5-1

PROBLEM 5-30 b. (cont.)

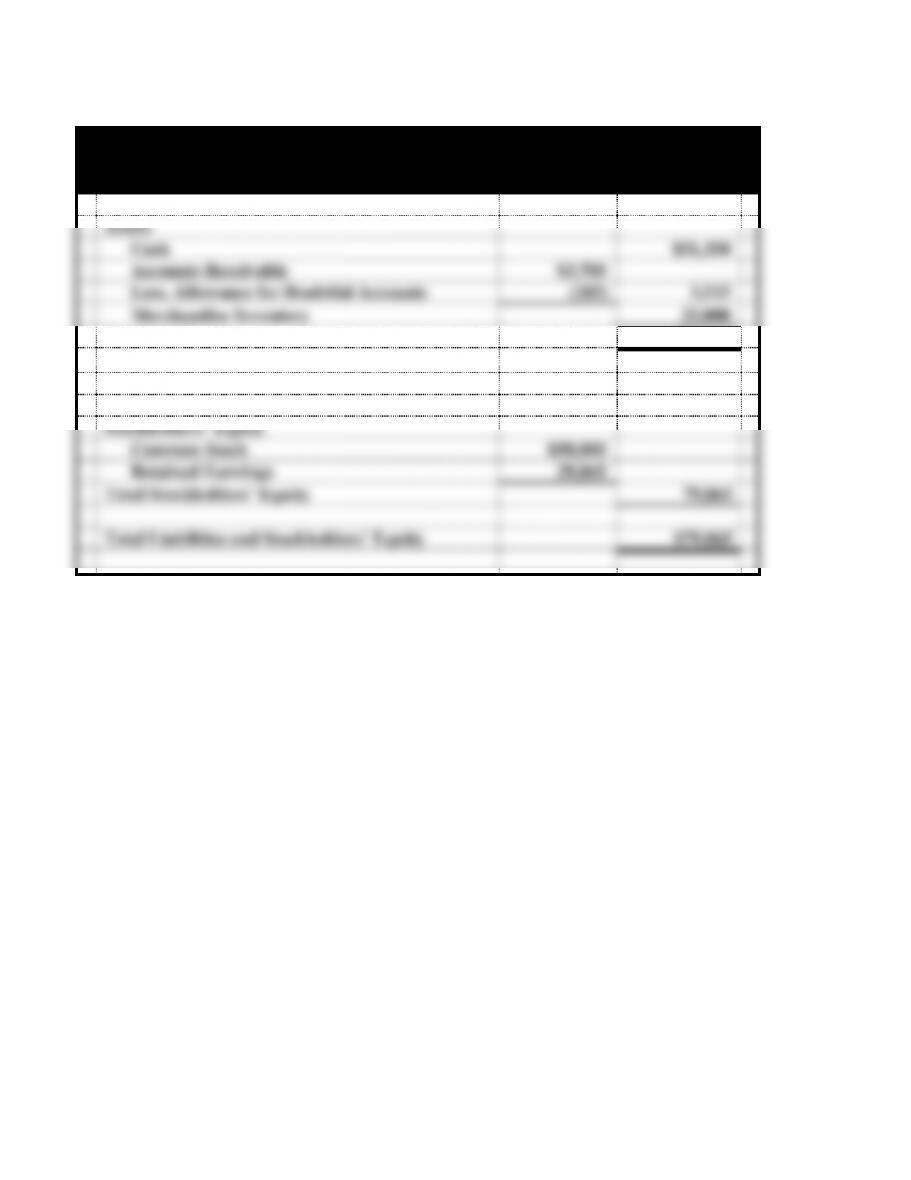

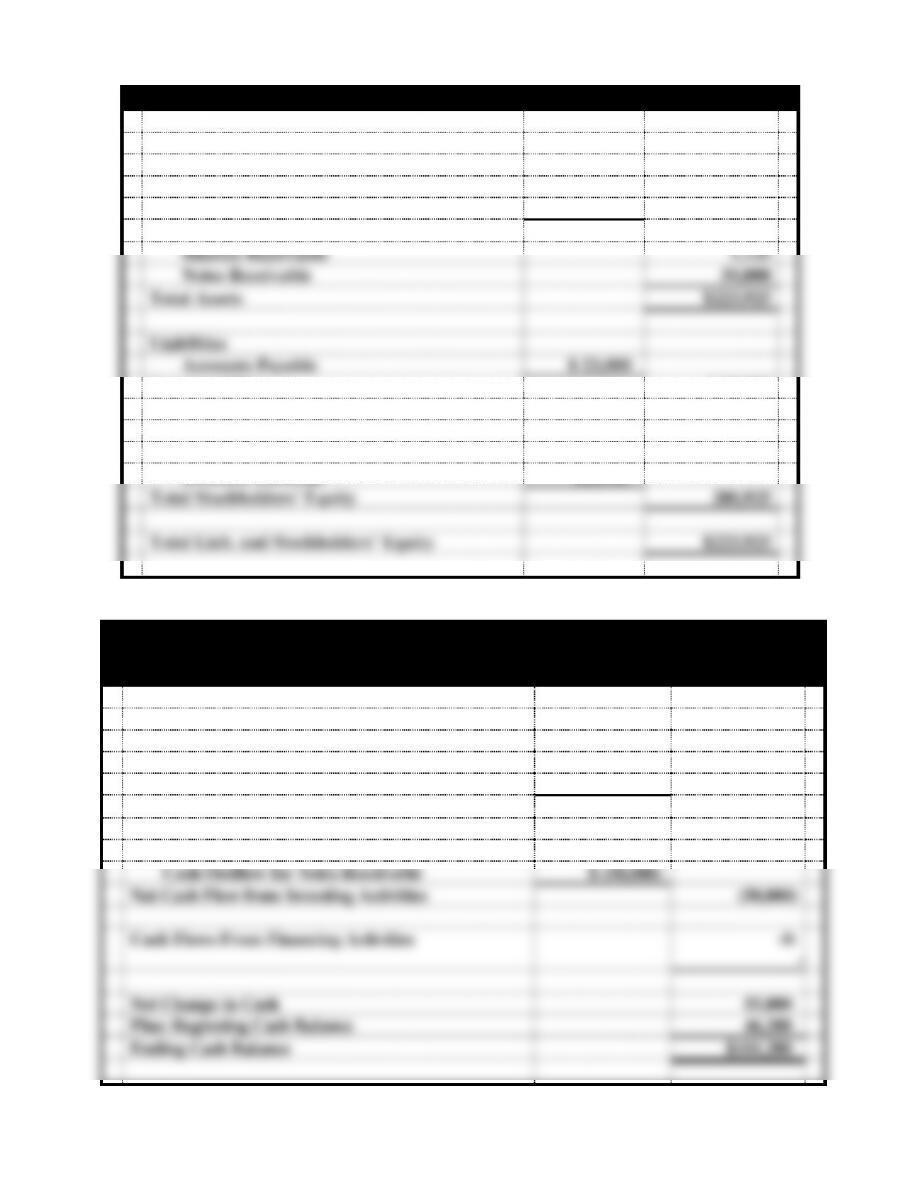

Iupe Supply Company

Balance Sheet

As of the End of the Year 2014

Assets

Cash

$51,350

Accounts Receivable

$3,700

Less, Allowance for Doubtful Accounts

(185)

3,515

Merchandise Inventory

25,000

Total Assets

$79,865

Liabilities

$ -0-

Stockholders’ Equity

Common Stock

$50,000

Retained Earnings

29,865

Total Stockholders’ Equity

79,865

Total Liabilities and Stockholders’ Equity

$79,865

5-2

PROBLEM 5-30 b. (cont.)

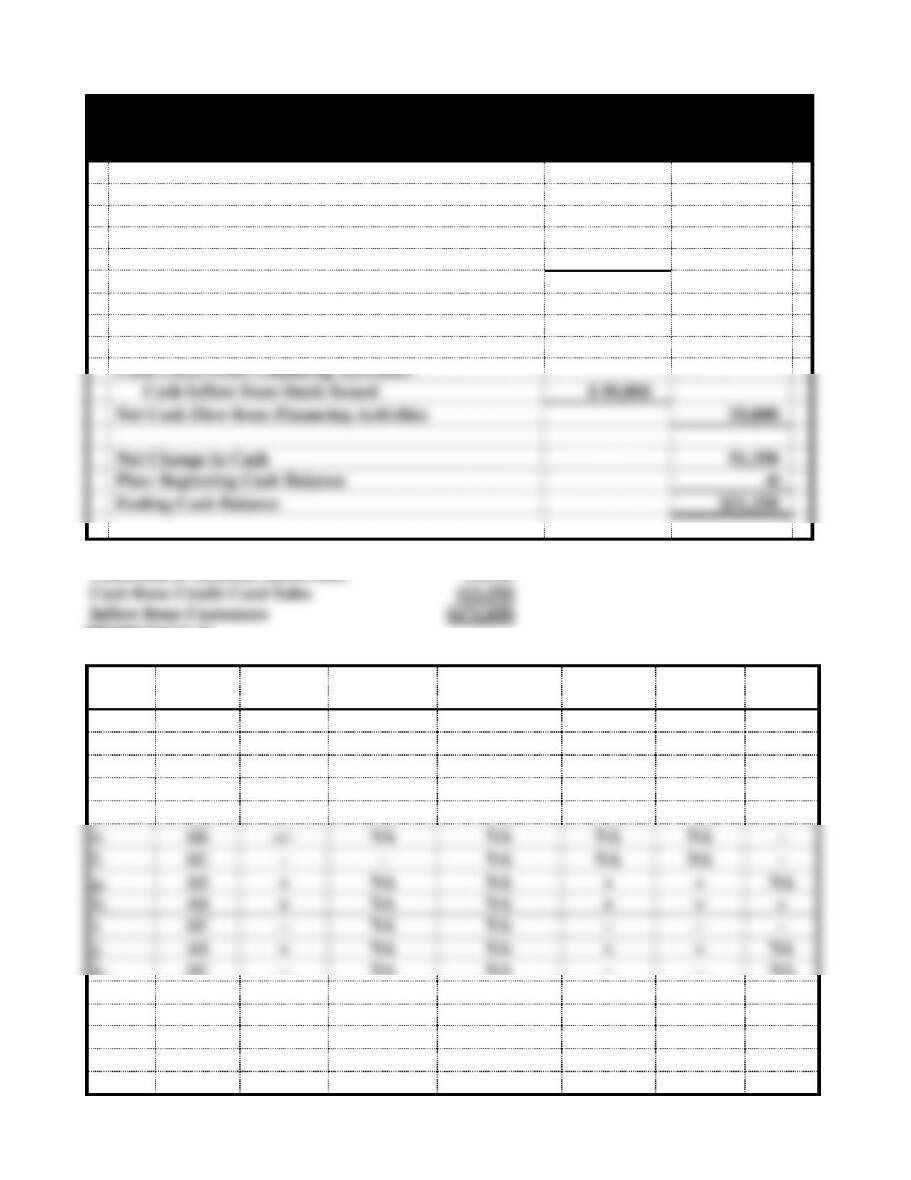

Iupe Supply Company

Statement of Cash Flows

For the Year Ended 2014

Cash Flows From Operating Activities:

Inflow from Customers1

$172,850

Outflow for Inventory

(120,000)

Outflow for Expenses

(51,500)

Net Cash Flow from Operating Activities

$ 1,350

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Cash Inflow from Stock Issued

$ 50,000

Net Cash Flow from Financing Activities

50,000

Net Change in Cash

51,350

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$51,350

1Cash Sales $50,000

Collection of Accounts Receivable 11,300

PROBLEM 5-31

Event

Type of

Event

Assets

Liabilities

Common

Stock

Retained

Earnings

Net

Income

Cash

Flow

a1.*

AS

+

NA

NA

+

+

NA

a2.*

AU

−

NA

NA

−

−

NA

b.

AE

+−

NA

NA

NA

NA

+

c.

AU

−

−

NA

NA

NA

−

d.

AE

+−

NA

NA

NA

NA

+

e.

AE

+/−

NA

NA

NA

NA

−

f.

AU

−

−

NA

NA

NA

−

g.

AS

+

NA

NA

+

+

NA

h.

AS

+

NA

NA

+

+

+

i.

AU

−

NA

NA

−

−

−

j.

AS

+

NA

NA

+

+

NA

k.

AU

−

NA

NA

−

−

NA

l.

AE

+−

NA

NA

NA

NA

+

m.

AS

+

NA

NA

+

+

+

n.

AE

+−

NA

NA

NA

NA

−

o.

AU

−

NA

NA

−

−

−

5-3

PROBLEM 5-32

a.

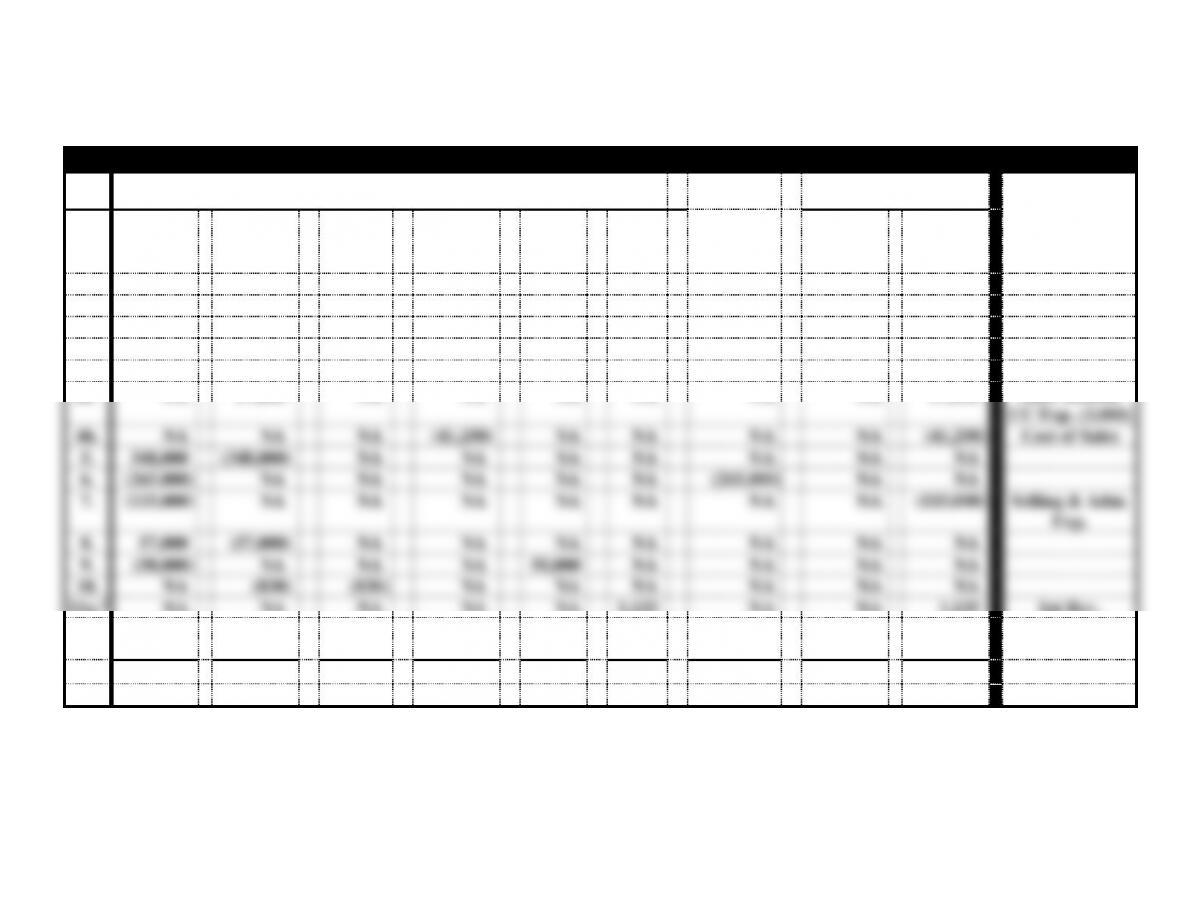

Village Cycle Sales and Service – 2014

Assets

=

Liabilities

+

Equity

Acct. Title/RE

Even

t

Cash

+

A. Rec.

−

Allow.

+

Mdse Inv.

+

Notes

Rec.

+

Int.

Rec

=

Accts.

Pay.

+

Com. Stock

=

Ret. Earn.

Bal.

46,200

21,300

1,350

85,600

NA

NA

28,000

80,000

43,750

1.

NA

NA

NA

260,000

NA

NA

260,000

NA

NA

2a.

NA

340,000

NA

NA

NA

NA

NA

NA

340,000

Sales Rev.

2b.

NA

NA

NA

(243,000)

NA

NA

NA

NA

(243,000)

Cost of Sales

3a.

80,000

NA

NA

NA

NA

NA

NA

NA

80,000

Service Rev.

4a.1

NA

57,000

NA

NA

NA

NA

NA

NA

57,000

Sales $60,000

CC Exp. (3,000)

4b.

NA

NA

NA

(41,250)

NA

NA

NA

NA

(41,250)

Cost of Sales

5.

348,000

(348,000)

NA

NA

NA

NA

NA

NA

NA

6.

(265,000)

NA

NA

NA

NA

NA

(265,000)

NA

NA

7.

(115,000)

NA

NA

NA

NA

NA

NA

NA

(115,000)

Selling & Adm.

Exp.

8.

57,000

(57,000)

NA

NA

NA

NA

NA

NA

NA

9.

(50,000)

NA

NA

NA

50,000

NA

NA

NA

NA

10.

NA

(830)

(830)

NA

NA

NA

NA

NA

NA

11a.2

NA

NA

NA

NA

NA

1,125

NA

NA

1,125

Int Rev.

11b.3

NA

NA

1,700

NA

NA

NA

NA

NA

(1,700)

Uncoll. Accts.

Exp.

Bal.

101,200

+

12,470

−

2,220

+

61,350

+

50,000

+

1,125

=

23,000

+

80,000

+

120,925

1$60,000 x 5% = $3,000; $60,000 − $3,000 = $57,000

2$50,000 x 9% = $4,500; $4,500 x 3/12 = $1,125

3$340,000 x .5% = $1,700

5-4

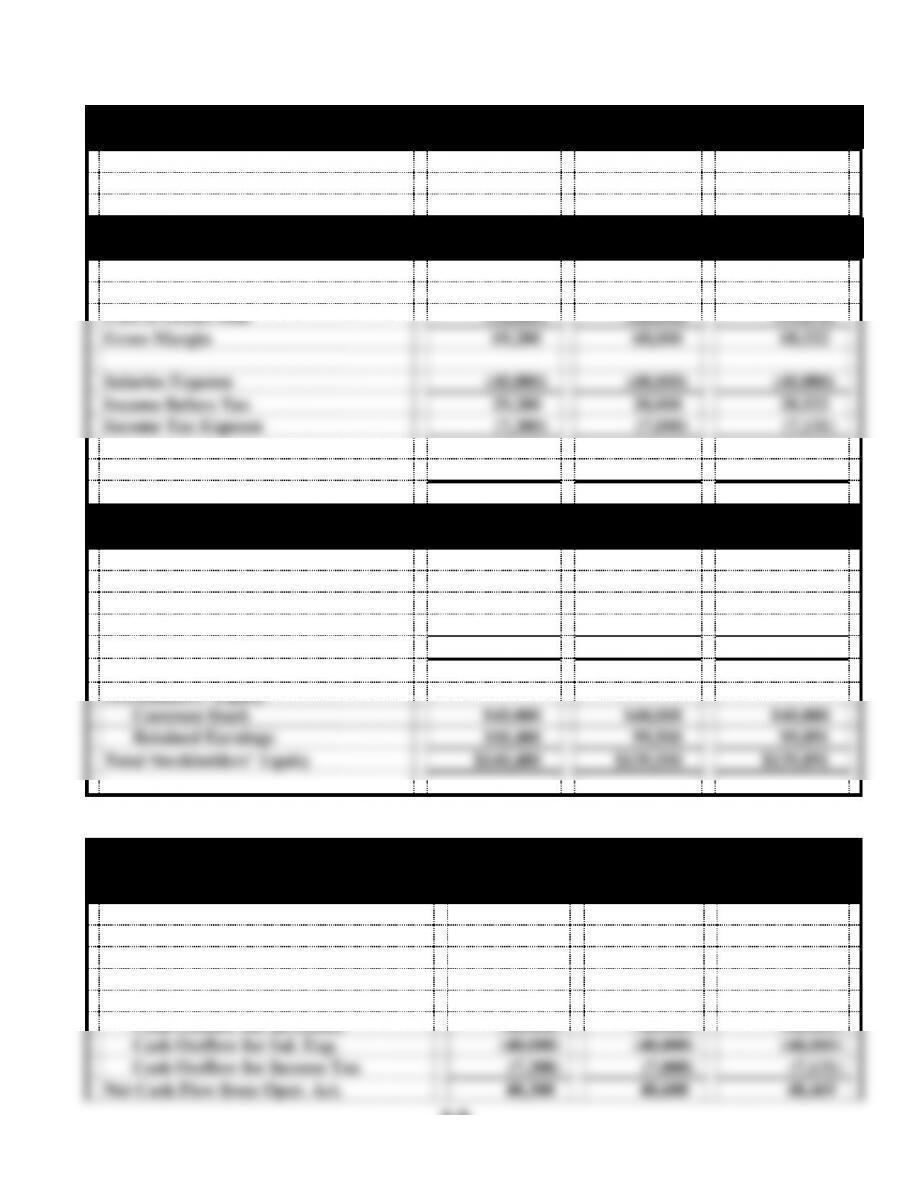

PROBLEM 5-32 (cont.)

Village Cycle Sales and Service

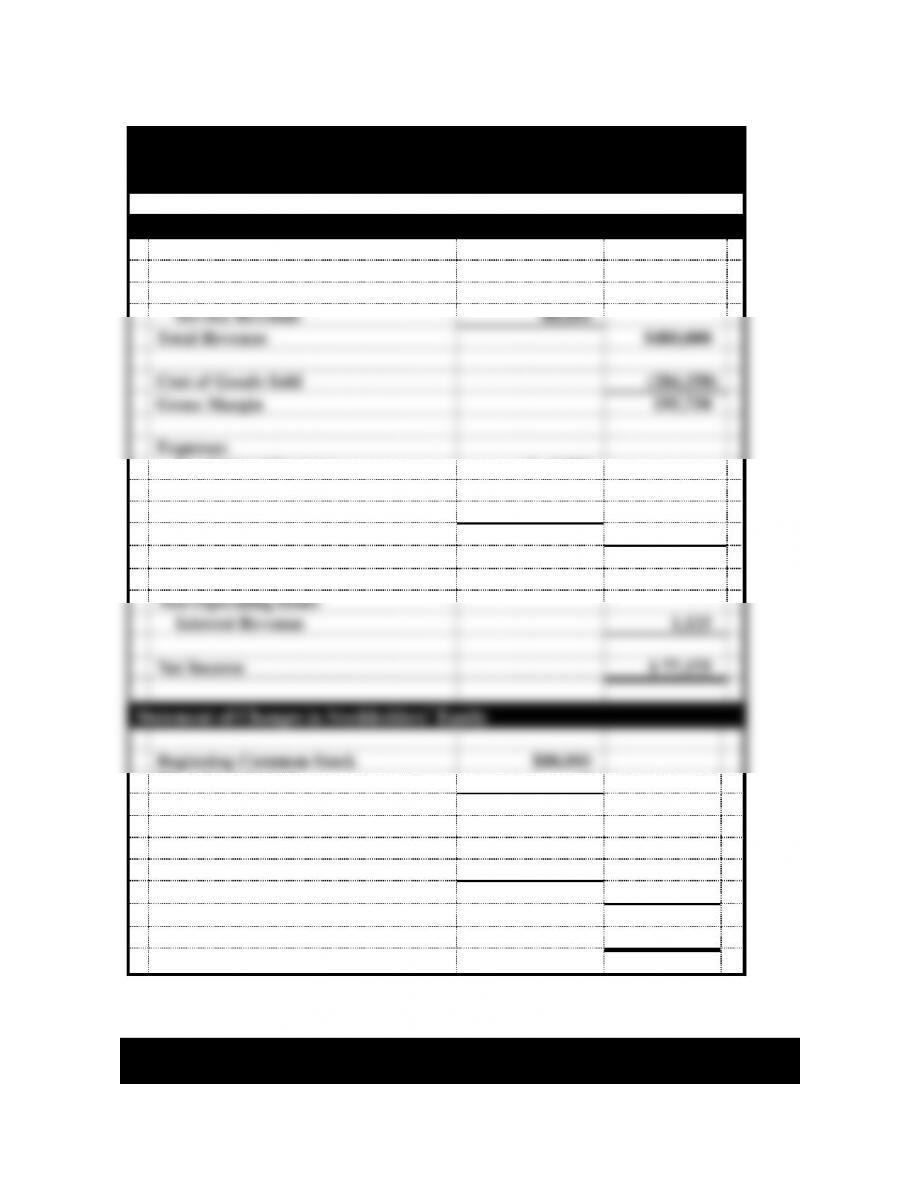

Financial Statements

For the Year Ended December 31, 2014

Income Statement

Revenue

Sales Revenue

$400,000

Service Revenue

80,000

Total Revenue

$480,000

Cost of Goods Sold

(284,250)

Gross Margin

195,750

Expenses

Credit Card Expense

$ 3,000

Selling & Adm. Expenses

115,000

Uncollectible Accts. Exp.

1,700

Total Operating Expenses

(119,700)

Operating Income

76,050

Non-Operating Items

Interest Revenue

1,125

Net Income

$ 77,175

Statement of Changes in Stockholders’ Equity

Beginning Common Stock

$80,000

Plus: Stock Issued

-0-

Ending Common Stock

$ 80,000

Beginning Retained Earnings

$43,750

Plus: Net Income

77,175

Ending Retained Earnings

120,925

Total Stockholders’ Equity

$200,925

PROBLEM 5-32 (cont.)

Village Cycle Sales and Service

Balance Sheet

5-5

As of December 31, 2014

Assets

Cash

$101,200

Accounts Receivable

$12,470

Less: Allow. for Doubtful Accts.

(2,220)

10,250

Merchandise Inventory

61,350

Interest Receivable

1,125

Notes Receivable

50,000

Total Assets

$223,925

Liabilities

Accounts Payable

$ 23,000

Total Liabilities

$ 23,000

Stockholders’ Equity

Common Stock

$ 80,000

Retained Earnings

120,925

Total Stockholders’ Equity

200,925

Total Liab. and Stockholders’ Equity

$223,925

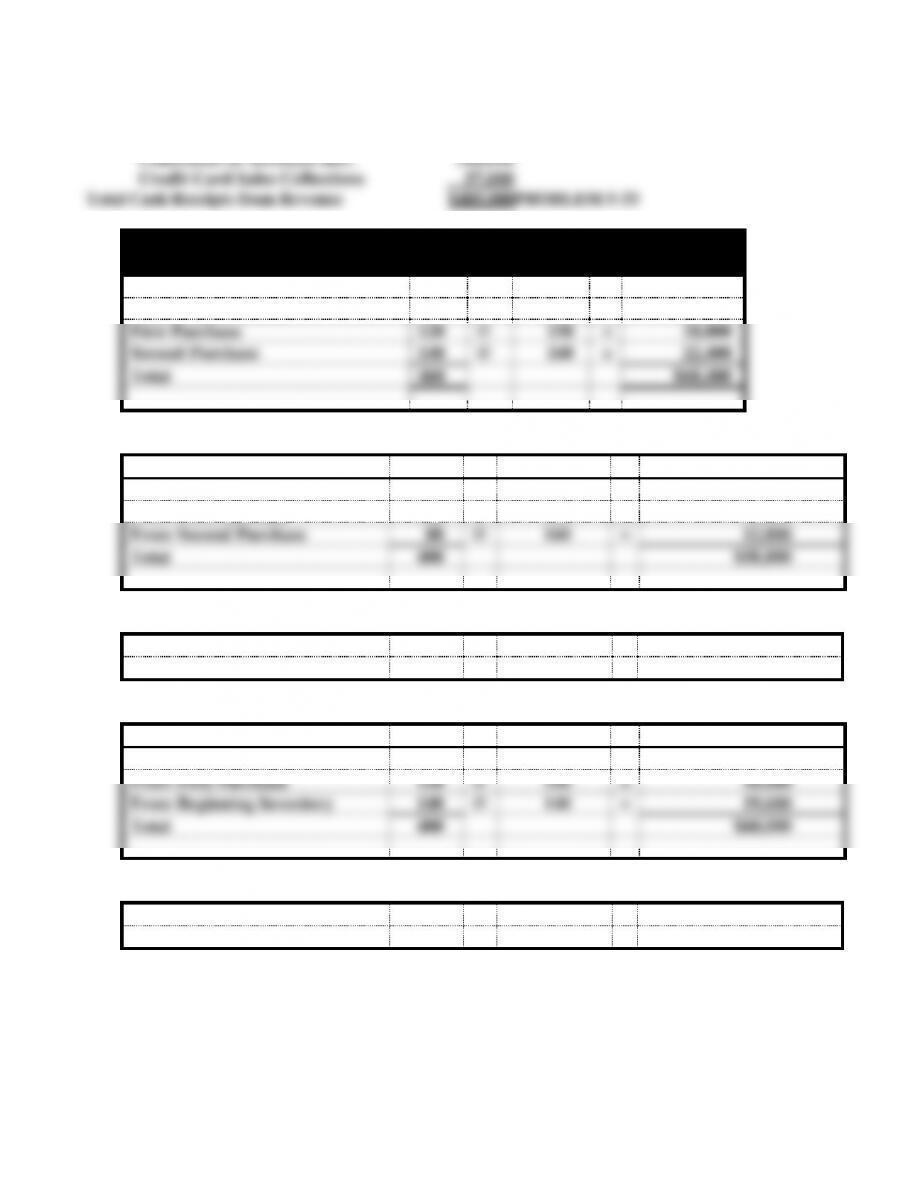

PROBLEM 5-32 (cont.)

Village Cycle Sales and Service

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash Flows From Operating Activities:

Cash Receipts from Revenue*

$485,000

Cash Payment for Accounts Pay. (Inv.)

(265,000)

Cash Payments for Expenses

(115,000)

Net Cash Flow from Operating Activities

$105,000

Cash Flows From Investing Activities:

Cash Outflow for Notes Receivable

$ (50,000)

Net Cash Flow from Investing Activities

(50,000)

Cash Flows From Financing Activities

-0–

-0–

Net Change in Cash

55,000

Plus: Beginning Cash Balance

46,200

Ending Cash Balance

$101,200

5-6

*Cash Receipts from Revenue:

Cash Sales $ 80,000

Carrol’s Lamp Shop

Inventory Purchases

Beginning Inventory

200

@

$140

=

$28,000

First Purchase

120

@

150

=

18,000

Second Purchase

140

@

160

=

22,400

Total

460

$68,400

a. (1) Cost of Goods Sold:

FIFO

Units

Unit Cost

Cost of Goods Sold

From Beginning Inventory

200

@

$140

=

$ 28,000

From First Purchase

120

@

150

=

18,000

From Second Purchase

80

@

160

=

12,800

Total

400

$58,800

Ending Inventory:

FIFO

Units

Unit Cost

Ending Inventory

From Second Purchase

60

@

$160

=

$9,600

a. (2) Cost of Goods Sold:

LIFO

Units

Unit Cost

Cost of Goods Sold

From Second Purchase

140

@

$160

=

$22,400

From First Purchase

120

@

150

=

18,000

From Beginning Inventory

140

@

140

=

19,600

Total

400

$60,000

Ending Inventory:

LIFO

Units

Unit Cost

Ending Inventory

From Beginning Inventory

60

@

$140

=

$8,400

5-7

PROBLEM 5-33 a. (cont.)

a. (3)

Weighted Average

Total Cost

Total Units

=

Cost per Unit

$68,400

460

=

$148.696

Cost of Goods Sold:

400 units

@

$148.696

=

$59,478*

Ending Inventory:

60 units

@

$148.696

=

$ 8,922*

*rounded

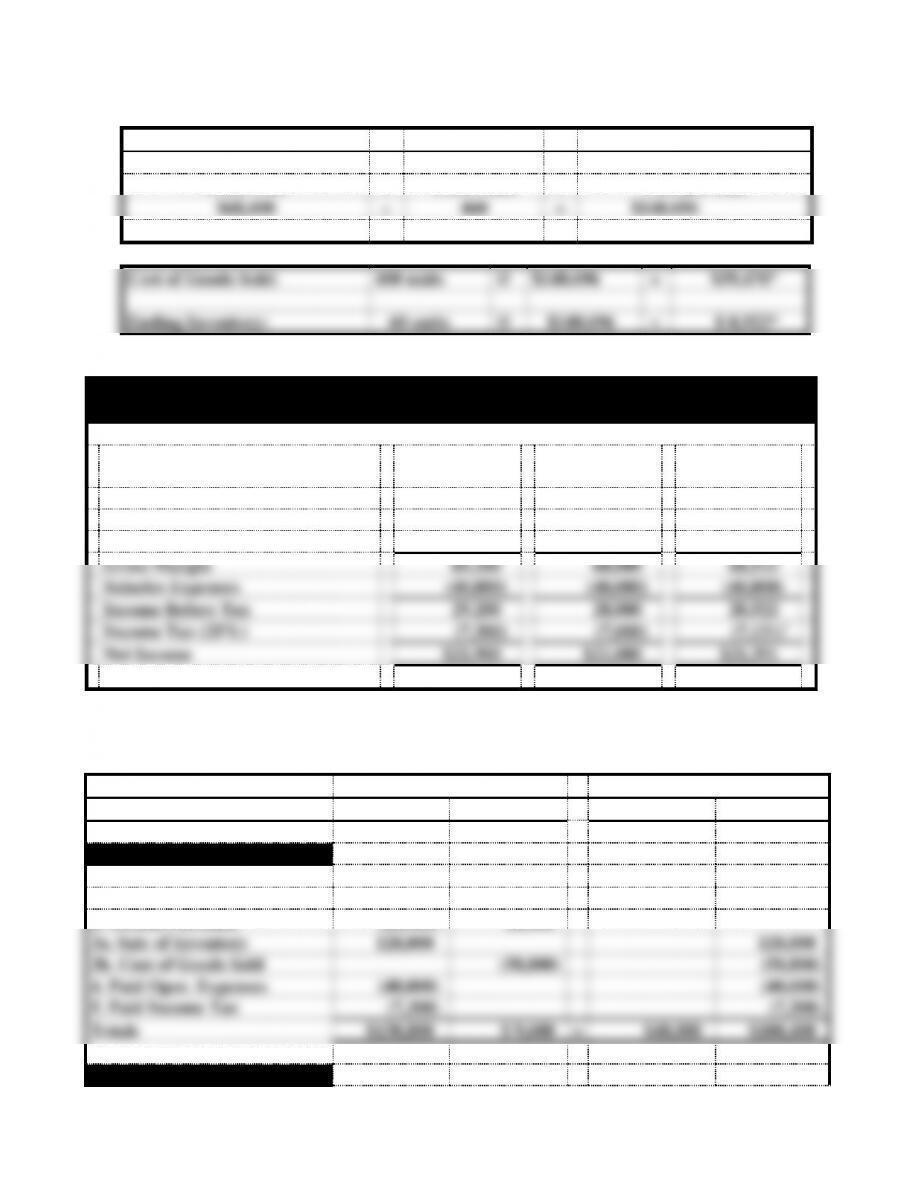

Carrol’s Lamp Shop

Computation of Income Tax Expense and Net Income

FIFO

LIFO

Weighted

Average

Sales (400 units @ $320)

$128,000

$128,000

$128,000

Cost of Goods Sold

(58,800)

(60,000)

(59,478)

Gross Margin

69,200

68,000

68,522

Salaries Expenses

(40,000)

(40,000)

(40,000)

Income Before Tax

29,200

28,000

28,522

Income Tax (25%)

(7,300)

(7,000)

(7,131)*

Net Income

$21,900

$21,000

$21,391

*RoundedPROBLEM 5-33 (cont.)

b. The Accounting Equation is provided for the use of the instructor.

Assets

=

Stockholders’ Equity

Event

Cash

Inventory

=

Com Stock

Ret. Earn.

FIFO Cost Flow

Beginning Balance

$90,500

$28,000

$40,000

$78,500

1. First Purchase

(18,000)

18,000

2. Second Purchase

(22,400)

22,400

3a. Sale of Inventory

128,000

128,000

3b. Cost of Goods Sold

(58,800)

(58,800)

4. Paid Oper. Expenses

(40,000)

(40,000)

5. Paid Income Tax

(7,300)

(7,300)

Totals

$130,800

$ 9,600

=

$40,000

$100,400

LIFO Cost Flow

5-8

Beginning Balance

$90,500

$28,000

$40,000

$78,500

1. First Purchase

(18,000)

18,000

2. Second Purchase

(22,400)

22,400

3a. Sale of Inventory

128,000

128,000

3b. Cost of Goods Sold

(60,000)

(60,000)

4. Paid Oper. Expenses

(40,000)

(40,000)

5. Paid Income Tax

(7,000)

(7,000)

Totals

$131,100

$ 8,440

=

$40,000

$99,500

Weighted Average

Beginning Balance

$90,500

$28,000

$40,000

$78,500

1. First Purchase

(18,000)

18,000

2. Second Purchase

(22,400)

22,400

3a. Sale of Inventory

128,000

128,000

3b. Cost of Goods Sold

(59,478)

(59,478)

4. Paid Oper. Expenses

(40,000)

(40,000)

5. Paid Income Tax

(7,131)

(7,131)

Totals

$130,969

$ 8,922

=

$40,000

$99,891

5-9

PROBLEM 5-33 (cont.)

b.

Carrol’s Lamp Shop

Financial Statements

FIFO

LIFO

Weight. Av.

Income Statements

For Year Ended December 31, 2014

Sales

$128,000

$128,000

$128,000

Cost of Goods Sold

(58,800)

(60,000)

(59,478)

Gross Margin

69,200

68,000

68,522

Salaries Expense

(40,000)

(40,000)

(40,000)

Income Before Tax

29,200

28,000

28,522

Income Tax Expense

(7,300)

(7,000)

(7,131)

Net Income

$21,900

$21,000

$21,391

Balance Sheets

As of December 31, 2013

Assets

Cash

$130,800

$131,100

$130,969

Inventory

9,600

8,400

8,922

Total Assets

$140,400

$139,500

$139,891

Stockholders’ Equity

Common Stock

$40,000

$40,000

$40,000

Retained Earnings

100,400

99,500

99,891

Total Stockholders’ Equity

$140,400

$139,500

$139,891

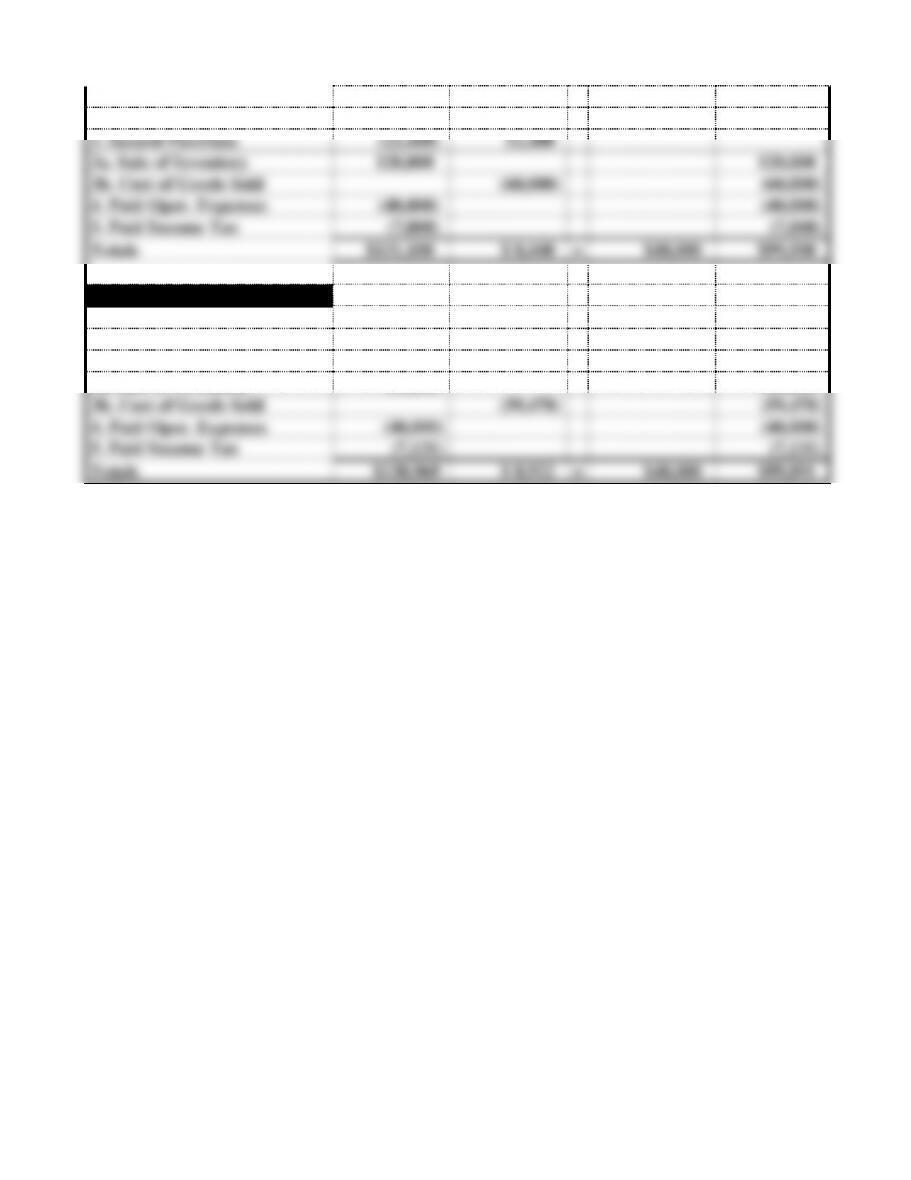

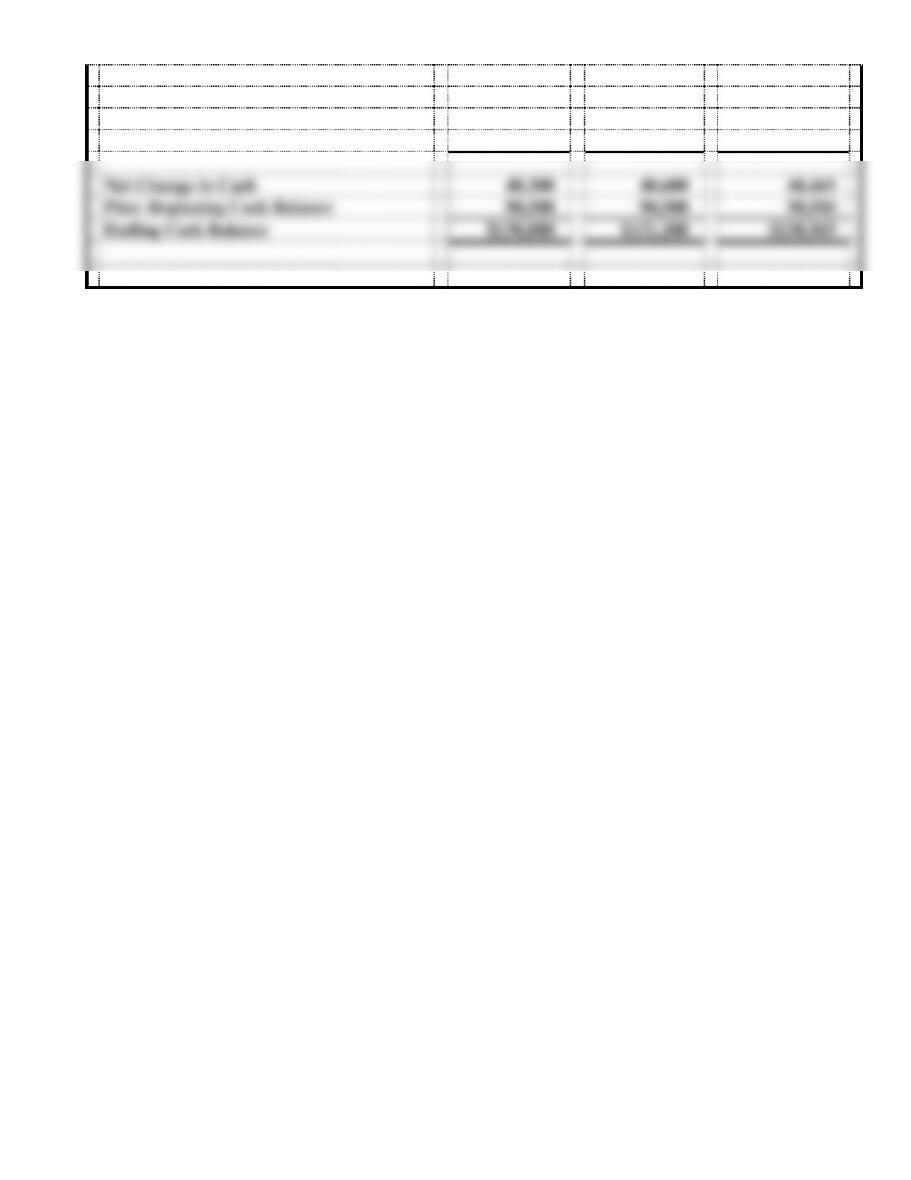

PROBLEM 5-33 b. (cont.)

Carrol’s Lamp Shop

Statements of Cash Flows

For the Year Ended December 31, 2014

FIFO

LIFO

Weight. Av.

Cash Flows From Oper. Act.:

Cash Inflow from Customers

$128,000

$128,000

$128,000

Cash Outflow for Inventory

(40,400)

(40,400)

(40,400)

Cash Outflow for Sal. Exp.

(40,000)

(40,000)

(40,000)

Cash Outflow for Income Tax

(7,300)

(7,000)

(7,131)

Net Cash Flow from Oper. Act.

40,300

40,600

40,469

5-10

Cash Flows From Investing Act.

-0-

-0-

-0-

Cash Flows From Financing Act.

-0-

-0-

-0-

Net Change in Cash

40,300

40,600

40,469

Plus: Beginning Cash Balance

90,500

90,500

90,500

Ending Cash Balance

$130,800

$131,100

$130,969

5-11

ATC 5-1

Dollar amounts are in millions.

a. Receivables ÷ Total assets = %

b. Allow. for doubtful accts. ÷ Acct. Rec. = Uncollectible %

c. According to Note 11, “Historically, we recognized an allowance for doubtful

d. Inventory ÷ Total assets = %

e. According to Note 12, the company uses the LIFO method.

f. No, according to Note 12, “We routinely enter into arrangements with vendors