Chapter 14 Planning for Profit and Cost Control

14-1

Answers to Questions

1. Budgets are useful for large companies with complex activities as well as small

companies. Budgets act as a vehicle for communication by formalizing management’s

2. The budget represents the companywide plans stated in financial terms as to how to

coordinate operating activities to accomplish goals and objectives. Accordingly, its

the master budget.

3. The three levels of planning are as follows:

(1) Strategic planning – the long-run planning activities that address issues such as

overall company goals and objectives.

4. The span of time is the primary factor that distinguishes the three levels of planning

5. The perpetual budget has the advantage of keeping management involved in the budget

6. The primary advantages associated with budgeting are as follows:

Planning – formalizes management’s plans in a document that communicates company

objectives.

Corrective action – acts as an early warning system that promotes corrective action.

7. Budgeted amounts represent management’s expectations regarding how the firm as a

whole and individual departments within the firm should perform. By comparing

Chapter 14 Planning for Profit and Cost Control

14-2

8. Mr. Shilov’s failure with budgets seems to stem from his misunderstanding of the

human element. He states that “he made budgets.” Experience shows that, in general,

the budget and would be unmotivated to accomplish budget standards.

10. The sales forecast normally functions as the starting point for the development of the

master budget. Clearly, production and other related activities depend upon the level

of sales.

11. The cash budget is composed of three major components:

(1) Cash receipts – expected cash inflows from sales, sale of investments, and

borrowing activities, etc.

12. Determining the amount of the cash balance to include on the budgeted balance sheet is

an insignificant reason for preparing a cash budget. The real purpose of preparing a

cash budget is to enable a company to effectively manage its financing and investing

The pro forma income statement provides information about the expected profitability of the

company. The completion of this statement is dependent on the departmental operating

Chapter 14 Planning for Profit and Cost Control

14-3

13. The cash budget, like the pro forma statement of cash flows, provides information as to

Exercise 14-1

Ms. Weller appears to be a person with an attitude problem. She does not understand how to

involve her colleagues in the budgeting process. She degrades their input and uses the budget

as a tool for criticism. In so doing, Ms. Weller has failed to gain the support of upper-level

management. The attitudes of upper-level management will have a significant impact on the

change. Perhaps the most effective solution in this case is to replace Ms. Weller.

Exercise 14-2

a.

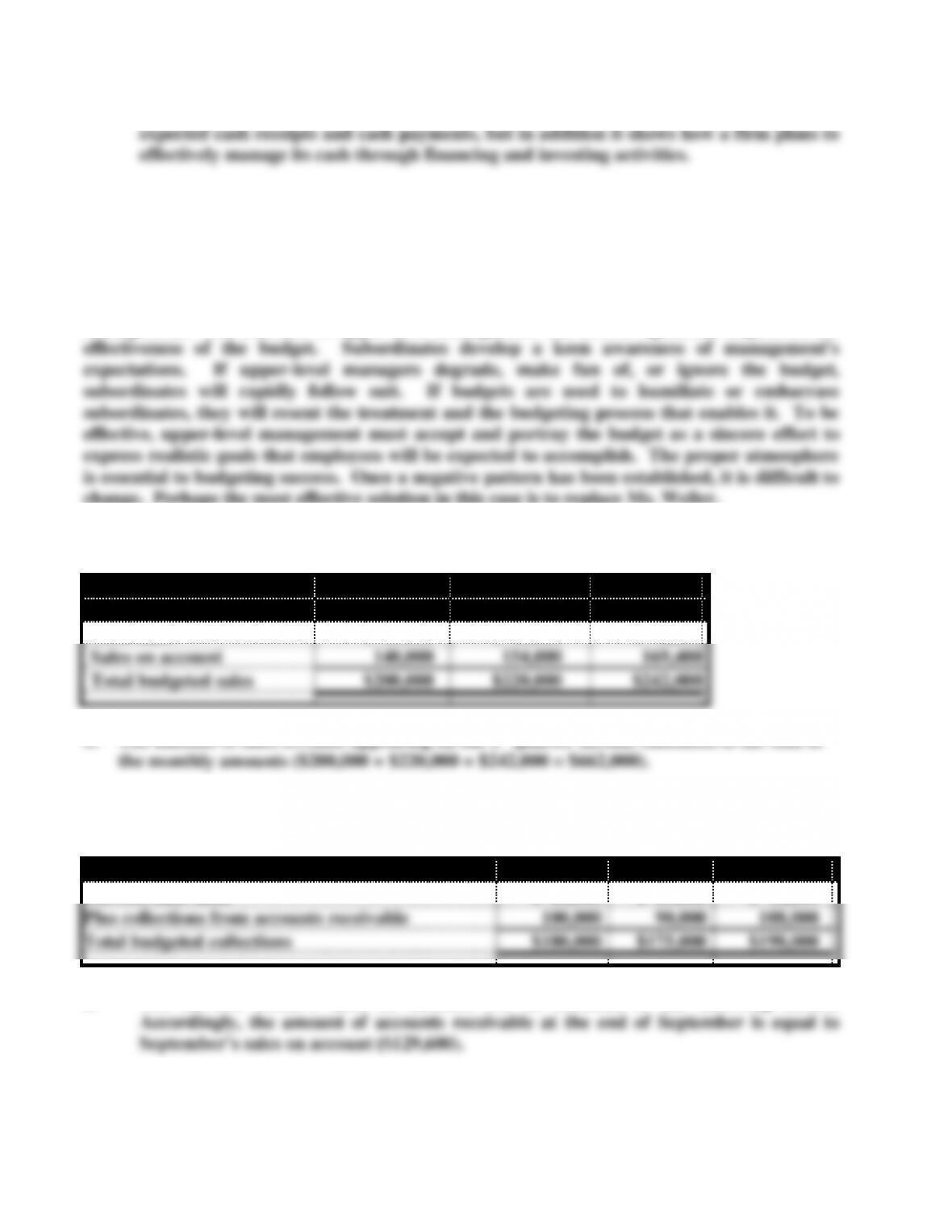

Sales Budget

January

February

March

Cash sales

$ 60,000

$ 66,000

$ 72,600

Sales on account

140,000

154,000

169,400

Total budgeted sales

$200,000

$220,000

$242,000

b. The amount of sales revenue appearing on the 1st quarter income statement is the sum of

Exercise 14-3

a.

Schedule of Cash Receipts

July

August

September

Current cash sales

$ 80,000

$ 85,000

$ 90,000

Plus collections from accounts receivable

100,000

90,000

108,000

Total budgeted collections

$180,000

$175,000

$198,000

b. The current month’s sales on account will be collected in the following month.

Exercise 14-4

a.

Chapter 14 Planning for Profit and Cost Control

14-4

1st Quarter

2nd Quarter

3rd Quarter

4th Quarter

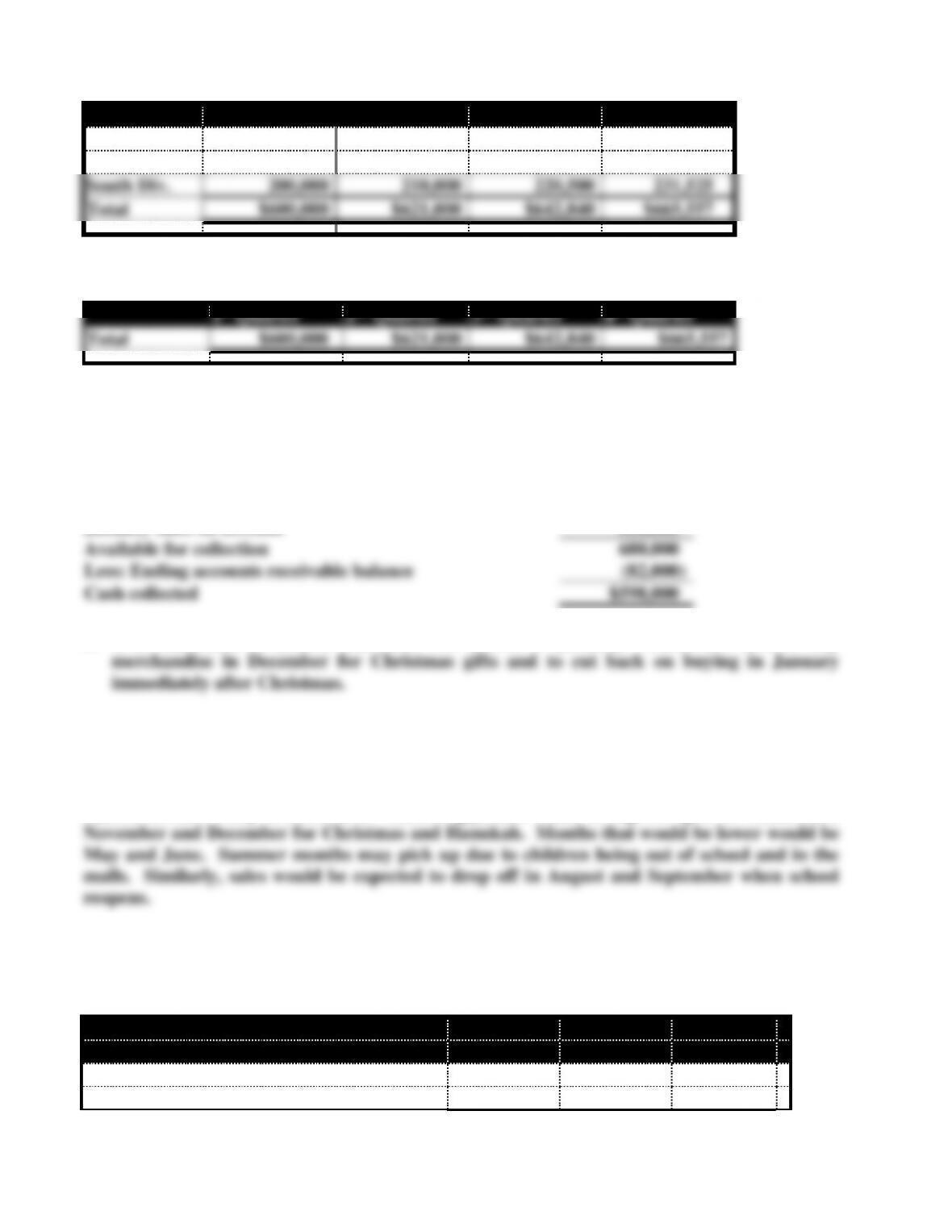

East Div.

$150,000

$156,000

$162,240

$168,730*

West Div.

250,000

255,000

260,100

265,302

South Div.

200,000

210,000

220,500

231,525

Total

$600,000

$621,000

$642,840

$665,557

*Rounded

b.

1st Quarter

2nd Quarter

3rd Quarter

4th Quarter

Total

$600,000

$621,000

$642,840

$665,557

Exercise 14-5

a. Sales for January are expected to be $560,000 ($800,000 x 0.70)

Beginning accounts receivable balance

$120,000

January sales on account

560,000

Available for collection

680,000

Less: Ending accounts receivable balance

(82,000)

Cash collected

$598,000

b. It is reasonable to assume that sales will decline in January. Customers tend to buy

Exercise 14-6

Sales would likely be highest in late January or early February because of Valentine’s Day

sales. October may also produce higher sales due to buying for Halloween. Other holiday

seasons are also likely to boost sales. Accordingly, sales would be high in April for Easter, and

Exercise 14-7

a.

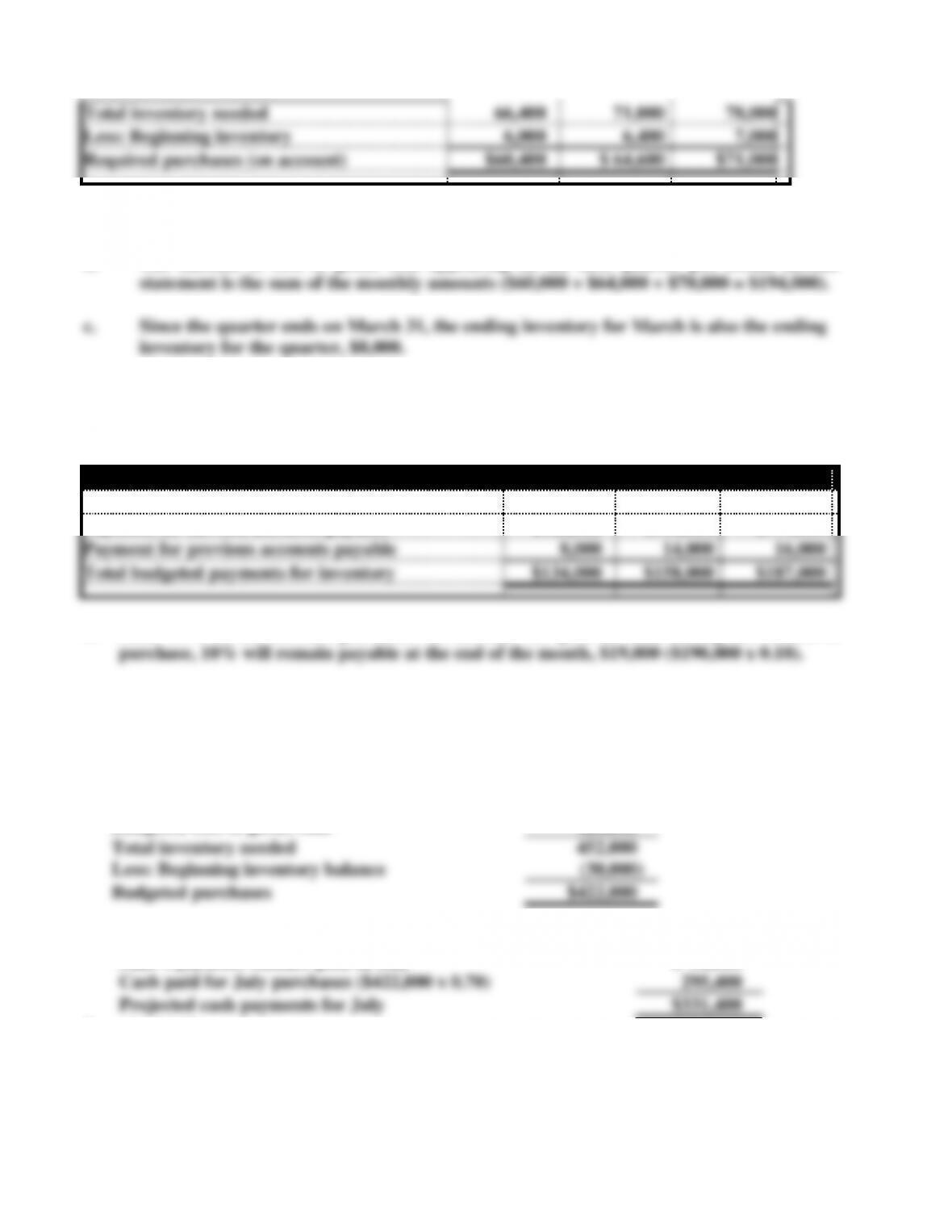

Inventory Purchases Budget

January

February

March

Budgeted cost of goods sold

$60,000

$ 64,000

$70,000

Plus: Desired ending inventory

6,400

7,000

8,000

Chapter 14 Planning for Profit and Cost Control

14-5

Total inventory needed

66,400

71,000

78,000

Less: Beginning inventory

6,000

6,400

7,000

Required purchases (on account)

$60,400

$ 64,600

$71,000

Exercise 14-7 (continued)

b. The amount of cost of goods sold appearing on the first quarter pro forma income

Exercise 14-8

a.

Schedule of Cash Payments for Inventory Purchases

April

May

June

Payment for current accounts payable

$126,000

$144,000

$171,000

Payment for previous accounts payable

8,000

14,000

16,000

Total budgeted payments for inventory

$134,000

$158,000

$187,000

b. Since 90% of the current purchases on account are paid in cash during the month of

Exercise 14-9

a. Budgeted cost goods sold for July is $420,000 ($400,000 x 1.05)

Ending inventory balance

$ 32,000

Budgeted cost of goods sold

420,000

Total inventory needed

452,000

Less: Beginning inventory balance

(30,000)

Budgeted purchases

$422,000

b.

June’s payables balance paid in July

$ 36,000

Cash paid for July purchases ($422,000 x 0.70)

295,400

Projected cash payments for July

$331,400

Exercise 14-10

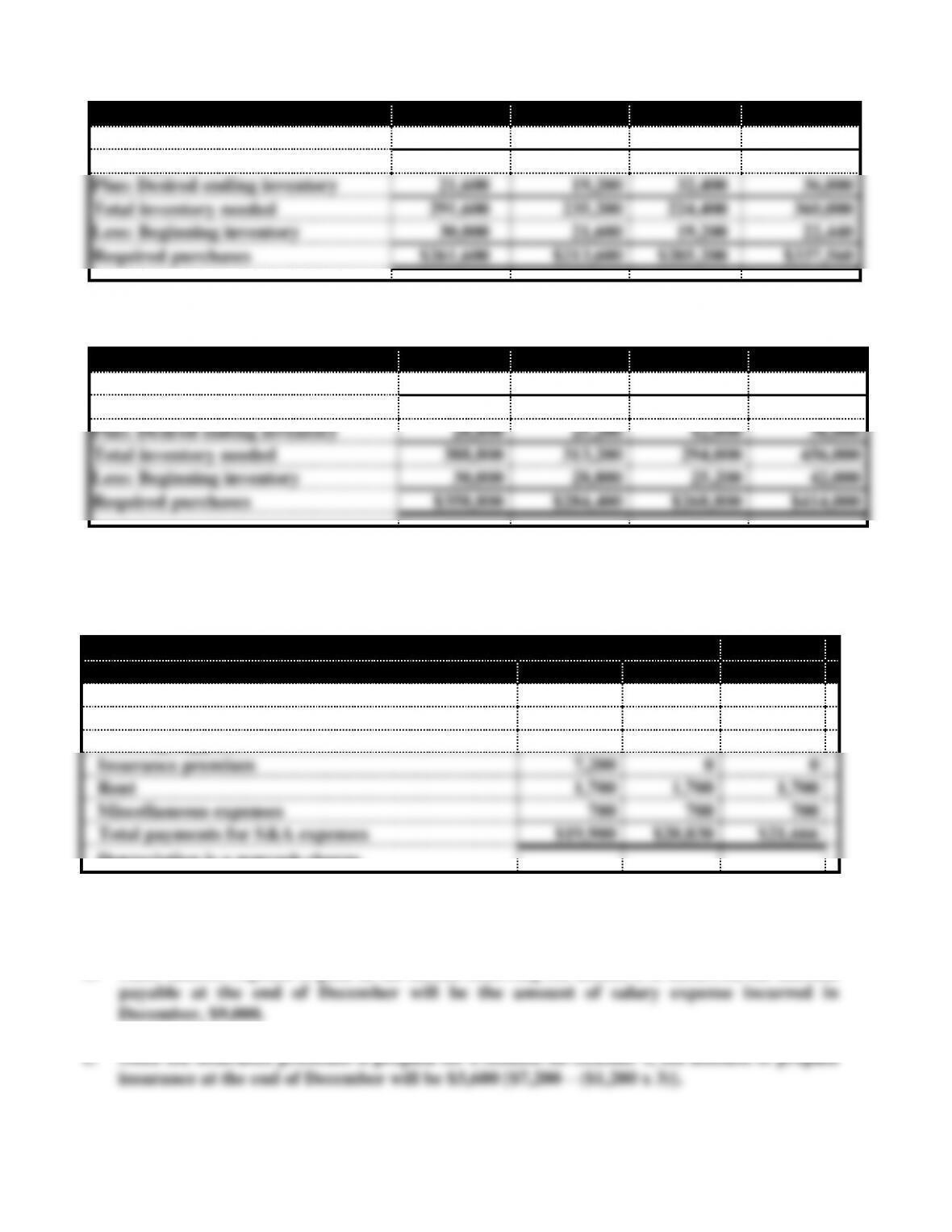

a. An inventory purchases budget prepared with the sales manager’s estimate:

Chapter 14 Planning for Profit and Cost Control

14-6

1st Quarter

2nd Quarter

3rd Quarter

4th Quarter

Sales

$450,000

$360,000

$320,000

$540,000

Cost of goods sold

$270,000

$216,000

$192,000

$324,000

Plus: Desired ending inventory

21,600

19,200

32,400

36,000

Total inventory needed

291,600

235,200

224,400

360,000

Less: Beginning inventory

30,000

21,600

19,200

22,440

Required purchases

$261,600

$213,600

$205,200

$337,560

b. An inventory purchases budget prepared with the marketing consultant’s estimate:

1st Quarter

2nd Quarter

3rd Quarter

4th Quarter

Sales

$600,000

$480,000

$420,000

$700,000

Cost of goods sold

$360,000

$288,000

$252,000

420,000

Plus: Desired ending inventory

28,800

25,200

42,000

36,000

Total inventory needed

388,800

313,200

294,000

456,000

Less: Beginning inventory

30,000

28,800

25,200

42,000

Required purchases

$358,800

$284,400

$268,800

$414,000

Exercise 14-11

a.

Schedule of Cash Payments for S&A Expenses

Oct.

Nov.

Dec.

Equipment lease expense

$7,500

$ 7,500

$ 7,500

Prior month’s salary expense, 100%

0

8,200

8,700

Cleaning supplies

2,800

2,730

3,066

Insurance premium

7,200

0

0

Rent

1,700

1,700

1,700

Miscellaneous expenses

700

700

700

Total payments for S&A expenses

$19,900

$20,830

$21,666

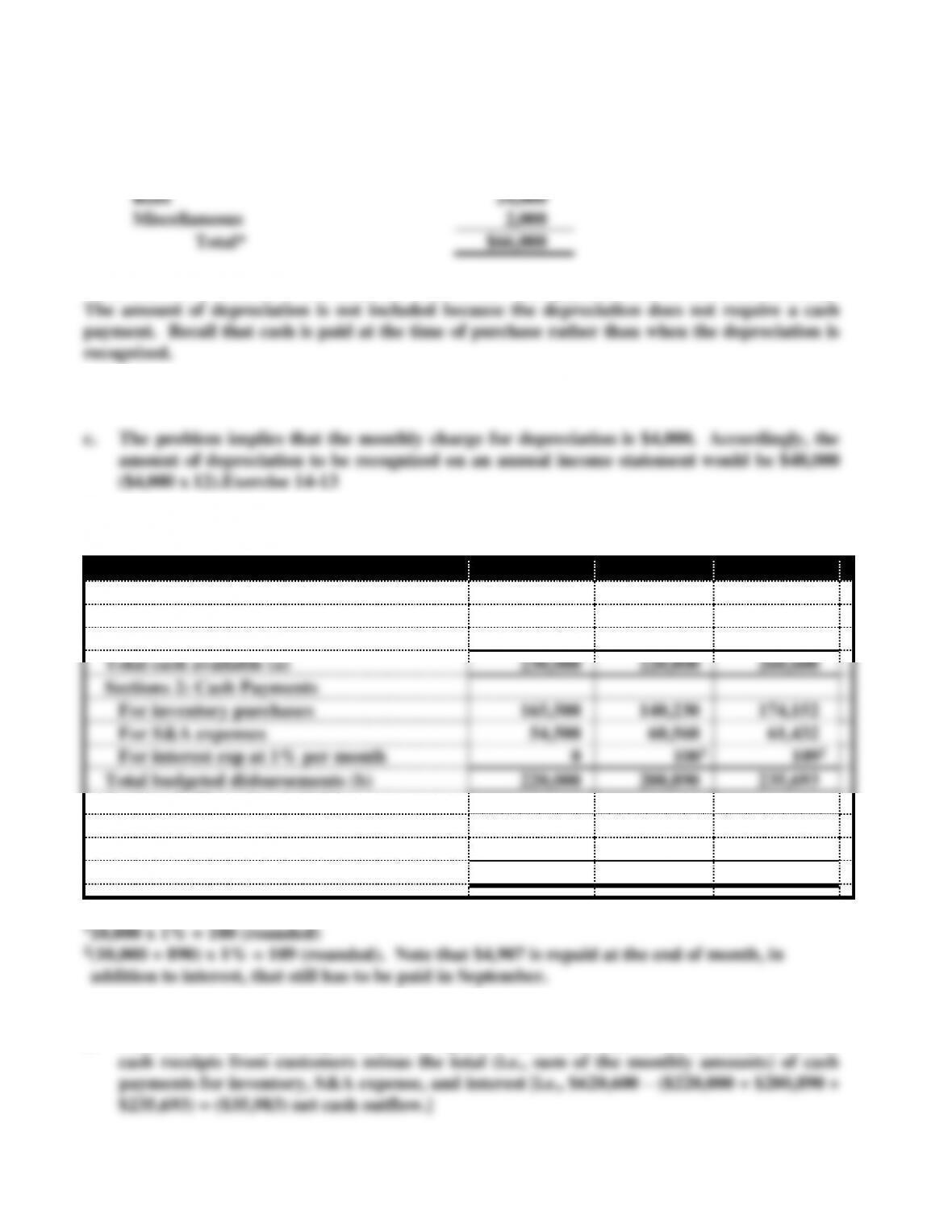

Depreciation is a noncash charge.

Exercise 14-11

b. Since salaries expense is paid in the month following the month it is incurred, the amount

Chapter 14 Planning for Profit and Cost Control

14-7

Exercise 14-12

a. Budgeted payments for January:

Sales commissions

$40,000

Rent

24,000

Miscellaneous

2,000

Total*

$66,000

*The amount of utilities is not included because the cash payment will be made in February.

b. The full $8,000 balance for the utilities charge will remain payable at the end of January.

a.

Cash Budget

July

August

September

Section 1: Cash receipts

Beginning cash balance

$ 50,000

$ 20,000

$ 20,000

Add cash receipts

180,000

200,000

240,600

Total cash available (a)

230,000

220,000

260,600

Sections 2: Cash Payments

For inventory purchases

165,500

140,230

174,152

For S&A expenses

54,500

60,560

61,432

For interest exp at 1% per month

0

1001

1092

Total budgeted disbursements (b)

220,000

200,890

235,693

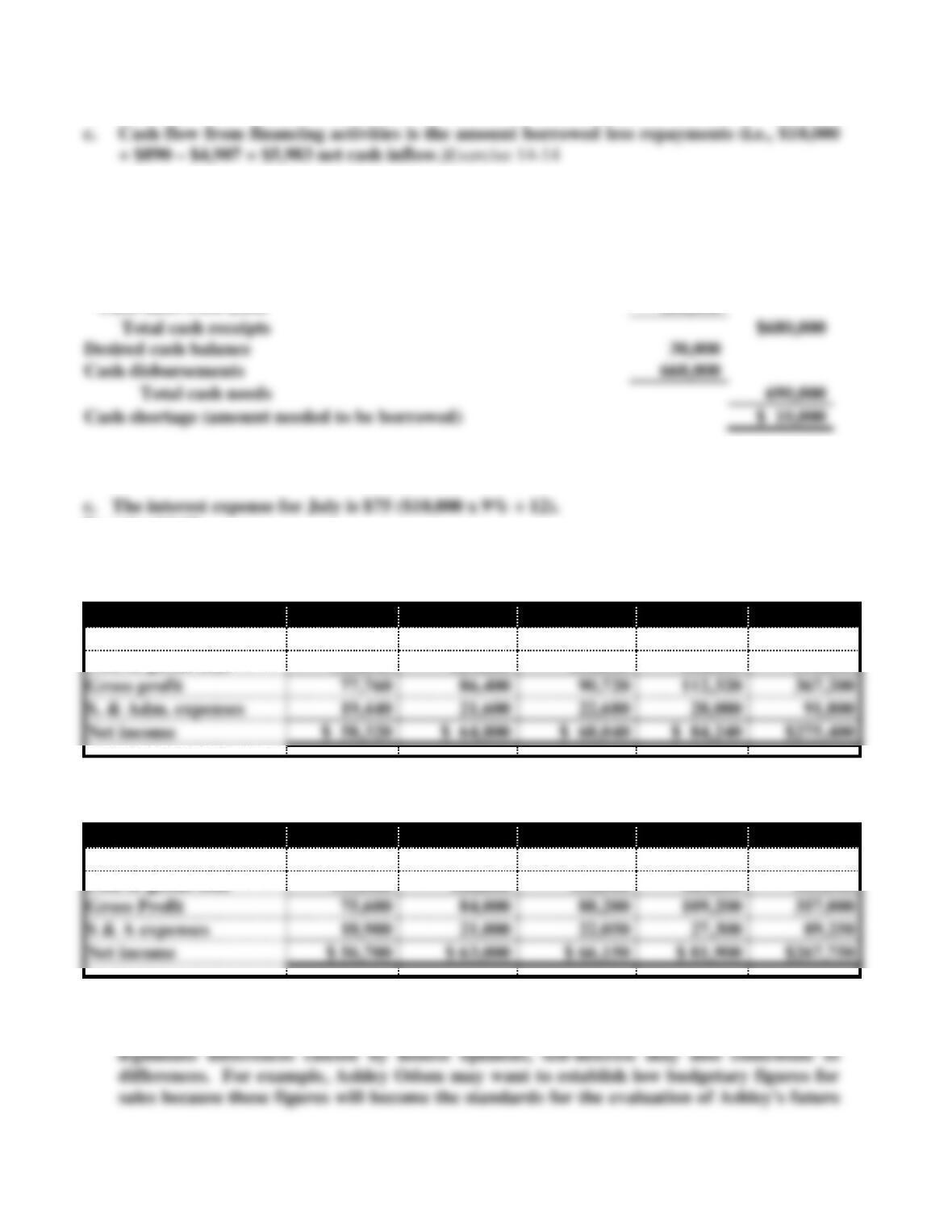

Sections 3: Financing Activities

Cash surplus (shortage) (a – b=c)

10,000

19,110

24,907

Borrowing (repayment) (d–c)

10,000

890

(4,907)

Ending cash balance (d)

$ 20,000

$ 20,000

$ 20,000

b. Cash flow from operating activities is equal to total (i.e., sum of the monthly amounts)

Chapter 14 Planning for Profit and Cost Control

14-8

a.

Cash Collections

Collections from May’s receivables balance

$ 80,000

Collections from June’s credit sales ($500,000 x .80)

400,000

Cash sales from June

200,000

Total cash receipts

$680,000

Desired cash balance

30,000

Cash disbursements

660,000

Total cash needs

690,000

Cash shortage (amount needed to be borrowed)

$ 10,000

b. The interest expense for June is $0 because the loan is taken at the end of June.

Exercise 14-15

a. Pro forma income statement prepared with Mr. Meier’s estimate:

1st Quarter

2nd Quarter

3rd Quarter

4th Quarter

Total

Sales revenue

$194,400

$216,000

$226,800

$280,800

$918,000

Cost of goods sold

116,640

129,600

136,080

168,480

550,800

Gross profit

77,760

86,400

90,720

112,320

367,200

S. & Adm. expenses

19,440

21,600

22,680

28,080

91,800

Net income

$ 58,320

$ 64,800

$ 68,040

$ 84,240

$275,400

b. Pro forma income statement prepared with Ms. Odom‘s estimate:

1st Quarter

2nd Quarter

3rd Quarter

4th Quarter

Total

Sales revenue

$189,000

$210,000

$220,500

$273,000

$892,500

Cost of goods sold

113,400

126,000

132,300

163,800

535,500

Gross Profit

75,600

84,000

88,200

109,200

357,000

S & A expenses

18,900

21,000

22,050

27,300

89,250

Net income

$ 56,700

$ 63,000

$ 66,150

$ 81,900

$267,750

c. Forecasting is not likely to be 100% accurate. Therefore, different executive officers

within the same company may have different estimates about the future. In addition to

Chapter 14 Planning for Profit and Cost Control

14-9

Problem 14-16

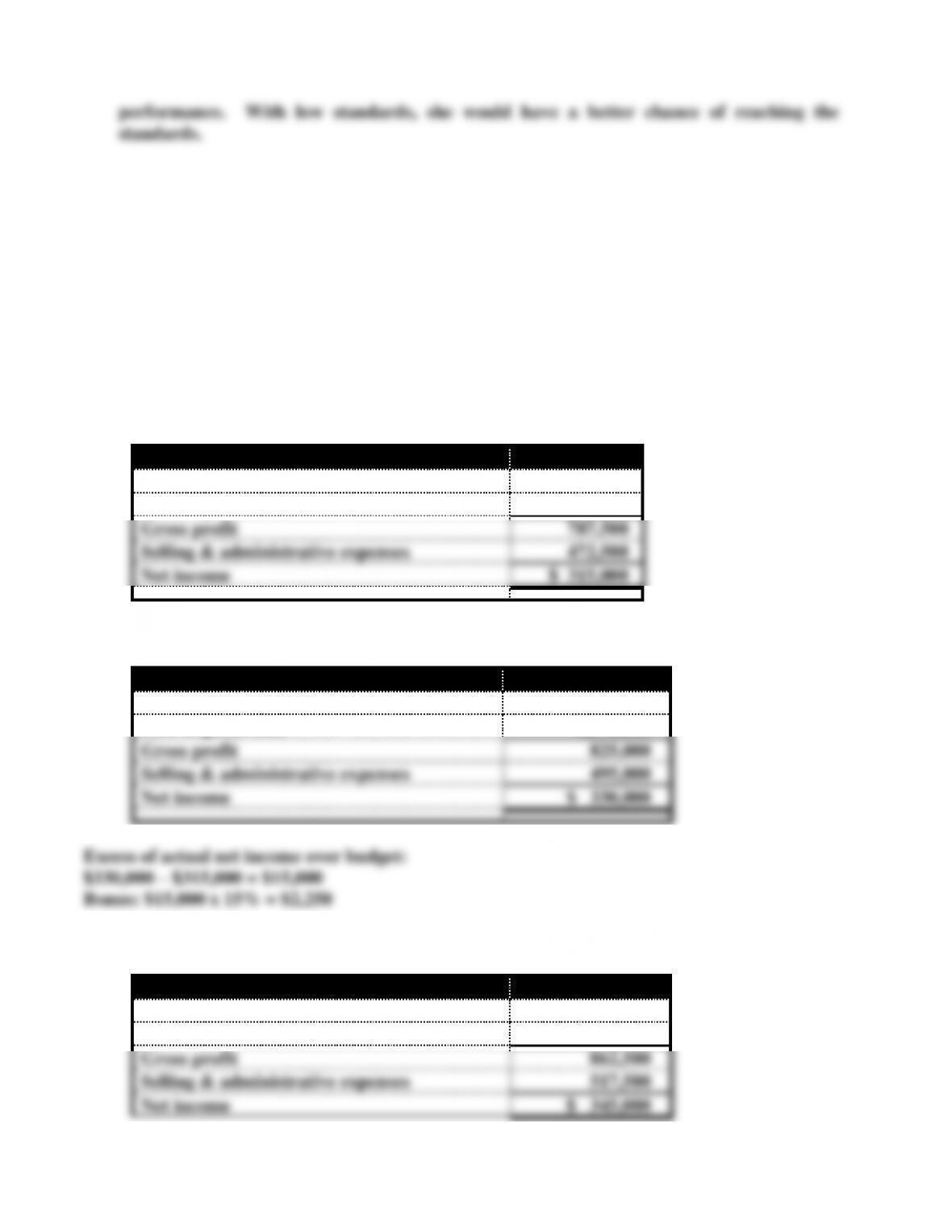

a. Pro forma income statement assuming 5% growth:

Budget

Sales revenue

$2,100,000

Cost of goods sold

1,312,500

Gross profit

787,500

Selling & administrative expenses

472,500

Net income

$ 315,000

b. Pro forma income statement with 10% growth:

Actual Result

Sales revenue

$2,200,000

Cost of goods sold

1,375,000

Gross profit

825,000

Selling & administrative expenses

495,000

Net income

$ 330,000

c. Pro forma income statement assuming 15% growth:

Budget

Sales revenue

$2,300,000

Cost of goods sold

1,437,500

Gross profit

862,500

Selling & administrative expenses

517,500

Net income

$ 345,000

Chapter 14 Planning for Profit and Cost Control

Problem 14-16 (continued)

e. The process of participative budgeting is recommended. This process requires two-way

communication between the president and divisional vice presidents. Any disagreement

about the budget assumptions should be fully discussed and pros and cons well considered.

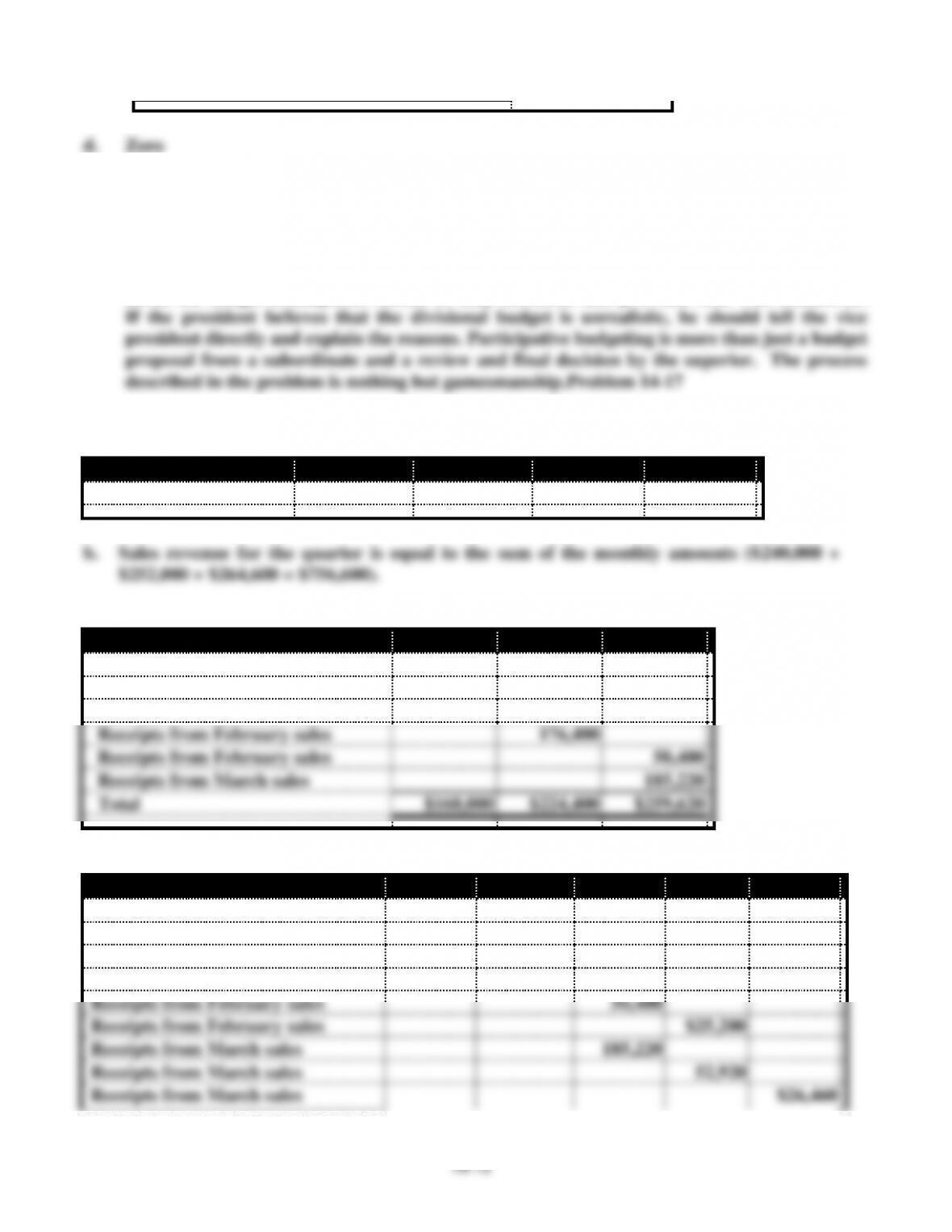

a.

Sales Budget

January

February

March

Total

Sales on account

$240,000

$252,000

$264,600

$756,600

c.

Schedule of Cash Receipts

January

February

March

Receipts from January sales

$168,000

Receipts from January sales

$ 48,000

Receipts from January sales

$ 24,000

Receipts from February sales

176,400

Receipts from February sales

50,400

Receipts from March sales

185,220

Total

$168,000

$224,400

$259,620

d.

Schedule of Cash Receipts

January

February

March

April

May

Receipts from January sales

$168,000

Receipts from January sales

$ 48,000

Receipts from January sales

$ 24,000

Receipts from February sales

176,400

Receipts from February sales

50,400

Receipts from February sales

$25,200

Receipts from March sales

185,220

Receipts from March sales

52,920

Receipts from March sales

$26,460

Chapter 14 Planning for Profit and Cost Control

14–11

Total

$168,000

$224,400

$259,620

$78,120

$26,460

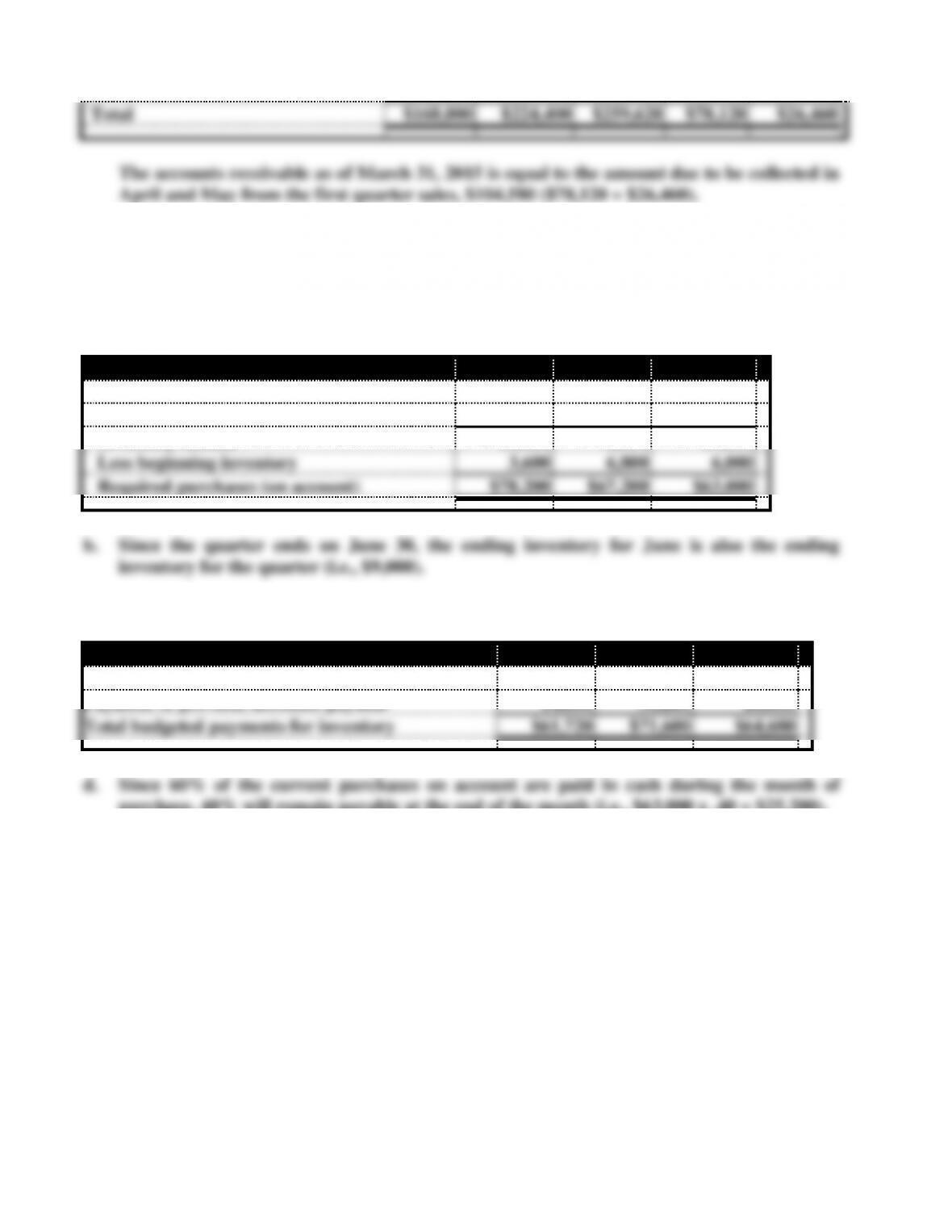

The accounts receivable as of March 31, 2015 is equal to the amount due to be collected in

April and May from the first quarter sales, $104,580 ($78,120 + $26,460).

Problem 14-18

a.

Inventory Purchases Budget

April

May

June

Budgeted cost of goods sold

$75,000

$68,000

$60,000

Plus desired ending inventory

6,800

6,000

9,000

Inventory needed

81,800

74,000

69,000

Less beginning inventory

3,600

6,800

6,000

Required purchases (on account)

$78,200

$67,200

$63,000

c.

Schedule of Cash Payments

April

May

June

Payment of current accounts payable

$46,920

$40,320

$37,800

Payment of previous accounts payable

14,800

31,280

26,880

Total budgeted payments for inventory

$61,720

$71,600

$64,680

purchase, 40% will remain payable at the end of the month (i.e., $63,000 x .40 = $25,200).

Problem 14-19