5-1

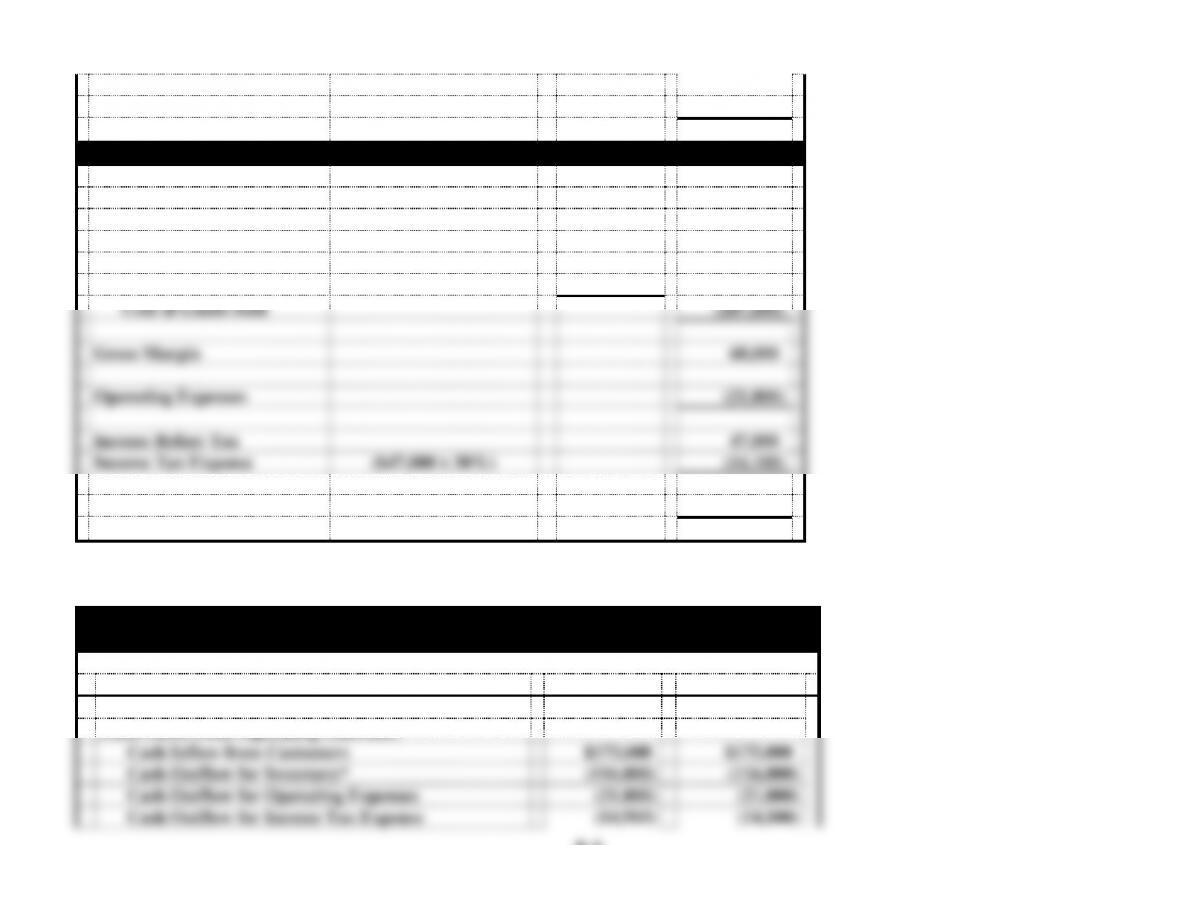

Net Income

$34,790

LIFO

Sales (3,500 @ $50)

$175,000

Cost of Goods Sold:

From 10/1 Purchase

1,000 units @ $32

=

$32,000

From 4/1 Purchase

2,500 units @ $30

=

75,000

Cost of Goods Sold

(107,000)

Gross Margin

68,000

Operating Expenses

(21,000)

Income Before Tax

47,000

Income Tax Expense

($47,000 x 30%)

(14,100)

Net Income

$32,900

EXERCISE 5-21 (cont.)

b. Income tax savings would be the difference between the tax using FIFO and the tax using LIFO, or $14,910 − $14,100 = $810.

c.

Windjammer Company

Cash Flows from Operating Activities

FIFO

LIFO

Cash Flows From Operating Activities:

Cash Inflow from Customers

$175,000

$175,000

Cash Outflow for Inventory*

(116,000)

(116,000)

Cash Outflow for Operating Expenses

(21,000)

(21,000)

Cash Outflow for Income Tax Expense

(14,910)

(14,100)

5-2

Net Cash Flow from Operating Activities

$23,090

$23,900

*Computation of cash paid for inventory:

4/1 Purchase 2,800 units @ $30 = $ 84,000

b. More income tax must be paid on the higher amount of income before tax reported under FIFO. Therefore, more cash used for

operating activities leaves less net cash flow from operating activities.

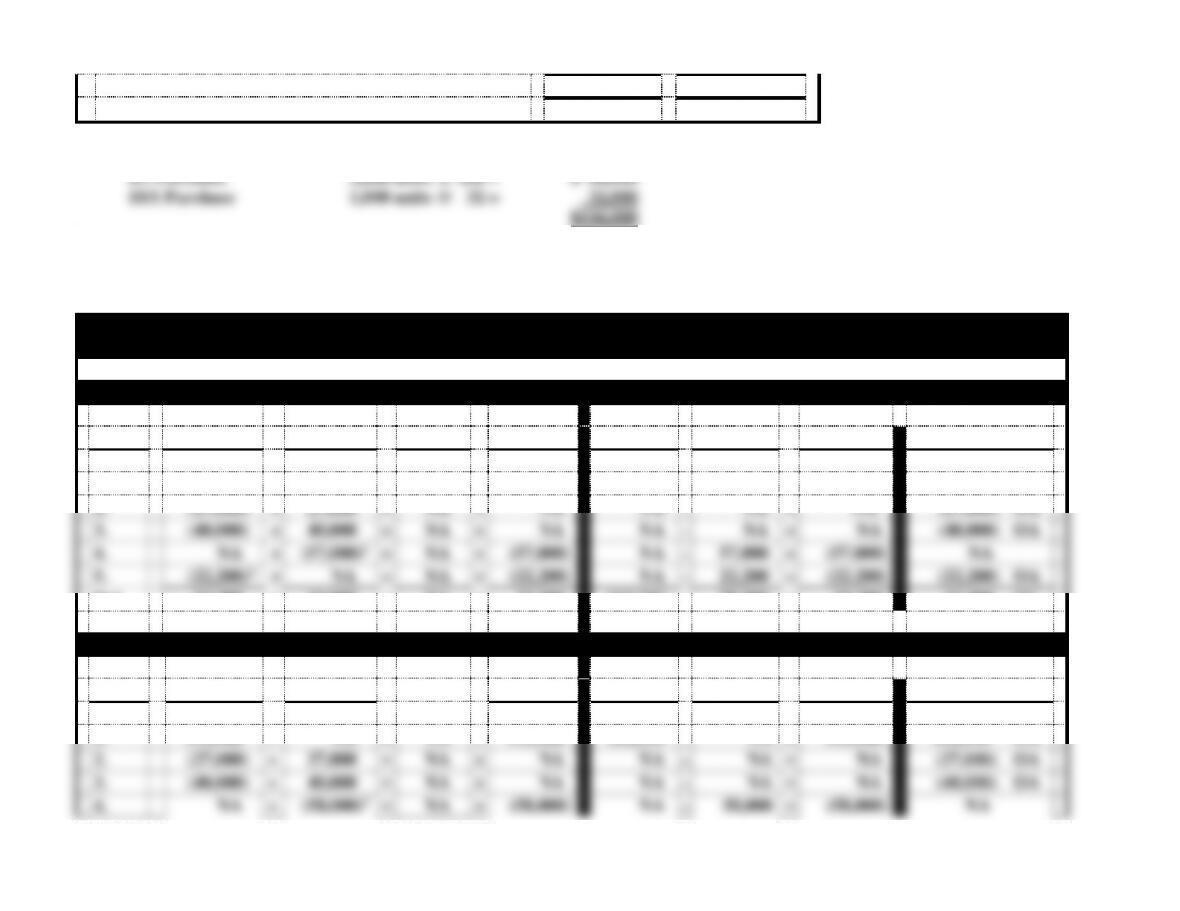

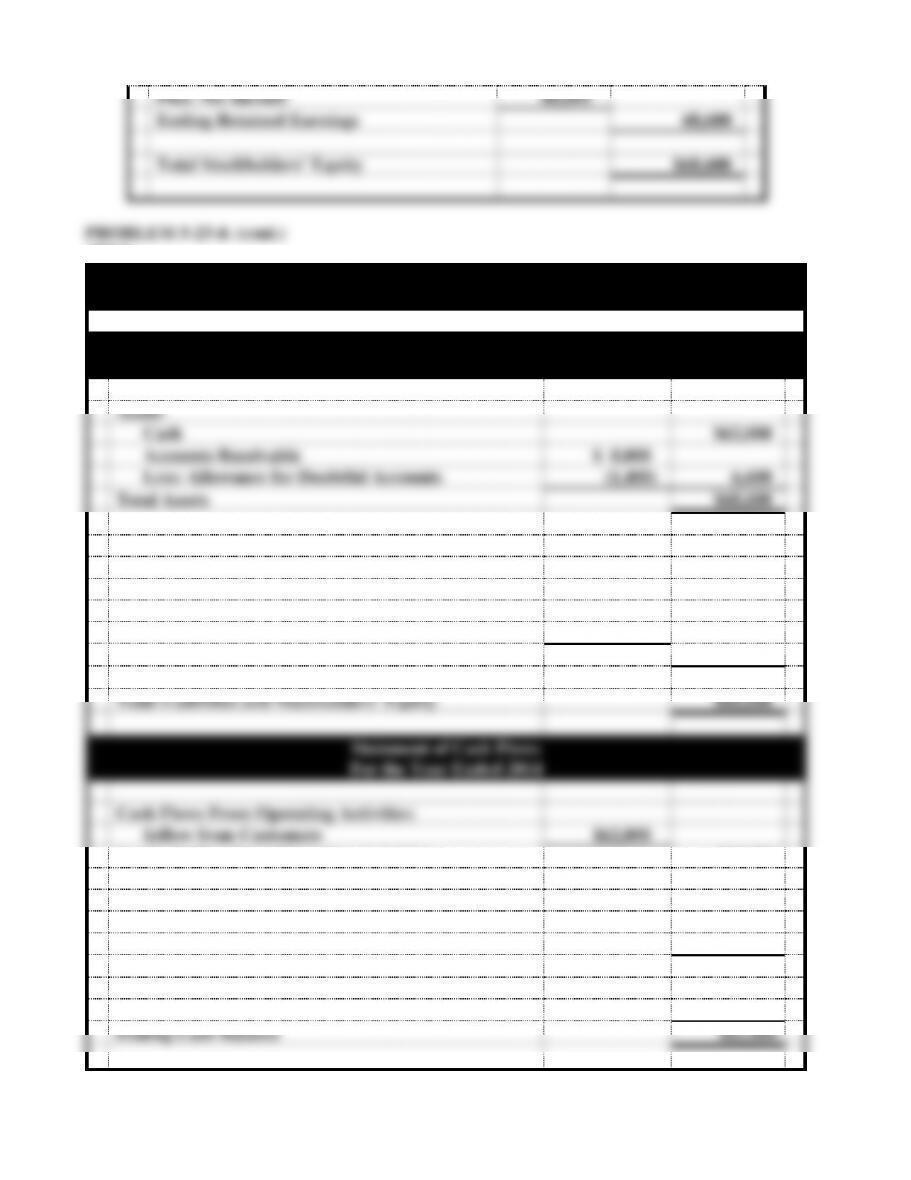

EXERCISE 5-22

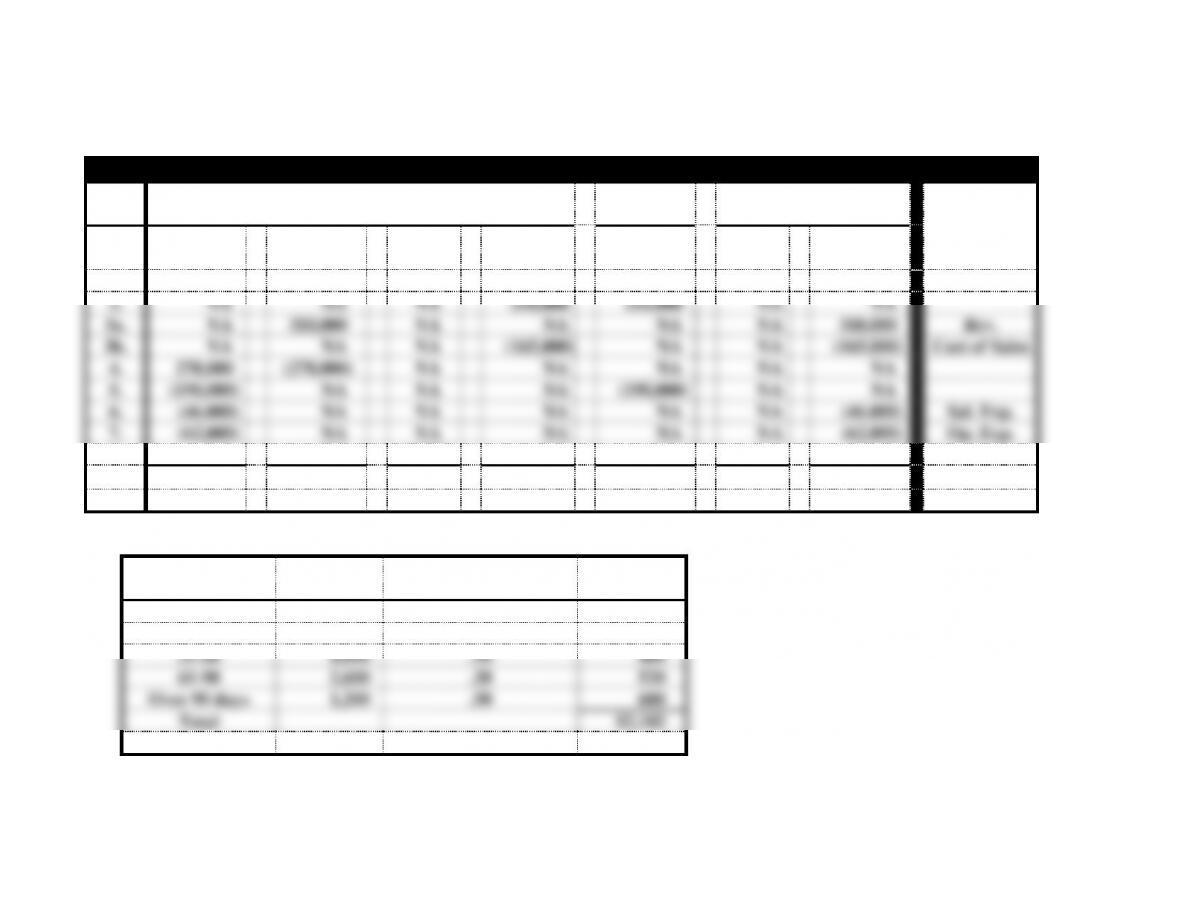

Garden Gifts, Inc.

Effect of Events on Financial Statements

Panel 1: FIFO Cost Flow

Event

Cash

+

Inv.

=

C. Stk.

+

Ret. Ear.

Rev.

−

Exp.

=

Net Inc.

Cash Flows

1.

112,500

+

NA

=

NA

+

112,500

112,500

−

NA

=

112,500

112,500 OA

2.

(27,000)

+

27,000

=

NA

+

NA

NA

−

NA

=

NA

(27,000) OA

3.

(40,000)

+

40,000

=

NA

+

NA

NA

−

NA

=

NA

(40,000) OA

4.

NA

+

(57,000)1

=

NA

+

(57,000)

NA

−

57,000

=

(57,000)

NA

5.

(22,200)2

+

NA

=

NA

+

(22,200)

NA

−

22,200

=

(22,200)

(22,200) OA

Bal.

23,300

+

10,000

=

NA

+

33,300

112,500

−

79,200

=

33,300

23,300 NC

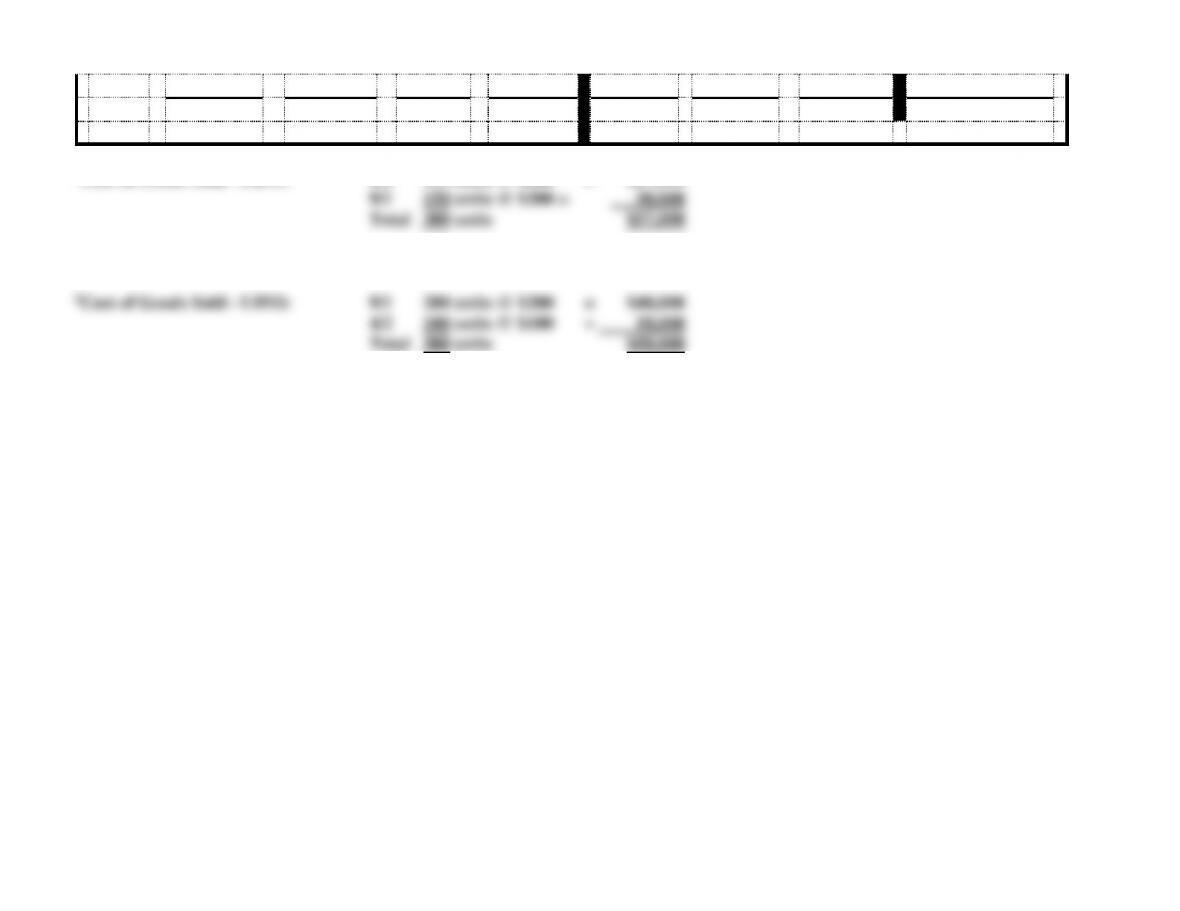

Panel 2: LIFO Cost Flow

Event

Cash

+

Inv.

=

C. Stk

+

Ret. Ear.

Rev.

−

Exp.

=

Net Inc.

Cash Flows

1.

112,500

+

NA

=

NA

+

112,500

112,500

−

NA

=

112,500

112,500 OA

2.

(27,000)

+

27,000

=

NA

+

NA

NA

−

NA

=

NA

(27,000) OA

3.

(40,000)

+

40,000

=

NA

+

NA

NA

−

NA

=

NA

(40,000) OA

4.

NA

+

(58,000)3

=

NA

+

(58,000)

NA

−

58,000

=

(58,000)

NA

5-3

5.

(21,800)4

+

NA

=

NA

+

(21,800)

NA

−

21,800

=

(21,800)

(21,800) OA

Bal.

23,700

+

9,000

=

NA

+

32,700

112,500

−

79,800

=

32,700

23,700 NC

1Cost of Goods Sold – FIFO: 4/2 150 units @ $180 = $27,000

2Income Tax Expense: ($112,500 − $57,000) x 40% = $22,200

4Income Tax Expense ($112,500 − $58,000) x 40% = $21,800

5-4

EXERCISE 5-22 (cont.)

b. Net Income assuming FIFO cost flow: $33,300 (see statements model above).

c. Net Income assuming LIFO cost flow: $32,700 (see statements model above).

d. LIFO produces a lower income tax by $400 ($22,200 − $21,800). This results because a

larger amount of inventory is expensed resulting in a lower income before tax. The last

purchase was bought at a higher price than the first purchase.

SOLUTIONS TO PROBLEMS – CHAPTER 5

PROBLEM 5-23

a.

Event Number

Type of Transaction

2014

1.

Asset Source

2.

Asset Exchange

3.

Asset Use

2015

1.

Asset Source

2.

Asset Exchange

3.

Asset Exchange

4a.*

Asset Exchange

4b.*

Asset Exchange

5.

Asset Use

6.

Asset Use

b. 2014 and 2015

Effect of Transactions on Financial Statements

No.

Assets

=

Liab.

+

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

2014

1.

+

NA

+

+

NA

+

NA

2.

+−

NA

NA

NA

NA

NA

+ OA

3.

−

NA

−

NA

+

−

NA

2015

1.

+

NA

+

+

NA

+

NA

5-5

2.

+−

NA

NA

NA

NA

NA

+ OA

3.

+−

NA

NA

NA

NA

NA

NA

4a.*

+−

NA

NA

NA

NA

NA

NA

4b.*

+−

NA

NA

NA

NA

NA

+ OA

5.

−

NA

−

NA

+

−

− OA

6.

−

NA

−

NA

+

−

NA

*4a. is reinstatement of the previously charged off receivable; 4b is the collection of the account.

PROBLEM 5-23 (cont.)

c. 2014

Expert Consulting Accounting Equation – 2014

Event

Assets

=

Liab.

+

Equity

Acct.

Title/RE

Cash

+

A. Rec.

−

Allow.

=

+

Ret. Earn.

1.

NA

70,000

NA

NA

70,000

Rev.

2.

62,000

(62,000)

NA

NA

NA

3.

NA

NA

1,400*

NA

(1,400)

Uncoll.

Exp

Bal.

62,000

+

8,000

−

1,400

=

-0-

+

68,600

*$70,000 x 2% = $1,400

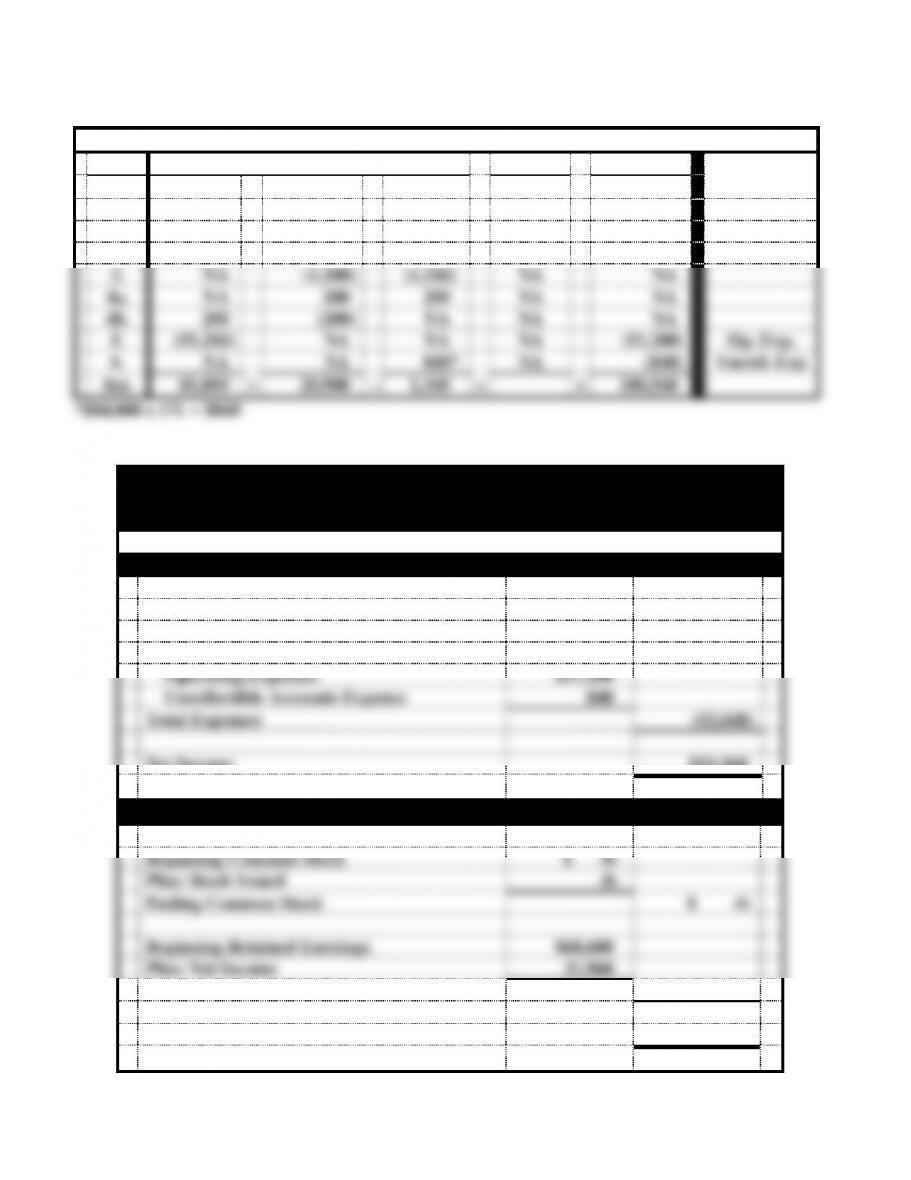

d. (2014)

Expert Consulting

Financial Statements

For the Year Ended 2014

Income Statement

Service Revenue

$70,000

Uncollectible Accounts Expense

(1,400)

Net Income

$68,600

Statement of Changes in Stockholders’ Equity

Beginning Common Stock

$ -0-

Plus: Stock Issued

-0-

Ending Common Stock

$ -0-

Beginning Retained Earnings

$ -0-

5-6

Plus: Net Income

68,600

Ending Retained Earnings

68,600

Total Stockholders’ Equity

$68,600

(2014)

Expert Consulting

Financial Statements

Balance Sheet

As of December 31, 2014

Assets

Cash

$62,000

Accounts Receivable

$ 8,000

Less: Allowance for Doubtful Accounts

(1,400)

6,600

Total Assets

$68,600

Liabilities

$ -0-

Stockholders’ Equity

Common Stock

$ -0-

Retained Earnings

68,600

Total Stockholders’ Equity

68,600

Total Liabilities and Stockholders’ Equity

$68,600

Statement of Cash Flows

For the Year Ended 2014

Cash Flows From Operating Activities:

Inflow from Customers

$62,000

Net Cash Flow from Operating Activities

$62,000

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities

-0-

Net Change in Cash

62,000

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$62,000

5-7

PROBLEM 5-23 (cont.)

c. 2015

Expert Consulting Accounting Equation – 2015

Event

Assets

=

Liab.

+

Equity

Acct./RE

Cash

+

A. Rec.

−

Allow.

=

+

Ret. Earn.

Bal.

62,000

8,000

1,400

-0-

68,600

1.

NA

84,000

NA

NA

84,000

Rev.

2.

70,000

(70,000)

NA

NA

NA

3.

NA

(1,100)

(1,100)

NA

NA

4a.

NA

200

200

NA

NA

4b.

200

(200)

NA

NA

NA

5.

(51,200)

NA

NA

NA

(51,200)

Op. Exp.

6.

NA

NA

840*

NA

(840)

Uncoll. Exp

Bal.

81,000

+

20,900

−

1,340

=

+

100,560

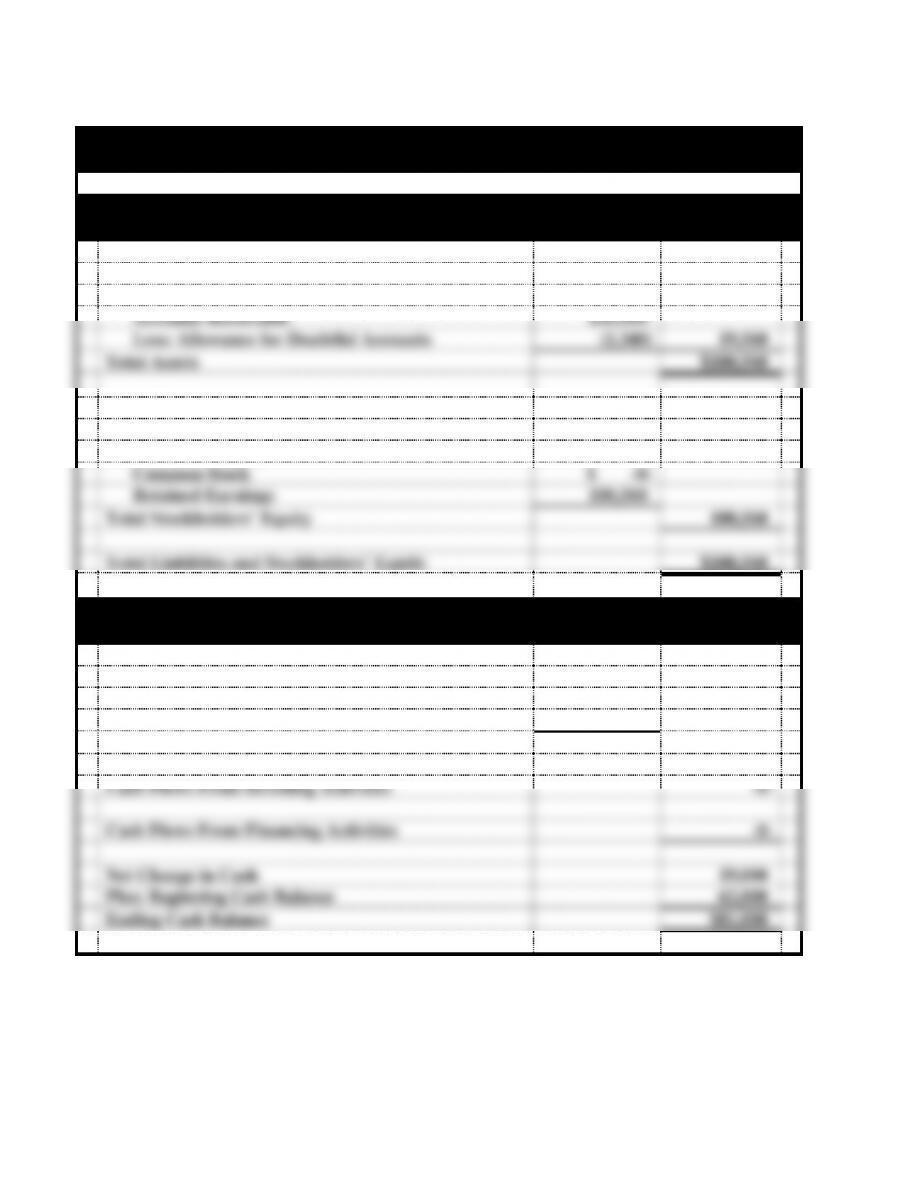

c. (2015)

Expert Consulting

Financial Statements

For the Year Ended 2015

Income Statement

Service Revenue

$84,000

Expenses

Operating Expenses

$51,200

Uncollectible Accounts Expense

840

Total Expenses

(52,040)

Net Income

$31,960

Statement of Changes in Stockholders’ Equity

Beginning Common Stock

$ -0-

Plus: Stock Issued

-0-

Ending Common Stock

$ -0-

Beginning Retained Earnings

$68,600

Plus: Net Income

31,960

Ending Retained Earnings

100,560

Total Stockholders’ Equity

$100,560

5-8

PROBLEM 5-23 d. (cont.)

(2014)

Expert Consulting

Financial Statements

Balance Sheet

As December 31, 2015

Assets

Cash

$ 81,000

Accounts Receivable

$20,900

Less: Allowance for Doubtful Accounts

(1,340)

19,560

Total Assets

$100,560

Liabilities

$ -0-

Stockholders’ Equity

Common Stock

$ -0-

Retained Earnings

100,560

Total Stockholders’ Equity

100,560

Total Liabilities and Stockholders’ Equity

$100,560

Statement of Cash Flows

For the Year Ended 2015

Cash Flows From Operating Activities:

Inflow from Customers

$70,200

Outflow for Expenses

(51,200)

Net Cash Flow from Operating Activities

$19,000

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities

-0-

Net Change in Cash

19,000

Plus: Beginning Cash Balance

62,000

Ending Cash Balance

$81,000

5-9

PROBLEM 5-24

a.

Accounts Receivable

Allowance for Doubtful Accounts

Beg. Bal. 96,200

Beg. Bal. 6,250

Sales on account. 726,000

Uncoll. Acct. expense 3,630

Collections on account (715,000)

Write off of bad accts (3,100)

Write off of bad accts (3,100)

Bal. 6,780

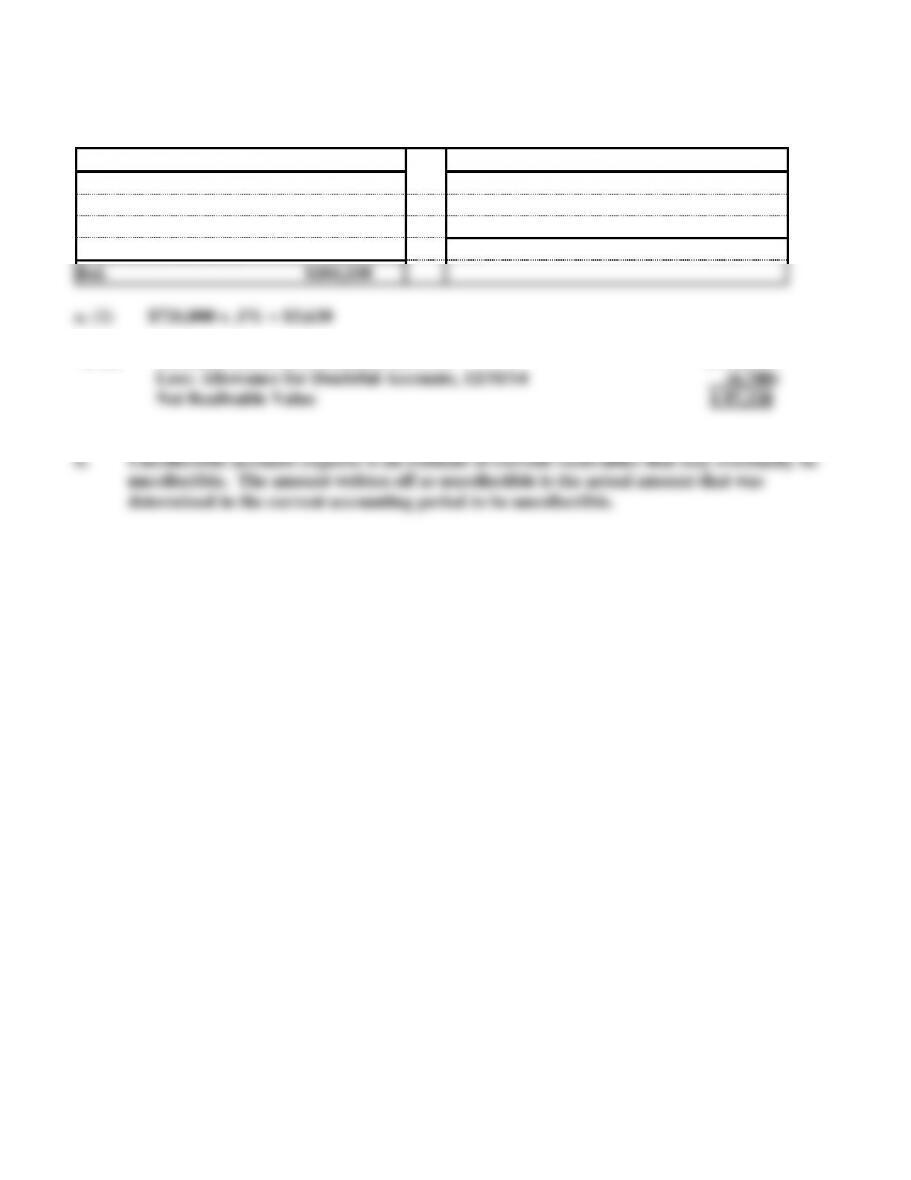

Bal. $104,100

a. (2) Accounts Receivable Balance, 12/31/14

$104,100

Less: Allowance for Doubtful Accounts, 12/31/14

(6,780)

Net Realizable Value

$ 97,320

5-10

PROBLEM 5-25

a.

Frankel Inc. Accounting Equation 2014

Assets

=

Liab.

+

Equity

Event

Cash

+

A. Rec.

−

Allow.

+

Mdse Inv.

=

Accts. Pay.

+

Com.

Stock

=

Ret. Earn.

Acct.

Title/RE

1.

60,000

NA

NA

NA

NA

60,000

NA

2.

NA

NA

NA

210,000

210,000

NA

NA

3a.

NA

310,000

NA

NA

NA

NA

310,000

Rev.

3b.

NA

NA

NA

(165,000)

NA

NA

(165,000)

Cost of Sales

4.

278,000

(278,000)

NA

NA

NA

NA

NA

5.

(190,000)

NA

NA

NA

(190,000)

NA

NA

6.

(46,000)

NA

NA

NA

NA

NA

(46,000)

Sal. Exp.

7.

(62,000)

NA

NA

NA

NA

NA

(62,000)

Op. Exp.

8.

NA

NA

2,102*

NA

NA

NA

(2,102)

Uncoll. Exp.

Bal.

40,000

+

32,000

−

2,102

+

45,000

=

20,000

+

60,000

+

34,898

*

Number of Days

Past Due

Amount

Percent Likely to Be

Uncollectible

Allowance

Balance

Current

$15,700

.01

$ 157

0-30

8,500

.05

425

31-60

4,000

.10

400

61-90

2,600

.20

520

Over 90 days

1,200

.50

600

Total

$2,102

5-11

PROBLEM 5-25 (cont.)

b.

Frankel Inc.

Financial Statements

For the Year Ended 2014

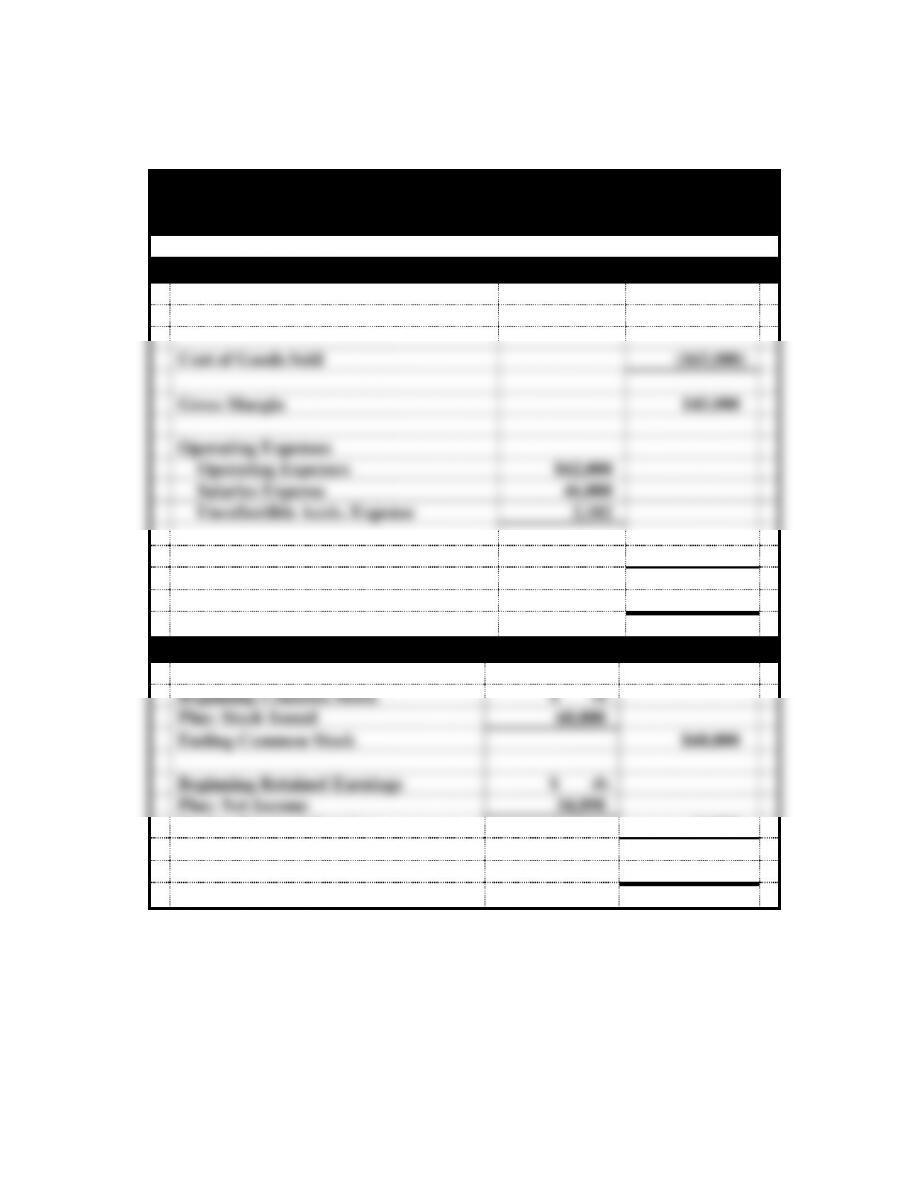

Income Statement

Sales Revenue

$310,000

Cost of Goods Sold

(165,000)

Gross Margin

145,000

Operating Expenses

Operating Expenses

$62,000

Salaries Expense

46,000

Uncollectible Accts. Expense

2,102

Total Operating Expenses

(110,102)

Net Income

$ 34,898

Statement of Changes in Stockholders’ Equity

Beginning Common Stock

$ -0-

Plus: Stock Issued

60,000

Ending Common Stock

$60,000

Beginning Retained Earnings

$ -0-

Plus: Net Income

34,898

Ending Retained Earnings

34,898

Total Stockholders’ Equity

$94,898