Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

6-1

ANSWERS TO QUESTIONS - CHAPTER 6

1. Long-term operational assets are those assets that are used by a business to generate

2. Tangible assets are those assets that have a physical existence. Some examples include

3. Specifically identifiable intangible assets are those assets that are purchased for a specific

value or have a known value. Examples include patents, leases, and copyrights. Intangible

4. Depreciation is the systematic allocation of the cost of property, plant and equipment to the

5. Natural resources are assets that are produced by nature. Some examples include oil,

6. Land is not a depreciable asset because land has an infinite life. Land is not destroyed by its

7. Amortization is the systematic allocation of the cost of intangible assets over their estimated

8. The historical cost concept requires that long-term operational assets be recorded at the

amount paid for them. This is the amount that will be shown on the balance sheet as long as

9. The cost of a building includes the amount paid for the building plus any amounts that are

10. A basket purchase of assets is the purchase of a group of assets for a single purchase price.

6-2

relative fair market value method. The fair market value of each asset is determined and

then its ratio to the total fair market value of all assets is applied to the total purchase price.

11. The life cycle of a long-term operational asset simply describes the process of acquiring,

12. Straight-line depreciation. This method allocates an equal amount of depreciation to each

period over the useful life of the asset. Example: Asset cost of $4,000 with a 4-year life and

no salvage value would produce a depreciation expense of $1,000 per year. This method is

appropriate when the usefulness of an asset is consistent over the asset's life.

called double-declining balance because the method applies twice the straight-line rate to the

book value of the asset.

Example: Asset cost of $4,000 with an estimated useful life of 4 years would produce an

expense of $2,000 in the first year [$4,000 x (2 x .25)]. The amount of depreciation expense

13. Recognition of depreciation expense reduces total assets; while the asset account

14. The recognition of depreciation expense does not affect cash flows. Depreciation

15. Total assets will be lower at the end of the first year of the asset’s life if MalMax chooses the

double-declining balance method of computing depreciation rather than straight-line. This

16. When the total cost of an asset is expensed in the year acquired, total expense will be

6-3

17. Salvage value is the estimated value of a plant asset at the end of its useful life to the

business.

18. Accumulated depreciation is a contra asset account. As the cost of a plant asset is expensed,

a contra asset account is credited, rather than a direct reduction of the related asset account.

19. Book value of an asset is its historical cost less any accumulated depreciation.

20. Recording the depreciation recognized in the contra asset account allows the total cost of the

asset and the total amount expensed to be shown in the accounts and on the balance sheet.

21. Book value is computed as the cost of the equipment less the accumulated depreciation of

that equipment, $5,000 − $3,000 = $2,000. This does not represent the fair market value of

22. The method of depreciation chosen for a particular piece of equipment should represent

as closely as possible the pattern of its usage of that piece of equipment. For instance,

23. When an asset is purchased and put into service, an estimate is made of the expected

useful life of the asset. However, as the asset is used, it may become apparent that the

estimate was incorrect or circumstances may have changed (e.g., the asset is used more

24. When an expenditure improves the quality of an asset, this improvement is accounted for as

if a new asset is purchased; the equipment account is debited. The improvement is

6-4

25. When a long-term operational asset is sold for a gain, total assets and equity increase by the

amount of the gain. The gain is the amount the asset is sold for over the book value of the

26. Depletion is the process of systematically allocating the cost of natural resources to expense

based on estimated production of the asset. The most common method used to calculate

27. Some of the most common intangible assets include patents, copyrights, and goodwill.

Amortization is generally based on the legal life of the asset, the useful life of the asset, or, in

28. Most countries have developed accounting principles that they apply to financial

statements. While there are many similarities, some significant differences do exist. For

29. The estimated useful life and salvage of an asset is determined based on the judgment and

estimation of the accountant or management. Because the length of time of actual use and

the actual value at disposal is not known, these amounts are based on the best judgment of

SOLUTIONS TO EXERCISES - CHAPTER 6

EXERCISE 6-1

Note: There are many possibilities for answers to this question. The answers given are only a

few examples of long-term operational assets that these companies may own. Also note that even

6-5

though the companies have very different business activities, they may have some of the same

kinds of long-term operational assets.

(a) Freds:

Buildings, Office Equipment, Cash Registers, Shelving, Land, etc.

(d) Harley-Davidson Co.:

Buildings, Land, Office Equipment, Manufacturing Equipment, etc.EXERCISE 6-2

Event

Long-Term Operational Asset

a.

No

b.

Yes

c.

Yes (If the company is in a business that uses or sells timber)

d.

Yes (As long as it is not held for investment purposes)

e.

Yes

f.

Yes

g.

No

h.

Yes

i.

Yes

j.

No

k.

No

l.

Yes

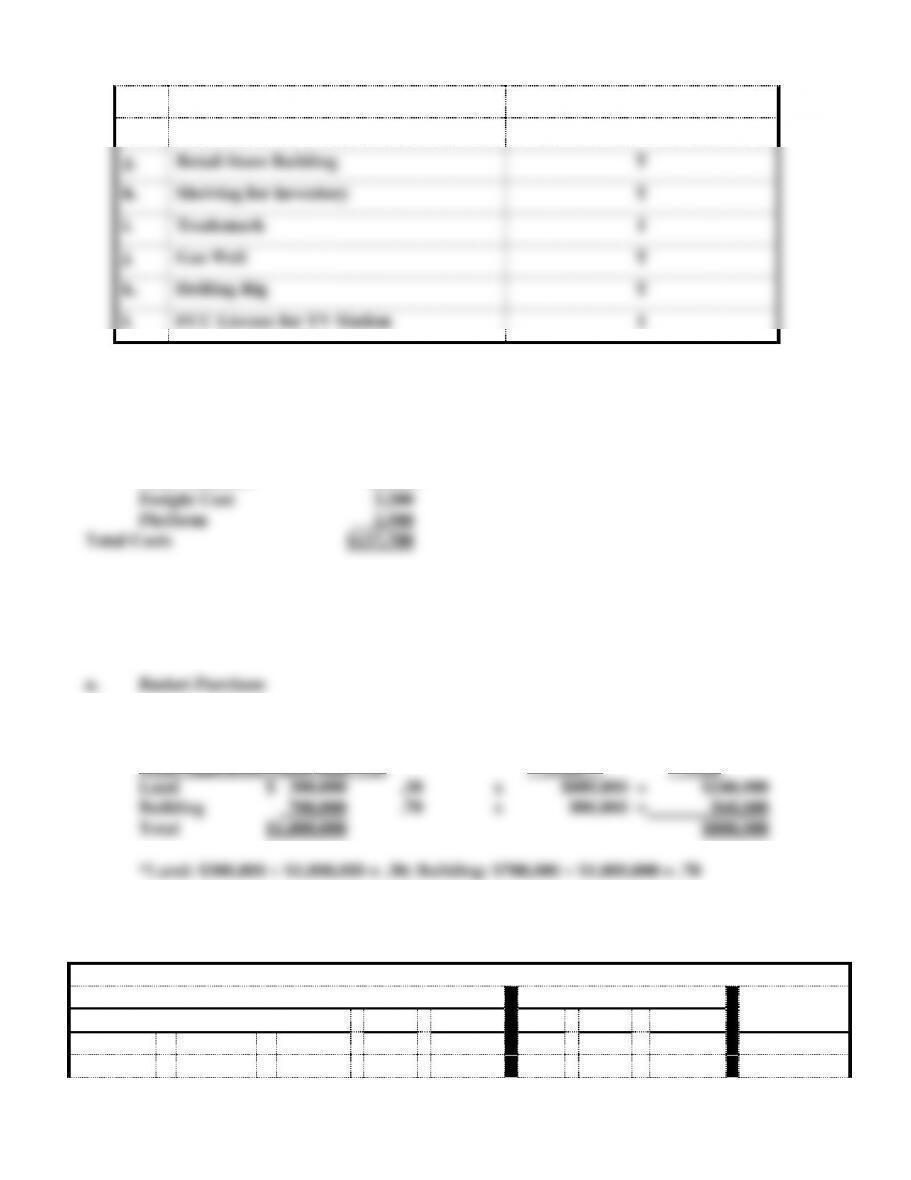

EXERCISE 6-3

No.

Tangible (T), Intangible (I)

a.

18-Wheel Truck

T

b.

Timber

T

c.

Log Loader

T

d.

Dental Chair

T

6-6

e.

Goodwill

I

f.

Computer Software

I

g.

Retail Store Building

T

h.

Shelving for Inventory

T

i.

Trademark

I

j.

Gas Well

T

k.

Drilling Rig

T

l.

FCC License for TV Station

I

EXERCISE 6-4

Costs that are to be capitalized:

List Price $160,000

Less: Discount (8,000)*

*$160,000 x 5% = $8,000

The operator salary and increase in insurance are operating expenses.

EXERCISE 6-5

b. % of* Purchase Allocated

Total Appraised Value App. Val. Price Cost

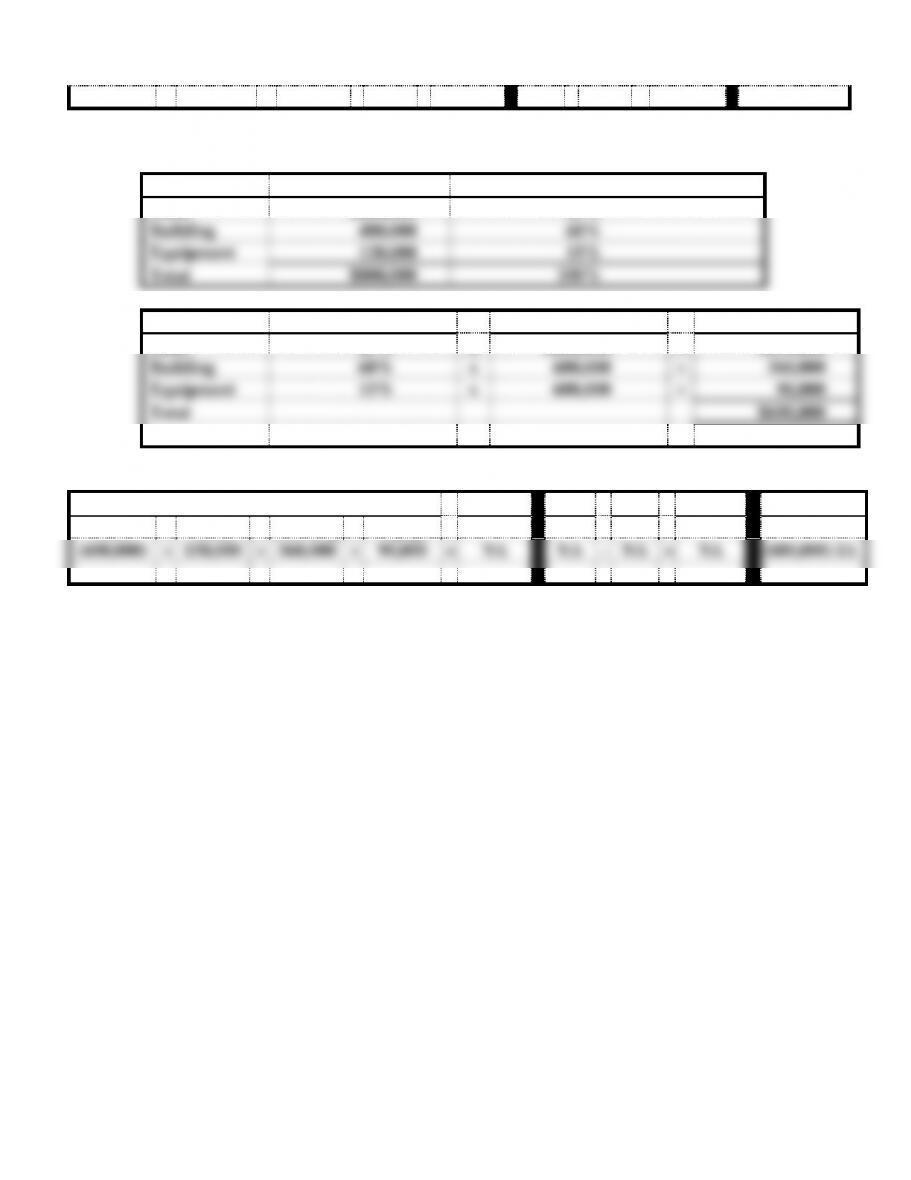

c. No, the historical cost concept requires that assets be recorded at the amount paid for them.

d.

Balance Sheet

Income Statement

Statemt. of

Assets

=

Liab.

+

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

Cash

+

Land

+

Bldg.

=

+

(800,000)

+

240,000

+

560,000

=

NA

+

NA

NA

−

NA

=

NA

(800,000) IA

6-7

EXERCISE 6-6

a.

Asset

Appraised Value

Percent of Appraised Value

Land

$200,000

25%

Building

480,000

60%

Equipment

120,000

15%

Total

$800,000

100%

Asset

% of App. Value

Purchase Price

Allocated Cost

Land

25%

x

$600,000

=

$150,000

Building

60%

x

600,000

=

360,000

Equipment

15%

x

600,000

=

90,000

Total

$600,000

b.

Assets

=

Equity

Rev.

−

Exp.

=

Net. Inc.

Cash Flow

Cash

+

Land

+

Building

+

Equip.

=

(600,000)

+

150,000

+

360,000

+

90,000

=

NA

NA

−

NA

=

NA

(600,000) IA

6-8

EXERCISE 6-7

a.

Balance Sheet

Income Statement

Statemt. of

Assets

=

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

Event

Cash

+

Equip.

−

A. Depr.

=

Com.

Stock

+

Ret.

Earn.

1.

20,000

NA

NA

20,000

NA

NA

NA

NA

20,000 FA

2.

(20,000)

20,000

NA

NA

NA

NA

NA

NA

(20,000) IA

3.

36,000

NA

NA

NA

36,000

36,000

NA

36,000

36,000 OA

4.

(21,000)

NA

NA

NA

(21,000)

NA

21,000

(21,000)

(21,000) OA

5.

(6,000)

NA

NA

NA

(6,000)

NA

6,000

(6,000)

(6,000) OA

6.

NA

NA

3,0001

NA

(3,000)

NA

3,000

3,000)

NA

Bal.

9,000

+

20,000

−

3,000

=

20,000

+

6,000

36,000

30,000

6,000

9,000 NC

1(Cost − Salvage value) ÷ useful life = Depreciation expense per year

$20,000 − $5,000 = $15,000; $15,000 ÷ 5 = $3,000 per year

b. $3,000

d. No; depreciation expense is a non-cash activity.

6-9

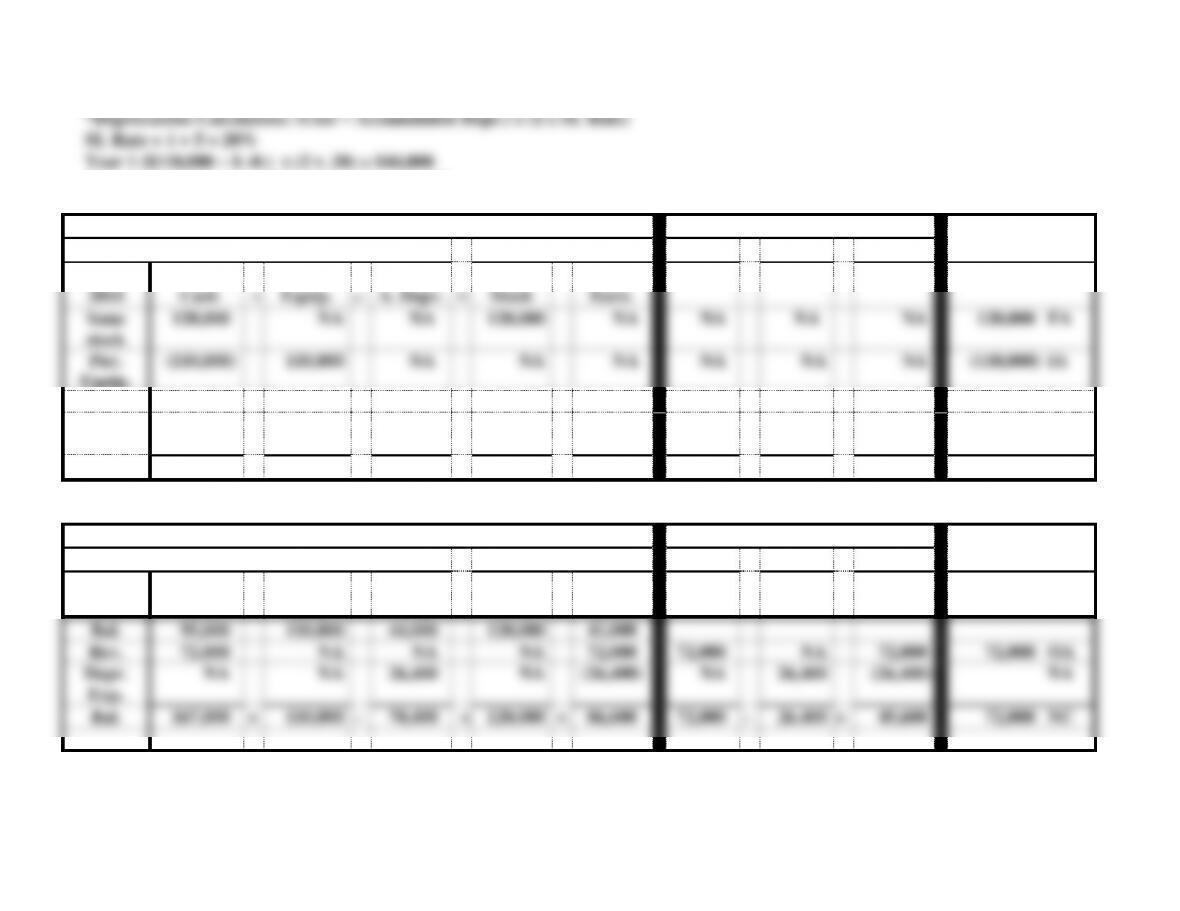

EXERCISE 6-

Year 2 ($110,000 − $44,000) x (2 x .20) = $26,400

a.

Balance Sheet

Income Statement

Statemt. of

Assets

=

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

Event

2014

Cash

+

Equip.

−

A. Depr.

=

Com.

Stock

+

Ret.

Earn.

Issue

stock

120,000

NA

NA

120,000

NA

NA

NA

NA

120,000 FA

Pur.

Equip.

(110,000)

110,000

NA

NA

NA

NA

NA

NA

(110,000) IA

Rev.

85,000

NA

NA

NA

85,000

85,000

NA

85,000

85,000 OA

Depr.

Exp.

NA

NA

44,000

NA

(44,000)

NA

44,000

(44,000)

NA

Bal.

95,000

+

110,000

−

44,000

=

120,000

+

41,000

85,000

44,000

41,000

95,000 NC

Balance Sheet

Income Statement

Statemt. of

Assets

=

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

Event

2015

Cash

+

Equip.

−

A. Depr.

=

Com.

Stock

+

Ret.

Earn.

Bal.

95,000

110,000

44,000

120,000

41,000

Rev.

72,000

NA

NA

NA

72,000

72,000

NA

72,000

72,000 OA

Depr.

Exp.

NA

NA

26,400

NA

(26,400)

NA

26,400

(26,400)

NA

Bal.

167,000

+

110,000

−

70,400

=

120,000

+

86,600

72,000

−

26,400

=

45,600

72,000 NC

6-10

EXERCISE 6-8 (cont.)

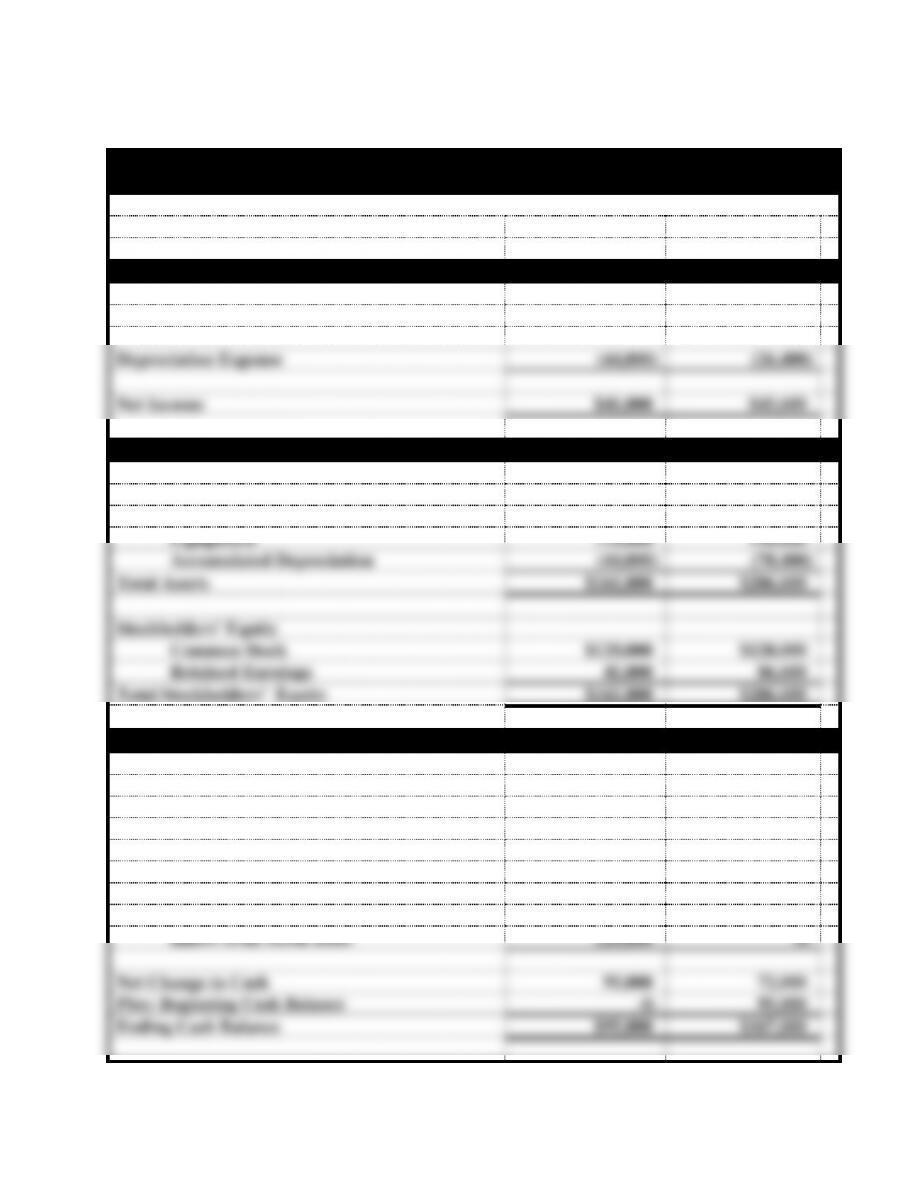

Posey Company

Financial Statements

2014

2015

Income Statements for the Year Ended December 31

Service Revenue

$85,000

$72,000

Depreciation Expense

(44,000)

(26,400)

Net Income

$41,000

$45,600

Balance Sheets as of December 31

Assets

Cash

$ 95,000

$167,000

Equipment

110,000

110,000

Accumulated Depreciation

(44,000)

(70,400)

Total Assets

$161,000

$206,600

Stockholders’ Equity

Common Stock

$120,000

$120,000

Retained Earnings

41,000

86,600

Total Stockholders’ Equity

$161,000

$206,600

Statements of Cash Flows for the Year Ended December 31

Cash Flows From Operating Activities:

Inflow from Customers

$85,000

$ 72,000

Cash Flows From Investing Activities:

Outflow to Purchase Equipment

(110,000)

-0-

Cash Flows From Financing Activities:

Inflow from Stock Issue

120,000

-0-

Net Change in Cash

95,000

72,000

Plus: Beginning Cash Balance

-0-

95,000

Ending Cash Balance

$95,000

$167,000

6-11

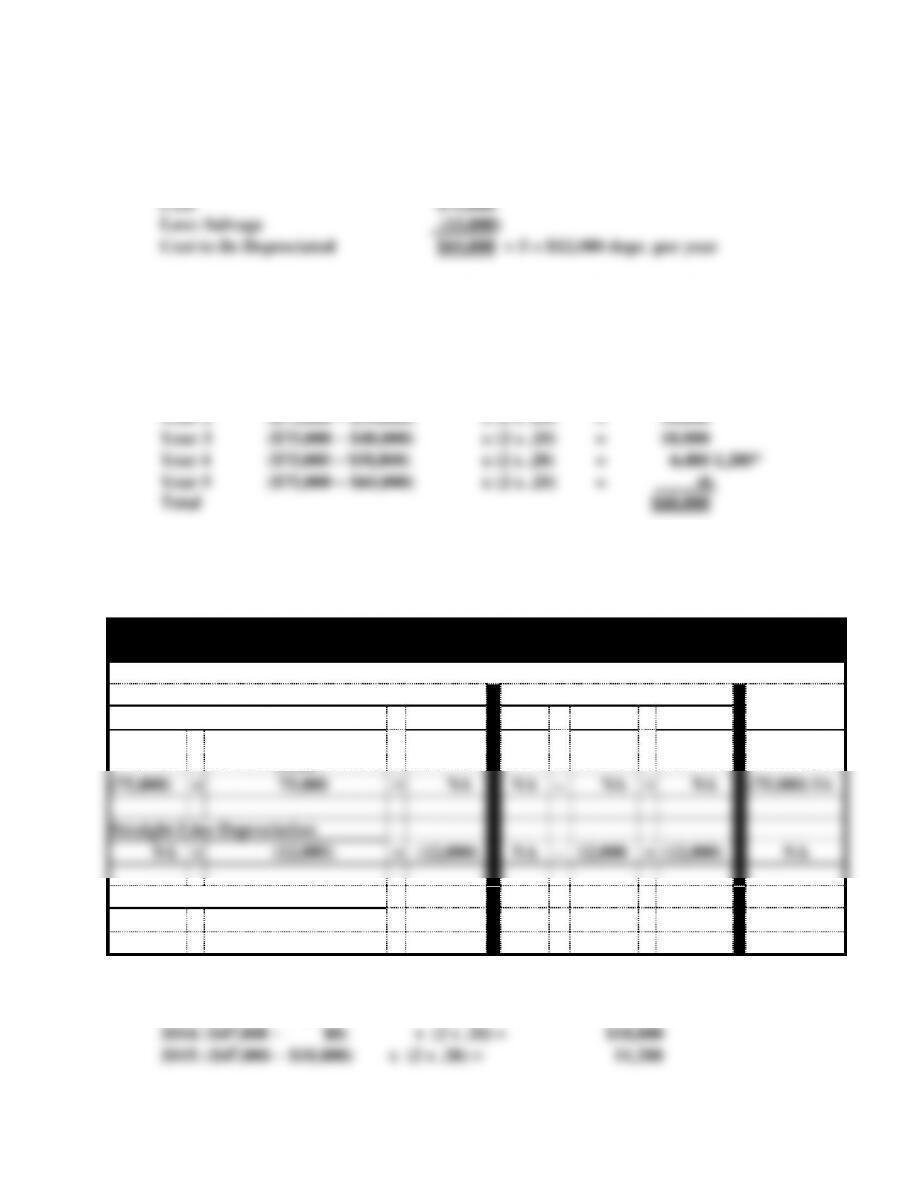

EXERCISE 6-9

a.

1. Straight-Line Calculation:

2. Double-Declining Balance Calculation:

(Cost − Accumulated Depreciation) x (2 x Straight-Line Rate)

Straight-Line Rate = 1 5 = .20

Year 1 ($75,000 − $0) x (2 x .20) = $30,000

*Since the total depreciable cost is $60,000 ($75,000 − $15,000), the depreciation is

limited in Year 4 ($60,000 − $58,800).

b.

Metal Manufacturing

Statements Model

Balance Sheet

Income Statement

Stmt. of

Assets

=

Equity

Rev

−

Exp.

=

Net Inc.

Cash Flows

Cash

+

Book Value of Drill

Press

=

Ret. Ear.

(75,000)

+

75,000

=

NA

NA

−

NA

=

NA

(75,000) IA

Straight-Line Depreciation

NA

+

(12,000)

=

(12,000)

NA

−

12,000

=

(12,000)

NA

DDB Depreciation

NA

+

(30,000)

=

(30,000)

NA

−

30,000

=

(30,000)

NA

EXERCISE 6-10 Double-Declining Balance

(Cost − Accum. Depr.) x (2 x SL Rate) = Depr. Exp. Per Year

SL Rate = 1 5 = .20