ANSWERS TO QUESTIONS – CHAPTER 4

2. Internal control is the process designed to ensure reliable financial reporting, effective

and efficient operations, and compliance with applicable laws and regulations.

3. Section 404 of Sarbanes-Oxley requires a statement of management’s responsibility for

establishing and maintaining adequate internal control over financial reporting by

4. The five components of COSO’s framework are as follows:

1. Control Environment. The integrity and ethical values of the company,

actions that set the tone of the organization.

2. Risk Assessment. Management’s process of identifying potential risks that

3. Control Activities. These are the activities usually thought of as “the internal

control.” They include such things as separation of duties, account

4. Information and Communication. The internal and external reporting process,

and includes an assessment of the technology environment.

5. Monitoring. Assessing the quality of a company’s internal control over time

organization.

5. The Enterprise Risk Management (ERM)-An Integrated Framework is an updated

6. A strong internal control system should have:

• Separation of duties

7. Separation of duties is the procedure whereby different individuals separately perform

8. Quality employees should have the necessary ability to perform the required task and

9. A fidelity bond is insurance that a company can purchase to protect against loss due to

employee dishonesty.

10. When employees are not required to take extended periods of leave or vacation, the

11. The procedures manual sets forth the proper procedures for processing transactions.

12. Specific authorizations generally apply to specific positions within the organization.

For example, sale of major assets can only be authorized by the board of directors,

13. The use of prenumbered documents (i.e., checks, receipts, and invoices) is a control to

14. Physical controls are designed to safeguard assets. Storerooms should be kept locked

with limited access. Serial numbers on equipment should be recorded. Unannounced

15. Independent verification of performance provides an objective evaluation. It also

16. Cash includes currency and other items payable on demand such as checks, money

orders, bank drafts, and savings accounts.

In most cases, possession equates to ownership.

18. Giving customers receipts helps to prevent theft of cash receipts. Any missing receipts

19. Control procedures over cash receipts include:

• Timely deposits.

20. Procedures that will help protect cash disbursements include making all

disbursements by check, using prenumbered checks kept in a secure place, and

reference.

21. A debit memo included with the bank statement reduces the amount of cash and a

22. Information usually contained in the bank statement includes:

• The balance of the account at the beginning of the period.

23. The bank‘s balance will be larger than the book balance if there are outstanding

24. The bank reconciliation is a schedule prepared to identify items causing differences

between the bank statement balance and the Cash account balance. Preparation of a

25. An outstanding check is a cash disbursement that has been recorded on the payer’s

not “cleared” the bank).

26. A deposit in transit is a deposit that has been recorded on the depositor’s books but

27. A certified check is a check guaranteed by a bank to be a check drawn on an account

28. The amount of a customer check that was deposited and is later found to be NSF must

29. The three elements of the fraud triangle are (1) the availability of an opportunity (2)

30. The Six Articles of the AICPA Code of Professional Conduct are listed in Exhibit 4-

4, p. 144.

SOLUTIONS TO EXERCISES – CHAPTER 4

EXERCISE 4-1

a. SOX refers to the Sarbanes-Oxley Act of 2002.

b. COSO stands for The Committee of Sponsoring Organizations of the Treadway

c. The five components of COSO’s framework are as follows:

actions that set the tone of the organization.

2. Risk Assessment. Management’s process of identifying potential risks that

3. Control Activities. These are the activities usually thought of as “the internal

statements.

4. Information and Communication. The internal and external reporting process,

and includes an assessment of the technology environment.

5. Monitoring. Assessing the quality of a company’s internal control over time

d. The Enterprise Risk Management (ERM)-An Integrated Framework is the undated

EXERCISE 4-2

1. Separation of Duties: Whenever possible, the functions of authorization, recording,

2. Quality of Employees: Employees should be competent and adequately trained to

perform the required task.

3. Bonded Employees: Employers should hire employees with high personal integrity.

4. Periods of Absence: Employees should be required to take extended vacations

and/or be rotated among duties in order to discover patterns of dishonesty or theft.

5. Procedures Manual: A procedures manual should be established, kept up-to-date,

being followed.

6. Authority and Responsibility: A clear chain of command should be established and

for specific and general authority.

7. Prenumbered Documents: The use of prenumbered documents (checks, receipts,

8. Physical Control: All assets should be properly documented, and periodically

accounted for, with access limited to authorized personnel.

EXERCISE 4-3

Some of the internal control features that should be included in the memo to Dick Haney:

• Have as much separation of duties as possible. The manager should prepare the deposit

of cash receipts collected by the sales personnel. Dick should periodically check these

• Use prenumbered documents.

EXERCISE 4-4

• Receipts should be promptly written for all cash received and the funds deposited

• Cash handling and cash record-keeping duties should be separated as well as

authorization for cash disbursements.

EXERCISE 4-5

a. The discrepancy was most likely caused by theft by Rhonda Cox, the parts department

manager. It is unlikely that sloppy recordkeeping could account for this much of a

b. Separation of duties is one internal control procedure that could have helped prevent

this type of theft. If the company was so small that it had only one employee in the

Bonding the employees would help to insure against theft loss.

EXERCISE 4-6

Separation of duties would have eliminated this problem. Jones should not have had the

EXERCISE 4-7

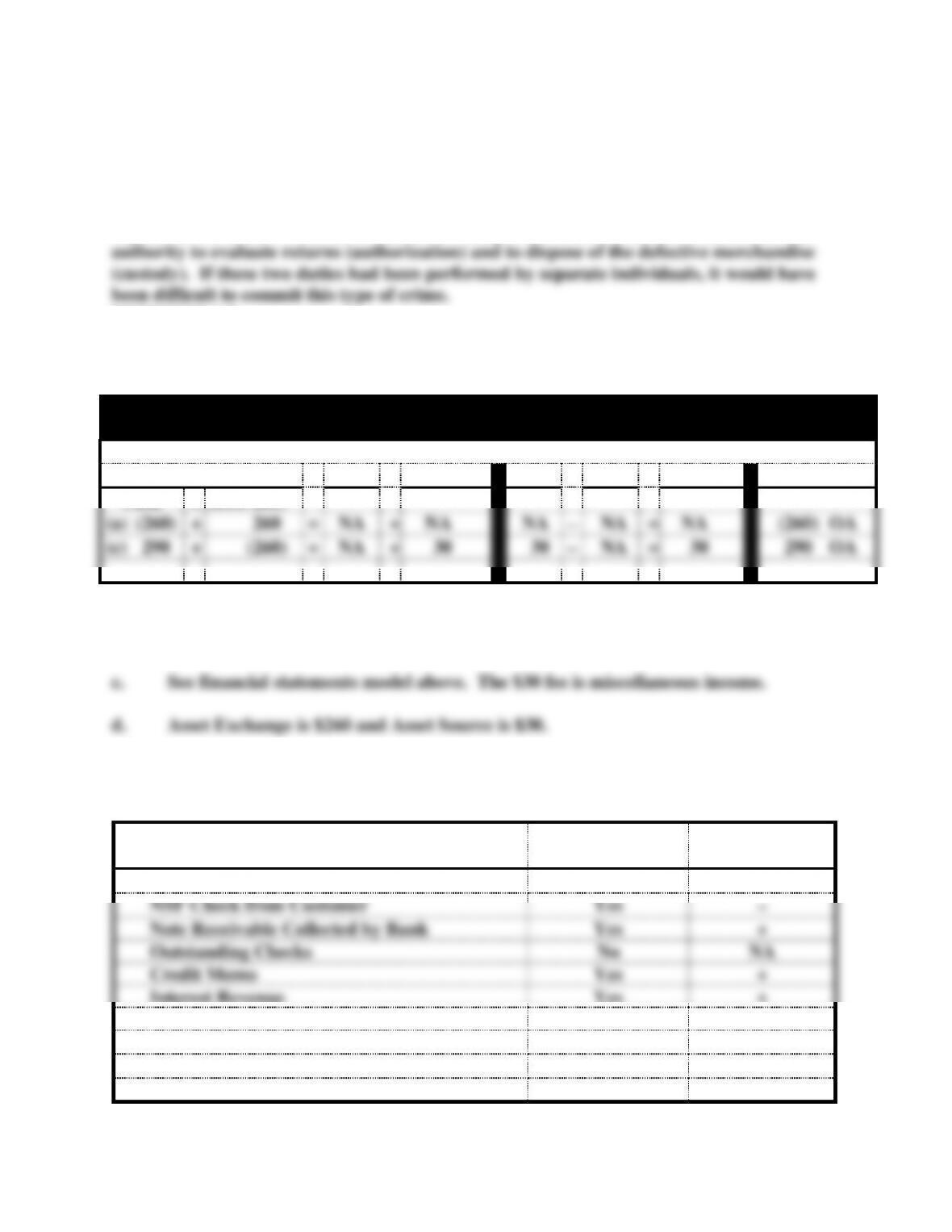

a. & c.

Montgomery Stationery

Statements Model

Assets

=

Liab.

+

S. Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Cash

+

Acct. Rec.

(a) (260)

+

260

=

NA

+

NA

NA

−

NA

=

NA

(260) OA

(c) 290

+

(260)

=

NA

+

30

30

−

NA

=

30

290 OA

b. Asset exchange.

EXERCISE 4-8

Reconciling Items

Book Balance

Adjusted?

Added or

Subtracted?

Charge for Checks

Yes

−

NSF Check from Customer

Yes

−

Note Receivable Collected by Bank

Yes

+

Outstanding Checks

No

NA

Credit Memo

Yes

+

Interest Revenue

Yes

+

Deposits in Transit

No

NA

Debit Memo

Yes

−

Service Charge

Yes

−

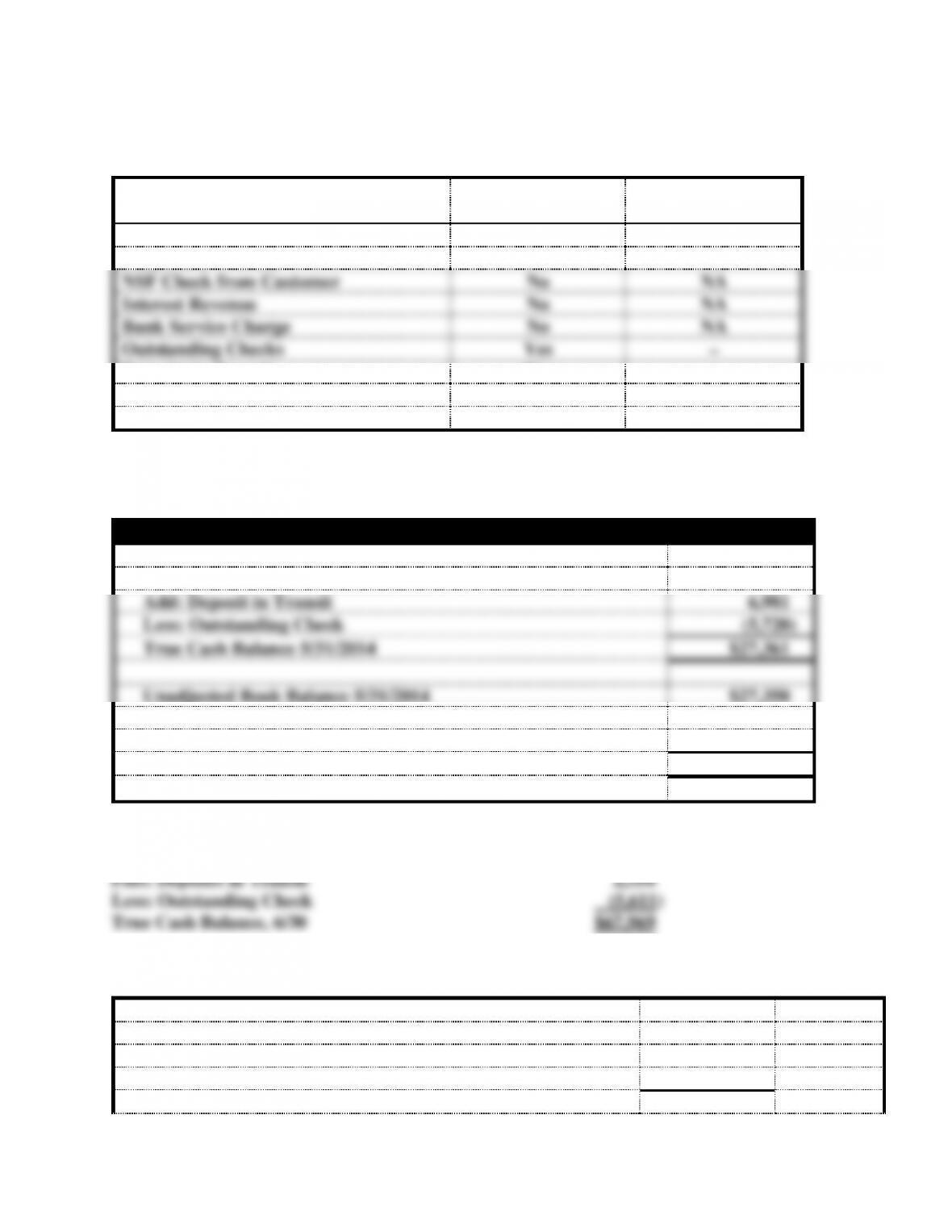

EXERCISE 4-9

Reconciling Items

Bank Balance

Adjusted?

Added or

Subtracted?

Certified Checks

No

NA

Petty Cash Voucher

No

NA

NSF Check from Customer

No

NA

Interest Revenue

No

NA

Bank Service Charge

No

NA

Outstanding Checks

Yes

−

Deposits in Transit

Yes

+

Debit Memo

No

NA

Credit Memo

No

NA

EXERCISE 4-10

Bank Reconciliation

Unadjusted Bank Balance 5/31/2014

$26,100

Add: Deposit in Transit

6,981

Less: Outstanding Check

(5,720)

True Cash Balance 5/31/2014

$27,361

Unadjusted Book Balance 5/31/2014

$27,350

Add: Credit Memo for Interest Earned

36

Less: Debit Memo for Service Charge

(25)

True Cash Balance 5/31/2014

$27,361

EXERCISE 4-11

Unadjusted Bank Balance, 6/30 $71,230

EXERCISE 4-12

Unadjusted Book Balance, 5/31

$7,215

Add: Interest Earned

$ 13

Note Collected by Bank

500

513

Less: NSF Check

68

Service Charges

50

(118)

True Cash Balance, 5/31

$7,610

EXERCISE 4-13

According to Article II (The Public Interest) of the AICPA Code of Professional Conduct,

an accounting professional should act in a way that will serve the public interest and honor

the public trust. Because Jessica is the sister of Mark Miller, her independence as the

EXERCISE 4-14

a. Several of the articles should be mentioned in the memo.

Article I Responsibilities

As a professional, Kato should exercise professional and moral judgment in

his position.

b. Pleading ignorance would not relieve Kato of responsibility. Article V requires that

members of the profession be competent and provide quality services.