7-1

ANSWERS TO QUESTIONS – CHAPTER 7

1. Cash payments to creditors is an asset use transaction. This type of transaction will

reduce both assets and liabilities.

3. The entry to record accrued interest consists of an increase to Interest Expense and an

increase to Interest Payable. The transaction is a claims exchange transaction and

reduces equity and increases liabilities.

5. The going concern assumption states that businesses will continue to operate in the future.

6. An adjustment for accrued but unpaid interest is necessary for the accounting records to

reflect the correct amount of liability and the correct amount of interest expense.

9. A contingent liability is a potential liability arising from a past event.

10. The three categories of contingent liabilities are:

11. Only those contingent liabilities that are probable and reasonably estimated are recorded

on the books.

liabilities that are remote are not recorded or disclosed in the financial statements.

14. A warranty is a guarantee of a product or service.

15. Recognizing future warranty obligations will increase liabilities and decrease equity. It

has the effect of increasing expenses thereby decreasing net income.

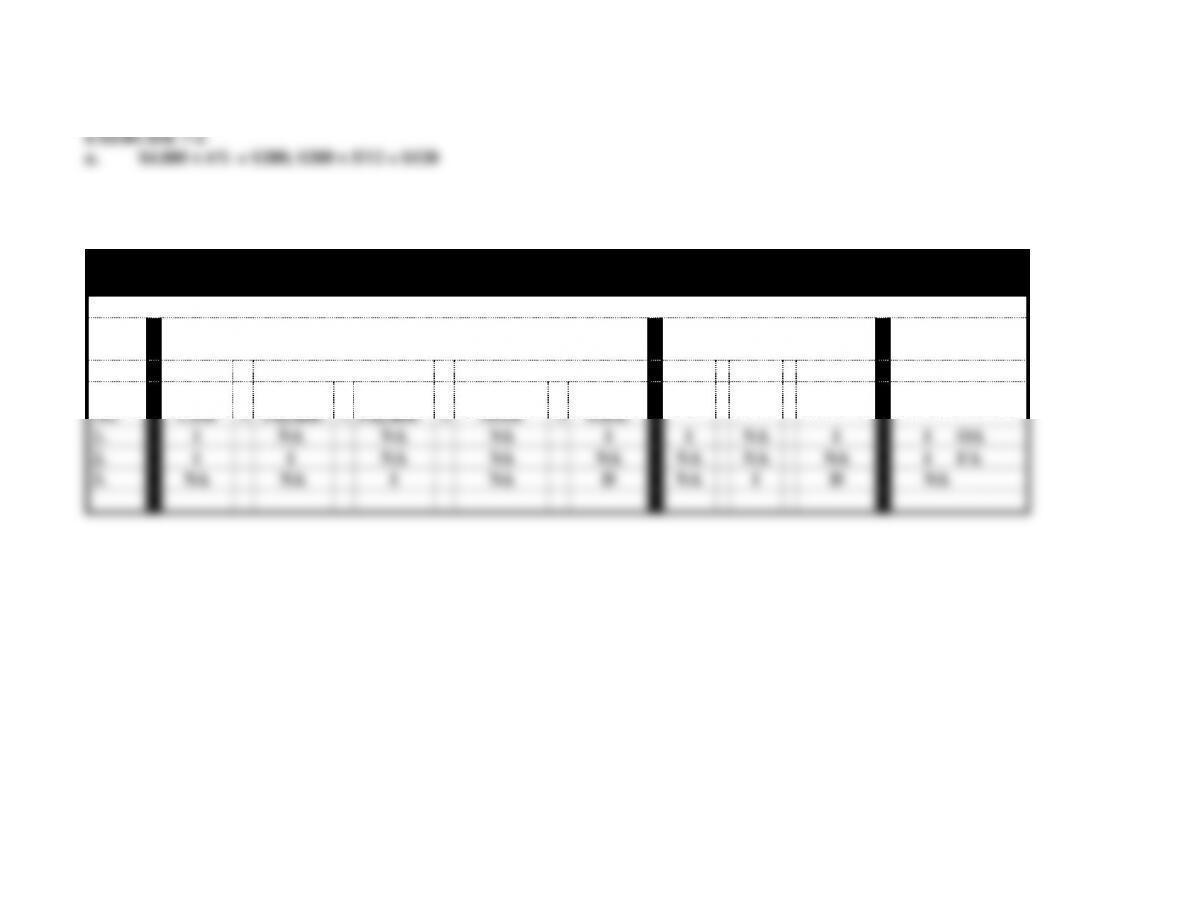

18.

Principal

Payment

Interest

Reduction

Period

Bal. 1/1

12/31

Exp. 8%

of Prin.

1

$ 72,000

$16,246

$5,760

$10,486

2

61,514

16,246

4,921

11,325

3

50,189

19. A line of credit is a preapproved amount of credit that is available to a business to use as

20. A business may need to borrow funds for a short period of time or a longer period. Most

short-term financing is in the form of loans from financial institutions. However, when a

21. One of the primary advantages of bond financing is that the company can usually obtain

22. One of the primary disadvantages of a bond issue is the restrictions that may be placed on

23. One reason that a company may be able to borrow money more cheaply if bonds are

issued rather than borrowing the money from a financial institution is the way financial

institutions make their money. Banks receive money from customers through

7-3

24. The issuance of $100,000, 5%, 10-year bonds at face value will result in an increase to

25. The mechanism that is used to adjust the stated interest rate to the market rate of interest

is called bond discount and bond premium.

26. When the effective interest rate is higher than the stated interest rate, the bond will sell at

27. The issuance of bonds by a company is an asset source transaction. Assets increase and

liabilities increase.

28. The passage of time is usually the cause of the effective interest rate and the stated

interest rate being different. When bonds are issued, the interest rate is set, usually at the

29. The cash received for the bond will be $975 ($1,000 x .975).

31. The carrying value of the bonds is $19,800 ($25,000 face minus $5,200 discount). The

carrying value of the bond represents the liability at any point in time.

32. When the effective interest rate is higher than the stated interest rate, interest expense

33. A classified balance sheet is one that separates assets and liabilities into current and

noncurrent items.

7-4

SOLUTIONS TO EXERCISES – CHAPTER 7

EXERCISE 7-1

a. $-0-. Interest will be paid at maturity of the note, April 30, 2014.

d. $61,800 [$60,000 principal + $1,800 interest ($60,000 x 6% x 6/12)]

7-5

b. $-0-, no interest was paid in 2014; interest will be paid in 2015.

c.

Jackson Company

Statements Model for 2014

Balance Sheet

Income Statement

Statement of

Cash Flows

Event

Assets

=

Liabilities

+

Stockholders’ Equity

Rev.

–

Exp.

=

Net Inc.

No.

Cash

=

Notes

Payable

+

Int.

Payable

+

Common

Stock

+

Ret.

Earn.

1.

I

NA

NA

NA

I

I

NA

I

I OA

2.

I

I

NA

NA

NA

NA

NA

NA

I FA

3.

NA

NA

I

NA

D

NA

I

D

NA

7-6

EXERCISE 7-3

a. Book Sales $215,000

b. Total Sales:

Event 1 $215,000

Total $375,000

Total Sales $375,000

7-7

EXERCISE 7-4

a.

Assets

=

Liabilities

+

Stockholder’s Equity

Income Statement

Statement of

Event

Cash

=

Sales Tax

Pay.

+

Com. Stock

+

Ret. Earn.

Rev.

−

Exp.

=

Net Inc.

Cash

Flow

1. Nov.

91,800

6,800

NA

85,000

85,000

NA

85,000

91,800 OA

2. Dec.

(6,800)

(6,800)

NA

NA

NA

NA

NA

(6,800) OA

3. Dec.

105,840

7,840

NA

98,000

98,000

NA

98,000

105,840 OA

b. Total sales tax paid in 2013: $6,800

c. Total sales tax collected in 2013: $6,800 + $7,840 = $14,640

7-8

EXERCISE 7-5

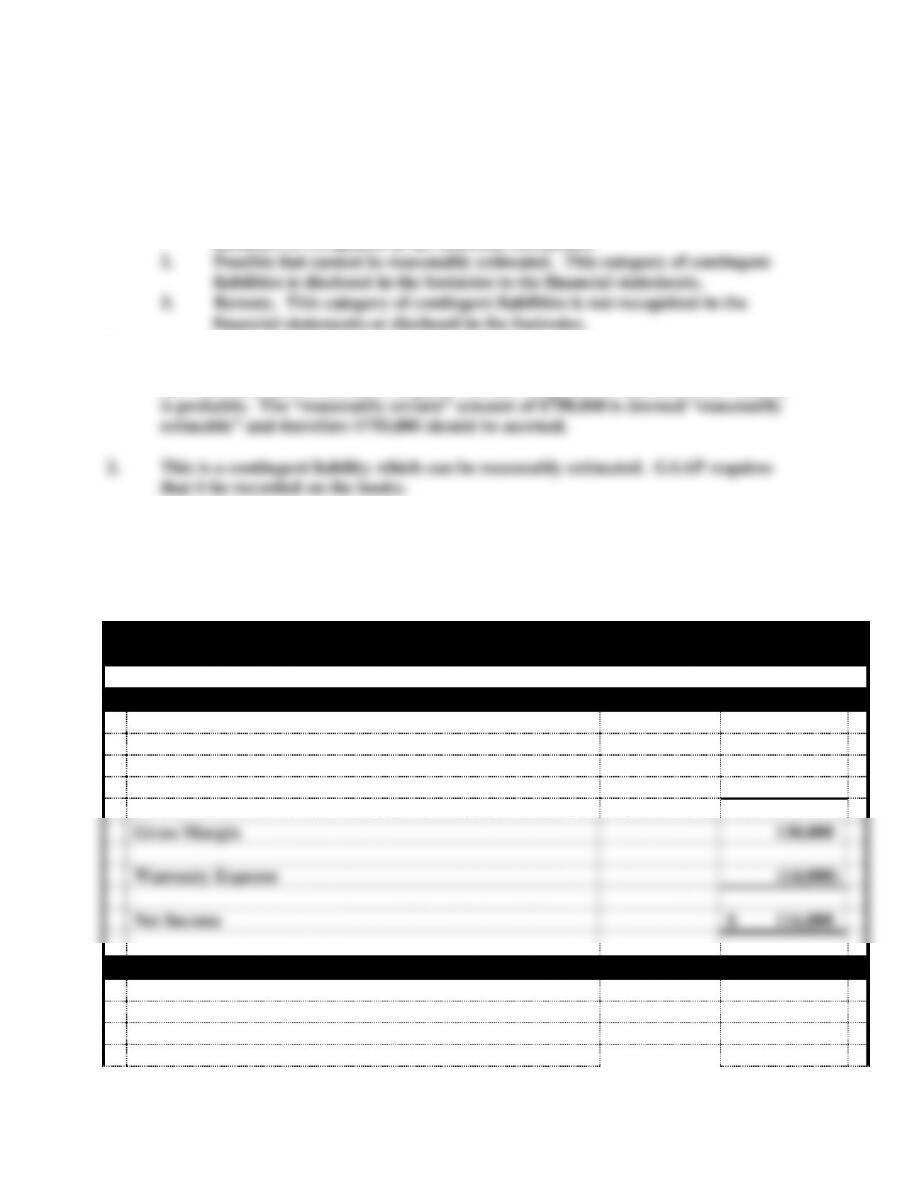

a. There are three categories of contingent liabilities:

1. Probable and can be reasonably estimated. This category of contingent

liabilities is recognized in the financial statements.

b.

1. This is a contingent liability. The event occurred. The lawsuit has been filed, and

the “attorney knows that the company will have to pay…”. Therefore, the liability

3. This is not a contingent liability since the likelihood of damage is not certain. It is

not recorded on the books or mentioned in the financial statements.

EXERCISE 7-6

a.

Devon’s Computers

Financial Statements

Income Statement

Sales Revenue

$280,000

Cost of Goods Sold

(150,000)

Gross Margin

130,000

Warranty Expense

(14,000)

Net Income

$ 116,000

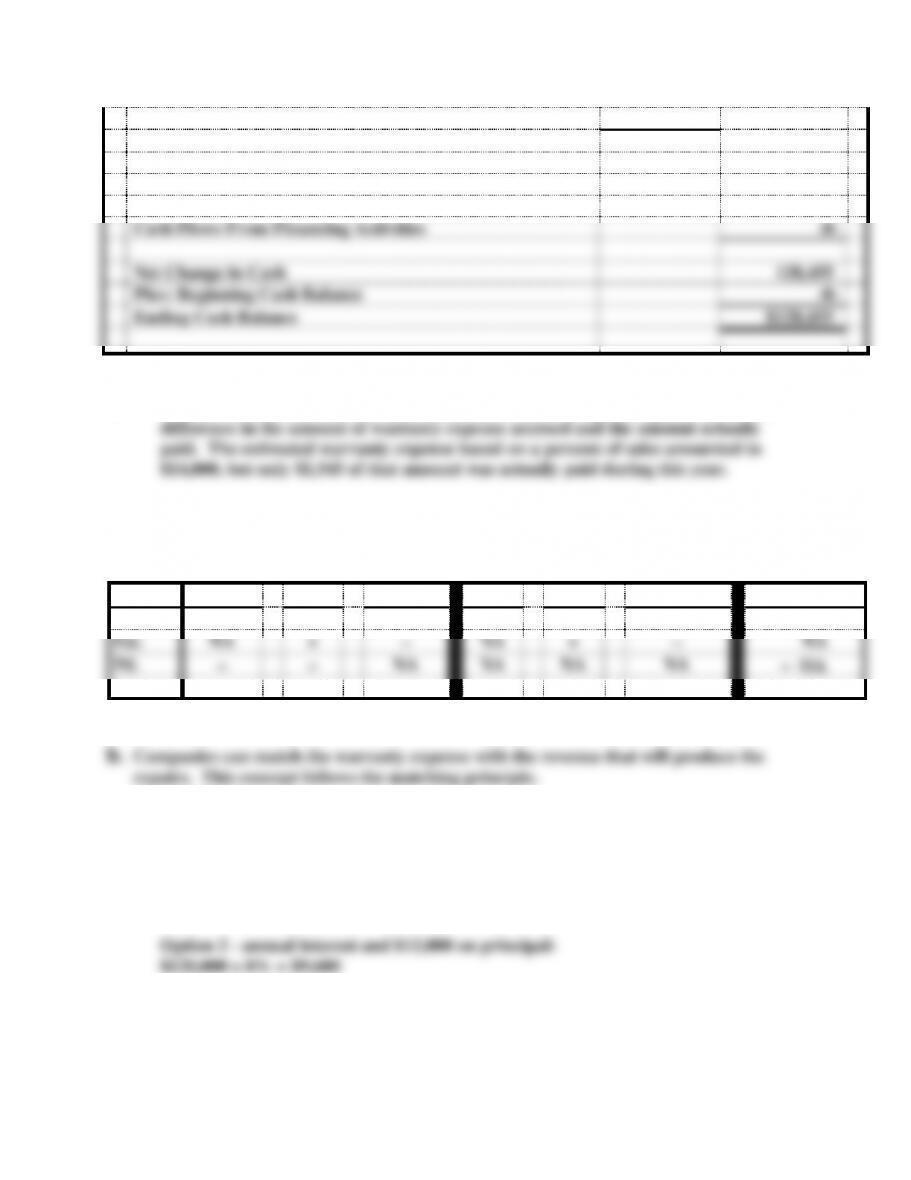

Statement of Cash Flows

Cash Flows From Operating Activities:

Inflow from Customers

$280,000

Outflow for Inventory

(150,000)

7-9

Outflow for Warranty Expense

(1,545)

Net Cash Flow from Operating Activities

$128,455

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities

-0-

Net Change in Cash

128,455

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$128,455

b. The difference between net income and cash flows from operating activities is the

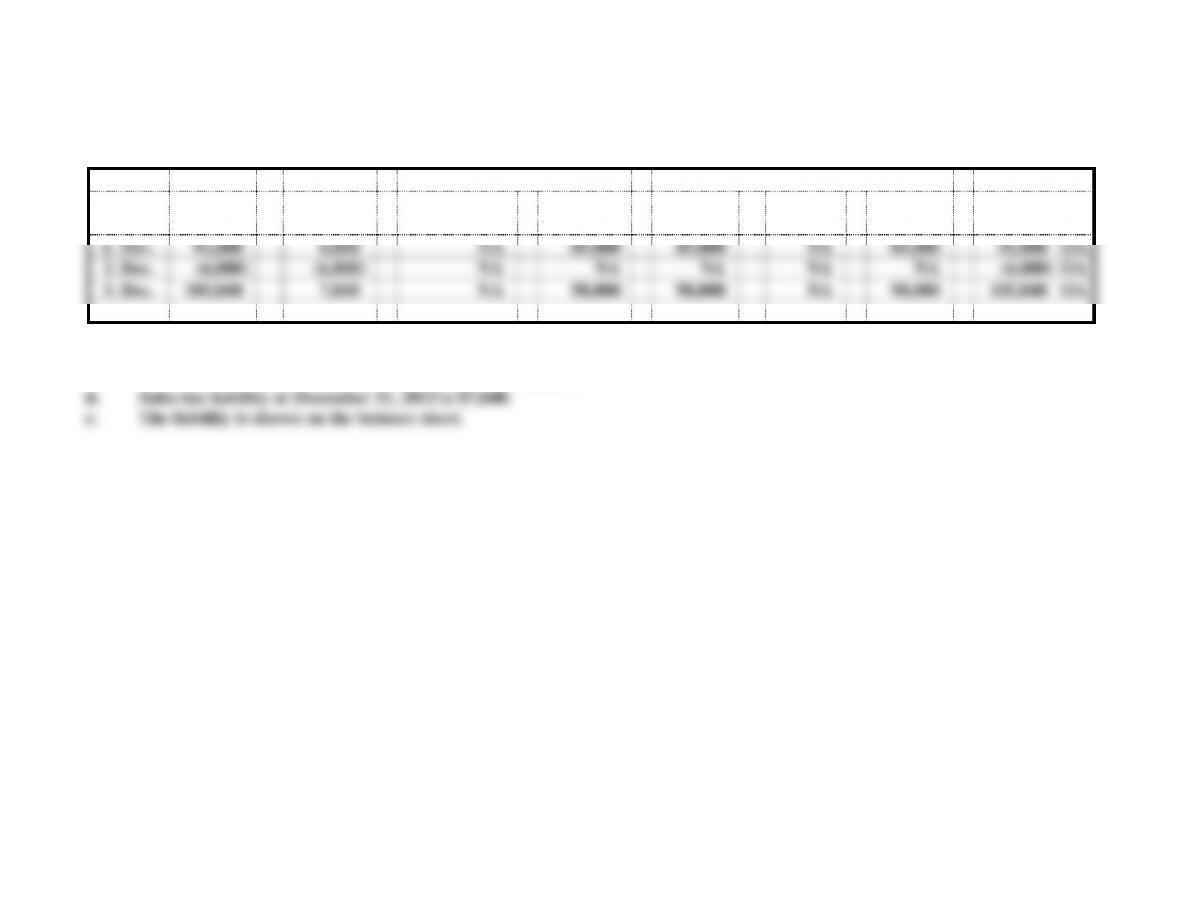

EXERCISE 7-7

a.

Event

Assets

=

Liab.

+

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Est.

NA

+

−

NA

+

−

NA

Pd.

−

−

NA

NA

NA

NA

− OA

c. EXERCISE 7-8

a. Year 1

Option 1 – annual interest only:

$120,000 x 8% = $9,600

Note: The amount of interest paid in year 1 is the same under both options because no

payment was made on the principal until the end of the year under option two.

7-10

b. Year 2

Option 1 – annual interest only:

$120,000 x 8% = $9,600

Option 2 – annual interest and $12,000 on principal:

Note: Under option two, less interest will be paid in year two and in future years because

the amount subject to interest is less.

c. Under option one, only annual interest is paid. This is a desirable option if a company

EXERCISE 7-9

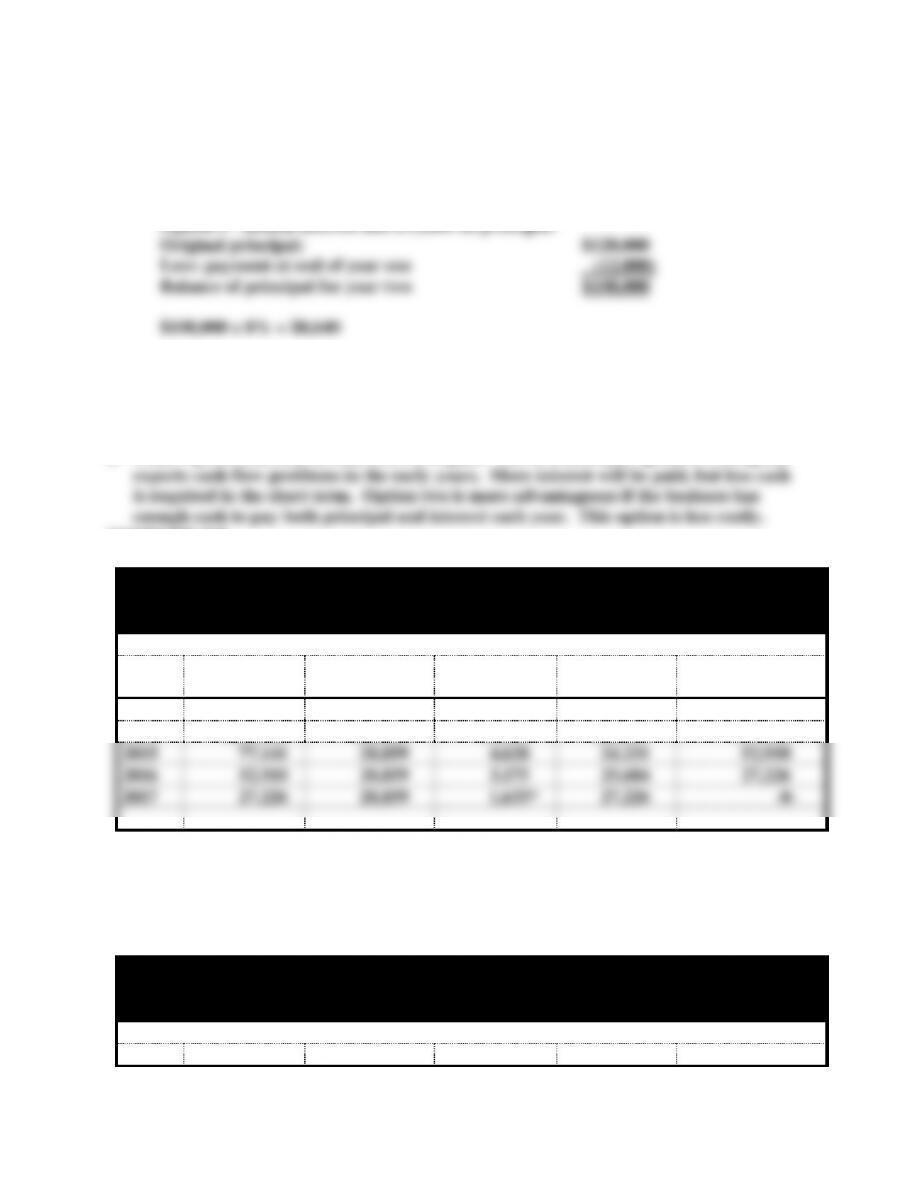

Hatch Co.

Amortization Schedule

$100,000, 4-Yr. Term Note, 6% Interest Rate

Year

Prin. Bal. on

Jan 1

Cash Pay. Dec.

31

Applied to

Interest

Applied to

Principal

Prin. Bal.

End of Period

2014

$100,000

$28,859

$6,000

$22,859

$77,141

2015

77,141

28,859

4,628

24,231

52,910

2016

52,910

28,859

3,175

25,684

27,226

2017

27,226

28,859

1,633*

27,226

-0-

*Adjusted due to rounding.

EXERCISE 7-10

The first four years are provided for the use of the instructor:

Mills Company

Amortization Schedule

$60,000, 10-Yr. Term Note, 6% Interest Rate

Prin. Bal. on

Cash Pay. Dec.

Applied to

Applied to

Prin Bal.

7-11

Year

Jan 1

31

Interest

Principal

End of Period

2014

$60,000

$8,152

$3,600

$4,552

$55,448

2015

55,448

8,152

3,327

4,825

50,623

2016

50,623

8,152

3,037

5,115

45,508

2017

45,508

8,152

2,730

5,422

40,086

a.

(1) $3,600

(2) $4,552

EXERCISE 7-11

a. $2,500 $50,000 = .05 or 5

Effect of Transactions on Financial Statements

Balance Sheet

Income Statement

Statement of

No.

Assets

=

Liab.

+

S. Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

2014

1.

50,000

=

50,000

+

NA

NA

−

NA

=

NA

50,000 FA

2015

2.

(11,549)

=

(9,497)

+

(2,052)

NA

−

2,052

=

(2,052)

(9,497) FA

(2,052) OA

c. (1)

Revenue

$75,000

Expenses

Operating Expenses

$35,000

Interest Expense

2,500

Total Expenses

(37,500)

Net Income

$ 32,500

(2) Outflow for Expenses

(37,500)

Net Cash Flow from Operating Activities

$32,500