4-1

1

EXERCISE 4-15

The three common features of ethical misconduct are:

1. The availability of an opportunity

By arguing that gambling on sports is no different than using accounting

information to buy stock, Jacob is rationalizing gambling, an activity that

EXERCISE 4-16

The memo should contain some of the following information:

Something is considered material if knowing about the problem would

affect the decisions of an average prudent investor. Thus, the concept is

subjective.

a. Since Ms. Norman was not able to complete the audit procedures,

b. The three types of audit opinions are:

1. Unqualified opinion – This is the most desirable type of

2. Adverse opinion – This is the most undesirable type of

opinion. This type of opinion means that something in the

4-2

2

3. Qualified opinion – This type of opinion means that for the

SOLUTIONS TO PROBLEMS

PROBLEM 4-18

a. Separation of duties would have helped to prevent this type of act.

b. Again, separation of duties would help to prevent this type of fraud.

c. Better control procedures could help eliminate this type of act.

Require an authorization for any discounts that are given. Also,

Four Aces

Bank Reconciliation

August 31, 2014

Unadjusted Bank Balance, August 31, 2014

$15,320

Add: Deposit in Transit

4,295

Less: Outstanding Checks

( 5,030)

True Cash Balance, August 31, 2014

$14,585

Unadjusted Book Balance, August 31, 2014

$13,910

Add: Error in recording check for inventory

750

Less: Debit Memo for new checks

(75)

True Cash Balance, August 31, 2014

$14,585

4-3

3

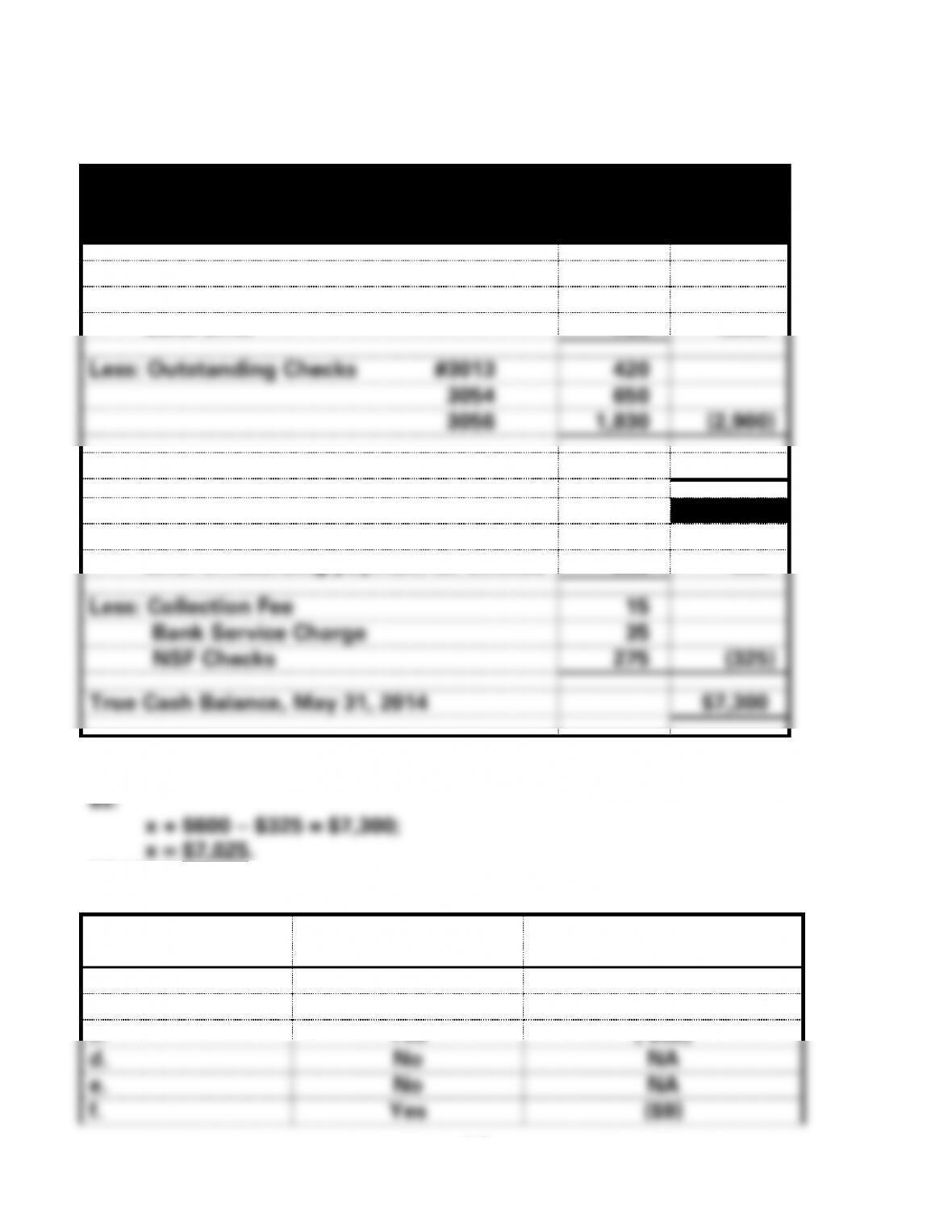

PROBLEM 4-20

Larry’s Auto Supply, Inc.

Bank Reconciliation

May 31, 2014

Unadjusted Bank Balance, May 31, 2014

$8,250

Add: Deposits in Transit

$1,230

Bank Error

720

1,950

Less: Outstanding Checks #3013

420

3054

650

3056

1,830

(2,900)

True Cash Balance, May 31, 2014

$7,300

Unadjusted Book Balance, May 31, 2014

$7,025*

Add: Note Collected by Bank

$ 400

Error in recording payment for utilities

200

600

Less: Collection Fee

15

Bank Service Charge

35

NSF Checks

275

(325)

True Cash Balance, May 31, 2014

$7,300

*Unadjusted cash balance per Larry’s Auto Supply’s books is computed

PROBLEM 4-21

Reconciling Items

Book Balance

Adjusted?

Added or

Subtracted?

a.

Yes

($30)

b.

No

NA

c.

Yes

( $62)

d.

No

NA

e.

No

NA

f.

Yes

($9)

4-4

4

g.

Yes

450

h.

No

NA

PROBLEM 4-22

a.

Sunset Valley Hotel

Bank Reconciliation

July 31, 2014

Unadjusted Bank Balance, July 31, 2014

$14,929

Add: Deposit in Transit

3,550

Less: Outstanding Checks #2353

$1,500

2356

745

(2,245)

True Cash Balance, July 31, 2014

$16,234

Unadjusted Book Balance, July 31, 2014

$13,200

Add: Credit Memo for Collection of Notes

Receivable

3,050

Less: Debit Memo for Printed Checks

(16)

True Cash Balance, July 31, 2014

$16,234

b.

Item No.

Affect on the cash account:

1.

Not affected

2.

Cash is increased

3.

Not affected

4.

Cash is decreased

5.

Not affected

6.

Not affected

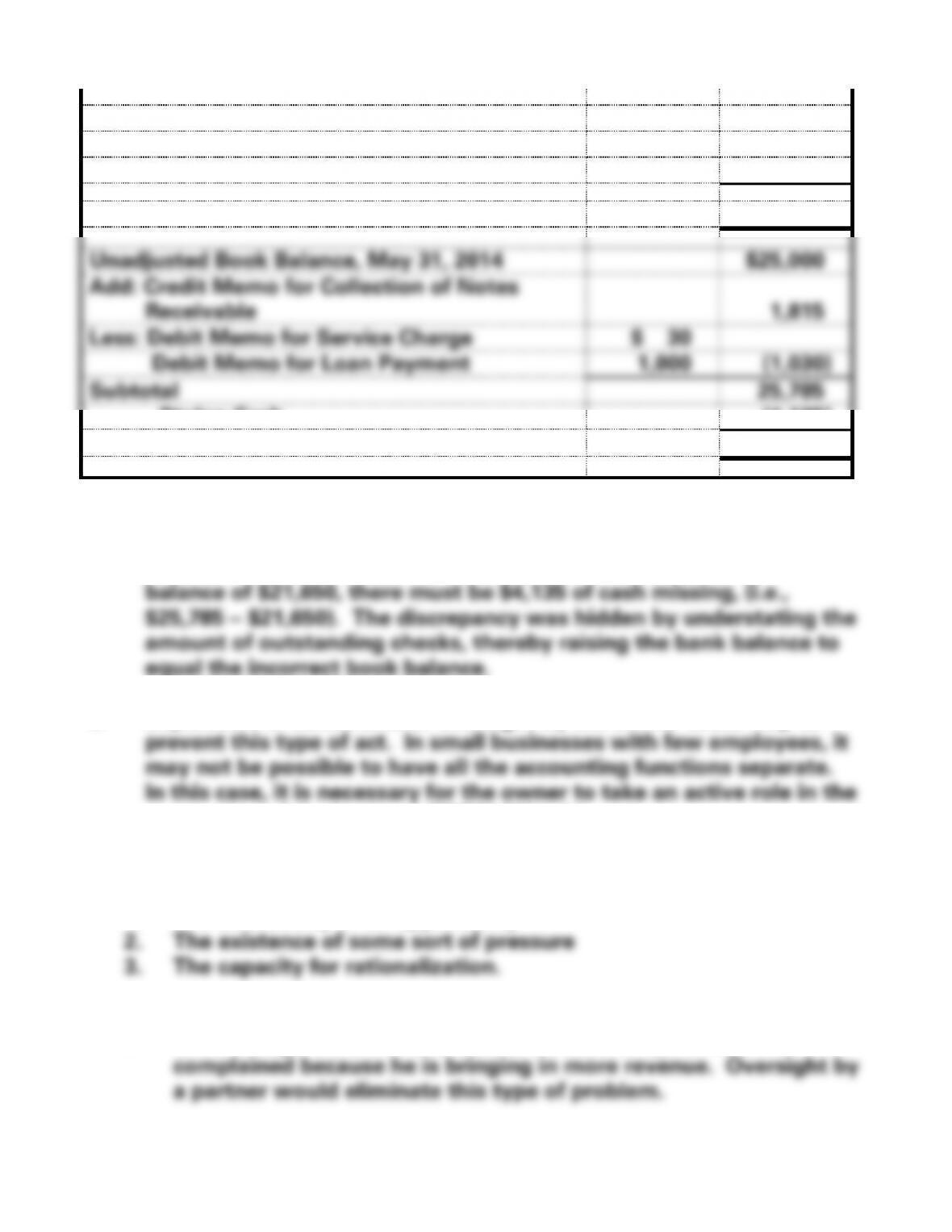

PROBLEM 4-23

a.

Pizza Express

Bank Reconciliation

May 31, 2014

4-5

Unadjusted Bank Balance, May 31, 2014

$22,000

Add: Deposit in Transit

4,250

Less: Outstanding Checks

(4,600)

True Cash Balance, May 31, 2014

$21,650

Unadjusted Book Balance, May 31, 2014

$25,000

Add: Credit Memo for Collection of Notes

Receivable

1,815

Less: Debit Memo for Service Charge

$ 30

Debit Memo for Loan Payment

1,000

(1,030)

Subtotal

25,785

Stolen Cash

(4,135)

True Cash Balance, May 31, 2014

$21,650

b. Correcting the amount of outstanding checks from $465 to $4,600

reveals a true cash balance of $21,650. Given the adjusted book

c. Separation of duties and/or oversight by the owner could help to

accounting of the business.PROBLEM 4-24

The three common features of ethical misconduct are:

1. The availability of an opportunity

1. Even though Robert has exceeded his authority, no one has

4-6

6

2. Robert is in a financial bind and does not want to discuss his

3. He rationalizes that his actions do not hurt anyone because the

PROBLEM 4-25

The memo should explain that his confidentiality requirements prohibit

actsPROBLEM 4-26

The memo should contain some of the following points:

1. Neither the CPA firm, a CPA of the firm, nor family members of the

CPA can have any ownership interest in the company it is auditing.

5. The CPA has a legal responsibility to members of the public who

have an interest in the firm being audited. Protection of the public is

a. According to Note 10, “Cash equivalents include highly liquid

investments with an original maturity of three months or less from

4-7

7

b. The two reports are the “Report of Management on Internal

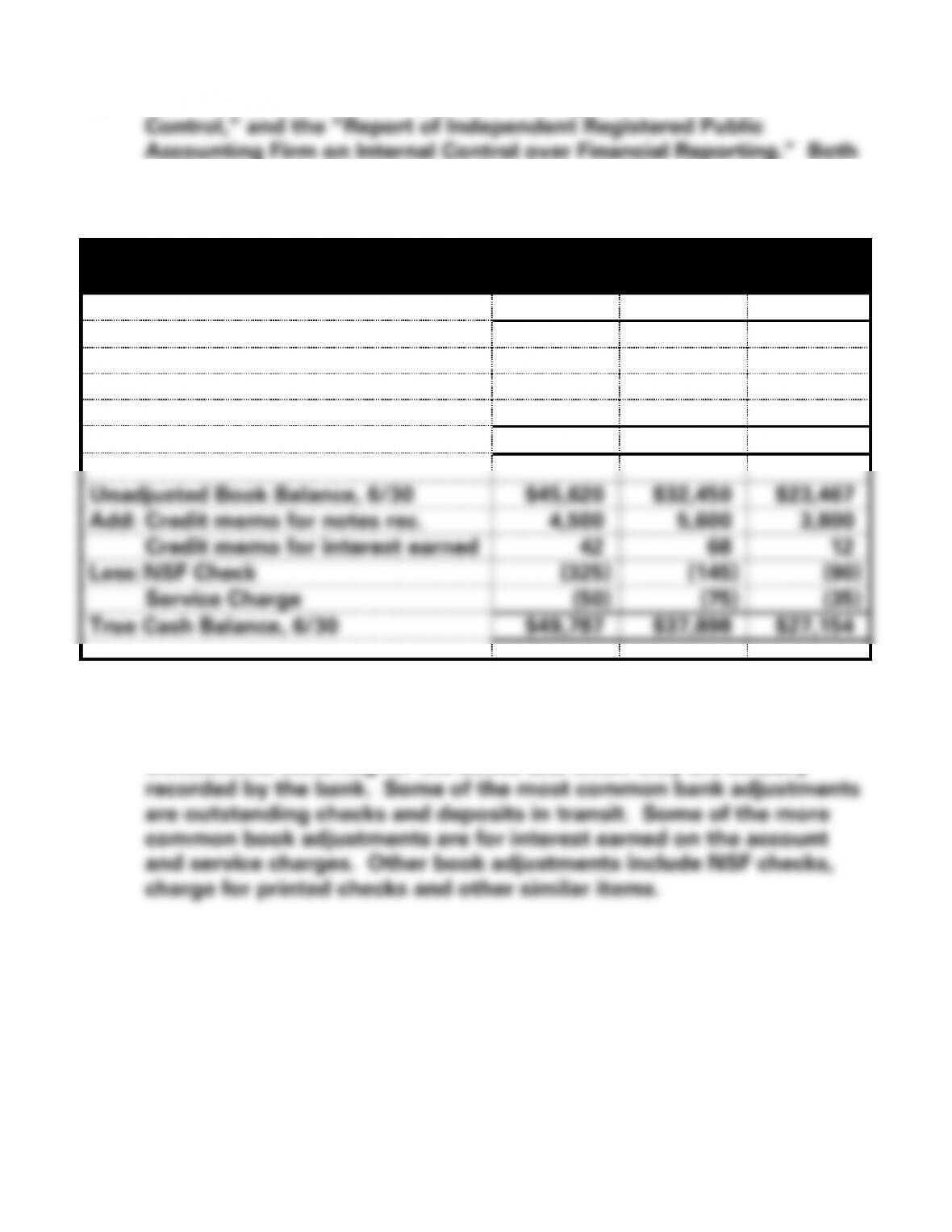

of these reports are on page 31.ATC 4-2

a. (1)

Bank Reconciliation

June 30, 2014

Peach Co.

Apple Co.

Pear Co.

Unadjusted Bank Balance, 6/30

$48,632

$37,176

$24,894

Add: Deposits in Transit

2,500

3,200

4,800

Less: Outstanding Checks

(1,345)

(2,478)

(2,540)

True Cash Balance, 6/30

$49,787

$37,898

$27,154

Unadjusted Book Balance, 6/30

$45,620

$32,450

$23,467

Add: Credit memo for notes rec.

4,500

5,600

3,800

Credit memo for interest earned

42

68

12

Less: NSF Check

(325)

(145)

(90)

Service Charge

(50)

(75)

(35)

True Cash Balance, 6/30

$49,787

$37,898

$27,154

b. The unadjusted cash balance and the ending bank statement

balance will generally be different because of the timing of

transactions occurring for the books and when they are actually

4-8

8

ATC 4-3

This solution is based on Smucker’s Form 10-K for year ended April 30,

2009, filed with the SEC on June 26, 2009.

a. Note 1 on page 47 defines cash and cash equivalents as:

b. The company’s annual report included two reports in which

Report of Management on Internal Control over Financial Reporting

on page 37.

ATC 4-4

Some of the procedures that should be suggested include:

• Separation of duties.

ATC 4-5

a. John’s scheme affects Southeast Industries’ balance sheet in two

ways. Since cash was erroneously paid for Mr. Tyler after his

4-9

9

b. Article I (responsibilities) of the AICPA Code of Professional Conduct

requires members to carry out their responsibilities with sensitive

c. The three elements of the fraud triangle are:

The existence of some form of pressure leading to an incentive –

The availability of an opportunity – John had the opportunity to carry

out his scheme with impunity because of weak internal controls at

indicated by past performance raises and Bill Jameson’s

acknowledgment that John “deserved a raise.” He may have also

ATC 4-5 (cont.)