Chapter 12 Cost Accumulation, Tracing, and Allocation

12-1

a.

1. Product

2. Fixed

3. Indirect

b. Based on “actual” costs and actual production levels for each month independently,

the cost per unit for February and March would be:

February

March

Total Cost

(a)

$4,375,000

$4,375,000

Units Produced

(b)

140,000

120,000

Cost Per Unit

(a ÷ b)

$31.25

$36.46

c. If HealthSouth expected its annual depreciation cost to be $53,000,000 and its annual

service level to be 1,650,000 patient-days of service, its predetermined cost for

depreciation would have been $32.12 ($53,000,000 ÷ 1,650,000). If HealthSouth used a

d. Based on actual depreciation costs and actual service level for the entire year, the

depreciation per patient-day of service would be:

$52,500,000 ÷ 1,597,779 patient-day of service

= $32.86 per patient-day of service.

expected.ATC 12-2

a. Since the accounting and marketing departments are larger than the management

department, they will benefit from an allocation base that divides the cost equally

b. It is in the self-interest of each department to minimize the amount of the overhead

cost allocation. By minimizing total cost, operating income will be maximized, and

the department will thereby receive the largest amount of discretionary funding. The

Chapter 12 Cost Accumulation, Tracing, and Allocation

12-2

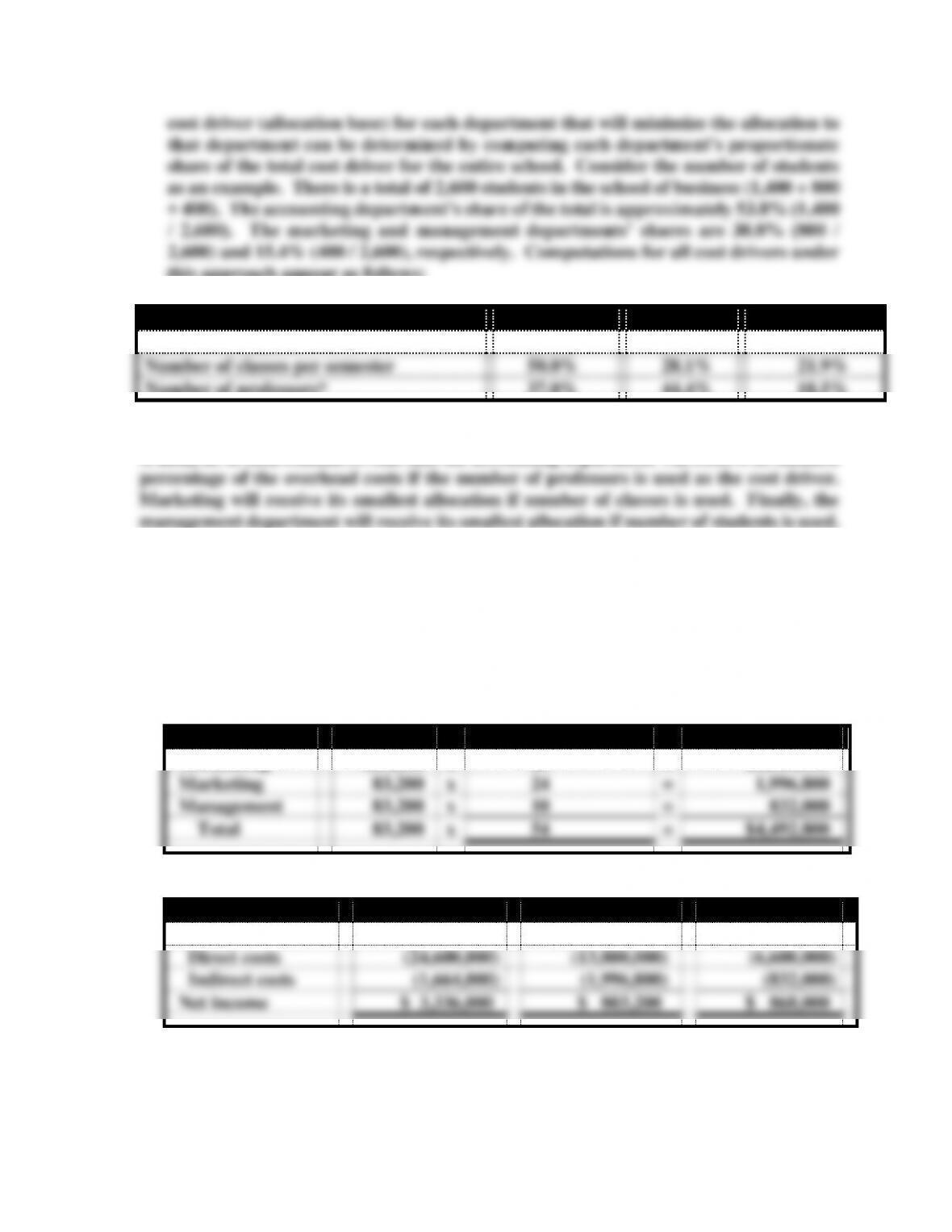

this approach appear as follows:

Cost Driver

Accounting

Marketing

Management

Number of students

53.8%

30.8%

15.4%

Number of classes per semester

50.0%

28.1%

21.9%

Number of professors*

37.0%

44.4%

18.5%

*The percentages do not add up to 100% because of rounding error.

A analysis of each column reveals that the accounting department will receive its smallest

ATC 12-2 (continued)

c. The groups in the section representing the accounting department should base their

allocation on number of professors. The following allocation results:

Allocation rate : Cost to be allocated / Cost driver = Allocation rate

$4,492,800 / 54 =$83,200 per professor

Department

Rate

x

No. of Professors

=

Allocated Cost

Accounting

$83,200

x

20

=

$1,664,000

Marketing

83,200

x

24

=

1,996,800

Management

83,200

x

10

=

832,000

Total

83,200

x

54

=

$4,492,800

Income Statements

Accounting

Marketing

Management

Revenue

$29,600,000

$16,600,000

$8,300,000

Direct costs

(24,600,000)

(13,800,000)

(6,600,000)

Indirect costs

(1,664,000)

(1,996,800)

(832,000)

Net income

$ 3,336,000

$ 803,200

$ 868,000

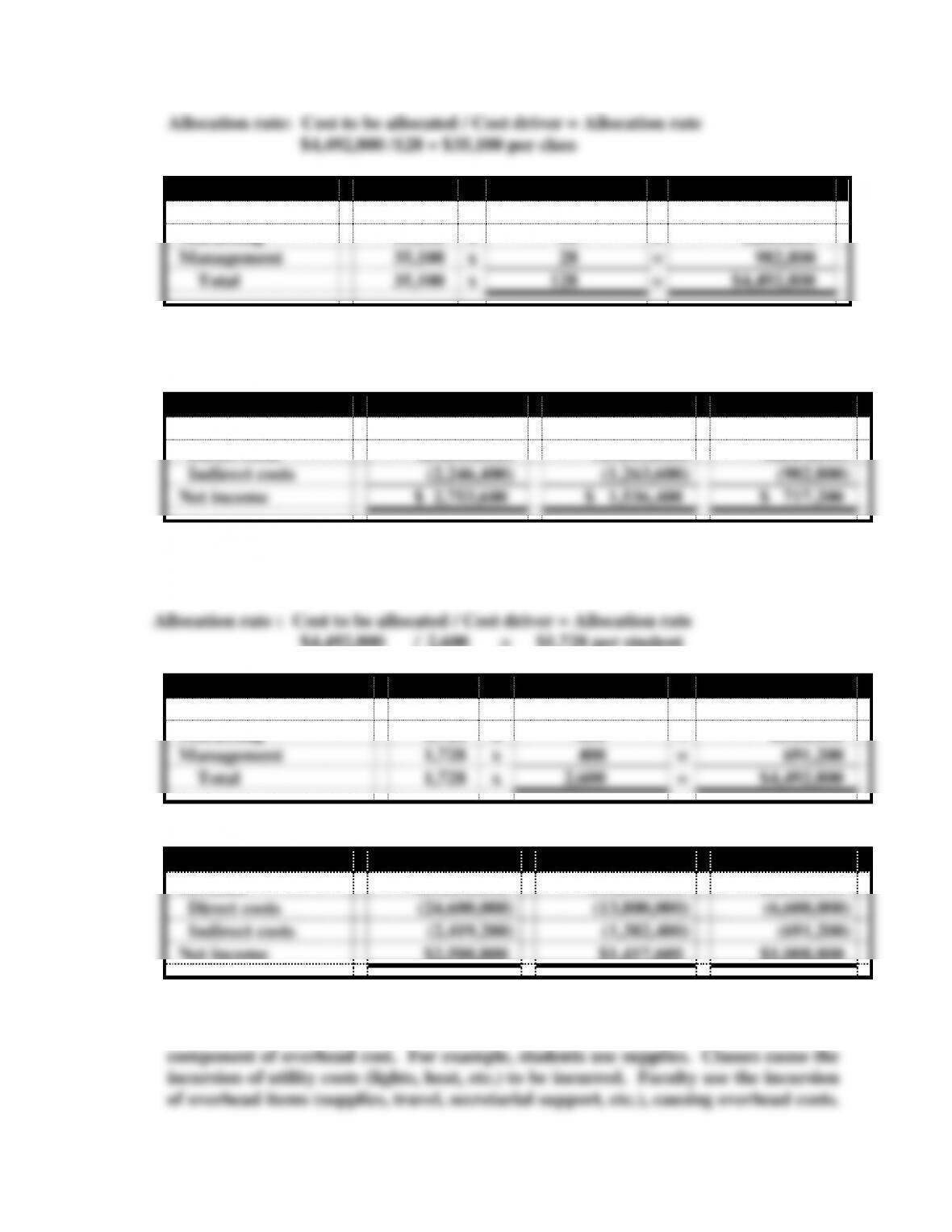

The groups in the section representing the marketing department should base their

allocation on number of classes per semester. The following allocation results:

Chapter 12 Cost Accumulation, Tracing, and Allocation

12-3

Department

Rate

x

No. of Classes

=

Allocated Cost

Accounting

$35,100

x

64

=

$2,246,400

Marketing

35,100

x

36

=

1,263,600

Management

35,100

x

28

=

982,800

Total

35,100

x

128

=

$4,492,800

ATC 12-2 (continued)

Income Statements

Accounting

Marketing

Management

Revenue

$29,600,000

$16,600,000

$8,300,000

Direct costs

(24,600,000)

(13,800,000)

(6,600,000)

Indirect costs

(2,246,400)

(1,263,600)

(982,800)

Net income

$ 2,753,600

$ 1,536,400

$ 717,200

The groups in the section representing the management department should base their

allocation on number of students. The following allocation should result:

Allocation rate : Cost to be allocated / Cost driver = Allocation rate

$4,492,800 / 2,600 = $1,728 per student

Department

Rate

x

No. Students

=

Allocated Cost

Accounting

$1,728

x

1,400

=

$2,419,200

Marketing

1,728

x

800

=

1,382,400

Management

1,728

x

400

=

691,200

Total

1,728

x

2,600

=

$4,492,800

Income Statements

Accounting

Marketing

Management

Revenue

$29,600,000

$16,600,000

$8,300,000

Direct costs

(24,600,000)

(13,800,000)

(6,600,000)

Indirect costs

(2,419,200)

(1,382,400)

(691,200)

Net income

$2,580,800

$1,417,600

$1,008,800

d. Many rational arguments are possible for each scenario. However, each argument

should establish a logical link between the allocation base and some identifiable

Chapter 12 Cost Accumulation, Tracing, and Allocation

12-4

ATC 12-3

a. Item 2 explains that shipping and handling costs are included within “costs of goods

sold.” Thus, these costs are not included in manufacturing costs. Some companies do

b. A good cost driver would be the weight of the products shipped. If individual products

were of approximately the same weight, i.e., a bottle of Dr. Pepper weighs the same as

c. In order to avoid unreasonable fluctuations in the cost per unit of beverages resulting

d. Soft drinks are a somewhat seasonal product; that is, customers drink more soft drinks

ATC 12-4

Each memo will be unique. Even so, the student should take the position that the current

cost driver (number of units) is an appropriate allocation base. The most appropriate cost

driver is the one that reflects the factors that cause overhead to be incurred. In the case of

ATC 12-5

a. The answer to the question as to “Who should pay?” is a matter of opinion.

b. Allocation could be used to spread the cost of disability services evenly over all courses.

For example, this cost could be treated as any other overhead cost. It would add $240

Chapter 12 Cost Accumulation, Tracing, and Allocation

12-5