ANSWERS TO QUESTIONS – CHAPTER 2

1. Accrual accounting attempts to record the effects of accounting events in the period

2. Recognition is the act of recording an event in the financial statements. When

3. Deferral is the recognition of revenue or expenses in a period after the cash

4. If cash is collected in advance for services, the revenue is recognized when the

services are rendered.

6. The issue of common stock, which is capital acquired from owners, increases

7. The recognition of revenue on account increases the corresponding revenue account

flow statement is affected when the account is collected.

8. Asset Source Transaction Effect on Accounting Equation

Issue of Common Stock Increases Assets

Increases Common Stock

9. Revenue is recognized under accrual accounting when a revenue-producing event

10. The collection of cash for accounts receivable is an asset exchange transaction. Only

11. If cash is collected in advance for services, a liability is created (unearned revenue),

increasing the claims side of the accounting equation.

13. The recognition of expenses affects the accounting equation by either decreasing

14. A claims exchange transaction is one where the claims of creditors (liabilities)

The total amount of claims is unchanged.

15. Cash payments to creditors are asset use transactions. These transactions result in

16. Expenses are recognized under accrual accounting at the time the expense is

incurred or resources are consumed, regardless of when cash payment is made.

17. Net cash flows from operations on the cash flow statement may be different from net

18. The income statement reflects the change in net assets associated with operating a

19. Net income increases stockholders’ claims on business assets by increasing retained

earnings.

20. A cost can be either an asset or an expense. If the item acquired has already been

21. A cost is held in the asset account until the item is used to produce revenue. When

the revenue is generated, the asset is converted into an expense in order to match

22. Supplies used during the accounting period are recognized in a single adjusting

supplies purchased).

23. An expense is a decrease in assets or an increase in liabilities that occurs in the

process of generating revenue.

25. The purpose of the statement of changes in stockholders’ equity is to display the

as a result of its operations and transactions with its stockholders.

26. The purpose of the balance sheet is to provide information about an entity’s assets,

27. The balance sheet is dated as of a specific date because it shows information about

an entity’s assets, liabilities, and stockholders’ equity as of that date, not measured

28. Assets are listed on the balance sheet in accordance with their respective levels of

liquidity (how rapidly they can be converted to cash).

29. The statement of cash flows explains the change in cash from one accounting period

30. An adjusting entry is an entry that updates account balances prior to preparation of

the financial statements. The entry means that there is an item that needs proper

31. Temporary accounts (revenue, expense and dividends) are closed at the end of the

32. Period costs are costs that are recognized in an accounting period. Examples of

period costs include rent expense, utilities expense, and salaries expense.

produces.

34. The four stages of the accounting cycle: Record transactions; adjust the accounts;

prepare statements; and close the temporary accounts. The adjustment and closing

SOLUTIONS TO EXERCISES – CHAPTER 2

EXERCISE 2-1

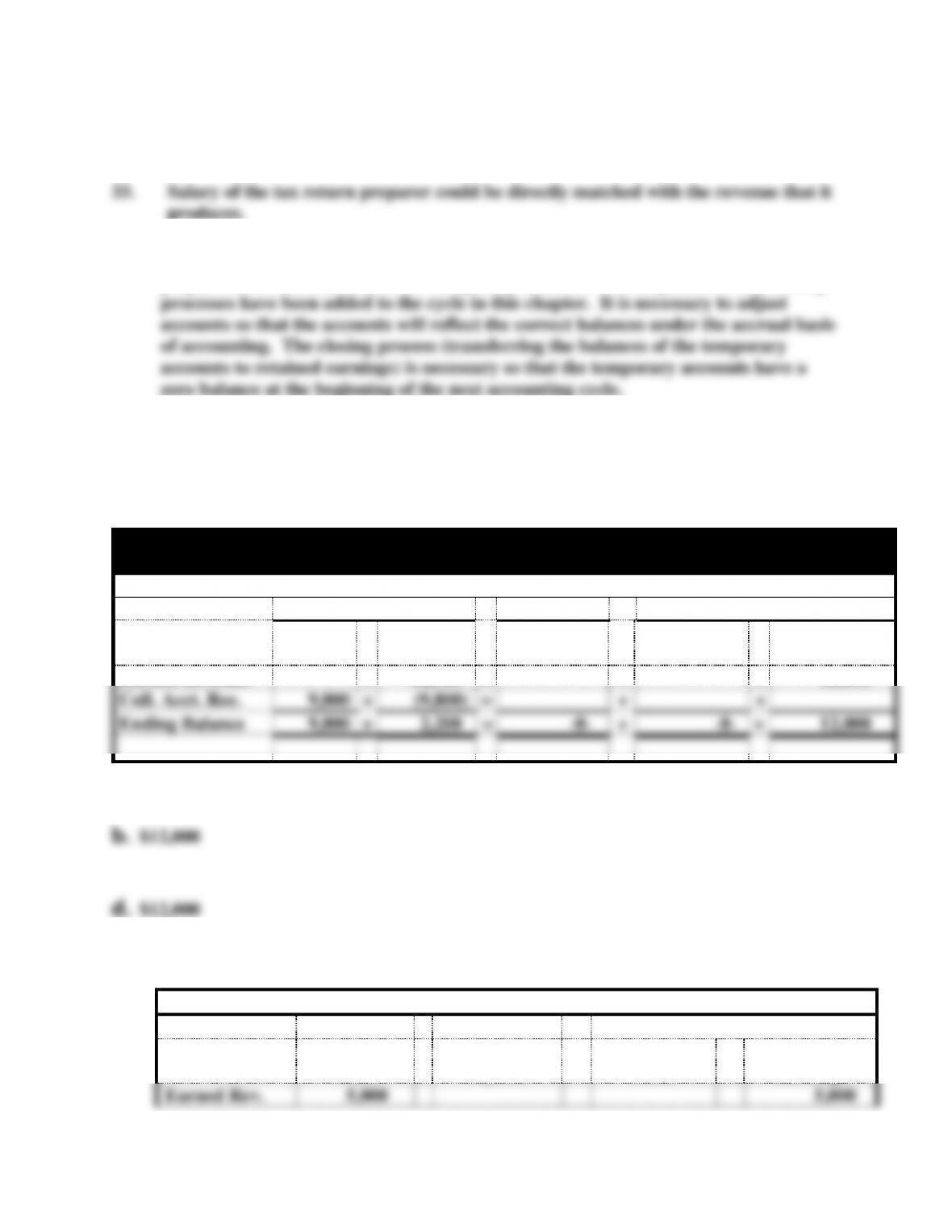

Burke Company

Effect of Events on the 2014 Accounting Equation

Assets

=

Liabilities

+

Stockholders’ Equity

Event

Cash

+

Accounts

Rec.

=

+

Common

Stock

+

Retained

Earnings

Earned Revenue

+

12,000

=

+

+

12,000

Coll. Acct. Rec.

9,800

+

(9,800)

=

+

+

Ending Balance

9,800

+

2,200

=

-0-

+

-0-

+

12,000

a. Accounts Receivable: $12,000 – $9,800 = $2,200

c. $9,800 cash collected from accounts receivable.

e. $12,000 of revenue was earned but only $9,800 of it was collected. EXERCISE 2-2

a.

Crest Corporation Accounting Equation – 2014

Event

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

=

Salaries

Payable

+

Common

Stock

+

Retained

Earnings

Earned Rev.

5,000

5,000

Accrued Sal.

(3,000)

(3,000)

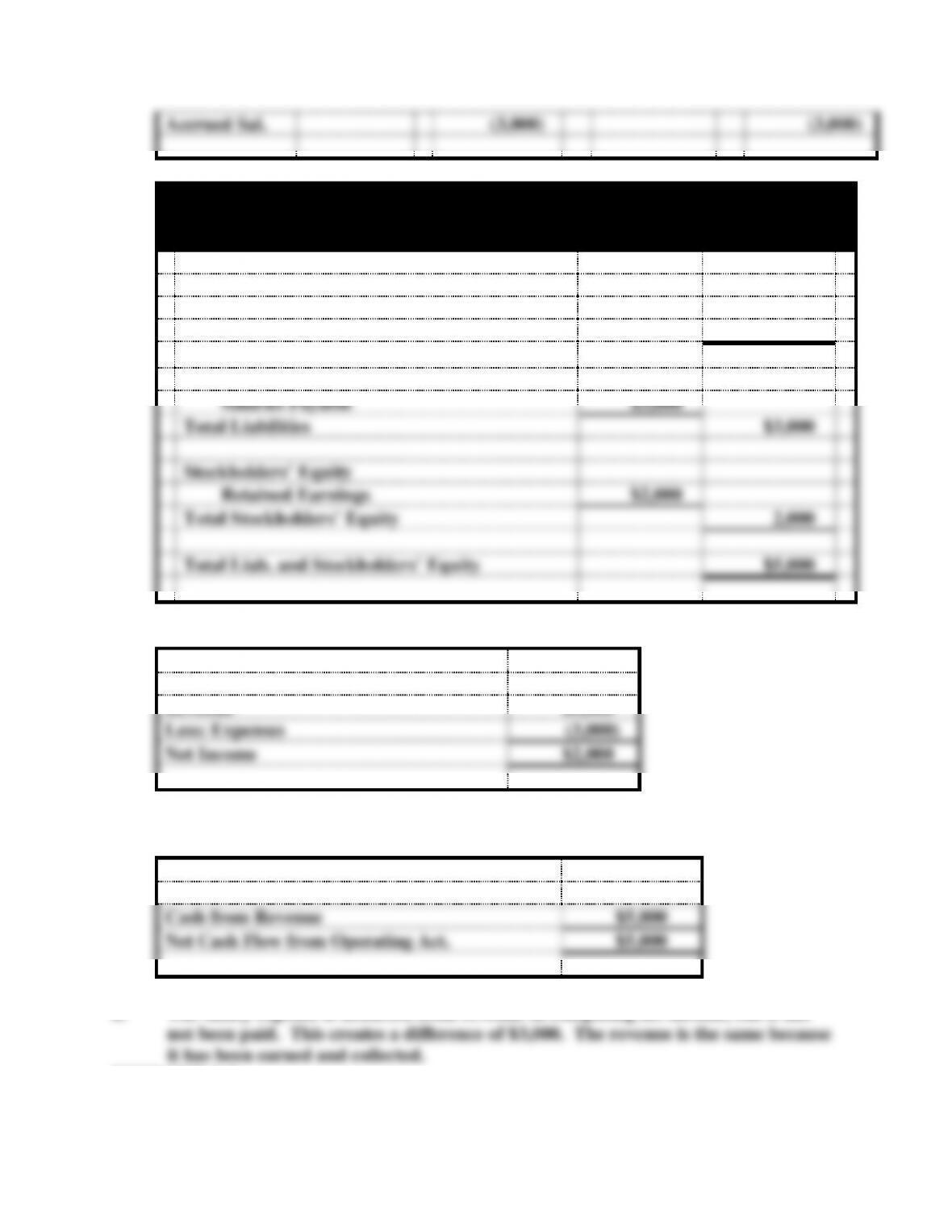

Crest Corporation

Balance Sheet

As of December 31, 2014

Assets

Cash

$5,000

Total Assets

$5,000

Liabilities

Salaries Payable

$3,000

Total Liabilities

$3,000

Stockholders’ Equity

Retained Earnings

$2,000

Total Stockholders’ Equity

2,000

Total Liab. and Stockholders’ Equity

$5,000

b.

Computation of Net Income

Revenue

$5,000

Less: Expenses

(3,000)

Net Income

$2,000

EXERCISE 2-2 (cont.)

c.

Cash Flow from Operating Activities

Cash from Revenue

$5,000

Net Cash Flow from Operating Act.

$5,000

d. The salary expense is deducted from revenue in computing net income, but it has

EXERCISE 2-3

a.

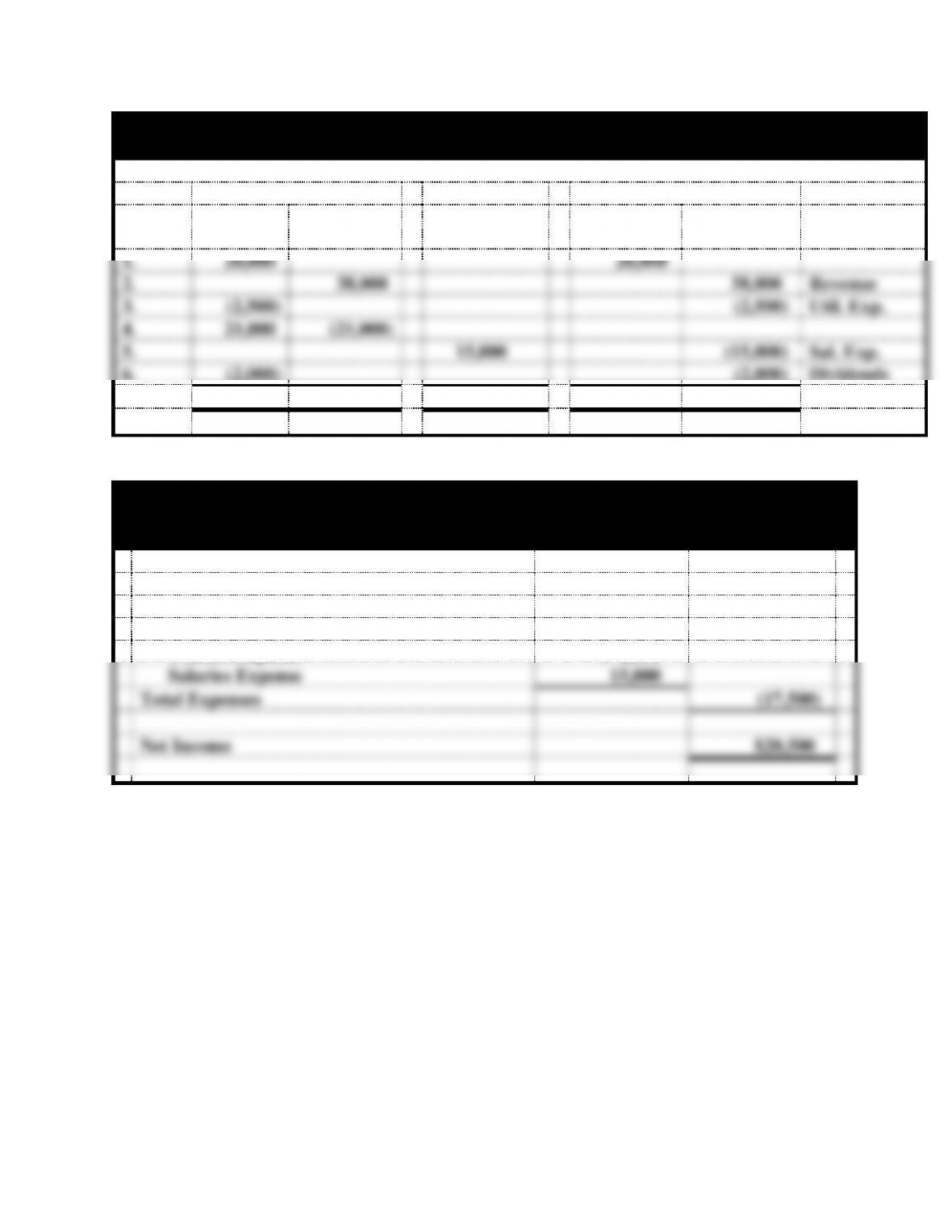

Coates, Inc.

General Ledger Accounts for the Year Ended December 31, 2014

Assets

=

Liabilities

+

Stockholders’ Equity

Event

Cash

Accts. Rec.

=

Salaries Pay.

+

Common

Stock

Retained

Earnings

Acct. Title

for RE

1.

20,000

20,000

2.

38,000

38,000

Revenue

3.

(2,500)

(2,500)

Util. Exp.

4.

21,000

(21,000)

5.

15,000

(15,000)

Sal. Exp.

6.

(2,000)

(2,000)

Dividends

Totals

36,500

17,000

=

15,000

+

20,000

18,500

b.

Coates, Inc.

Income Statement

For the Year Ended December 31, 2014

Revenue

$38,000

Expenses

Utilities Expense

$ 2,500

Salaries Expense

15,000

Total Expenses

(17,500)

Net Income

$20,500