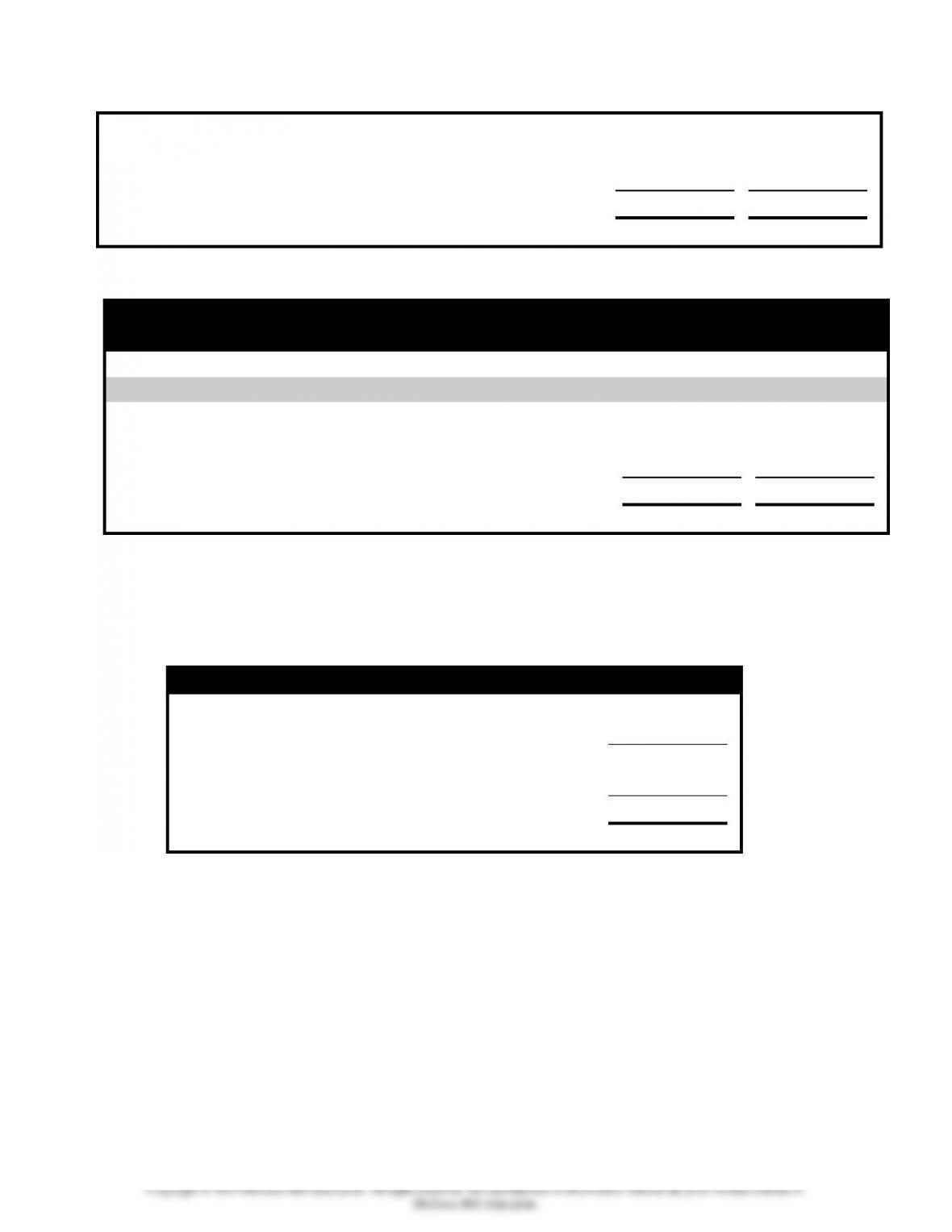

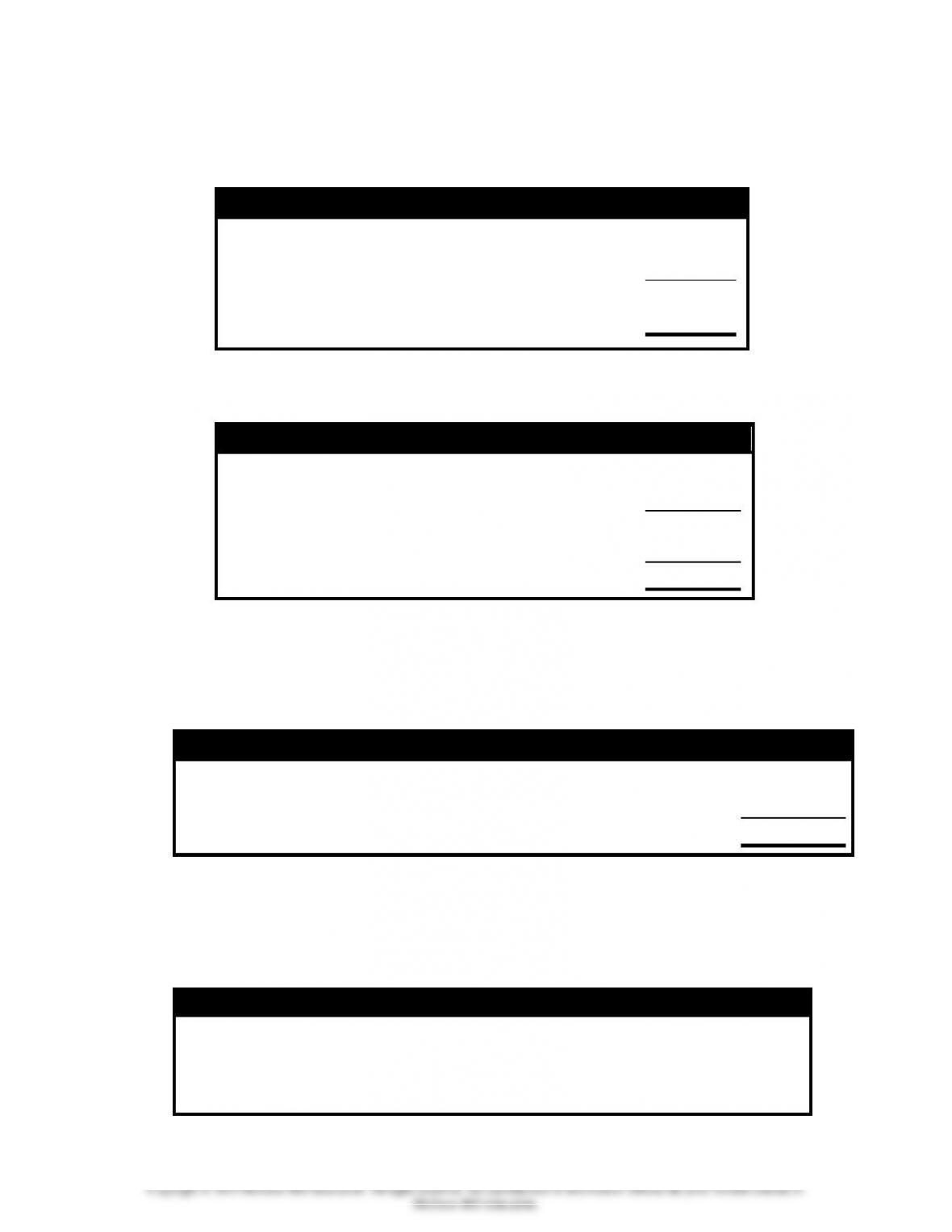

(3) Equation Approach

(a) Use the break-even equation and solve for number of units:

Break-Even Equation

Sales Price x Units = (Variable Cost x Units) + Fixed Cost

$350 x Units = ($210 x Units) + $5,600

$140 x Units = $5,600

Units = 40 sets

(b) Compute the break-even point in dollars as in part a3

above:

Chapter 11 – Cost Behavior, Operating Leverage, and Profitability Analysis

11-2

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

Break-Even Point in Sales Dollars

Sales Price

$ 350

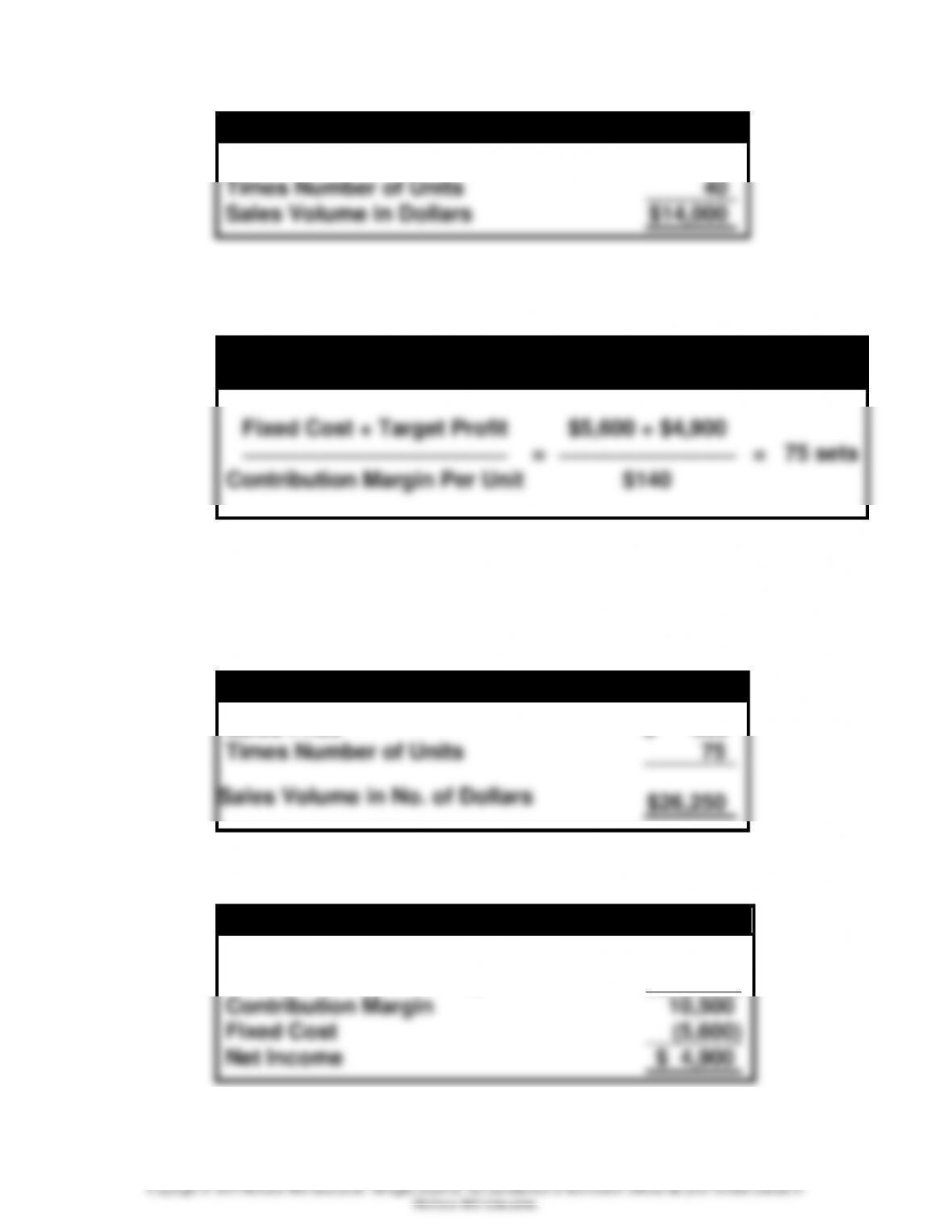

Times Number of Units

40

Sales Volume in Dollars

$14,000

b. Target profit

(1) Sales Volume Required to Earn a Desired Profit

Formula for Computation of Sales Volume Necessary to Earn

a Target Profit of $4,900

Fixed Cost + Target Profit

$5,600 + $4,900

⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯

=

⎯⎯⎯⎯⎯⎯⎯⎯

=

75 sets

Contribution Margin Per Unit

$140

Demonstration Problem 11-4 Solution continued

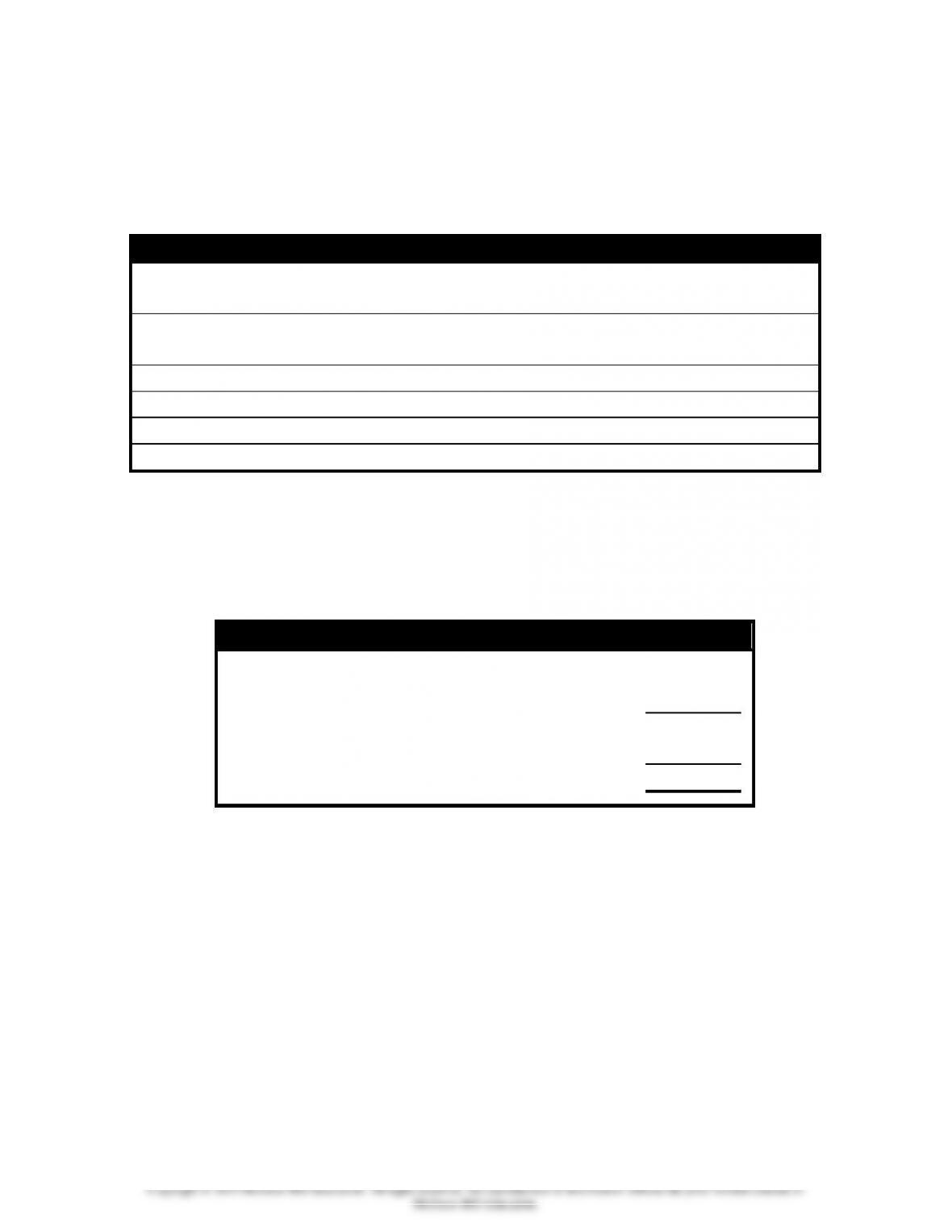

(2) Determine the sales volume in dollars required to earn the

desired profit.

Required Sales in Number of Dollars

Sales Price

$ 350

Times Number of Units

75

Sales Volume in No. of Dollars

$26,250

(3) Confirm the answers by preparing an income statement.

Income Statement

Sales

$26,250

Variable Cost (75 x $210)

(15,750)

Contribution Margin

10,500

Fixed Cost

(5,600)

Net Income

$ 4,900

Chapter 11 – Cost Behavior, Operating Leverage, and Profitability Analysis

11-3

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

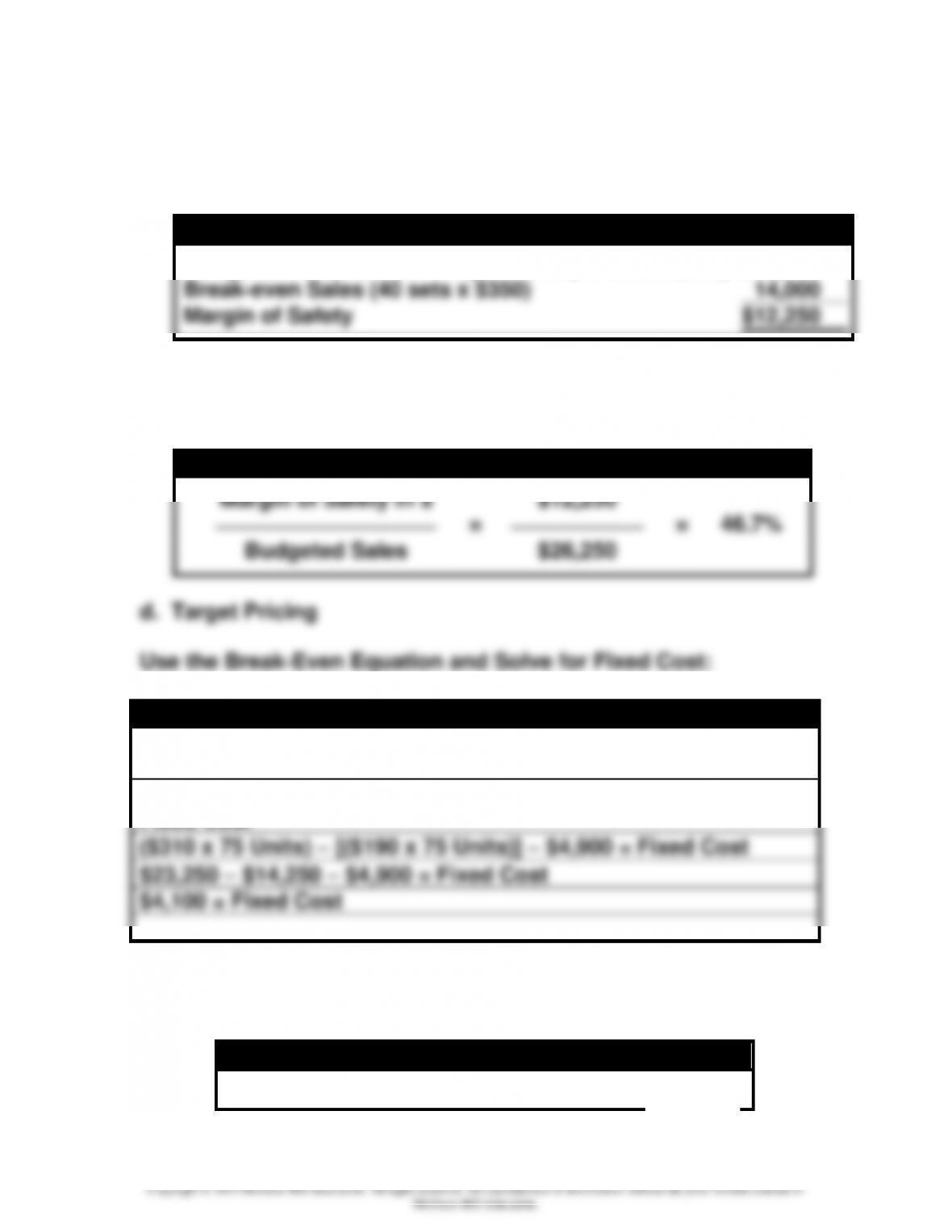

c. Margin of Safety

(1) Margin of Safety Expressed in Sales Dollars:

Margin of Safety

Budgeted Sales to Earn Target Profit (75 sets x $350)

$26,250

Break-even Sales (40 sets x $350)

14,000

Margin of Safety

$12,250

Demonstration Problem 11-4 Solution continued

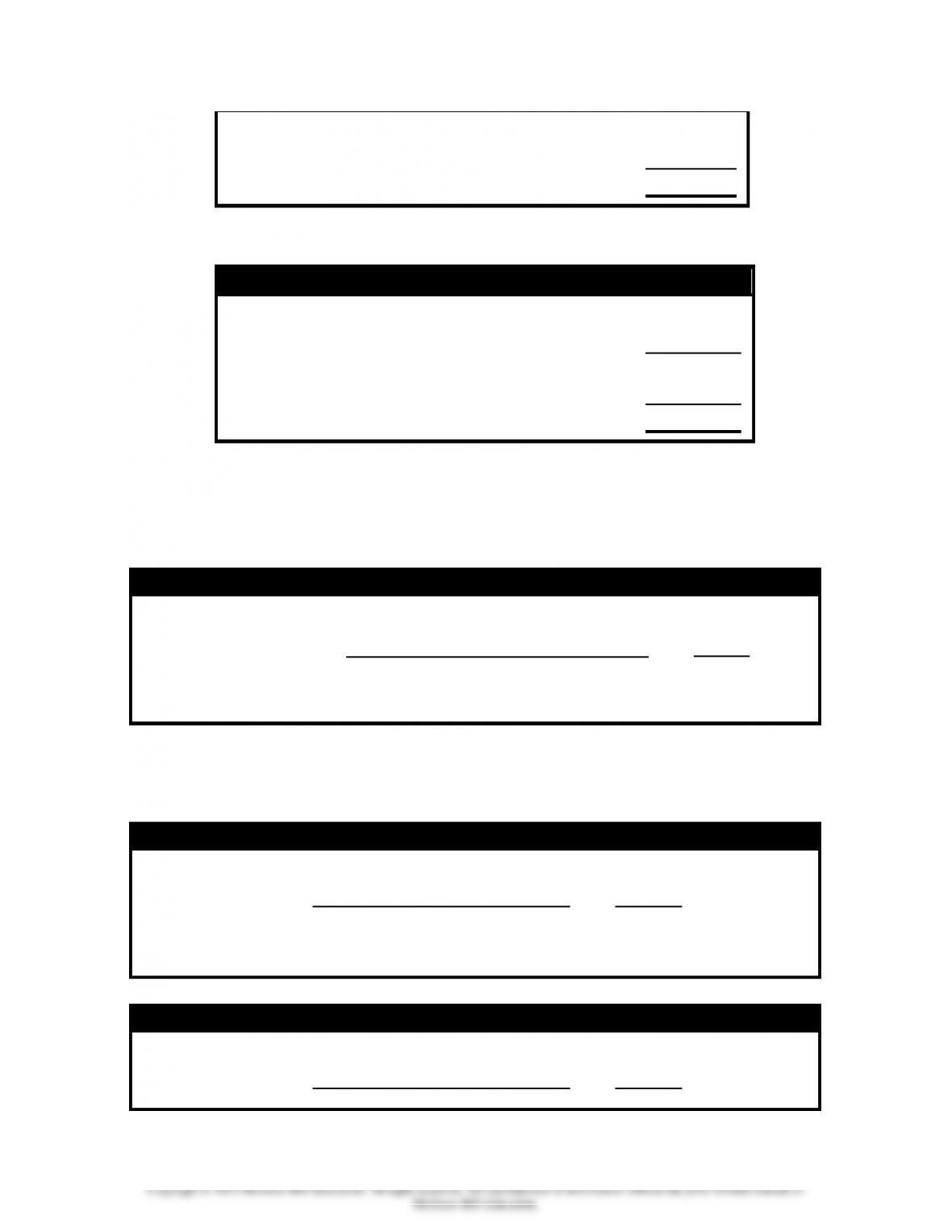

(2) Margin of Safety Expressed as a Percentage:

Margin of Safety Percentage

Margin of Safety in $

$12,250

⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯

=

⎯⎯⎯⎯⎯⎯

=

46.7%

Budgeted Sales

$26,250

d. Target Pricing

Use the Break-Even Equation and Solve for Fixed Cost:

Equation Approach to Compute Fixed Cost

Sales Price x Units = Fixed Cost + (Variable Cost Per Unit x

Units) + Profit

(Sales Price x Units) − [(Variable Cost Per Unit x Units)] − Profit =

Fixed Cost

($310 x 75 Units) − [($190 x 75 Units)] − $4,900 = Fixed Cost

$23,250 − $14,250 − $4,900 = Fixed Cost

$4,100 = Fixed Cost

Confirm the computations by preparing an income

statement.

Income Statement

Sales (75 x $310)

$23,250

Chapter 11 – Cost Behavior, Operating Leverage, and Profitability Analysis

11-4

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

Variable Cost (75 x $190)

(14,250)

Contribution Margin

9,000

Fixed Cost

(4,100)

Net Income

$ 4,900

Demonstration Problem 11-1 Work Papers

a.1.

Number of People Attending

1,000

2,000

4,000

Total Commission Cost

Average Commission Cost Per Person

Type of cost:

a.2.

Number of People Attending

1,000

2,000

4,000

Total Cost of Books

Average Per Unit Book Cost

Type of cost:

b.1.

Number of Tickets Sold

3,600

% Change

4,000

% Change

4,400

Revenue ($6 Per Ticket)

( %)

+ %

Commission Cost (Fixed)

Net Income

$ 1,600

( %)

$ 4,000

+ %

$ 6,400

Percentage Change in Revenue:

Percentage Change in Net Income:

b.2.

Number of Tickets Sold

3,600

% Change

4,000

% Change

4,400

Revenue ($6 Per Ticket)

( %)

$24,000

+ %

Commission Cost (Variable)

20,000

Net Income

$ 3,600

( %)

$ 4,000

+ %

$ 4,400

Chapter 11 – Cost Behavior, Operating Leverage, and Profitability Analysis

11-5

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

Percentage Change in Revenue:

Percentage Change in Net Income:

Demonstration Problem 11-1 Work Papers, continued

c.1. (Same as part a.1.)

Number of People Attending

1,000

2,000

4,000

Total Commission Cost

Average Commission Cost Per Person

Type of cost:

c.2.

Number of Exhibitions (a)

1

2

3

Total Expected Commission Cost

Cost Per Exhibition

Type of cost: Demonstration Problem 11-2 Work Papers

a.

My

Company

Your

Company

Number of Rafters

4,000

4,000

Revenue

Cost of Guides My Company

Fixed

Cost of Guides Your Company

Variable

Net income

b.

My

Company

Your

Company

Number of Rafters (a)

6,000

2,000

Revenue My Company

Chapter 11 – Cost Behavior, Operating Leverage, and Profitability Analysis

11-6

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

Revenue Your Company

Cost of Guides My Company

Fixed

Cost of Guides Your Company

Variable

Net Income

d.

My

Company

Your

Company

Number of Rafters

4,000

4,000

Revenue

Cost of Guides My Company

Fixed

Cost of Guides Your Company

Variable

Net Loss

Demonstration Problem 11-3 Work Papers

a. Income Statement Using a Contribution Margin Format,

Volume of 100 Deliveries

Revenue

Variable Expenses

Contribution Margin

Fixed Expenses

Net Income

b. Magnitude of Operating Leverage = Contribution Margin ÷

Net Income:

$________ ÷ $_________ = ___ times.

Therefore, a 10% increase in sales will produce a _________

increase in net income. Similarly, a 10% decrease in sales

will produce a __________ decrease in net income.

Chapter 11 – Cost Behavior, Operating Leverage, and Profitability Analysis

11-7

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

c. Income Statement Using a Contribution Margin Format,

Volume of 110 Deliveries

Revenue

Variable Expenses

Contribution Margin

Fixed Expenses

Net Income

(Alternative Net Income − Base Net Income) ÷ Base:

($______ − $______) ÷ $______ = _____%

Demonstration Problem 11-4 Work Papers

a. Break-even point

(1) Contribution Margin Per Unit Approach

(a) Determine the contribution margin per unit.

Per Unit Contribution Margin

Sales Price

$

$

(b) When the total contribution margin is sufficient to pay for

the fixed costs, Mr. Jamail will break even. The number of

units required to break even can be computed as follows:

Formula for Computation of Break-Even Point in Units

$

⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯

=

⎯⎯⎯⎯

=

$

(c) The break-even point in number of dollars can be

computed as follows:

Break-Even Point in Sales Dollars

Chapter 11 – Cost Behavior, Operating Leverage, and Profitability Analysis

11-8

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

Sales Price Per Unit

$

$

(d) Confirm the results by preparing an income statement.

Income Statement

Sales

$

( )

( )

Net Income

$ 0

Demonstration Problem 11-4 Work Papers, continue

(2) Contribution Margin Ratio Approach

(a) The contribution margin ratio is computed as follows.

Contribution Margin Ratio

Contribution

$

Margin

=

=

=

Ratio

$

(b) Using the contribution margin ratio, calculate the break–

even point in sales dollars and units.

Break-Even Point in Sales Dollars

Break-Even

$

in Sales

=

=

=

$

Dollars

Break-Even Point in Number of Units

Break-Even

$

in Units

=

=

=

11-9

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

$

Demonstration Problem 11-4 Work Papers, continued

(3) Equation Approach

(a) Use the break-even equation and solve for number of units:

Break-Even Equation

(b) Compute the break-even point in dollars as in part a3

above:

Break-Even Point in Sales Dollars

Sales Price

$

$

b. Target profit

(1) Sales Volume Required to Earn a Desired Profit

Formula for Computation of Sales Volume Necessary to Earn

a Target Profit of $4,900

⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯

=

⎯⎯⎯⎯⎯⎯⎯⎯

=

Demonstration Problem 11-4 Work Papers, continued

Chapter 11 – Cost Behavior, Operating Leverage, and Profitability Analysis

11–10

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

(2) Determine the sales volume in dollars required to earn the

desired profit.

Required Sales in Number of Dollars

Sales Price

$

$

(3) Confirm the answers by preparing an income statement.

Income Statement

Sales

$

( )

( )

Net Income

$

c. Margin of Safety

(1) Margin of Safety Expressed in Sales Dollars:

Margin of Safety

$

$12,250

Demonstration Problem 11-4 Work Papers, continued

(2) Margin of Safety Expressed as a Percentage:

Margin of Safety Percentage

$

⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯

=

⎯⎯⎯⎯⎯⎯

=

$

Chapter 11 – Cost Behavior, Operating Leverage, and Profitability Analysis

11–11

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

d. Target Pricing

Use the Break-Even Equation and Solve for Fixed Cost:

Equation Approach to Compute Fixed Cost

Confirm the computations by preparing an income

statement.

Income Statement

Sales

$

( )

( )

Net Income

$ 4,900